Statement in Response to Inspectors Matters, Issues and Questions to Examination of Leeds Sap Matters & Issues (M7/141/2) Matter 7A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Birthday Parties

£95 for 30 people 30 for £95 £65 for 20 people 20 for £65 Prices head. Please ask for further details. further for ask Please head. supplied by Megabites of Rothwell, from £5 per per £5 from Rothwell, of Megabites by supplied If you wish we can provide food for your party, party, your for food provide can we wish you If new castings for old, missing and broken parts. broken and missing old, for castings new See our collection of historic patterns used to make make to used patterns historic of collection our See are available at the Moor Road shop. Road Moor the at available are Hot and cold drinks and confectionery confectionery and drinks cold and Hot and let the children have fun in the play area. play the in fun have children the let and food for consumption on the train or at Park Halt Halt Park at or train the on consumption for food have a go operating the model train model the operating go a have You are welcome to bring your own own your bring to welcome are You Relax in our cafe with a hot drink and a sandwich, a and drink hot a with cafe our in Relax See the inside of a boiler and learn how it works. it how learn and boiler a of inside the See of a steam locomotive steam a of locomotive and preparing it for your journey ahead. journey your for it preparing and locomotive Climb onto the footplate and learn the controls controls the learn and footplate the onto Climb Watch the crew undertake their duties, caring for the the for caring duties, their undertake crew the Watch Halt and Moor Road after each trip. -

Newsletter No. 74 Autumn 2008 Editorial

NEWSLETTER NO. 74 AUTUMN 2008 EDITORIAL Welcome to the latest Newsletter; I hope you have had an enjoyable summer in spite of the dreadful weather, Due to a clash of dates I was unable to attend this year’s AIA Conference which was held in Wiltshire and I look forward to reading the report which will appear in Industrial Archaeology News. I am also looking forward to the forthcoming 2008-2009 Lecture Programme; full details are given on the separate sheet, meeting as usual on Saturday mornings at Claremont. In the past the Section has considered whether midweek evening meetings or Saturday afternoons would attract more members to join and attend but the general view from those who have expressed it, is that Saturday mornings are preferred. However please note that the 2009 AGM will be starting earlier at 10.30am. This is because we will have another local walk in the afternoon starting at 2pm and starting the AGM half an hour earlier gives a little more time for members’ contributions and lunch. I am sure that you will agree with me that our Lecture Secretary, Jane Ellis, has yet again organised an interesting and varied programme and I hope many of you will be able to attend at least a few lectures during the season. Robert Vickers will also lead a walk around Huddersfield on Sunday 10 May 2009, meeting at the Railway Station at 11am with a pub lunch. Let’s hope there is better weather for this than his walk around Bradford, which is reported on later in the Newsletter. -

Leeds Economy Handbook Leeds Property Market

LEEDS ECONOMY HANDBOOK August 2016 LEEDS PROPERTY MARKET CONTENTS The Leeds property market Employment land PROPERTY INVESTMENT IN LEEDS: 2006‐2015 Counting only individual property schemes valued at £1m or over, £9.8bn worth of major developments have either been completed, are currently under construction or have been proposed in Leeds in the period 2006 to 2015. Of this total, almost £4.0bn has been completed; £695m are under construction and £5.1bn are proposed or currently on hold. Property schemes valued £1m or more, 2006‐2015, Leeds MD £m Completed Under Proposed/ TOTAL Construction On hold Major Mixed Use* 12 ‐ 1,400 1,412 Office Devts 728 254 1,437 2,419 Retail 572 174 20 765 Leisure 629 54 291 974 City Centre Apartments 924 16 981 1,921 Mfrg/Distribution 306 ‐ 277 583 Other 821 197 695 1,712 Total 3,992 695 5,101 9,786 * The data on office, retail, leisure and apartments is for stand‐alone schemes only. The mixed‐use developments can include significant elements of these. Source : Economic Development, Leeds City Council MAJOR SCHEMES During 2016, the Kirkgate Market refurb and 6 Wellington Place were completed. Currently under construction in the city centre are the hotel on Greek Street, Education campus on Hunslet Road, Ruth Gorse Academy, City House’ Hilton Leeds Arena hotel, Merrion House, 6 Queen Street, 3 Sovereign Square, Victoria Gate, 5 Wellington Place, Central Square on Wellington Street. Outside the city centre are the incinerator on Pontefract Lane and UTC on Hunslet Road. Three city centre schemes over £100m each are proposed or currently on hold: Latitude, Caddick development at Quarry Hill, Temple Quarter and Wellington Place. -

The Industrial Archaeology of West Yorkshire

The Industrial Archaeology of West Yorkshire Introduction: The impact of the Industrial Revolution came comparatively late to the West Yorkshire region. The seminal breakthroughs in technology that were made in a variety of industries (e.g. coal mining, textile, pottery, brick, and steam engine manufacture) during the 17th and 18th centuries, and the major production centres that initially grew up on the back of these innovations, were largely located elsewhere in the country. What distinguishes Yorkshire is the rate and density at which industry developed in the region from the end of the 18th century. This has been attributed to a wide variety of factors, including good natural resources and the character of the inhabitants! The portion of the West Riding north and west of Wakefield had become one of most heavily industrialised areas in the Britain by the end of the 19th century. It was also one of the most varied - there were some regional specialities, but at one time or another Yorkshire manufacturers supplied everything from artificial manure to motorcars. A list of local products for the 1890s would run into hundreds of items. Textile Manufacturing: The most prominent industry in the region has always been textile manufacture. There was a long tradition in the upland areas of the county of cloth production as a home-based industry, which supplemented farming. The scale of domestic production could hardly be considered negligible - the industry in Calderdale was after all so large that in 1779 it produced the Piece Hall in Halifax as an exchange centre and market. However, the beginnings of the factory system, and the birth of modern textile mills, dates to the introduction of mass-production techniques for carding and spinning cotton. -

A Perspective on Agile Working in Historic Buildings

A Perspective on Agile Working in Historic Buildings Prepared for: Historic England 1 By: RAMIDUS CONSULTING LIMITED Date: 6th April 2018 A Perspective on Agile Working in Historic Buildings Contents Page 1.0 Introduction 1 1.1 Buildings as responsive environments 2.0 New economy, new work 3 2.1 Changing economic landscape 2.2 Emerging workstyles: agile working 2.3 Implications for the workplace 3.0 New work, new workplace 9 3.1 Workplace: a new purpose 3.2 Workplace design and fitout 3.3 Workplace management 4.0 From feudal to functional 14 4.1 Models of provision: the flexible space market 4.2 Affordability, clusters and mixed use 4.3 New models in historic buildings 5.0 New workplaces in historic buildings? 20 5.1 Public realm 5.2 Physical attributes 5.3 Management attributes 5.4 Cultural/social attributes 6.0 Case studies 25 6.1 Cromford Mill, Derbyshire 6.2 The Round Foundry, Leeds 6.3 Toffee Factory, Newcastle upon Tyne 7.0 Conclusions 31 Prepared for: Historic England ii By: RAMIDUS CONSULTING LIMITED Date: 6th April 2018 A Perspective on Agile Working in Historic Buildings 1.0 Introduction This paper was commissioned by Historic England from Ramidus Consulting in February 2018. The overriding purpose of the commission was to explore and discuss the potential for agile working in historic buildings. The Heritage Lottery Fund report, New Ideas Need Old Buildings (2013) suggested that, nationally, there were over 130,000 businesses operating in Listed buildings alone. The report was clear in its view that historic buildings have an important role in supporting modern businesses. -

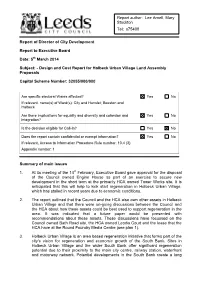

Report of Director of City Development Report to Executive Board Date

Report author: Lee Arnell, Mary Stockton Tel: x75408 Report of Director of City Development Report to Executive Board Date: 5th March 2014 Subject: - Design and Cost Report for Holbeck Urban Village Land Assembly Proposals Capital Scheme Number: 32055/000/000 Are specific electoral Wards affected? Yes No If relevant, name(s) of Ward(s): City and Hunslet; Beeston and Holbeck Are there implications for equality and diversity and cohesion and Yes No integration? Is the decision eligible for Call-In? Yes No Does the report contain confidential or exempt information? Yes No If relevant, Access to Information Procedure Rule number: 10.4 (3) Appendix number: 1 Summary of main issues 1. At its meeting of the 14 th February, Executive Board gave approval for the disposal of the Council owned Engine House as part of an exercise to secure new development in the short term at the primarily HCA owned Tower Works site. It is anticipated that this will help to kick start regeneration in Holbeck Urban Village, which has stalled in recent years due to economic conditions. 2. The report outlined that the Council and the HCA also own other assets in Holbeck Urban Village and that there were on-going discussions between the Council and the HCA about how these assets could be best used to support regeneration in the area. It was indicated that a future paper would be presented with recommendations about these assets. These discussions have focussed on the Council owned Bath Road site, the HCA owned Leodis Court and the lease that the HCA have at the Round Foundry Media Centre (see plan 1). -

Public Document Pack

Public Document Pack EAST (OUTER) AREA COMMITTEE Meeting to be held in the Civic Hall, Leeds on Tuesday, 18th September, 2007 at 4.00 pm MEMBERSHIP Councillors S Armitage - Cross Gates and Whinmoor P Grahame - Cross Gates and Whinmoor P Gruen - Cross Gates and Whinmoor M Dobson - Garforth and Swillington A Harrison - Garforth and Swillington T Murray - Garforth and Swillington J Lewis - Kippax and Methley K Parker - Kippax and Methley K Wakefield - Kippax and Methley W Hyde - Temple Newsam J Langdale - Temple Newsam M Lyons - Temple Newsam Agenda compiled by: Janet Pritchard Acting Area Manager: Governance Services Unit John Woolmer Civic Hall Tel: 214 3235 LEEDS LS1 1UR Telephone: 247 4327 Produced on Recycled Paper A A BRIEF EXPLANATION OF COUNCIL FUNCTIONS AND EXECUTIVE FUNCTIONS There are certain functions that are defined by regulations which can only be carried out at a meeting of the Full Council or under a Scheme of Delegation approved by the Full Council. Everything else is an Executive Function and, therefore, is carried out by the Council’s Executive Board or under a Scheme of Delegation agreed by the Executive Board. The Area Committee has some functions which are delegated from full Council and some Functions which are delegated from the Executive Board. Both functions are kept separately in order to make it clear where the authority has come from so that if there are decisions that the Area Committee decides not to make they know which body the decision should be referred back to. B A G E N D A Item Ward/ Item Not Page No Open No 1 APPEALS AGAINST REFUSAL OF INSPECTION OF DOCUMENTS To consider any appeals in accordance with Procedure Rule 25 of the Access to Information Procedure Rules (in the event of an Appeal the press and public will be excluded). -

Leeds City Region HS2 Growth Strategy

LEEDS CITY REGION HS2 GROWTH STRATEGY DRAFT FOR ENGAGEMENT: 15TH JANUARY TO 2ND MARCH 2018 For more information please visit: www.westyorks-ca.gov.uk/hs2growthstrategy 02 LEEDS CITY REGION HS2 GROWTH STRATEGY | DRAFT FOR ENGAGEMENT CONTENT FOREWORD 05 1. EXECUTIVE SUMMARY 07 2. INTRODUCTION 13 3. LEEDS CITY REGION 19 4. PRINCIPLES 33 TRANSFORMING THE CITY REGION ECONOMY 36 A STEP CHANGE IN CONNECTIVITY FOR THE CITY REGION 44 A NEW WORLD CLASS GATEWAY AT LEEDS STATION 50 A CATALYST FOR REGENERATION 58 INSPIRING OUR PEOPLE 64 DEVELOPING OUR BUSINESSES AND SUPPLY CHAIN 68 A MAGNET FOR INVESTMENT AND CULTURAL DESTINATION 72 5. PROPOSALS 75 6. CONCLUSION 83 LEEDS CITY REGION HS2 GROWTH STRATEGY | DRAFT FOR ENGAGEMENT 03 04 LEEDS CITY REGION HS2 GROWTH STRATEGY | DRAFT FOR ENGAGEMENT FOREWORD Our city region is growing and HS2 is vital to support the next step in transforming our economy. HS2 is much more than just a transport project. It will act as a catalyst for regeneration and growth around our main transport hubs, it will improve connectivity to our towns and cities across the Leeds City Region and the North, it will improve the skills and job opportunities for our workforce, it will create opportunities for our businesses and supply chains, and enhance the image and profile of our city region. HS2 is part of our wider ambitions for inclusive growth across the Leeds City Region. This growth is essential in order to raise living standards and tackle deprivation, boost innovation, exports and create new jobs. HS2 helps achieve our goals by strengthening business links, by opening up new markets and access to talent and by connecting people to jobs. -

Newsletter 89 Late Spring 2013

NEWSLETTER 89 LATE SPRING 2013 EDITORIAL I hope you all enjoyed the summer and made the most of the wonderful weather we have experienced in being able to visit some IA sites. I am now looking forward to our next Lecture programme and another year of activities. Details of the lectures and events are enclosed with this Newsletter and are also available on the YAHS website. Don’t forget to check the website regularly for details of other events and news throughout the year and a reminder that you can also use the website to order publications from the online shop. Also enclosed are the minutes from the April AGM, please let me know in writing or email if you have any corrections to propose to the minutes. We are now three quarters of the way through the Yorkshire Archaeological & Historical Society’s 150th anniversary year and I hope that some of you have been able to attend some of the events that have been organised to celebrate the year. Highlights of the events are available on the YAHS website and include the Section walk on 12 May led by Robert Vickers. A more extended report of this event is included later in the Newsletter, the weather could have been better but the small group who attended were appreciative of Robert’s efforts in researching and leading the walk. The Section’s next event as part of the celebrations will be held on Saturday 21 September with the day school at the National Coal Mining Museum and I hope this will be well attended. -

Index to Yorkshire Journal

Index to Yorkshire Journal A full index to the previous year’s issues was published in each Spring issue from 1994 to 2004. It would be extremely time consuming to combine these annual indexes into a single master index, so the annual indexes are individually reproduced in the remainder of this document. Fortunately it is relatively simple to find all references using the search function in your reader – usually this is invoked by pressing the Cntrl and F keys simultaneously. No index exists for the last three 2004 issues, as publication ceased at the end of this year, Each reference is indexed by the issue number (in bold type) followed by the page number. The issue numbers are: Spring Summer Autumn Winter 1993 1 2 3 4 1994 5 6 7 8 1995 9 10 11 12 1996 13 14 15 16 1997 17 18 19 20 1998 21 22 23 24 1999 25 26 27 28 2000 29 30 31 32 2001 33 34 35 36 2002 37 38 39 40 2003 - 41 42 43 2004 44 45 46 47 There was also a trial issue (Winter 1992) referenced by 0 The following suffixes have been used to identify the different types of material being referenced: a an illustration: drawing, painting, etc p photograph cp cover photograph v verse dv dialect verse ss short story (R) book review For example, 2 110p refers to a photograph on page 110 of the summer 1993 issue. Where no suffix is given, the reference is textual. Subject Index A Askrigg Kings Arms I 89-90 Addingham Atkinson, John Christopher Church of St Peter 3 68p Forty Years in a ‘Moorland Paris/1 Addlebrough 2 83p (r891), excpt 3 22 Adel auctions 4 I 15—17 Church of St John the Baptist -

Marshall's Mill, Holbeck

Marshall’s Mill Holbeck Design Statement Revised 8th August 2004 Prepared by... URBED with Bauman Llyons Architects Martin Stockley Associates and King Sturge For Igloo URBED 10 Little Lever Street MANCHESTER M1 1RF t. 0161 200 5500 f. 0161 237 3994 19 Store Street LONDON WC1E 7DH t. 0207 436 8050 f. 0207 436 8083 [email protected] Marshall’s Mill Holbeck Contents Introduction 1 3b Masterplanning structure 19 3c Masterplan form 21 PART 1: The Leeds context 2 3d Masterplan blocks 23 1a Leeds 3 3e Masterplan massing 24 1b The development of Leeds 5 3f. Masterplan townscape and Heritage 25 3g. Proposed Uses 26 PART 2: The Holbeck Urban Village Area 6 3h. Public Realm 27 2a The development of Holbeck 7 2b History of the Site 8 PART 4: Transport Strategy 28 2c The area today 11 4a. The curent situation 29 2c The area today (continued) 12 4b. Access strategy 31 2d Townscape Analysis 13 4c. Parking and servicing 33 2e Policy context 14 PART 5: Socially Responsible Investment 34 5a. Sustainable energy strategy 35 PART 3: Masterplan Development 16 5a. Daylight and overshadowing 37 3a Reconnecting Holbeck Urban Village 17 5b. Wind assessment 39 A report by URBED with Bauman Lyons, Martin Stockley Associates and King Sturge Introduction This design statement has been pro- The masterplan for Marshall’s duced in support of the outline planning Mill proposes a mixed-use, application for the Marshall’s Mill site dense urban quarter that can that is being submitted to Leeds City contribute positively to the Council by Igloo. -

Historic Character Map of Leeds

HOLBECK: Walking Tour HOLBECK: This short 1km tour explores the inherited character of part of Holbeck, a former industrial area of Leeds undergoing heritage-led regeneration. A rich industrial heritage is interspersed with large gap sites, many of which have secured investment to create an urban village immediately south of the city centre. Poor quality developments in the late 20th century led to adoption of the Holbeck Urban Village Planning Framework (2006). Principles within it are guiding future development, helping to “preserve the area’s unique character, combining the architectural legacy with new high-quality and contemporary design”. Moving around the area we’ll be exploring some techniques of characterisation, a method used to understand and describe how a place is distinctive. We’ll explore some policies in the Urban Village Planning Framework, and considering how more recent developments have contributed to the area’s character. Relevant principles within the ‘Urban Design & Public Realm’ and ‘Conservation & Listed Buildings’ chapters of the Holbeck Urban Village Planning Framework are introduced along the way, demonstrating the important roles that strategic planning and development management have in heritage-led regeneration. You can navigate the tour by following the map and the key points along it. Short descriptions with images are provided for each point. N.B. Some principles of the Holbeck Urban Village Framework are slightly abridged in places. The full version can be found at http://www.leeds.gov.uk/docs/Holbeck%20Urban%20Village.pdf. A NOTE ABOUT SAFETY! The tour follows a number of busy streets in Holbeck, and special care should be taken when crossing them.