Tranzrail A/R Front

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NZ TRANSPORT AGENCY NATIONAL OFFICE WAKA KOTAHI 50 Victoria Street Private Bag 6995 Wellington 6141 New Zealand T 64 4 894 5400 F 64 4 894 6100

NZ TRANSPORT AGENCY NATIONAL OFFICE WAKA KOTAHI 50 Victoria Street Private Bag 6995 Wellington 6141 New Zealand T 64 4 894 5400 F 64 4 894 6100 www.nzta.govt.nz 9 November 2015 Tony Randle [email protected] Dear Tony Request made under the Official Information Act 1982 Thank you for your email of 9 October 2015 requesting the following information under the Official Information Act 1982: a. the source document for the cost estimate of $2.3Million to be provided to the GWRC to "improve the Wairarapa Line" (although you stated it was actually for improving the Hutt Line). b. a description of the work that the $2.3Million was to support (I understand the GWRC claimed the funding is to "go toward replacing corroded rail and rolling out more powerful DFB diesel locomotives" but that NZTA is only funding track replacement). c. the funding memo notes that poor track causes an average loss of travel time of 10 minutes generates negative travel time benefits of approximately $5 million per annum, based on an average travel time value of $5 per hour (combined peak and off peak values), delay of ten minutes and 6,382,000 passenger trips on the Hutt Valley Line" for all commuters. A copy of the source that outlines the 10 minutes estimate for travel time loss currently affecting 6,382,000 passenger trips on the Hutt Valley Line that will be address by this funding investment to be provided. d. any meeting notes or correspondence associated with the $2,290,000 investment by the NZTA to the GWRC to "bring forward and substantially address the deferred maintenance" as outlined in the NZTA Memo. -

Wairarapa Train Services: Survey Results

Wairarapa train services: survey results Introduction Greater Wellington Regional Council carried out a survey of passengers on the north-bound Wairarapa trains on 22 June 2011 as part of the Wairarapa Public Transport Service Review. A total of 725 completed forms were returned. We would like to thank passengers and train-staff for your help with this survey. A summary of the results are shown below. The full survey report is available at www.gw.govt.nz/wairarapareview Where people live and how they get to the station About 25% of passengers live in each of Masterton, Carterton or Featherston. A further 13% of passengers live in Greytown and 6% in Martinborough. Sixty-eight percent of passengers travel to the station by car (57% parking their car at the station and 11% being dropped off). A further 23% of passengers walk or cycle to the station and 7% use the bus. Origin and destination The main boarding station in Wairarapa is Featherston (33%), followed by Masterton (28%), Carterton (25%) and Woodside (12%). Most passengers (85%) are going to Wellington, with the rest (15%) going to the Hutt Valley. Why people use the train, and purpose and frequency of travel The main reason people said they use the train is because it is cheaper than taking the car (56% of passengers) and a significant number also said it is quicker than driving (29% of passengers). Comfort (45% of passengers) and ability to work on the train (47% of passengers) were also important. Twenty-six percent of passengers also indicated that it’s environmentally responsible and 20% said they had no other transport option. -

Autumn 2017 Twuwheel

THE AUTUMN 2017 TWUWHEEL www.twuwa.org.au OFFICIAL PUBLICATION OF THE TRANSPORT WORKERS UNION (WA BRANCH) PH: 1800 657 477 STRONG AS EVER! Toll Ipec Members With Toll negotiations underway our overall aim is to change the transport industry for all workers including • Permanent Employees • Casuals • Owner Drivers • Labour Hire Workers vows State Secretary Tim Dawson Do you need a HR truck licence? We offer 1 or 2 day HR-B for $990* or lessons to suit your requirement Other transport essentials available Fatigue Management Certificate III Driver operations First Aid Load Restraint / Secure Cargo Implement Traffic Management Plan Forklift Call us today to discuss your requirements Unit 2 / 347 Great Eastern Hwy Fire Courses Redcliffe WA 6104 Supply Fire & First Aid equipment (08) 6180 -8065 / 0427 159 039 RTO 40599 Considering a career in Public Transport? With 13 depots across Perth and the SouthWest, there is sure to be one near you. Contact 9247 7500 or download an application form at www.swantransit.com.au Published by Perth Advertising Services. Phone: 9375 1922. Fax: 9275 2955. RATECUTTING RIFE! system to tackle the root causes of ‘Things have never many truck crashes. Instead, pressure is increasing on drivers to speed, drive long hours and been this bad for skip their mandatory rest breaks. The Turnbull Government’s own report showed the RSRT would have cut truck owner drivers’ crashes by 28% and yet it went ahead claims TIM DAWSON and tore it down. It is clearly willing to play politics with people’s lives. Throughout the transport industry the highest for any industry, according hundreds of owner-drivers are either to Safe Work Australia. -

Rail Network Investment Programme

RAIL NETWORK INVESTMENT PROGRAMME JUNE 2021 Cover: Renewing aged rail and turnouts is part of maintaining the network. This page: Upgrade work on the commuter networks is an important part of the investment programme. 2 | RAIL NETWORK INVESTMENT PROGRAMME CONTENTS 1. Foreword 4 2. Introduction and approval 5 • Rail Network Investment Programme at a glance 3. Strategic context 8 4. The national rail network today 12 5. Planning and prioritising investment 18 6. Investment – national freight and tourism network 24 7. Investment – Auckland and Wellington metro 40 8. Other investments 48 9. Delivering on this programme 50 10. Measuring success 52 11. Investment programme schedules 56 RAIL NETWORK INVESTMENT PROGRAMME | 3 1. FOREWORD KiwiRail is pleased to present this This new investment approach marks a turning point that is crucial to securing the future of rail and unlocking its inaugural Rail Network Investment full potential. Programme. KiwiRail now has certainty about the projected role of rail Rail in New Zealand is on the cusp of in New Zealand’s future, and a commitment to provide an exciting new era. the funding needed to support that role. Rail has an increasingly important role to play in the This Rail Network Investment Programme (RNIP) sets out transport sector, helping commuters and products get the tranches of work to ensure the country has a reliable, where they need to go – in particular, linking workers resilient and safe rail network. with their workplaces in New Zealand’s biggest cities, and KiwiRail is excited about taking the next steps towards connecting the nation’s exporters to the world. -

Annual Report 2020 Contents Contents

ANNUAL REPORT 2020 CONTENTS CONTENTS About Us ..............................................................................4 ALC Members ......................................................................5 Message From ALC Chair, Philip Davies .............................6 Message From CEO, Kirk Coningham, OAM ......................8 Board Members ...................................................................12 Our Values ...........................................................................14 ALC Team Members ............................................................14 Committees .........................................................................15 Strategic Plan ......................................................................18 COVID-19 ............................................................................20 @AustLogistics Key Policy & Advocacy Achievements ................................22 Key Safety Achievements ....................................................24 linkedin.com/company/australian-logistics-council Appendix .............................................................................26 Policies ..........................................................................27 Suite 17B, National Press Club Building Submissions ..................................................................27 16 National Circuit, BARTON, ACT 2611 P: +61 2 6273 0755 Media Releases .............................................................28 E: [email protected] Financials .......................................................................30 -

Wellington Network Upgrade

WELLINGTON NETWORK UPGRADE Better rail services for the region. Around 500,000 Wellingtonians and visitors take over 14 million passenger journeys each year on our Metro Rail Network. KiwiRail, Greater Wellington Regional Council and Metlink are working together to modernise the rail, thanks to investment of almost $300 million from the Government to enable: Train services to be more reliable. More people and freight travelling on rail in the future. The Wellington Metro Upgrade Programme is being delivered on a busy, well-maintained but ageing network where trains run 18 hours a day. The focus of our work is: Renewing existing network infrastructure to improve rail services. Renewing traction power overhead line system and signals power supply, and improving the track across the network including inside the four major tunnels. Adding capacity to the network so more people can travel on trains in the future while still allowing for freight services. This includes: Double tracking between Trentham and Upper Hutt. Improvements to Wellington station approaches. Changes at Plimmerton. More information www.kiwirail.co.nz (Wellington Metro Upgrade) HUTT LINE DOUBLE TRACKING More frequent, reliable trains. The 2.7 kilometres of rail line between Trentham and Upper Hutt is being double tracked so trains can travel in both directions at the same time. This will allow more frequent and reliable services along this section of the busy line from Wellington to Upper Hutt and Wairarapa. Stations are being upgraded and we are making it safer around our tracks. Wairarapa Existing Upper Hutt Future Connecting new second track to the network Level crossing upgrade at Blenheim Street Wallaceville Closing pedestrian crossing just North of Wallaceville New platform with shelters will be built in the style of Ava’s (pictured). -

Rail Electrification and Extension from Papakura to Pukekohe Updates Glossary

Agenda Item 13 (iv) Rail Electrification and Extension from Papakura to Pukekohe Updates Glossary Auckland Council (AC) Auckland Electrified Area (AEA) Auckland Plan (AP) Auckland Transport (AT) Construcciones y Auxiliar de Ferrocarriles (CAF) Diesel Multiple Unit (DMU) Electric Multiple Unit (EMU) KiwiRail Group (KRG) New Zealand Transport Agency (NZTA) North Auckland Line (NAL) North Island Main Trunk Line (NIMT) Onehunga Branch Line (OBL) Regional Land Transport Programme (RLTP) Rapid Transit Network (RTN) Executive Summary Item 1: Auckland Rail Electrification Update AT and KRG are currently undertaking preparatory works for electrification of the Auckland Rail Network between Papakura and Swanson Stations, with the first EMU services being tested and commissioned from September 2013. The target is for EMU passenger services to be introduced from December 2013, initially on the OBL. The remainder of the EMU fleet will be introduced in stages until the full fleet is in service under current programme timelines in mid-2016. The electrification projects can be grouped as follows: a) Installation and commissioning of electrification infrastructure: overhead wires, gantries, earthing of stations, etc., primary responsibility with KRG. b) Station and depot infrastructure: preparation for electrification includes construction of an EMU depot at Wiri, upgrading of a number of existing stations to a common standard, construction of a new station at Parnell, ensuring sufficient stabling for the EMU fleet. Responsibility is primarily with AT; c) Procurement of new EMU fleet: Including operational transitioning from the existing DMU and diesel locomotives to the new EMUs. Responsibility rests with AT. d) Operational readiness for electrification: Training of staff, train drivers and contractors for working within an electrified environment, agreement on responsibility for maintaining electrification assets, agreement on safety provisions for public and contractors, communications with the public and other stakeholders. -

BUILDING a SUSTAINABLE FUTURE Redevelopments at Both Picton and Wellington Are Part of the Ferry Replacement Programme

STATEMENT OF CORPORATE INTENT 2022-2024 F.18a BUILDING A SUSTAINABLE FUTURE Redevelopments at both Picton and Wellington are part of the ferry replacement programme. Front cover: KiwiRail plays an important role in shi ing logs as New Zealand continues to move towards peak “Wall of Wood”. 2 KiwiRail Statement of Corporate Intent 2022-2024 CONTENTS OUR PURPOSE .....................................................................4 ENVIRONMENT AND SUSTAINABILITY ..........................22 INTRODUCTION ....................................................................6 HOW KIWIRAIL CREATES VALUE ...................................... 24 NATURE AND SCOPE ........................................................... 8 ASPIRATIONS AND OBJECTIVES ...................................... 26 COVID-19 STRATEGIC RESPONSE ...................................... 9 FINANCIAL CAPITAL ........................................................27 MARKET OUTLOOK AND ECONOMIC ASSUMPTIONS ...... 9 RELATIONSHIPS CAPITAL ............................................. 28 STRATEGIC PRIORITIES .....................................................11 ASSETS CAPITAL ............................................................ 29 FINANCIAL .....................................................................12 PEOPLE CAPITAL ............................................................31 RELATIONSHIPS ............................................................ 13 SKILLS AND KNOW-HOW CAPITAL ................................32 INVESTMENT IN ASSETS .............................................. -

The Colonial Reinvention of the Hei Tiki: Pounamu, Knowledge and Empire, 1860S-1940S

The Colonial Reinvention of the Hei Tiki: Pounamu, Knowledge and Empire, 1860s-1940s Kathryn Street A thesis submitted to Victoria University of Wellington in fulfilment of the requirements for the degree of Master of Arts in History Victoria University of Wellington Te Whare Wānanga o te Ūpoko o te Ika a Māui 2017 Abstract This thesis examines the reinvention of pounamu hei tiki between the 1860s and 1940s. It asks how colonial culture was shaped by engagement with pounamu and its analogous forms greenstone, nephrite, bowenite and jade. The study begins with the exploitation of Ngāi Tahu’s pounamu resource during the West Coast gold rush and concludes with post-World War II measures to prohibit greenstone exports. It establishes that industrially mass-produced pounamu hei tiki were available in New Zealand by 1901 and in Britain by 1903. It sheds new light on the little-known German influence on the commercial greenstone industry. The research demonstrates how Māori leaders maintained a degree of authority in the new Pākehā-dominated industry through patron-client relationships where they exercised creative control. The history also tells a deeper story of the making of colonial culture. The transformation of the greenstone industry created a cultural legacy greater than just the tangible objects of trade. Intangible meanings are also part of the heritage. The acts of making, selling, wearing, admiring, gifting, describing and imagining pieces of greenstone pounamu were expressions of culture in practice. Everyday objects can tell some of these stories and provide accounts of relationships and ways of knowing the world. The pounamu hei tiki speaks to this history because more than merely stone, it is a cultural object and idea. -

For Personal Use Only Use Personal For

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 F +61 3 9694 2880 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 19 August 2014 The Manager Auustralian Stock Exchange Company Announcement Office Level 4 20 Bridge Street Sydney NSW 2000 Lodged Through ASX On Line Total No. of Pages: 139 Dear Sir FULL YEAR RESULTS 30 JUNE 2014 – APPENDIX 4E Please find attached for immediate release to the market the following with regard the abovementioned subject: • Appendix 4E Preliminary Final Report For Year Ended 30 June 2014. Yours faithfully TOLL HOLDINGS LIMITED Bernard McInerney Company Secretary Encl. For personal use only TOLL HOLDINGS LIMITED AND ITS CONTROLLED ENTITIES Preliminary Final Report for the Year Ended 30 June 2014 ASX Appendix 4E Preliminary Final Report Name of entity Toll Holdings Limited ABN 25 006 592 089 Reporting period Year ended 30 June 2014 Previous corresponding period Year ended 30 June 2013 Results for announcement to the market 201 4 201 3 Change Change $M $M $M % Revenue 8,811.2 8,719.4 91.8 +1.1 EBIT pre individually significant items 444.4 425.9 18.5 +4.3 NPAT pre individually significant items 298.5 282.4 16.1 +5.7 Individually significant items (net of tax) (5.4) (190.7) 185.3 Net profit after tax 293.1 91.7 201.4 +219.6 Non-controlling interests (7.0) (7.2) 0.2 +2.8 NPAT attributable to shareholders 286.1 84.5 201.6 +238.6 Refer to attached Media Release for commentary on results. -

2001/02 Annual Plan Vol. I Submissions

2001/02 Annual Plan Vol. I Submissions 16 1 Annual Plan Submissions Note: Those submitters identified in bold type have expressed a desire to be heard in support of their submissions. 1. Norm Morgan Acquisition of TranzMetro, Kick start funding, Water integration, effectiveness of submission process 2. Steve Ritchie Bus service for Robson Street and McManaway Grove , Stokes Valley 3. Nicola Harvey Acquisition of TranzMetro, Kick start funding, Water integration, Marine conservation project for Lyall Bay 4. Alan Waller Rates increases, upgrade to Petone Railway Station 5. John Davis Acquisition of TranzMetro, Water integration, MMP for local government, Emergency management 6. Wellington City Council Floodplain management funding policy 7. Kapiti Coast Grey Power Annual Plan presentation, acquisition of TranzMetro, Kick Assn Inc start funding, rates, operating expenditure, financial management, land management, Parks and Forests, Investment in democracy, 8. John Mcalister Acquisition of TranzMetro, Kick Start funding, Water integration, water supply in the Wairarapa 9. Hutt 2000 Limited Installation of security cameras in Bunny Street Lower 16 Hutt 10. Walk Wellington Inclusion of walking in Regional Land Transport Strategy 11. Hugh Barr Acquisition of TranzMetro, Kick Start funding, Water integration, public access to Water collection areas 2 12. Porirua City Council Bulk Water levy, Transparency of Transport rate, support for Friends of Maara Roa, environmental management and Biodiversity 13. Keep Otaki Beautiful Otaki Bus Shelter 14. Barney Scully Cobham Drive Waterfront/Foreshore 15. Upper Hutt City Council Acquisition of TranzMetro, Water Integration, Hutt River Floodplain Management 16. Wairarapa Green Acquisition of TransMetro, Rick start funding, Issues Network environmental education, rail services, biodiversity 17. -

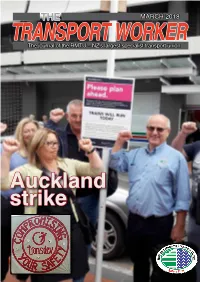

Auckland Strike

THE MARCH 2018 TRANSPORThe journal of the RMTU – NZ'sT largest WORKER specialist transport union Auckland strike 2 CONTENTS EDITORIAL ISSUE 1 • march 2018 "On page 14 there is reference to Saida Abad, WHOLE BODY VIBRATION the first female loco 7 engineer in Morocco. I found this billboard with her very moving quote whilst in London recently." Tana Umaga lends a hand to campaign to overcome WBV among LEs. Wayne Butson 10 HISTORIC FIRST General secretary RMTU The entire KiwiRail board made an historic first visit to Hutt workshops Is this the year the recently. MORROCAN CONFERENCE dog bites back? 14 ELCOME to the first issue ofThe Transport Worker magazine for 2018 which, as always, is packed full of just some of the things that your RMTU Union does in the course of its organising for members. delegate Last year ended with a change of Government which should Christine prove to be good news for RMTU members as the governing partners and their sup- Fisiihoi trav- portW partners all have policies which are strongly supportive of rail, ports and the elled all the transport logistics sectors. way to According to the Chinese calendar, 2018 is the year of the dog. However, in my Marrakech view, 2018 is going to be a year of considerable change for RMTU members. We have and was seen Transdev Auckland alter from being a reasonable employer who we have been blown away! doing business with since 2002 to one where dealing with most items has become combative and confrontational. Transdev Wellington is an employer with much less of a working history but we COVER PHOTOGRAPH: Auckland RMTU were able to work with them on the lead up to them taking over the Wellington members pledging solidarity outside Britomart Metro contract and yet, from almost the get go after they took over the running of Place.