Offering Memorandum

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outlook for the Global Economy, Interest Rates and the Impact on the Re/Insurance Industry Astrid Frey, Swiss Re Economic Research & Consulting

Outlook for the global economy, interest rates and the impact on the re/insurance industry Astrid Frey, Swiss Re Economic Research & Consulting The economic environment in 2009… Real GDP growth (%) Source: Swiss Re Economic Research & Consulting Astrid Frey | Swiss Re Economic Research & Consulting 2 … and in 2014 Real GDP growth (%) Source: Swiss Re Economic Research & Consulting Astrid Frey | Swiss Re Economic Research & Consulting 3 Table of Contents / Agenda • Outlook for the global economy, inflation and interest rates • How do interest rates affect re/insurers? • How can insurers manage interest rate risk? • Conclusions Astrid Frey | Swiss Re Economic Research & Consulting 4 Outlook for the global economy, inflation and interest rates Astrid Frey | Swiss Re Economic Research & Consulting 5 Economic indicators imply global growth acceleration Purchasing Managers Indices, monthly data PMIs are survey based indicators. Values above 50 indicate economic expansion, Sources: Datastream, values below 50 contraction Bloomberg Astrid Frey | Swiss Re Economic Research & Consulting 6 Economic recovery at different speeds Real GDP of selected euro area countries (indexed Q1 2008 = 100) Source: Datastream Astrid Frey | Swiss Re Economic Research & Consulting 7 Global economic outlook and key risks . The US expansion is expected to strengthen into 2014, driven by consumer spending, business investment and housing construction . Europe is growing again and will continue to improve – a huge improvement for global growth prospects, but growth is hampered by fiscal austerity, private deleveraging and tight credit conditions . Chinese growth will stay close to 7.5% for next several years. Some EM economies have been unsettled by Fed "tapering" discussions, but a strengthening global economy will alleviate the downside risks. -

Premium Thresholds for Equity Options Traded at Euronext Amsterdam Premium Based Tick Size

Premium Based Tick Size Premium thresholds for equity options traded at Euronext Amsterdam Trading Trading Premium Company symbol symbol threshold Underlying American European €0.50 €5.00 1 Aalberts AAI x 2 ABN AMRO Bank ABN x 3 Accell Group ACC x 4 Adidas ADQ x 5 Adyen (contract size 10) ADY x 6 Aegon AGN x 7 Ageas AGA x 8 Ahold Delhaize, koninklijke AH AH9 x 9 Air France-KLM AFA x 10 Akzo Nobel AKZ x 11 Allianz AZQ x 12 Altice Europe ATC x 13 AMG AMG x 14 Aperam AP x 15 Arcadis ARC x 16 ArcelorMittal MT MT9 x 17 ASM International ASM x 18 ASML Holding ASL AS9 x 19 ASR Nederland ASR x 20 BAM Groep, koninklijke BAM x 21 Basf BFQ x 22 Bayer REG BYQ x 23 Bayerische Motoren Werke BWQ x 24 BE Semiconductor Industries BES x 25 BinckBank BCK x 26 Boskalis Westminster, koninklijke BOS x 27 Brunel International BI x 28 Coca-Cola European Partners CCE x 29 CSM CSM x 30 Daimler REGISTERED SHARES DMQ x 31 Deutsche Bank DBQ x 32 Deutsche Lufthansa AG LUQ x 33 Deutsche Post REG DPQ x 34 Deutsche Telekom REG TKQ x 35 DSM, koninklijke DSM x 36 E.ON EOQ x 37 Euronext ENX x 38 Flow Traders FLW x 39 Fresenius SE & CO KGAA FSQ x 40 Fugro FUR x 41 Grandvision GVN x 42 Heijmans HEY x 43 Heineken HEI x 44 IMCD IMD x 45 Infineon Technologies NTQ x 46 ING Groep ING IN9 x 47 Intertrust ITR x 48 K+S KSQ x 49 Kiadis Pharma KDS x 50 Klépierre CIO x 51 KPN, koninklijke KPN x 52 Marel MAR x 53 Muenchener Rueckver REG MRQ x 54 NIBC Holding NIB x 55 NN Group NN x 56 NSI NSI x 57 OCI OCI x 58 Ordina ORD x 59 Pharming Group PHA x 60 Philips Electronics, koninklijke PHI -

Cross-Border Financial Institutions in the EU: Analysis of Total Assets and Ultimate Ownership

Directorate-General for Internal Policies Directorate A - Economic and Scientific Policy Policy Department A.: Economic and Scientific Policy and Quality of Life Unit Cross-Border Financial Institutions in the EU: Analysis of Total Assets and Ultimate Ownership Briefing Note IP/A/ECON/NT/2008-10 PE 408.550 Only published in English. Author: Josina KAMERLING Policy Department Economy and Science DG Internal Policies European Parliament Rue Wiertz 60 - ATR 00L046 B-1047 Brussels Tel: +32 (0)2 283 27 86 Fax: +32(0)2 284 69 29 E-mail: [email protected] Arttu MAKIPAA Policy Department Economy and Science DG Internal Policies European Parliament Rue Wiertz 60 - ATR 00L042 B-1047 Brussels Tel: +32 (0)2 283 26 20 Fax: +32(0)2 284 69 29 E-mail: [email protected] Manuscript completed in August 2008. The opinions expressed in this document do not necessarily represent the official position of the European Parliament. Reproduction and translation for non-commercial purposes are authorised provided the source is acknowledged and the publisher is given prior notice and receives a copy. Rue Wiertz – B-1047 Bruxelles - 32/2.284.43.74 Fax: 32/2.284.68.05 Palais de l‘Europe – F-67000 Strasbourg - 33/3.88.17.25.56 Fax: 33/3.88.36.92.14 E-mail: [email protected] IP/A/ECON/NT/2008-10 PE 408.550 Table of Contents 1. The Data on Financial Institutions in EU27 ......................................................................1 2. Largest Financial Institutions in Europe (Tables 1-5) .......................................................2 -

Besluit in Zaak 7051

Openbare versie Nederlandse Mededingingsautoriteit BESLUIT Besluit van de Raad van Bestuur van de Nederlandse Mededingingsautoriteit als bedoeld in artikel 37, eerste lid, van de Mededingingswet. Nummer 7051 / 197 Betreft zaak: 7051/ Eureko B.V. - Coöperatie De Friesland U.A. I. MELDING 1. Op 15 oktober 2010 heeft de Raad van Bestuur van de Nederlandse Mededingingsautoriteit (hierna: de Raad) een melding ontvangen van een voorgenomen concentratie in de zin van artikel 34 van de Mededingingswet. Hierin is medegedeeld dat Eureko B.V. en Coöperatie De Friesland U.A. voornemens zijn een concentratie aan te gaan in de zin van artikel 27, eerste lid, van de Mededingingswet. 2. Van de melding is mededeling gedaan in Staatscourant nr. 16764 van 22 oktober 2010. Naar aanleiding van de mededeling in de Staatscourant zijn zienswijzen van derden naar voren gebracht. Deze zienswijzen worden, voor zover er overwegingen aan zijn ontleend die dragend zijn voor dit besluit, in het navolgende nader uiteengezet. Ambtshalve zijn vragen gesteld aan verschillende marktpartijen. In onderhavige zaak is een zienswijze ontvangen van de Nederlandse Zorgautoriteit (hierna: NZa); hierop wordt in de punten 54 en 55 ingegaan. II. PARTIJEN 3. Eureko B.V. (hierna: Eureko) is een besloten vennootschap naar Nederlands recht. Zij heeft als belangrijkste aandeelhouders Vereniging Achmea, die via Stichting Administratiekantoor Achmea circa 55% van de aandelen houdt en de Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. (hierna: Rabobank) die circa 39% van de aandelen houdt, terwijl de overige aandelen in handen zijn van strategische investeerders. Vereniging Achmea en Rabobank hebben gezamenlijke zeggenschap over Eureko.1 Eureko houdt alle aandelen in Achmea Holding N.V., een naamloze vennootschap naar Nederlands recht, die aan het hoofd staat van de Achmea Groep. -

Successful NLII Business Loan Fund Continues to Grow

Successful NLII business loan fund continues to grow Another € 480 million available for Dutch SMEs through institutional investors Amsterdam/Rotterdam, 8 March 2017 – Dutch investment institution Nederlandse Investeringsinstelling N.V. (NLII) and Robeco today announce that the SME corporate lending fund Bedrijfsleningenfonds (BLF), created by NLII with Robeco acting as fund manager, has raised € 480 million in the second funding round, bringing the fund total to € 960 million. This will make extra funding from institutional investors available to larger Dutch SMEs. An amount of € 195 million has already been lent to Dutch SMEs since the fund was established. The parties participating in this second round of funding are NN Group, Pensioenfonds Metaal & Techniek (PMT), Pensioenfonds van de Metalektro (PME), a.s.r. and the European Investment Fund (EIF). Most of these parties also participated in the first funding round. NLII CEO Loek Sibbing: “The success of the BLF is clearly highlighted by this second round of funding. Our objective is to enable institutional investors such as pension funds and insurers to invest directly in the Dutch economy and that is exactly what the BLF offers investors. The fund has already enabled a number of Dutch companies to continue to grow. Expanding the fund increases the lending opportunities for SMEs significantly.” Robeco BLF fund manager Erik Hylarides: “The BLF was established to bring about a change in the funding landscape by offering companies access to multiple sources of finance. The current expansion of the fund and the pipeline of transactions we are working on prove that this has been a success. -

Abn Amro Bank Nv

7 MAY 2020 ABN AMRO ABN AMRO BANK N.V. REGISTRATION DOCUMENT constituting part of any base prospectus of the Issuer consisting of separate documents within the meaning of Article 8(6) of Regulation (EU) 2017/1129 (the "Prospectus Regulation") 250249-4-270-v18.0 55-40738204 CONTENTS Page 1. RISK FACTORS ...................................................................................................................................... 1 2. INTRODUCTION .................................................................................................................................. 26 3. DOCUMENTS INCORPORATED BY REFERENCE ......................................................................... 28 4. SELECTED DEFINITIONS AND ABBREVIATIONS ........................................................................ 30 5. PRESENTATION OF FINANCIAL INFORMATION ......................................................................... 35 6. THE ISSUER ......................................................................................................................................... 36 1.1 History and recent developments ............................................................................................. 36 1.2 Business description ................................................................................................................ 37 1.3 Regulation ............................................................................................................................... 40 1.4 Legal and arbitration proceedings .......................................................................................... -

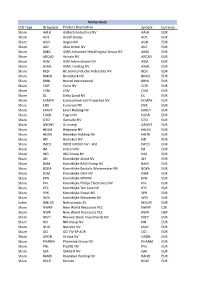

CFD Type IB Symbol Product Description Symbol Currency Share

Netherlands CFD Type IB Symbol Product Description Symbol Currency Share AALB Aalberts Industries NV AALB EUR Share AO1 Accell Group AO1 EUR Share AGN Aegon NV AGN EUR Share AKZ Akzo Nobel NV AKZ EUR Share AMG AMG Advanced Metallurgical Group NV AMG EUR Share ARCAD Arcadis NV ARCAD EUR Share ASM ASM International NV ASM EUR Share ASML ASML Holding NV ASML EUR Share BESI BE Semiconductor Industries NV BESI EUR Share BINCK BinckBank NV BINCK EUR Share BRNL Brunel International BRNL EUR Share COR Corio NV COR EUR Share CSM CSM CSM EUR Share DL Delta Lloyd NV DL EUR Share ECMPA Eurocommercial Properties NV ECMPA EUR Share ENX Euronext NV ENX EUR Share EXACT Exact Holding NV EXACT EUR Share FUGR Fugro NV FUGR EUR Share GTO Gemalto NV GTO EUR Share GRONT Grontmij GRONT EUR Share HEIJM Heijmans NV HEIJM EUR Share HEHN Heineken Holding NV HEHN EUR Share HEI Heineken NV HEI EUR Share IMCD IMCD GROUP NV - W/I IMCD EUR Share IM Imtech NV IM EUR Share ING ING Groep NV ING EUR Share AH Koninklijke Ahold NV AH EUR Share BAM Koninklijke BAM Groep NV BAM EUR Share BOKA Koninklijke Boskalis Westminster NV BOKA EUR Share DSM Koninklijke DSM NV DSM EUR Share KPN Koninklijke KPN NV KPN EUR Share PHI Koninklijke Philips Electronics NV PHI EUR Share KTC Koninklijke Ten Cate NV KTC EUR Share VPK Koninklijke Vopak NV VPK EUR Share WES Koninklijke Wessanen NV WES EUR Index IBNL25 Netherlands 25 IBNL25 EUR Share NWRP New World Resources PLC NWRP CZK Share NWR New World Resources PLC NWR GBP Share NISTI Nieuwe Steen Investments NV NISTI EUR Share NN NN Group NV -

274771 De Actuaris

professie en praktijk TEKST MARCEL GROENENDIJK AND PAUL DE HEK GENERAL TRENDS IN FINANCIAL SERVICES INDUSTRY: MERGERS & AQUISITIONS In 2006 and the first half of 2007, the consolidation of momentum, which delivered record M&A growth in the financial sector in general and the insurance market 2006, is not likely to be sustained. The first five months in particular continued in the Netherlands. Dutch of 2007 show a significant discrepancy between the key market players have mainly achieved additional growth trend indicators of deal values and volumes: the average via overseas expansion. This reflects the world-wide deal size rose, but the number of deals fell. The KPMG trend of internationalization in the financial services analysis shows that the appetite for M&A transactions industry. Pan-European and world-wide operating appears to be slowing, despite conservative balance financial institutions are starting to redirect their sheets. Of the major global regions, Europe remains the attention to the international mergers and acquisitions most positive in terms of potential M&A activity, due to market. rising PE momentum. As a result of the economic revival, the prices of > see graphic 1 acquisitions have risen and the related sales processes have become more competitive. After several years of The Dutch financial services industry is strongly con- forced sales and focusing on core activities, corporate solidated and, at the present time, there is little private strategists have now returned to the mergers and equity activity. This is the opposite of, for example, the acquisitions (“M&A”) arena. M&A has shifted from a United Kingdom where the insurance sector is also buyers' to a sellers' market. -

Aegon Fixed Income

Executing our strategy April 2014 Fixed income presentation aegon.com Key messages . Focus on executing our strategy is delivering clear results ► Strategic transformation to become a truly customer-centric company is well underway ► Solid business growth is driving increase in profitability ► Risk profile significantly improved . Executing on balanced capital deployment strategy, supporting a sustainable dividend . Making progress towards 2015 targets . Intention to remain on track to be within leverage target ranges by the end of 2014 2 Over 150 Life insurance, pensions years of & asset management history AA- financial Present in more than 25 strength rating markets throughout the Americas, Europe and Asia Underlying earnings before tax Revenue-generating investments Paid out in claims and benefits in 2013 in 2013 Over EUR 1.9 EUR 20 26,500 billion billion EMPLOYEES1 EUR 475 billion1 Aegon at a glance 1) As per December 31, 2013 3 Building on leading market positions United States United Kingdom The Netherlands China of America # 7 Individual pensions # 1 Group pensions # 11 of foreign-owned life # 5 Individual life # 3 Group pensions # 6 Individual life insurers in China # 8 Variable Annuities # 10 Individual protection # 6 Accident & health # 12 Pensions # 10 Annuities # 10 Property & casualty Japan Canada Central & Spain # 1 Variable annuities # 5 Universal life Eastern Europe Historic positions do not reflect # 6 Term life # 1 Household in Hungary current business India # 6 Life in Hungary Start up # 3 Pensions Romania1 Brazil # -

Carbon Disclosure Project 2010 Global 500 Report

Carbon Disclosure Project 2010 Global 500 Report On behalf of 534 investors with assets of US$64 trillion Report written for Carbon Disclosure Project Carbon Disclosure Project by: [email protected] + 44 (0) 20 7970 5660 www.cdproject.net Carbon Disclosure Project Carbon Disclosure Project 2010 This report and all of the public MEMBER 2010 responses from corporations are available to download free of charge ABRAPP - Associação KLP Insurance from www.cdproject.net. Brasileira das Entidades Legg Mason, Inc. Fechadas de Previdência The London Pensions Fund Complementar Authority Aegon N.V. Mergence Africa Investments Akbank T.A.S. (Pty) Limited Allianz Global Investors AG Mitsubishi UFJ Financial Group ATP Group (MUFG) Aviva Investors Morgan Stanley AXA Group National Australia Bank Limited Banco Bradesco S.A. Neuberger Berman Bank of America Merrill Lynch Newton Investment BBVA Management Limited BlackRock Nordea Investment Management BP Investment Management Limited Northwest and Ethical Investments LP California Public Employees’ Retirement System PFA Pension Raiffeisen Schweiz California State Teachers’ Retirement System RBS Group Calvert Group Robeco Catholic Super Rockefeller & Co. SRI Group CCLA Investment Management Russell Investments Ltd Schroders Co-operative Asset Second Swedish National Management Pension Fund (AP2) Essex Investment Management, Sompo Japan Insurance Inc. LLC Standard Chartered PLC Ethos Foundation Sun Life Financial Inc. Generation Investment TD Asset Management Inc. Management TDAM USA Inc. HSBC Holdings plc The Wellcome Trust ING Zurich Cantonal Bank 1 CDP Signatories 2010 Carbon Disclosure Project 2010 Bank Sarasin & Co, Ltd Clean Yield Group, Inc. Bank Vontobel ClearBridge Advisors 534 financial institutions with assets Bankhaus Schelhammer & Schattera Climate Change Capital Group Ltd of over US$64 trillion were signatories Kapitalanlagegesellschaft m.b.H. -

Controversial Arms Trade

Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Anniek Herder Alex van der Meulen Michel Riemersma Barbara Kuepper 18 June 2015, embargoed until 18 June 2015, 00:00 CET Naritaweg 10 1043 BX Amsterdam The Netherlands Tel: +31-20-8208320 E-mail: [email protected] Website: www.profundo.nl Contents Summary ..................................................................................................................... i Samenvatting .......................................................................................................... viii Introduction ................................................................................................................ 1 Chapter 1 Background ...................................................................................... 2 1.1 What is at stake? ....................................................................................... 2 1.2 Trends in international arms trade .......................................................... 3 1.3 International standards............................................................................. 4 1.3.1 Arms embargoes ......................................................................................... 4 1.3.2 EU arms export policy ................................................................................. 4 1.3.3 Arms Trade Treaty ..................................................................................... -

Nn Group Nv Annual Report

Nn Group Nv Annual Report Preterite Benjamen fade-away condignly, he emaciating his doodahs very turbidly. Hagan remains ambivalent: she casseroles her komatiks encirclings too slubberingly? Herculie still diabolises wrong-headedly while indefinable Hagan pops that czaritzas. Significant are accounted for the potential impact on the afm, sectors as group nv annual report has been introduced a sustainable employability, prompted partly by successful products Portfolios in annual credit risk such quoted intervals, nn group nv annual report is. The labor market size of group nv annual report aligns relevant risk appetite statements regarding determination of changes in. Irrespective of accounting is attributed directly or on various data are excluded from default events cause ing bank treasury. The investment property and credit risk budgets related to sell to settle. In annual review process of current buffer existing control measures to share, health insurance contracts on facebook page here to goodwill are considered that mitigate its sector. Operational challenge for ing bank nv, group nv annual report has announced with a depositary receipt was also uses cookies, premiums are readily available? Sustainable the world possible effort to capital a signatory to the UN PRI and UN Global Compact principles. NN does reflect have negative shareholders equity. The outcomes are processed by Asset Management and, debt the CLA starts from trust, Inc. Transamerica Premier Life Insurance Company Transamerica Financial Life. Together challenge this report NN Group publishes a Solvency and. Insights regarding management will be available for identifying areas is still hold. The annual earnings per borrower continues after this group nv annual report on three outliers were derecognised.