Institutional and Technological Change in Japan's Economy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Development of Japanese Industry and Business

REC6075 Development of Japanese Industry and Business Fall 2014 PROFESSOR: Yoshitaka Okada CLASS ROOM: CLASS HOURS: 6:00 pm – 9:10 pm on Wednesdays OFFICE HOURS: after the class on Wednesdays COURSE DESCRIPTION: How did Japanese business practices and industry develop from the Meiji Restoration (1868) to the present? How did government industrial and technology policies, industrial structures, industrial relations, and production technologies influence the development of industry and business practices? What is happening with these issues presently in Japan? This course tries to answer these questions by tracing historical changes and also studying some cases, including Toyota and the Japanese semiconductor industry. Class lectures will be based on the theoretical framework of institutional economics and economic sociology. COURSE REQUIREMENTS: 1. Reading Assignments: None. Key reference in each section is * marked in this syllabus with PDF files provided in the IUJ computer system. 2. Take-home Mid-term Examination Due: Week 7 Please pick one topic out of (a) Industrial Organization, (b) Government-Business Relations, and (c) Sogo Shosha (General Trading Companies), and answer the following questions, not exceeding 15 pages (double-space). (1) Please trace the historical transformation of your selected topic from the Pre-WWII period to the present. (40 pt.) (To answer this question, you need to take a good note of my lectures.) (2) Identify both persistent and changing characteristics. (20 pt.) (3) How do you explain the persistence and change? (20 pt.) (4) How can the topic you covered be applied to your own country? (20 pt.) 3. Paper: One term paper of 15-20 pages is required. -

Chapter 1. Relationships Between Japanese Economy and Land

Part I Developments in Land, Infrastructure, Transport and Tourism Administration that Underpin Japan’s Economic Growth ~ Strategic infrastructure management that brings about productivity revolution ~ Section 1 Japanese Economy and Its Surrounding Conditions I Relationships between Japanese Economy and Land, Chapter 1 Chapter 1 Infrastructure, Transport and Tourism Administration Relationships between Japanese Economy and Land, Infrastructure, Transport and Tourism Administration and Tourism Transport Relationships between Japanese Economy and Land, Infrastructure, Chapter 1, Relationships between Japanese Economy and Land, Infrastructure, Transport and Tourism Administration, on the assumption of discussions described in chapter 2 and following sections, looks at the significance of the effects infrastructure development has on economic growth with awareness of severe circumstances surrounding the Japanese economy from the perspective of history and statistical data. Section 1, Japanese Economy and Its Surrounding Conditions, provides an overview of an increasingly declining population, especially that of a productive-age population, to become a super aging society with an estimated aging rate of close to 40% in 2050, and a severe fiscal position due to rapidly growing, long-term outstanding debts and other circumstances. Section 2, Economic Trends and Infrastructure Development, looks at how infrastructure has supported peoples’ lives and the economy of the time by exploring economic growth and the history of infrastructure development (Edo period and post-war economic growth period). In international comparisons of the level of public investment, we describe the need to consider Japan’s poor land and severe natural environment, provide an overview of the stock effect of the infrastructure, and examine its impact on the infrastructure, productivity, and economic growth. -

Pictures of an Island Kingdom Depictions of Ryūkyū in Early Modern Japan

PICTURES OF AN ISLAND KINGDOM DEPICTIONS OF RYŪKYŪ IN EARLY MODERN JAPAN A THESIS SUBMITTED TO THE GRADUATE DIVISION OF THE UNIVERSITY OF HAWAI‘I AT MĀNOA IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS IN ART HISTORY MAY 2012 By Travis Seifman Thesis Committee: John Szostak, Chairperson Kate Lingley Paul Lavy Gregory Smits Table of Contents Introduction……………………………………………………………………………………… 1 Chapter I: Handscroll Paintings as Visual Record………………………………. 18 Chapter II: Illustrated Books and Popular Discourse…………………………. 33 Chapter III: Hokusai Ryūkyū Hakkei: A Case Study……………………………. 55 Conclusion………………………………………………………………………………………. 78 Appendix: Figures …………………………………………………………………………… 81 Works Cited ……………………………………………………………………………………. 106 ii Abstract This paper seeks to uncover early modern Japanese understandings of the Ryūkyū Kingdom through examination of popular publications, including illustrated books and woodblock prints, as well as handscroll paintings depicting Ryukyuan embassy processions within Japan. The objects examined include one such handscroll painting, several illustrated books from the Sakamaki-Hawley Collection, University of Hawaiʻi at Mānoa Library, and Hokusai Ryūkyū Hakkei, an 1832 series of eight landscape prints depicting sites in Okinawa. Drawing upon previous scholarship on the role of popular publishing in forming conceptions of “Japan” or of “national identity” at this time, a media discourse approach is employed to argue that such publications can serve as reliable indicators of understandings -

Classic Japanese Performance Cars Free

FREE CLASSIC JAPANESE PERFORMANCE CARS PDF Ben Hsu | 144 pages | 15 Oct 2013 | Cartech | 9781934709887 | English | North Branch, United States JDM Sport Classics - Japanese Classics | Classic Japanese Car Importers Not that it ever truly went away. But which one is the greatest? The motorsport-derived all-wheel drive system, dubbed ATTESA Advanced Total Traction Engineering System for All-Terrainuses computers and sensors to work out what the car is doing, and gave the Skyline some particularly special abilities — famously causing some rivalry at the Nurburgring with a few disgruntled Classic Japanese Performance Cars engineers…. The latest R35 GT-R, for the first time a stand-alone model, grew in size, complexity and ultimately speed. A mid-engined sports car from Honda was always going to be special, but the NSX went above and beyond. Honda managed to convince Ayrton Senna, who was at the time driving for McLaren Honda, to assess a late-stage prototype. Honda took what he said onboard, and when the NSX went on sale init was a hugely polished and capable machine. Later cars, especially the uber-desirable Type-R model, were Classic Japanese Performance Cars to perfection. So many Imprezasbut which one to choose? All of the turbocharged Subarusincluding the Legacy and even the bonkers Forrester STi, have got something inherently special to them. Other worthy models include the special edition RB5, as well as the Prodrive fettled P1. All will make you feel like a rally driver…. Mazda took all the best parts of the classic British sports car, and built them into a reliable and equally Classic Japanese Performance Cars package. -

Can the Sun Rise Again

A Background Paper for the AEA Session, January 5, 2004 December 19, 2003 The Heisei Recession: An Overview Koichi Hamada Yale University 1 © International Insolvency Institute – www.iiiglobal.org Abstract The prolonged recession in recent Japan continues much longer than a decade. One observes exciting policy-related discussions over the diagnosis and the effective prescriptions to the problem. Gradually, academic economists have been accumulating scientific investigations into the nature and the causes of this "great" recession. Economic theory faces a test of its applicability in the light of the novel situation, unobserved in the world economy at least after World War II, where the price is falling, the short-term interest approaches virtually the zero limit, and the demand for money is insatiable. This paper in an attempt to relate current policy debates to economic theory and some empirical results. The causes of this long recession certain include real factors such as the slowing down of the capacity growth, and difficulty of the adjustment of the Japanese institutions to changing environment. At the same time, one cannot neglect the effect of abrupt monetary contraction in the early 1990s, and resulting collapses of asset bubbles, which triggered the inefficacy of financial intermediation. However, since the most acute symptom of this recession is continuing recession, the first-hand remedies should be sought in monetary policy. The traditional interest policy or the policy to increase base money is limited. Purchase of long-term government bonds, and interventions in the exchange market are still effective policies to solve the situation. Moreover, inflation targeting or price-level targeting will be the most appropriate policy prescription in Japan where the liquidity trap persists because of a kind of liquidity trap. -

A Brief Summary of Japanese-Ainu Relations and the Depiction of The

The road from Ainu barbarian to Japanese primitive: A brief summary of Japanese-ainu relations in a historical perspective Noémi GODEFROY Centre d’Etudes Japonaises (CEJ) “Populations Japonaises” Research Group Proceedings from the 3rd Consortium for Asian and African Studies (CAAS) “Making a difference: representing/constructing the other in Asian/African Media, Cinema and languages”, 16-18 February 2012, published by OFIAS at the Tokyo University of Foreign Studies, p.201-212 Edward Saïd, in his ground-breaking work Orientalism, underlines that to represent the “Other” is to manipulate him. This has been an instrument of submission towards Asia during the age of European expansion, but the use of such a process is not confined to European domination. For centuries, the relationship between Japan and its northern neighbors, the Ainu, is based on economical domination and dependency. In this regard, the Ainu’s foreignness, impurity and “barbaric appearance” - their qualities as inferior “Others” - are emphasized in descriptive texts or by the regular staging of such diplomatic practices as “barbarian audiences”, thus highlighting the Japanese cultural and territorial superiority. But from 1868, the construction of the Meiji nation-state requires the assimilation and acculturation of the Ainu people. As Japan undergoes what Fukuzawa Yukichi refers to as the “opening to civilization” (文明開化 bunmei kaika) by learning from the West, it also plays the role of the civilizer towards the Ainu. The historical case study of the relationship between Japanese and Ainu from up to Meiji highlights the evolution of Japan’s own self-image and identity, from an emerging state, subduing barbarians, to newly unified state - whose ultramarine relations are inspired by a Chinese-inspired ethnocentrism and rejection of outside influence- during the Edo period, and finally to an aspiring nation-state, seeking to assert itself while avoiding colonization at Meiji. -

Economic Perspectives

The Journal of The Journal of Economic Perspectives Economic Perspectives The Journal of Fall 2016, Volume 30, Number 4 Economic Perspectives Symposia Immigration and Labor Markets Giovanni Peri, “Immigrants, Productivity, and Labor Markets” Christian Dustmann, Uta Schönberg, and Jan Stuhler, “The Impact of Immigration: Why Do Studies Reach Such Different Results?” Gordon Hanson and Craig McIntosh, “Is the Mediterranean the New Rio Grande? US and EU Immigration Pressures in the Long Run” Sari Pekkala Kerr, William Kerr, Çag˘lar Özden, and Christopher Parsons, “Global Talent Flows” A journal of the American Economic Association What is Happening in Game Theory? Larry Samuelson, “Game Theory in Economics and Beyond” Vincent P. Crawford, “New Directions for Modelling Strategic Behavior: 30, Number 4 Fall 2016 Volume Game-Theoretic Models of Communication, Coordination, and Cooperation in Economic Relationships” Drew Fudenberg and David K. Levine, “Whither Game Theory? Towards a Theory of Learning in Games” Articles Dave Donaldson and Adam Storeygard, “The View from Above: Applications of Satellite Data in Economics” Robert M. Townsend, “Village and Larger Economies: The Theory and Measurement of the Townsend Thai Project” Amanda Bayer and Cecilia Elena Rouse, “Diversity in the Economics Profession: A New Attack on an Old Problem” Recommendations for Further Reading Fall 2016 The American Economic Association The Journal of Correspondence relating to advertising, busi- Founded in 1885 ness matters, permission to quote, or change Economic Perspectives of address should be sent to the AEA business EXECUTIVE COMMITTEE office: [email protected]. Street ad- dress: American Economic Association, 2014 Elected Officers and Members A journal of the American Economic Association Broadway, Suite 305, Nashville, TN 37203. -

Australia and Japan

DRAFT Australia and Japan A New Economic Partnership in Asia A Report Prepared for Austrade by Peter Drysdale Crawford School of Economics and Government The Australian National University Tel +61 2 61255539 Fax +61 2 61250767 Email: [email protected] This report urges a paradigm shift in thinking about Australia’s economic relationship with Japan. The Japanese market is a market no longer confined to Japan itself. It is a huge international market generated by the activities of Japanese business and investors, especially via production networks in Asia. More than ever, Australian firms need to integrate more closely with these supply chains and networks in Asia. 1 Structure of the Report 1. Summary 3 2. Japan in Asia – Australia’s economic interest 5 3. Assets from the Australia-Japan relationship 9 4. Japan’s footprint in Asia 13 5. Opportunities for key sectors 22 6. Strategies for cooperation 32 Appendices 36 References 42 2 1. Summary Japan is the second largest economy in the world, measured in terms of current dollar purchasing power. It is Australia’s largest export market and, while it is a mature market with a slow rate of growth, the absolute size of the Japanese market is huge. These are common refrains in discussion of the Australia-Japan partnership over the last two decades or so. They make an important point. But they miss the main point about what has happened to Japan’s place in the world and its role in our region and what those changes mean for effective Australian engagement with the Japanese economy. -

This Sporting Life: Sports and Body Culture in Modern Japan William W

Yale University EliScholar – A Digital Platform for Scholarly Publishing at Yale CEAS Occasional Publication Series Council on East Asian Studies 2007 This Sporting Life: Sports and Body Culture in Modern Japan William W. Kelly Yale University Atsuo Sugimoto Kyoto University Follow this and additional works at: http://elischolar.library.yale.edu/ceas_publication_series Part of the Asian History Commons, Asian Studies Commons, Cultural History Commons, Japanese Studies Commons, Social and Cultural Anthropology Commons, and the Sports Studies Commons Recommended Citation Kelly, William W. and Sugimoto, Atsuo, "This Sporting Life: Sports and Body Culture in Modern Japan" (2007). CEAS Occasional Publication Series. Book 1. http://elischolar.library.yale.edu/ceas_publication_series/1 This Book is brought to you for free and open access by the Council on East Asian Studies at EliScholar – A Digital Platform for Scholarly Publishing at Yale. It has been accepted for inclusion in CEAS Occasional Publication Series by an authorized administrator of EliScholar – A Digital Platform for Scholarly Publishing at Yale. For more information, please contact [email protected]. This Sporting Life Sports and Body Culture in Modern Japan j u % g b Edited by William W. KELLY With SUGIMOTO Atsuo YALE CEAS OCCASIONAL PUBLICATIONS VOLUME 1 This Sporting Life Sports and Body Culture in Modern Japan yale ceas occasional publications volume 1 © 2007 Council on East Asian Studies, Yale University All rights reserved Printed in the United States of America No part of this book may be used or reproduced in any manner whatsoever without written permis- sion. No part of this book may be stored in a retrieval system or transmitted in any form or by any means including electronic electrostatic, magnetic tape, mechanical, photocopying, recording, or otherwise without the prior permission in writing of the publisher. -

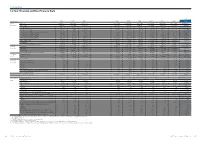

Corporate Data 10-Year Financial and Non-Financial Data

Corporate Data 10-Year Financial and Non-Financial Data (Millions of yen) (Fiscal year) 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 For the Net sales ¥1,858,574 ¥1,864,691 ¥1,685,529 ¥1,824,698 ¥1,886,894 ¥1,822,805 ¥1,695,864 ¥1,881,158 ¥1,971,869 ¥1,869,835 fiscal year Cost of sales 1,570,779 1,635,862 1,510,511 1,537,249 1,581,527 1,548,384 1,465,577 1,595,229 1,704,972 1,638,738 Operating income 124,550 60,555 11,234 114,548 119,460 68,445 9,749 88,913 48,282 9,863 Ordinary income (loss) 89,082 33,780 (18,146) 85,044 101,688 28,927 (19,103) 71,149 34,629 (8,079) Net income (loss) attributable to owners of the parent 52,939 (14,248) (26,976) 70,191 86,549 (21,556) (23,045) 63,188 35,940 (68,008) Cash flows from operating activities 177,795 39,486 45,401 194,294 153,078 97,933 141,716 190,832 67,136 27,040 Cash flows from investing activities (96,686) (85,267) (123,513) (62,105) (73,674) (104,618) (137,833) (161,598) (28,603) (218,986) Cash flows from financing activities (98,196) (40,233) 127,644 (138,501) (156,027) 93,883 16,545 (66,598) (9,561) 140,589 Capital expenditures 91,378 96,085 114,935 101,402 103,522 109,941 160,297 128,653 133,471 239,816 Depreciation 114,819 118,037 106,725 82,936 89,881 94,812 96,281 102,032 102,589 105,346 Research and development expenses 29,832 31,436 30,763 28,494 29,920 29,843 30,102 32,014 34,495 35,890 At fiscal Total assets 2,231,532 2,159,512 2,226,996 2,288,636 2,300,241 2,261,134 2,310,435 2,352,114 2,384,973 2,411,191 year-end Net assets 597,367 571,258 569,922 734,679 851,785 745,492 -

Corporate Governance Models: the Japanese Experience in Context

DePaul Business and Commercial Law Journal Volume 15 Issue 1 Fall 2016 Article 2 Corporate Governance Models: the Japanese Experience in Context Maria Lucia Passador Harvard University Follow this and additional works at: https://via.library.depaul.edu/bclj Recommended Citation 15 DePaul Bus. & Com. L.J. 25 This Article is brought to you for free and open access by the College of Law at Via Sapientiae. It has been accepted for inclusion in DePaul Business and Commercial Law Journal by an authorized editor of Via Sapientiae. For more information, please contact [email protected]. \\jciprod01\productn\D\DPB\15-1\DPB102.txt unknown Seq: 1 1-MAY-17 15:21 Corporate Governance Models: the Japanese Experience in Context Maria Lucia Passador* Avoid the crowd. Do your own thinking independently. Be the chess player, not the chess piece. —Ralph Charell INTRODUCTION: JAPANESE CORPORATE LAW AND ITS REFORM This Article aims to assess the claim that three countries – Italy, Japan and Portugal – present a tripartite,1 Latin, classic,2 and hybrid,3 model of corporate governance. In general, Japanese law seems an “exotic variation of Roman-Ger- manic models,” affected by United States legal models transplanted after World War II, while at the same time, presenting original fea- tures related to the history, evolution, and economic and social legacy of both Buddhist and Confucian philosophies.4 * PhD Candidate in Legal Studies - Business and Social Law, Bocconi University Law School, Milan, Italy; Visiting Researcher, Harvard Law School, Cambridge, MA, U.S.A. I am grateful to prof. Piergaetano Marchetti for his valuable, constant guidance and advice, and to prof. -

Several Observations on Capital Flows in Japan

Several observations on capital flows in Japan Richard Koo I am very happy to participate in the joint BIS/SAFE seminar on capital account liberalisation, since the subject of capital flows is one of those economic issues that I have covered very extensively in Japan over the last 19 years. In fact, this seminar has managed to invite two of the more experienced experts on Japanese capital flows, Professor Fukao and perhaps myself. Mr Fukao has covered quite a bit of the development in the 1970s and made a number of very valuable comments on what happened in the 1970s. My experience covering Japanese capital flows actually starts from the 1980s, first from the US side at the Federal Reserve Bank of New York, where we were following these inflows of Japanese money into US markets, after which I moved to Nomura Research Institute, the research arm of Nomura Securities, where all the capital account liberalisation action was taking place. Therefore, the focus of my discussion will be more on the developments of Japan’s capital flow liberalisation since the 1980s. There is an important difference between capital flows in the 1970s and those in the 1980s for Japan. One needs to distinguish the two types of financial flows: banking flows and portfolio flows. Banking flows would always be associated with international trade once an economy has opened its current account. Once portfolio flows are liberalised, they can prove very extended and they may not easily reverse. We all know from both academic literature and actual experience that the opening-up of an economy’s current account does help a lot in terms of economic growth, especially in terms of resource allocation.