Download (Pdf)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

Annual Report 1980

Annual Report 1980 The Depository• Trust Company The ability of Depository Trust to conduct its activities rests largely on modern computer technology, reflecting a long chain of developments in several disciplines. Automated calculating and recordkeeping are the essence of DTC's book-entry capability. Telecommunications devices facilitate the flow of information among Participants, transfer agents, and others throughout the financial community. The ability to utilize minute intervals of time permits computers to operate in billionths of a second. The illustrations in this report depict historical developments in each of these disciplines. The graphic theme and appearance of this Annual Report were conceived by David S. Jobrack, Executive Assistant to the Chairman, who also acted as Creative Director throughout the production process, and wrote, edited and/or compiled the text, illustrations and captions. 1980 Annual Report Highlights. 2 Computer Communications A Message from Management. ..... 3 Facility (CCF) . 28 History, Ownership and Policies. ....... 4 Other Automation Developments .... 28 Growth in 1980 .... 6 Interfaces in a National Clearance and Settlement System .. ....... 30 Eligible Issues. .8 Municipal Bond Program ..... 8 Protection for Participants' Securities ..... 32 Outlook for Institutional Use. 10 Officers and Directors of The Institutional Delivery (ID) Depository Trust Company.. 38 System. 14 1980 in Retrospect . .40 Basic Services 16 Financial Statements. ............ 46 Fast Automated Securities Participants. 54 Transfer (FAST) .' 17 Stockholders. ........ 56 Ancillary Services. 20 Depository Facilities ... 56 ...... 20 Dividends Pledgees .............. 57 Voting Rights. 21 Banks Reported to be Participating in Other Ancillary Services. 22 the Depository on an Indirect Basis 57 The Automation of Depository Services. 26 Investment Companies Reported Participant Terminal System (PTS). -

Banknews Reprints of Articles About Your Community Bank • • 703.584.0840

Member BankNews Reprints of articles about your community bank • www.JohnMarshallBank.com • 703.584.0840 In 1992, he was hired by Chase Manhattan Personal John Marshall Financial Services as a Second Vice President originating and underwriting jumbo mortgages. In 1995, he Bank Expands returned to commercial lending and until 2002, he held AVP and VP commercial lending positions at Citibank, to Alexandria FSB, First Virginia Bank and F&M Bank of Northern Virginia. From 2002 until 2009, Mr. Johnson was Senior Vice President of commercial lending for Virginia Commerce Bank, where he was responsible for growing a small By Bob Tagert / reprinted from OldTownCrier.com commercial loan portfolio of $5 million into a $90 mil- lion portfolio with approximately $80 million in corre- As today’s banking world appears to be one acquisition sponding deposit and cash management relationships. In after another, it is nice to see a local bank, founded by 2009, he accepted the position as Chief Lending Officer people who are local to the area and employing profes- of 1st Commonwealth Bank of Virginia. sionals who know and live in the community. As the names of banks change as much as the weather, it is Johnson is the current Chairman of the Arlington refreshing to see a local bank making its presence felt. Industrial Loan Authority and has served on this board The bank was founded in 2006 and has their corporate since 2008. Mr. Johnson has been an active member of offices in Reston. John Marshall Bank is a strong commu- nity bank that is well capitalized and is one of the fastest growing banks in the DC Metro area. -

The Global Financial Crisis: Is It Unprecedented?

Conference on Global Economic Crisis: Impacts, Transmission, and Recovery Paper Number 1 The Global Financial Crisis: Is It Unprecedented? Michael D. Bordo Professor of Economics, Rutgers University, and National Bureau of Economic Research and John S. Landon-Lane Associate Professor of Economics, Rutgers University 1. Introduction A financial crisis in the US in 2007 spread to Europe and led to a recession across the world in 2007-2009. Have we seen patterns like this before or is the recent experience novel? This paper compares the recent crisis and recent recession to earlier international financial crises and global recessions. First we review the dimensions of the recent crisis. We then present some historical narrative on earlier global crises in the nineteenth and twentieth centuries. The description of earlier global crises leads to a sense of déjà vu. We next demarcate several chronologies of the incidence of various kinds of crises: banking, currency and debt crises and combinations of them across a large number of countries for the period from 1880 to 2010. These chronologies come from earlier work of Bordo with Barry Eichengreen, Daniela Klingebiel and Maria Soledad Martinez-Peria and with Chris Meissner (Bordo et al (2001), Bordo and Meissner ( 2007)) , from Carmen Reinhart and Kenneth Rogoff’s recent book (2009) and studies by the IMF (Laeven and Valencia 2009,2010).1 Based on these chronologies we look for clusters of crisis events which occur in a number of countries and across continents. These we label global financial crises. 1 There is considerable overlap in the different chronologies as Reinhart and Rogoff incorporated many of our dates and my coauthors and I used IMF and World Bank chronologies for the period since the early 1970s. -

Why Basel II Failed and Why Any Basel III Is Doomed

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Lall, Ranjit Working Paper Why Basel II failed and why any Basel III is doomed GEG Working Paper, No. 2009/52 Provided in Cooperation with: University of Oxford, Global Economic Governance Programme (GEG) Suggested Citation: Lall, Ranjit (2009) : Why Basel II failed and why any Basel III is doomed, GEG Working Paper, No. 2009/52, University of Oxford, Global Economic Governance Programme (GEG), Oxford This Version is available at: http://hdl.handle.net/10419/196313 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu • GLOBAL ECONOMIC GOVERNANCE PROGRAMME • Global Economic Governance Programme Centre for International Studies │ Department for Politics and International Relations The Global Economic Governance Programme was established at University College, Oxford in 2003 to foster research and debate into how global markets and institutions can better serve the needs of people in developing countries. -

Franklin Square National Bank OMB No. 1024 0018

NPS Form 10-900 0MB No, 1024-0018 (Expires 5/31/2012) United States Department of the Interior RECEIVED 2280 National Park Service SEP 2 6 2015 National Register of Historic Places Nat. Register of Historic Places Registration Form National Park Service This form is for use in nominating or requesting determinations for individual properties and districts. See instructions in National Register Bulletin, How to Complete the National Register of Historic Places Registration Form. If any item does not apply to the property being documented, enter "N/A" for "not applicable." For functions, architectural classification, materials, and areas of significance, enter only categories and subcategories from the instructions. Place additional certification comments, entries, and narrative items on continuation sheets if needed (NPS Form 10-900a). 1. Name of Property_ historic name Franklin Square National Bank other names/site number ---Franklin---------------- National Bank ---------------- 2. Location street & number 925 Hempstead Turnpike not for publication city or town Franklin Square .__ _ ___, vicinity state --------NY code NY county Nassau code 059 zip code _1_1_0_1_0 ___ 3. State/Federal Agency Certification As the designated authority under the National Historic Preservation Act, as amended, I hereby certify that this __x_ nomination_ request for determination of eligibility meets the documentation standards for registering properties in the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. In my opinion, the property _x_ meets __ does not meet the National Register Criteria. I recommend that this property be considered significant at the following level(s) of significance: national __x_ statewide .JLlocal Signature of certifying official/ Ille State or Federal agency/bureau or Tribal Government In my opinion, the property _meets_ does not meet the National Register criteria. -

US Accounts in 24 Hours

U.S. Accounts In 24 Hours - eBook Thank you for purchasing our featured "U.S. Accounts In 24 Hours" eBook / Online Information Packet offered at our web site, U.S. Account Setup.com Within our featured online information packet, you will find all of the resources, tools, information, and contacts you'll need to quickly & easily open a NON-U.S. Resident Bank Account within 24 hours. You'll find lists of U.S. Banks, Account Application Forms, Information on how to obtain a U.S. Mailing Address, plus so much more. Just point and click your way through our Online Information Packet using the links above. If you should have any questions or experience any difficulties in opening your Non-U.S. Resident Account, please feel free to email us at any time, and one of our representatives will get back with you promptly. For Support, Email: [email protected] Homepage: www.usaccountsetup.com Application Forms UPDATE - E-TRADE'S NEW ACCOUNT OPENING POLICIES Etrade is changed the rules in which they open International Banking/ Brokerage accounts for foreigners. They now require all new applications be submitted to the local branch office in your region. Once account is opened, you will be able to use it as a U.S. Bank/Brokerage Account out of your home country. Below, you will find a list of International Etrade Phone Numbers & Addresses. Contact the etrade office that best reflects where you reside or would like your account based out of and where you would like to receive your debit card. U.S. -

The Social Structure of Financial Crisis Governance, 1974 and 2008

The Social Structure of Financial Crisis Governance, 1974 and 2008 Pierre-Christian Fink Columbia University Running head: Financial Crisis Governance Word count: 7,100 * Pierre-Christian Fink, Department of Sociology, Columbia University, 606 West 122nd Street, MC 9649, New York, NY 10027. E-mail: [email protected]. FINANCIAL CRISIS GOVERNANCE 2 The Social Structure of Financial Crisis Governance, 1974 and 2008 Abstract: Crises are moments of uncertainty in which existing routines no longer apply. Yet across some crises, patterns of governance repeat themselves. This article defines the conditions under which crisis governance is partially predictable, and identifies mechanisms operative in such cases. The argument is developed through a comparison of governance during the financial crises of 1974 and 2008, drawing on original archival research. In both cases, the institutional set-up led to the Federal Reserve becoming the leading institution in crisis governance. The Federal Reserve recombined forms of expertise from its two main departments (monetary policy and financial regulation) that are separate during normal times. As a consequence, it conceived of both crises as runs not on banks but on the money market, through which banks and other institutions increasingly fund themselves. Because the framing of the crisis as a money-market run implied even more risk—a disaster for the entire economy—than that of a bank run, the Federal Reserve hid its framing from Congress and the public. To solve the crisis, the Federal Reserve and its allies from banks and executive agencies sought to stabilize the money market by repurposing old tools to create so-called funding facilities. -

And Consumer Credit in the United States in the 1960S

Christine Zumello The “Everything Card” and Consumer Credit in the United States in the 1960s First National City Bank (FNCB) of New York launched the Everything Card in the summer of 1967. A latecomer in the fi eld of credit cards, FNCB nonetheless correctly recognized a promising business model for retail banking. FNCB attempted not only to ride the wave of mass consumption but also to cap- italize on the profi t-generating potential of buying on credit. Although the venture soon failed, brought down by the losses that plagued the bank due to fraud, consumer discontent, and legislative action, this fi nal attempt by a major single commer- cial bank to launch its own plan did not signify the end of credit cards. On the contrary, the Everything Card was a har- binger of the era of the universal credit card. irst National City Bank (FNCB) of New York (now Citigroup), one F of the oldest leading commercial banks in the United States, intro- duced the Everything Card in the summer of 1967.1 FNCB was a pioneer in fostering consumer fi nance in the United States. The bank saw an opportunity to increase business by creating an innovative system that would enable masses of consumers to purchase a variety of goods and services on credit. By becoming the principal tool of consumer credit, credit cards revolutionized the banking business. Indeed, “where it couldn’t gain territory with bricks and mortar, Citibank tried to do so 2 with plastic.” The author wishes to express her gratitude to Lois Kauffman of the Citigroup Archives, Citi’s Center for Heritage and Strategy, New York City. -

Annual Report of the Federal Deposit Insurance Corporation 1974 V

ANNUAL REPORT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION 1974 V. Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis A preliminary report, highlighting the Corporation's operations during 1974, was published and submitted to the Congress on February 28, 1975. Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis LETTER OF TRANSMITTAL FEDERAL DEPOSIT INSURANCE CORPORATION Washington, D.C., August 15, 1975 SIRS: Pursuant to the provisions of section 17(a) of the Federal Deposit Insurance Act, the Federal Deposit Insurance Corporation is pleased to submit its annual report fo r the calendar year 1974. Respectfully yours, FRANK WILLE Chairman THE PRESIDENT OF THE SENATE THE SPEAKER OF THE HOUSE OF REPRESENTATIVES hi Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis FEDERAL DEPOSIT INSURANCE CORPORATION Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis FEDERAL DEPOSIT INSURANCE CORPORATION BOARD OF DIRECTORS Chairman............................................................................ Frank Wille D irector............................................................... George A. LeMaistre Comptroller of the Currency ..................................... James E. Smith OFFICIALS Deputy to the Chairman......................................... Robert E. Barnett Assistant to the Director ...................................John C.H. Miller, Jr. Assistan t to the Director ................................................... -

What Is Wrong with the American Banking System and What to Do About It Arthur John Keeffe

Maryland Law Review Volume 36 | Issue 4 Article 5 What is Wrong with the American Banking System and What to Do About It Arthur John Keeffe Mary S. Head Follow this and additional works at: http://digitalcommons.law.umaryland.edu/mlr Part of the Commercial Law Commons Recommended Citation Arthur J. Keeffe, & Mary S. Head, What is Wrong with the American Banking System and What to Do About It, 36 Md. L. Rev. 788 (1977) Available at: http://digitalcommons.law.umaryland.edu/mlr/vol36/iss4/5 This Article is brought to you for free and open access by the Academic Journals at DigitalCommons@UM Carey Law. It has been accepted for inclusion in Maryland Law Review by an authorized administrator of DigitalCommons@UM Carey Law. For more information, please contact [email protected]. WHAT IS WRONG WITH THE AMERICAN BANKING SYSTEM AND WHAT TO DO ABOUT IT ARTHUR JOHN KEEFFE* MARY S. HEAD** Many of the problems which currently plague the American banking system bear a striking resemblance to the financial excesses and abuses of the late 1920's and the early 1930's which resulted in the economic collapse of that period. The lack of effective bank regulation, the increasing expansion of banks into nonbanking activities, and the rapid growth of bank holding companies are developments which produced catastrophe in an earlier day and which threaten to produce similar results today if current trends in banking continue unchecked. During the first quarter of the twentieth century, the stability of the American banking system, already weakened by a wave of financial crises which began in 1869, was further jeopardized by the large-scale entry of banks into nonbanking enterprises, notably the sale of securities. -

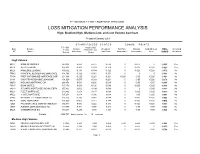

LOSS MITIGATION PERFORMANCE ANALYSIS High, Medium-High, Medium-Low, and Low Volume Servicers

FY 2000 SINGLE FAMILY MORTGAGE SERVICING LOSS MITIGATION PERFORMANCE ANALYSIS High, Medium-High, Medium-Low, and Low Volume Servicers Prepared January 2001 S T A N D A R D I Z E D S C O R E S B O N U S P O I N T S FY 1999 Actual Loss/ Svcr Servicer Loans Default Potential Loss Weighted FirstTime Minority UnderServed FINAL Increased ID * Name Scored Rate Score Score Total Score Homeowner Homeowner Area SCORE Incentives High Volume MUL1 BANK OF AMERICA 240,318 0.059 -0.727 -0.530 0 -0.025 0 -0.555 Yes MUL6 WELLS FARGO 656,303 -0.005 -0.503 -0.379 0 -0.025 -0.025 -0.429 Yes MUL5 HOMESIDE LENDING 439,502 -0.136 -0.384 -0.322 0 -0.025 -0.025 -0.372 No 75640 PRINCIPAL RESIDENTIAL MORTGAGE 191,398 -0.122 -0.361 -0.301 0 0 0 -0.301 No 77396 FIRST NATIONWIDE MORTGAGE COR 211,449 -0.125 -0.227 -0.201 -0.025 -0.05 -0.025 -0.301 No 64141 COUNTRYWIDE HOME LOANS INC 491,029 -0.075 -0.243 -0.201 0 -0.05 -0.025 -0.276 No 39276 MIDLAND MORTGAGE CO 266,458 0.521 -0.286 -0.085 0 -0.05 -0.05 -0.185 No 73815 BANK UNITED 117,179 0.039 -0.120 -0.080 0 -0.025 -0.025 -0.130 No 68013 ATLANTIC MORTGAGE AND INVESTM 155,832 -0.032 -0.104 -0.086 0 0 -0.025 -0.111 No MUL3 FLEET MORTGAGE 319,862 -0.258 0.137 0.038 0 -0.025 -0.025 -0.012 No MUL2 CHASE MORTGAGE 597,276 -0.018 0.096 0.068 0 -0.05 -0.025 -0.007 No 38092 NATIONAL CITY MORTGAGE CO 105,256 -0.236 0.142 0.048 0 -0.025 -0.025 -0.002 No MUL4 GMAC MORTGAGE 136,099 -0.057 0.211 0.144 0 -0.025 -0.025 0.094 No 12621 PNC MORTGAGE CORP OF AMERICA 102,937 0.082 0.222 0.187 0 -0.025 -0.025 0.137 No 10757 AURORA LOAN