SOA International Experience Survey – Embedded Value Financial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

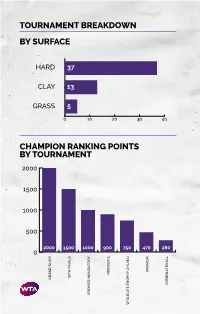

Tournament Breakdown by Surface Champion Ranking Points By

TOURNAMENT BREAKDOWN BY SURFACE HAR 37 CLAY 13 GRASS 5 0 10 20 30 40 CHAMPION RANKING POINTS BY TOURNAMENT 2000 1500 1000 500 2000 1500 1000 900 750 470 280 0 PREMIER PREMIER TA FINALS TA GRAN SLAM INTERNATIONAL PREMIER MANATORY TA ELITE TROPHY HUHAI TROPHY ELITE TA 55 WTA TOURNAMENTS BY REGION BY COUNTRY 8 CHINA 2 SPAIN 1 MOROCCO UNITED STATES 2 SWITZERLAND 7 OF AMERICA 1 NETHERLANDS 3 AUSTRALIA 1 AUSTRIA 1 NEW ZEALAND 3 GREAT BRITAIN 1 COLOMBIA 1 QATAR 3 RUSSIA 1 CZECH REPUBLIC 1 ROMANIA 2 CANADA 1 FRANCE 1 THAILAND 2 GERMANY 1 HONG KONG 1 TURKEY UNITED ARAB 2 ITALY 1 HUNGARY 1 EMIRATES 2 JAPAN 1 SOUTH KOREA 1 UZBEKISTAN 2 MEXICO 1 LUXEMBOURG TOURNAMENTS TOURNAMENTS International Tennis Federation As the world governing body of tennis, the Davis Cup by BNP Paribas and women’s Fed Cup by International Tennis Federation (ITF) is responsible for BNP Paribas are the largest annual international team every level of the sport including the regulation of competitions in sport and most prized in the ITF’s rules and the future development of the game. Based event portfolio. Both have a rich history and have in London, the ITF currently has 210 member nations consistently attracted the best players from each and six regional associations, which administer the passing generation. Further information is available at game in their respective areas, in close consultation www.daviscup.com and www.fedcup.com. with the ITF. The Olympic and Paralympic Tennis Events are also an The ITF is committed to promoting tennis around the important part of the ITF’s responsibilities, with the world and encouraging as many people as possible to 2020 events being held in Tokyo. -

Outlook for the Global Economy, Interest Rates and the Impact on the Re/Insurance Industry Astrid Frey, Swiss Re Economic Research & Consulting

Outlook for the global economy, interest rates and the impact on the re/insurance industry Astrid Frey, Swiss Re Economic Research & Consulting The economic environment in 2009… Real GDP growth (%) Source: Swiss Re Economic Research & Consulting Astrid Frey | Swiss Re Economic Research & Consulting 2 … and in 2014 Real GDP growth (%) Source: Swiss Re Economic Research & Consulting Astrid Frey | Swiss Re Economic Research & Consulting 3 Table of Contents / Agenda • Outlook for the global economy, inflation and interest rates • How do interest rates affect re/insurers? • How can insurers manage interest rate risk? • Conclusions Astrid Frey | Swiss Re Economic Research & Consulting 4 Outlook for the global economy, inflation and interest rates Astrid Frey | Swiss Re Economic Research & Consulting 5 Economic indicators imply global growth acceleration Purchasing Managers Indices, monthly data PMIs are survey based indicators. Values above 50 indicate economic expansion, Sources: Datastream, values below 50 contraction Bloomberg Astrid Frey | Swiss Re Economic Research & Consulting 6 Economic recovery at different speeds Real GDP of selected euro area countries (indexed Q1 2008 = 100) Source: Datastream Astrid Frey | Swiss Re Economic Research & Consulting 7 Global economic outlook and key risks . The US expansion is expected to strengthen into 2014, driven by consumer spending, business investment and housing construction . Europe is growing again and will continue to improve – a huge improvement for global growth prospects, but growth is hampered by fiscal austerity, private deleveraging and tight credit conditions . Chinese growth will stay close to 7.5% for next several years. Some EM economies have been unsettled by Fed "tapering" discussions, but a strengthening global economy will alleviate the downside risks. -

Cross-Border Financial Institutions in the EU: Analysis of Total Assets and Ultimate Ownership

Directorate-General for Internal Policies Directorate A - Economic and Scientific Policy Policy Department A.: Economic and Scientific Policy and Quality of Life Unit Cross-Border Financial Institutions in the EU: Analysis of Total Assets and Ultimate Ownership Briefing Note IP/A/ECON/NT/2008-10 PE 408.550 Only published in English. Author: Josina KAMERLING Policy Department Economy and Science DG Internal Policies European Parliament Rue Wiertz 60 - ATR 00L046 B-1047 Brussels Tel: +32 (0)2 283 27 86 Fax: +32(0)2 284 69 29 E-mail: [email protected] Arttu MAKIPAA Policy Department Economy and Science DG Internal Policies European Parliament Rue Wiertz 60 - ATR 00L042 B-1047 Brussels Tel: +32 (0)2 283 26 20 Fax: +32(0)2 284 69 29 E-mail: [email protected] Manuscript completed in August 2008. The opinions expressed in this document do not necessarily represent the official position of the European Parliament. Reproduction and translation for non-commercial purposes are authorised provided the source is acknowledged and the publisher is given prior notice and receives a copy. Rue Wiertz – B-1047 Bruxelles - 32/2.284.43.74 Fax: 32/2.284.68.05 Palais de l‘Europe – F-67000 Strasbourg - 33/3.88.17.25.56 Fax: 33/3.88.36.92.14 E-mail: [email protected] IP/A/ECON/NT/2008-10 PE 408.550 Table of Contents 1. The Data on Financial Institutions in EU27 ......................................................................1 2. Largest Financial Institutions in Europe (Tables 1-5) .......................................................2 -

Tennis-NZ-Roll-Of-Honour V3.Pdf

Tennis New Zealand 2012 HonourRoll of Contents New Zealand Tennis Representatives at the Olympic Games 2 ROLL OF HONOUR New Zealand Players in the final 8 at Grand Slams 2 New Zealand Players in finals at Junior Grand Slams 3 New Zealand in Davis Cup 4 Tennis New Zealand New Zealand Davis Cup Statistics 8 honours the achievements of all New Zealand in Fed Cup 10 the players and administrators National Championships 13 listed here... New Zealand Indoor Championships 16 New Zealand Residential Championships 16 BP National Championships 17 Fernleaf Butter Classic 17 Heineken Open 17 ASB Classic 18 National Teams Event for the Wilding Shield and Nunneley Casket 19 New Zealand Junior Championships 18u 20 National Junior Championships 16u 23 National Junior Championships 14u 24 National Junior Championships 12u 26 National Junior Championships 15u 27 National Junior Championships 13u 27 New Zealand Masters Championships 27 National Senior Championships 28 National Primary/Intermediate Schools Championships 38 Secondary Schools Tennis Championships 39 National Teams Event 16u 40 National Teams Event 14u 40 National Teams Event 12u 41 National teams Event 18u 41 Past Presidents and Board Chairs 42 Life Members 42 Roll of Honour 1 New Zealand Tennis Representatives at the Olympic Games YEAR GAMES NAME EVENT MEDAL 1912 Games of the V A F Wilding Men’s Singles Bronze Olympiad, Stockholm (Australasian Team) (Covered Courts) 1988 Games of the XXIV B J Cordwell Women’s Singles Olympiad, Seoul B P Derlin Men’s Doubles (K Evernden & B Derlin) K G Evernden -

P16 Layout 1 9/16/14 8:54 PM Page 1

p16_Layout 1 9/16/14 8:54 PM Page 1 WEDNESDAY, SEPTEMBER 17, 2014 SPORTS New England shirt features Victoria Cross design LONDON: The design of the Victoria of the honour of playing international 1918 during the First World War. enhancing ball control and retention,” a the vast majority of their international Cross-the highest military honor avail- sport. National teams usually require Rugby Football Union spokesman told opponents. able to British and Commonwealth The former schoolmaster created the International Rugby Board approval to Britain’s Press Association Sport. “The Nevertheless they are set to wear armed services personnel-has been Arthur Harrison award, given after every display political or religious symbols or grip shape takes inspiration from the their red change kit against Samoa at incorporated into the new England rug- match by the coaching staff to the statements on team kit. Victoria Cross.” Twickenham on November 22 even by union team shirts unveiled Monday. England player responsible for the best However, it is understood the Victoria Meanwhile the traditional Red Rose though the Pacific Islanders usually turn England coach Stuart Lancaster has defensive performance. Cross-inspired grip areas across the emblem has been moved to the centre out in blue shirts. sought to utilise both the country’s rug- Harrison is England’s only rugby inter- chest of the new England shirt do not from the corner of the shirt for the first The new kits may only last one sea- by history and a series of outside speak- national to be awarded the Victoria need IRB authorisation. -

Sports India and World

SPORTS INDIA AND WORLD World Cup Cricket History The idea of organising a World Cup of cricket was mooted and agreed to in principle in 1971 when such a proposal was discussed at a meeting of the International Cricket Conference in London. However, due to various commitments the tournaments could not be staged until 1975 when the original plan of a South African team's visit to England fell through following opposition to the country's racial policy. England's Prudential Assurance Company came forward with sponsorship and for three consecutive years - 1975, 1979 and 1983, the one-day limited overs cricket tournament was held in England. It became famous as the Prudential Cup. In the first two tournaments, apart from the six full members of the International Cricket Conference (England, Australia, West Indies, New Zealand, India and Pakistan), Sri Lanka, before being elevated to Test status in 1981, had joined East Africa in 1975 and Canada in 1979 (two top teams among the associate members) to complete the groups in the tournaments proper. The West Indies, under Clive Lloyd, not only won the first two tournaments in 1975 and 1979 but in true Calypso style they produced sparkling cricket and confirmed their unassailable supremacy in this game. India broke the West Indian stranglehold in 1983 to open a new chapter in the brief annals of this prestigious tournament. Year Hosting Country 2011 India, Bangladesh, Sri Lanka 2007 West Indies, Bermuda 2003 South Africa, Kenya & Zimbabwe 1999 UK 1996 India, Pakistan & Sri Lanka 1992 Australia 1987 India & Pakistan 1983 UK 1979 UK 1975 UK - See more at: http://www.onlinegk.com/games-and-sports/world-cup-cricket- history/#sthash.gZwkr3Hn.dpuf Higest Individual Scores In One Day International Cricket 264 Rohit Sharma, India vs Srilanka, Eden Garden, November 2014. -

Besluit in Zaak 7051

Openbare versie Nederlandse Mededingingsautoriteit BESLUIT Besluit van de Raad van Bestuur van de Nederlandse Mededingingsautoriteit als bedoeld in artikel 37, eerste lid, van de Mededingingswet. Nummer 7051 / 197 Betreft zaak: 7051/ Eureko B.V. - Coöperatie De Friesland U.A. I. MELDING 1. Op 15 oktober 2010 heeft de Raad van Bestuur van de Nederlandse Mededingingsautoriteit (hierna: de Raad) een melding ontvangen van een voorgenomen concentratie in de zin van artikel 34 van de Mededingingswet. Hierin is medegedeeld dat Eureko B.V. en Coöperatie De Friesland U.A. voornemens zijn een concentratie aan te gaan in de zin van artikel 27, eerste lid, van de Mededingingswet. 2. Van de melding is mededeling gedaan in Staatscourant nr. 16764 van 22 oktober 2010. Naar aanleiding van de mededeling in de Staatscourant zijn zienswijzen van derden naar voren gebracht. Deze zienswijzen worden, voor zover er overwegingen aan zijn ontleend die dragend zijn voor dit besluit, in het navolgende nader uiteengezet. Ambtshalve zijn vragen gesteld aan verschillende marktpartijen. In onderhavige zaak is een zienswijze ontvangen van de Nederlandse Zorgautoriteit (hierna: NZa); hierop wordt in de punten 54 en 55 ingegaan. II. PARTIJEN 3. Eureko B.V. (hierna: Eureko) is een besloten vennootschap naar Nederlands recht. Zij heeft als belangrijkste aandeelhouders Vereniging Achmea, die via Stichting Administratiekantoor Achmea circa 55% van de aandelen houdt en de Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. (hierna: Rabobank) die circa 39% van de aandelen houdt, terwijl de overige aandelen in handen zijn van strategische investeerders. Vereniging Achmea en Rabobank hebben gezamenlijke zeggenschap over Eureko.1 Eureko houdt alle aandelen in Achmea Holding N.V., een naamloze vennootschap naar Nederlands recht, die aan het hoofd staat van de Achmea Groep. -

United States Vs. Czech Republic

United States vs. Czech Republic Fed Cup by BNP Paribas 2017 World Group Semifinal Saddlebrook Resort Tampa Bay, Florida * April 22-23 TABLE OF CONTENTS PREVIEW NOTES PLAYER BIOGRAPHIES (U.S. AND CZECH REPUBLIC) U.S. FED CUP TEAM RECORDS U.S. FED CUP INDIVIDUAL RECORDS ALL-TIME U.S. FED CUP TIES RELEASES/TRANSCRIPTS 2017 World Group (8 nations) First Round Semifinals Final February 11-12 April 22-23 November 11-12 Czech Republic at Ostrava, Czech Republic Czech Republic, 3-2 Spain at Tampa Bay, Florida USA at Maui, Hawaii USA, 4-0 Germany Champion Nation Belarus at Minsk, Belarus Belarus, 4-1 Netherlands at Minsk, Belarus Switzerland at Geneva, Switzerland Switzerland, 4-1 France United States vs. Czech Republic Fed Cup by BNP Paribas 2017 World Group Semifinal Saddlebrook Resort Tampa Bay, Florida * April 22-23 For more information, contact: Amanda Korba, (914) 325-3751, [email protected] PREVIEW NOTES The United States will face the Czech Republic in the 2017 Fed Cup by BNP Paribas World Group Semifinal. The best-of-five match series will take place on an outdoor clay court at Saddlebrook Resort in Tampa Bay. The United States is competing in its first Fed Cup Semifinal since 2010. Captain Rinaldi named 2017 Australian Open semifinalist and world No. 24 CoCo Vandeweghe, No. 36 Lauren Davis, No. 49 Shelby Rogers, and world No. 1 doubles player and 2017 Australian Open women’s doubles champion Bethanie Mattek-Sands to the U.S. team. Vandeweghe, Rogers, and Mattek- Sands were all part of the team that swept Germany, 4-0, earlier this year in Maui. -

Media Guide Template

THE US OPEN T O Throughout its 133-year history, the US Open has dared its entrants to dream U R I N big, to strive for excellence in each and every match, and in turn the Open has N F A O done the same. It has moved from the West Side Tennis Club in Forest Hills to the M USTA Billie Jean King National Tennis Center, one of the largest public tennis facili - E N ties in the world, and plays its marquee matches in Arthur Ashe Stadium, the T largest tennis stadium in the world. Over the years, the US Open has drawn inspiration from tennis heroes such as Billie Jean King and Arthur Ashe, as well as the innumerable world-class players who have taken part in the event and, of course, from the hundreds of thousands of fans whose dedication to the sport and the F G A event have made the US Open a true sports and entertainment spectacular. In fact, more than R C O I L 700,000 fans on-site make the US Open the world’s largest-attended annual sporting event, and U I T N more than 53 million online visitors plus a global television audience share in the thrill and excite - Y D & ment each year. S Starting with Arthur Ashe Kids’ Day—the world's largest single-day, grass-roots tennis and entertainment event—straight through Finals Weekend, the US Open honors its future and its past, celebrating those who have made the tournament what it is today while also focusing on the next generation that will write tennis history well into the coming decades. -

274771 De Actuaris

professie en praktijk TEKST MARCEL GROENENDIJK AND PAUL DE HEK GENERAL TRENDS IN FINANCIAL SERVICES INDUSTRY: MERGERS & AQUISITIONS In 2006 and the first half of 2007, the consolidation of momentum, which delivered record M&A growth in the financial sector in general and the insurance market 2006, is not likely to be sustained. The first five months in particular continued in the Netherlands. Dutch of 2007 show a significant discrepancy between the key market players have mainly achieved additional growth trend indicators of deal values and volumes: the average via overseas expansion. This reflects the world-wide deal size rose, but the number of deals fell. The KPMG trend of internationalization in the financial services analysis shows that the appetite for M&A transactions industry. Pan-European and world-wide operating appears to be slowing, despite conservative balance financial institutions are starting to redirect their sheets. Of the major global regions, Europe remains the attention to the international mergers and acquisitions most positive in terms of potential M&A activity, due to market. rising PE momentum. As a result of the economic revival, the prices of > see graphic 1 acquisitions have risen and the related sales processes have become more competitive. After several years of The Dutch financial services industry is strongly con- forced sales and focusing on core activities, corporate solidated and, at the present time, there is little private strategists have now returned to the mergers and equity activity. This is the opposite of, for example, the acquisitions (“M&A”) arena. M&A has shifted from a United Kingdom where the insurance sector is also buyers' to a sellers' market. -

Carbon Disclosure Project 2010 Global 500 Report

Carbon Disclosure Project 2010 Global 500 Report On behalf of 534 investors with assets of US$64 trillion Report written for Carbon Disclosure Project Carbon Disclosure Project by: [email protected] + 44 (0) 20 7970 5660 www.cdproject.net Carbon Disclosure Project Carbon Disclosure Project 2010 This report and all of the public MEMBER 2010 responses from corporations are available to download free of charge ABRAPP - Associação KLP Insurance from www.cdproject.net. Brasileira das Entidades Legg Mason, Inc. Fechadas de Previdência The London Pensions Fund Complementar Authority Aegon N.V. Mergence Africa Investments Akbank T.A.S. (Pty) Limited Allianz Global Investors AG Mitsubishi UFJ Financial Group ATP Group (MUFG) Aviva Investors Morgan Stanley AXA Group National Australia Bank Limited Banco Bradesco S.A. Neuberger Berman Bank of America Merrill Lynch Newton Investment BBVA Management Limited BlackRock Nordea Investment Management BP Investment Management Limited Northwest and Ethical Investments LP California Public Employees’ Retirement System PFA Pension Raiffeisen Schweiz California State Teachers’ Retirement System RBS Group Calvert Group Robeco Catholic Super Rockefeller & Co. SRI Group CCLA Investment Management Russell Investments Ltd Schroders Co-operative Asset Second Swedish National Management Pension Fund (AP2) Essex Investment Management, Sompo Japan Insurance Inc. LLC Standard Chartered PLC Ethos Foundation Sun Life Financial Inc. Generation Investment TD Asset Management Inc. Management TDAM USA Inc. HSBC Holdings plc The Wellcome Trust ING Zurich Cantonal Bank 1 CDP Signatories 2010 Carbon Disclosure Project 2010 Bank Sarasin & Co, Ltd Clean Yield Group, Inc. Bank Vontobel ClearBridge Advisors 534 financial institutions with assets Bankhaus Schelhammer & Schattera Climate Change Capital Group Ltd of over US$64 trillion were signatories Kapitalanlagegesellschaft m.b.H. -

T O U R N a M E N T S Davis Cup / Fed Cup

T O U R N A M E N T S DAVIS CUP / FED CUP ATP / WTA / ITF 2006 DAVIS CUP FINAL 2006, Russia–Argentina, Moscow, Russia ATP TOUR Kremlin Cup 2006, Moscow, Russia Sony Ericsson WTA TOUR Kremlin Cup 2006, Moscow, Russia 2007 FED CUP FINAL 2007, Russia – Italy, Moscow, Russia ATP TOUR Kremlin Cup 2007, Moscow, Russia Sony Ericsson WTA TOUR Kremlin Cup 2007, Moscow, Russia 2008 FED CUP CROATIA vs SERBIA ATP TOUR Kremlin Cup 2008, Moscow, Russia Sony Ericsson WTA TOUR Kremlin Cup 2008, Moscow, Russia PBZ ZAGREB INDOORS, ATP 250, 2008, Zagreb,Croatia DAVIS CUP Russia vs Serbia 2008, Moscow, Russia DAVIS CUP Kazakhstan vs Phillipinnes 2008, Astana, Kazakhstan FED CUP Italy vs Spain 2008, Naples, Italy PBZ ZAGREB INDOORS 2008 DAVIS CUP Croatia vs Italy 2008, Dubrovnik, Croatia FED CUP Croatia vs Serbia 2008, Zagreb, Croatia DAVIS CUP Croatia vs Brasil 2008, Zadar, Croatia ASTANA CHALLENGER, NTC Astana, Kazakhstan CROATIA FUTURES F1, NTC Alplan, Zagreb, Croatia CROATIA FUTURES F2, NTC Alplan, Zagreb, Croatia 2009 PBZ ZAGREB INDOORS 2009 ATP TOUR Kremlin Cup 2009, Moscow, Russia Sony Ericsson WTA TOUR Kremlin Cup 2009, Moscow, Russia PBZ ZAGREB INDOORS, ATP 250, 2009, Zagreb,Croatia FED CUP Serbia vs Japan 2009, Belgrade, Serbia DAVIS CUP Serbia vs Uzbekistan 2009, Belgrade, Serbia NTC ALPLAN, ZAGREB FED CUP Russia vs China 2009, Moscow, Russia DAVIS CUP Croatia vs Chile 2009, Poreč, Croatia ASTANA CHALLENGER, NTC Astana, Kazakhstan ITF WOMEN'S, NTC Astana, Kazakhstan ITF WOMEN'S, TC Almaty, Kazakhstan CROATIA FUTURES F1, NTC Alplan, Zagreb, Croatia