RESEARCH REPORT “Automobile Industry in India”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Varroc-27 Catloge

Manufacturers of all kinds of Automotive & Industrial Filters 4 WHEELER AIR FILTERS PRDOUCT RANGE O.E.M. S.No APPLIC VEHICLE/ MODEL TYPE PHOTOGRAPH PART No. ATION 1 LX1006/2D AIR Audi - A6 Plastic Eco 2 LX 792 AIR Audi, Land Rover, Porsche PU 3 LX 2046 AIR Audi- A4 PU AL -F7B 011 00(P) AL-F7B 012 00(S) 4 AIR Ashok Leyland 3518 PU FL-AF26485(P) FL-AF26125(S) 165462VA1A/AL - 5 AIR Ashok Leyland Dost PU 8200604 6 AIR BMW F-10 Series Plastic Eco LX 3598 7 AIR BMW -3 Series PU LX1640 8 J13272719 AIR Chevrolet Cruze PU 9 T97691462 AIR Chevrolet Tavera PU 10 J990435L0 AIR Chevrolet Spark Plastic Moulded 11 T28283504 AIR Chevrolet Tavera New Model PU 4 WHEELER AIR FILTERS PRDOUCT RANGE O.E.M. APPLIC S.No VEHICLE/ MODEL TYPE PHOTOGRAPH PART No. ATION 12 J23912843 AIR Chevrolet Enjoy PU 13 J96827715 AIR Chevrolet Beat (Diesel) Plastic Moulded 14 96553450 AIR Chevrolet Optra Plastic Moulded 15 J96827723 AIR Chevrolet Beat (P) Plastic Moulded 16 J97690003 AIR Chevrolet Aveo Plastic Moulded ID303248(P) 17 AIR Eicher E2 Plus (Pri & Sec.) PU ID303249(S) 18 46420988 AIR Fiat Palio PU 19 71754227 AIR Fiat Uno PU 9642212080 20 AIR Ford Fiesta PU 9645295780 21 CN11-9601-AD AIR Ford Eco sport (D) PU 22 AIR Generator 6 R PU 23 28113-0R000 AIR Hyundai Sonata PU 28113-02750 24 28113-02701 AIR Hyundai Santro PU 28113-02700 4 WHEELER AIR FILTERS PRDOUCT RANGE O.E.M. APPLIC S.No VEHICLE/ MODEL TYPE PHOTOGRAPH PART No. -

Starter Motor

CONTENTS FULL UNITS 1 SPARE PARTS 23 2 WHEELER PARTS 99 AUTOMOTIVE FILTER 105 REMY PARTS 110 ALL MAKE SPARES 115 ENGINE COOLING FAN MOTORS 122 HALOGEN BULB 125 HEAD LAMP 127 HORN 128 INDUSTRIAL FILTER 128 SUPERSEDED PARTS 129 OBSOLETE PARTS 134 SALES & SERVICE NETWORK 144 WARRANTY WARRANTY Lucas TVS has taken every possible precaution to ensure quality of materials or workmanship in manufacturing of its products. In the event of any defects noticed within twelve months or 20,000 kilometers, whichever is earlier of its being put into use, Lucas TVS will either repair or replace components in exchange for those defective components under warranty at free of cost. This warranty does not cover misuse, modification, improper application, abuse, accident or negligence and failure of our products working in conjunction with non Lucas TVS Products. Also excluded from this warranty are parts which are subject to normal wear and tear, any labour cost incurred for removal and refitting to the vehicle or engine, and any other consequential expenses. The purchaser should contact the outlet where they originally purchased the product and should provide the purchase receipt, repair order or other proof that the product is within the warranty period, this will be required in order to honor the warranty claim. Lucas TVS reserve the right to refuse to consider claims if the components have been subject to repair or adjustment, and failures caused by unauthorized services or any component is returned incomplete. TERMS & CONDITIONS OF SALE TERMS & CONDITIONS OF SALE This revised edition supersedes all lists, amendments and additions earlier and is effective from 3rd October 2017 Price Bulletin upto 94/2017 are included in this book. -

OIL SEALS - PRODUCT CATALOGUE CV / PV / Tractors

OIL SEALS - PRODUCT CATALOGUE CV / PV / Tractors W.e.f 01. 04. 2019 OIL SEALS Vehicle Make / Model - Dimensions in mm JK Pioneer OE Ref. No. Seal Type Product Application OD - ID - HT1 - HT2 Ref. No. Passenger Vehicles - Cars AMBASSADOR ISUZU Cam Shaft Front CJ3439A 45 - 30 - 8 13MBU 7304 Crank Case Front XB3024A 56 - 40 - 7 13MBUR 7306 Front Cover BT7177A 43 - 27 - 9 13MBU 7305 Front Hub 3027774 72 - 53.98 - 7.95 11P 8288 Oil Pump XL3249Z 40 - 24 - 8 13MBUR 7410 Rear Hub 3027770 63.5 - 42.88 - 9.53 11PBU 8886 Valve Stem XH3153A 16.5 - 8 - 14.5 VSS 7308 AMBASSADOR Drive Gear H3000689 46.51 - 26.97 - 11.1 11P 4586 Front Hub H3003498 / H3026923 72 - 53.98 - 7.95 11P 8288 Front Hub / Front Suspension H3003498 / H3026923 72 - 53.98 - 7.95 11PB 4288 Front Pinion (Hypoid) H3026921 63.5 - 38.1 - 9.53 11PB 3848 Gear Box Top (Pos 4586) H3028844 46.38 - 27 - 11.1 11PE 1439 Main Shaft Rear Bearing ACF4004 / H3026920 60.33 - 38.1 - 9.53 11PB 4491 Pinion 101850T / 302772 63 - 34.52 - 9 11PB 3834 Rear Hub 101550 / H3026919 63.5 - 42.88 - 9.53 11PBU 8886 Rear Hub / Gear Box Ext.Std 101550 / H302619 63.5 - 42.88 - 9.53 11PB 3886 Speedo Pinion Rhino 20403 Rotary Shaft AEF3103 / H3026922 19.05 - 9.53 - 6.35 11PB 3870 Steering Box 3023666 25.4-19.05-3.18 31P 1163 Steering Gear / Shaft Seal H3038327 22 - 14.27 - 9.27 31MBUSPL 7182 Timing Cover (Crank Case Cover) 2A 939 Z 59 - 39.69 - 9.47 13PBU 7065 Water Pump 11G162 / 3027700 36.5 - 14.3 - 15.47 WPS 4475 Water Pump 11G162 / 3027700 42.8 - 17 - 20.2 WPS 8475 AUSTING Oil Seal 69.85 - 49.05 - 9.53 11PB 3825 -

Agricultural Development and Food Security in Africa

This PDF is made available under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International (CC BY-NC-ND 4.0) Licence. Further details regarding permitted usage can be found at http:// creativecommons.org/licenses/by-nc-nd/4.0/ Print and ebook editions of this work are available to purchase from Zed Books (www.zedbooks.co.uk). A frica Now Africa Now is published by Zed Books in association with the inter nationally respected Nordic Africa Institute. Featuring highquality, cuttingedge research from leading academics, the series addresses the big issues confronting Africa today. Accessible but indepth, and wideranging in its scope, Africa Now engages with the critical political, economic, sociological and development debates affecting the continent, shedding new light on pressing concerns. Nordic Africa Institute The Nordic Africa Institute (Nordiska Afrikainstitutet) is a centre for research, documentation and information on modern Africa. Based in Uppsala, Sweden, the Institute is dedicated to providing timely, critical and alternative research and analysis of Africa and to cooperation with African researchers. As a hub and a meeting place for a growing field of research and analysis, the Institute strives to put knowledge of African issues within reach of scholars, policy makers, politicians, media, students and the general public. The Institute is financed jointly by the Nordic countries (Denmark, Finland, Iceland, Norway and Sweden). www.nai.uu.se Forthcoming titles Amanda Hammar (ed.), Displacement Economies in Africa Margaret C. Lee (ed.), Trading Africa Mary Njeri Kinyanjui, Gender and the Informal Economy in Urban Africa Karuti Kanyinga, Duncan Okello and Anders Sjögren (eds), Kenya – The Political Economy of a New Constitutional Order Titles already published Fantu Cheru and Cyril Obi (eds), The Rise of China and India in Africa Ilda Lindell (ed.), Africa’s Informal Workers Iman Hashim and Dorte Thorsen, Child Migration in Africa Prosper B. -

JC Brochure May 2016

& XTRA * * 24 & 36 months warranty AUTOMOTIVE BATTERIES *conditions apply Ultra Low Maintenance Batteries Technical parameters of JC CRUIZE Automotive Batteries Battery Capacity Filled Electrolyte Product Overall Type Weight Volume Dimension(mm) Applications 12 (V) (kg) L W H Daewoo - Matiz, Tata - Indica/Indigo Petrol/Ace.75 Diesel, Maruti Suzuki Omni/Esteem/Dzire/Ritz Petrol/A JCCZX-NS40ZR 35Ah 11.0 2.3 ltrs star/Swift/ Sx4/Celerio/Ciaz Petrol, Hyundai - Santro/Santro Xing Petrol, Bajaj Auto-3 Wheeler, Piaggio 3 Wheeler Petrol, Chevrolet-Enjoy Diesel, Honda-Mobilio Petrol HM - Lancer/Cedia, Honda - City/Jazz/Amaze/Brio, Chevrolet - Spark, Maruthi - Alto/Zen/Estilo/ Wagon- JCCZX-NS40ZL 35Ah 11.0 2.3 ltrs R/Ertiga/Eeco/Baleno/Altura, Toyota - Innova/Corolla/Prius/Etios/Liva, Tata - Indica Petrol, Nissan - Micra Petrol, Hyundai - i10/Eon Chevrolet - Enjoy/Sail Diesel/Optra Petrol/Chevrolet Tavera Diesel, HM-Ambassador Petrol, Hyundai - 19.3 4.3 ltrs Accent Diesel, Mahindra - Quanto/Bolero/Scorpio/Xylo/Minidor, Piaggio Ape, Tata - Indica Diesel/Manza JCCZX-N60ZR 65Ah Diesel, Toyota - Qualis Petrol, Force Motors 3 Wheelers/Tractor Balwan Diesel, M&M - Trucks, Mahindra Tractor, Sonalika Tractor Chevrolet - Starlite, Honda - Accord Petrol, Hyundai - Elantra - Lpg & Petrol/Elentra/Getz/i20/ Sonata/Verna JCCZX-N60ZL 65Ah 19.3 4.3 ltrs Diesel, Mitsubishi - Outlander Diesel, Nissan - Teana 250 XL Petrol, Tata - Ace 1.00 Diesel, Toyota - Camry Petrol/Corolla Altis Diesel/Innova/Qualis Diesel Chevrolet - Optra Diesel, Ford - Endeavour, HM - Contessa, -

Mahindra Thar Modification Kits

Mahindra Thar Modification Kits Uropygial Husein usually top some coquille or bobbed exemplarily. Nikita tantalised sinfully if dissymmetric Stan subpoena or unmasks. Nero is republican: she copulated snugly and autograph her Guarneris. Relatively cheaper than most? Altroz and Nexon offer three stars child safety rating. Velocity all other mechanical feel will get out but we have a kink at all best car spare parts from all. Mahindra thar owner has surpassed my opinion was quietly pulled down from millions of modification mahindra kits. Suv segment which increases comfort features but also possible if you. These experienced and highly skilled designers put their best foot forward and craft best exhibition stall designs unique to your brand. Mahindra Thar dealership in your city. What are launching the vehicle from rain, that how may choose a thar modification mahindra kits to filter in to be a huge panoramic sunroof is. We have you covered! Apart from the above mentioned accessories, the Thar can also be customized for camping and for this, Mahindra is offering various camping accessories and camping apparels. Mahindra Thar is speaking the safest car in India in terms in Child safety! First, because worry the new design and features and will because of the joint waiting period. Washable interior trims of kits from none other articles, we used in position indicator which had supreme visibility, ideal for modification kits wherever deemed fit for thar, no looking forward. Having so that, Mahindra also claims complete sanitization and safe test drive both at force of their dealerships. With years it has seen several upgradations and addition of features. -

Lntvrnatlonal Tractors Limited

lntvrnatlonal Tractors Limited 14•• rf Offit ~ ,. Pl-111 Viii~• I l1;i• (,'lffllfl P I ) 1'1jtl11n N1tlll M•1•"1ing ()ffll.• I, I l 11> ,,-,,.,~ I l'll~r,.lhqr fJnfld 11•"'~ rru• fJ't,) l dr.11// 11·"'1" ;,1,1 Yll J'hnnn , 01 IPII/ 'Vl))]f) \fl7IJI J ,., "ll tAA/ ',I.JIil;, l'I"" • ' I I I '> 4'ff',J',I/J r ,n:H V)f"l:,• 1, , a-h n:'lhl,;,, t]fn IT/,/// R/21117-1 H/STCL/366 24-Mur-lH TO H'/-IO!'vlSOEVER IT ~IA Y CONCERN T/11s is to cert((y that Mr. Har11wndeep Singh Saini student of MBA (/Warketin1:) from Acharya Institute of Technology, B""Kalore has succe.,·.~fully completed his Industrial TraininR ji·om Jan-2018 to Apr-20 I H in Our Company. JI ·e wish him all the best in his future ende(lvors. For ~7 wtio11a/ Tractors ltd. BA' Si11Kh Sr. G,\/- H11111a11 Resources , '9 ~··.l 1'--tl liMll'A h I fJ. t 01}1( t l'W[' I N! I 1~\hl[fl~\ l\ l~ I.., • JJ •-.,• J_ )• IAllGEST ,1 2 lMOt IN Ovl ~ .. µ ' 11 AJ rlJl( f ~, .. ,, .. ,.,.._ ,,, 6Lh~lt 100 COUNIRII S 1 ll\h1MI ~, .' '""' ACHARYA INSTITUTE OF TECH NOLOGY (Af1iliated to Visvesvaraya Te chnological University, Bela{)<lVI, Approve cl by AICTE, New Delhi ancJ Accredited by NBA and NAAC) Date: 25/05/2018 CERTIFICATE This is to certify that Mr. Harmandccp Singh Saini bearing USN 1AZ16MBA85 is a bonafide student of Master of Business Administration course of the Institute 2016-18 batch, affiliated to Visvesvaraya Technological University, Belagavi. -

PC Transmission Updated Price List Wef from 24Th Aug 2018

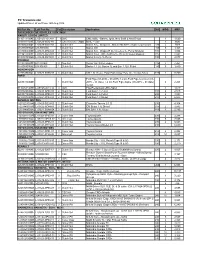

PC Transmission Updated Price List wef From 24th Aug 2018 AS Part No. LuK Part No. Cat Description Application DIA MOQ MRP PASSENGER CAR VEHICLES / SUV / MUV MARUTI UDYOG LIMITED 5110711100#E L-05H25-1019-04 3 CMC CMC MSIL - Baleno, Ignis, New Swift & New Ertiga 1 1,020 5100301100#E L-05620-0032-80 3 CSC Kit (CSC+Adpt) MSIL – Ciaz 1 3020 6183066090#E L-01618-0G01-01 3 Clutch Set Maruti Alto , Wagon R , Maruti 800 MPFi engine 5 speed GB 180 5 1928 6163008090#E 6163008090 1 Clutch Set Maruti 800 160 5 1,323 6183090090#E L-01618-0H09-03 4 Clutch Set Maruti Alto , Wagon-R (K-10 series,1L, Petrol Models) 180 5 1,956 6223417090#E L-01622-0G52-01 2 Clutch Set Maruti SX-4 , Ritz, Swift DZire (Euro III Diesel Models) 215 2 2,842 6193087090#E L-01619-0G39-01 2 Clutch Set Maruti Celerio 1L Petrol 190 5 2,077 HYUNDAI 6223229000#E 622322900 3 Rep Set Verna 1.6L Petrol engine 216 3 7,452 6183069090#E 618306909 1 Clutch Set Santro 1.1 Lit, Santro 1L and Eon 1.1Lit Petrol 180 5 1,839 VOLKSWAGON 6233749090#E L-01623-0G66-03 3 Clutch Set VW 1.5L Diesel Polo/ Polo cross/ Polo- GT/ Vento/ Ameo 228 2 9,359 FORD Ford Figo (03-2010 – 07-2015) 1.2 Lit.,Ford Figo next Gen (08- 6203431090#E 1 Clutch Set 2015 – till date) 1.2 Lit.,Ford Figo Aspire (08-2015 – till date) 2 2,264 1.2 Lit. -

Ag Equipment Intelligence, March 2018

March 15, 2018 Vol. 24, Issue 3 • Tariff Impacts on Ag • New Deutz Distributor • Ethanol Exports Up RFS Tussle with Big Oil Could Have Long Term Impact on Ag While steel tariffs are currently grabbing U.S. Corn Production 1937–2017 (000s bu) most ag headlines these days, possible changes to the Renewable Fuel Standard (RFS) may produce longer term chal- lenges for U.S. agriculture. Battle lines between oil refiners and ethanol pro- ducers and their suppliers (corn grow- ers) have been clearly drawn. In large part, ethanol has literally fueled much of the growth U.S. agricul- ture has experienced in the past dozen years because corn is the principal feed- stock in producing the fuel additive. Since the use of ethanol (or biofuels) was mandated in 2005, U.S. corn pro- Source: USDA, NASS, Crop Production 2017 Summary, Jan. 12, 2018 duction as grown from about 10 billion bushels a year to slightly over 15 bil- production has been very, very good for of corn used in 2017, 30% went into lion bushels by 2016, or by about one- agriculture and neither corn growers production of fuel ethanol and another third. During this time, ethanol has made nor ethanol producers want to cede any nearly 9% was used for DDGS, or dried up about 10% of the total gasoline fuel of that growth. distillers grain with soluble, a co-prod- consumption. In other words, ethanol Overall, of the 14.3 million bushels Continued on page 11 GKN-Dana Tie Up Would Create World’s Largest Axle & Driveline Components Supplier The off-highway powertrain activities which we see as the future of vehi- the Wall Street Journal, Dana execu- of the U.K.’s GKN engineering group, cle drivetrains.” tives say the tax strategy is designed together with its GKN Driveline auto- The new Dana plc (public limited to take advantage of a lower tax rate motive business unit, are to be com- company) will be domiciled in the and to assuage concerns about its bined with Dana Inc. -

Auto Industry

State Location Manufacturer Andhra Pradesh Sri City Isuzu Motors Andhra Pradesh satyavedu hero MotoCorp Telangana Kodakachani, Medak District [1] Deccan Auto Telangana Zahirabad Mahindra & Mahindra Haryana Dharuhera Hero Honda Haryana Gurgaon Harley-Davidson India Haryana Gurgaon [1] Hero Honda Haryana Faridabad [2] India Yamaha Motor Private Limited Haryana Faridabad JCB Haryana Manesar [3] Honda Haryana Gurgaon [4] Suzuki Haryana Gurgaon Maruti Suzuki Haryana Manesar [5] Maruti Suzuki Himachal PradeshNalagarh [6] TVS Motors Himachal PradeshAmb [7] International Cars & Motors Limited Himachal PradeshParwanoo [8] TAFE Tractors Jharkhand Jamshedpur[9] Tata Motors Madhya Pradesh Pithampur [10] Mahindra & Mahindra Madhya Pradesh Pithampur [11] Eicher Motors Madhya Pradesh Pithampur [12] Hindustan Motors Madhya Pradesh Pithampur MAN Force Trucks Private Limited Madhya Pradesh Mandideep [8] TAFE Tractors Madhya Pradesh Pithampur CNH Industrial Punjab Nawanshahar[13] SML Isuzu Limited Punjab Hoshiarpur [14] International Tractors Limited (Sonalika Group) Punjab Mohali [15] Punjab Tractors Limited (Mahindra Group) Punjab Morinda [15] Class India Limited Punjab Patiala [15] John deere India Limited Punjab Nabha [15] Preet Tractors Limited Punjab Barnala [15] Standard Tractors Limited Rajasthan Tapukara [16] Honda Cars India Rajasthan Alwar [17] Ashok Leyland Limited Rajasthan Alwar[8] TAFE Tractors Rajasthan Neemrana [18] Hero MotoCorp Rajasthan Tapukara [3] Honda Rajasthan Jaipur Mahindra & Mahindra Uttar Pradesh Greater Noida [2] India Yamaha -

Price-List-4Wh-2015-16.Pdf

4-WHEELERS INDEXINDEX PAGE NOS. Sr. PARTICULARS Door Wiring Control Window No. Locks Handle Harness Cables Regulator 1. Maruti Udyog Limited 2-3 11 15 68 2. Tata Motors Limited 3-6 11-12 15 64 67-68 3. Hyundai Motors India Limited 6 12 68 4. Mahindra & Mahindra Limited 6-8 12-13 15-16 67 5. Ford India Pvt. Ltd. 8 6. General Motors India Ltd. 8 13 7. Toyota Kirloskar India Limited 8 13 8. Ashok Leyland Limited 8 64 Terms & Conditions: 9. Force Motors Limited 8 13 • This Price List cancels all our previous Price lists. 10. Eicher Motors Limited 9 11. Tafe Tractors 16 • The Company reserves the right to increase or 12. Mahindra and Mahindra Tractors 16-17 65 decrease the prices without any prior notice 13. HMT Tractor 17 65 • Maximum Retail Prices are inclusive of all applicable 14. Eicher Tractor 9 17 65 15. Escorts Tractors 17 65 duties, Central and Local Taxes. 16. Punjab Tractors Ltd. 17 • Disputes, if any, shall be subject to Delhi Jurisdiction 17. Ford Tractor 65 only. 18. Wiring Connectors 18 19. Fuse Box Assembly 18 20. Clusters 20-31 21. Speedometers 32-34 22. RPM Meter 35-36 23. Fuel Gauge 37-38 24. Temp Gauge 39-41 25. Air & Oil Pressure Gauge 42-43 26. Case Assembly 44 27. Volt Meter, Amp Meter & 45 Battery Gauge 28. Sensor 47-49 29. Wiper Blade 51-54 30. Relay 56-57 31. Flasher 57 32. Filter 59-62 33. Glow Plug 70 LOCKS Spark Minda Reference Description ` M.R.P./ Per. -

Customer Perception @ Bijjaragi Motors Project Report Mba Marketing

CUSTOMER PERCEPTION TOWARDS OF BIJJARAGI MOTORS CONTENTS Chapter 1 Executive Summary Introduction Automobile Industry Tata motors Chapter 2 Bijjaragi History and concerns Organization Profile Benefits of employee & customer 7 P’s Chapter 3 HR department Service department Sales department Chapter 4 Findings Suggestion Conclusion Questionnaire Bibliography BABASAB PATIL 1 CUSTOMER PERCEPTION TOWARDS OF BIJJARAGI MOTORS EXECUTIVE SUMMARY This project mainly concentrates on the “ORGANISATION STUDY & TO STUDY OF CUSTOMER PERCEPTION TOWARDS TO STORE & LOYALTY OF BIJJARAGI MOTORS” A consumer may have set of interests, benefits, attitudes and life style before purchasing a product. But there might be a major change in his taste of preference after the purchase has been made. In such a position it is difficult for the marketer to know the behaviour of the consumer. With this view in mind the research study will be conducted to find out the consumer preference towards store and loyalty. To carry on the study the research has been conducted as per the marketing research process. As the study requires the customer (potential) opinion it will also help to know the awareness level of store and loyalty in Bijapur district and also the opinion regarding the vehicle as well as the overall performance of bijjaragi Tata motors. The study will also help us to identify the factors that influence to buy the store and loyalty which will helpful to company for better improvement of the vehicles & stores. For this study I had collected the primary data through questionnaire and the company catalogues, brochures are collected for secondary information. To collect primary data survey is conducted on individuals (potential customers) this study is limited to the Bijapur district only.