Copyright by Shea Matthew Suski 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2015 Guideway Status Report

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2015 Legislative Report Guideway Status November 2015 PREPARED BY The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 55155-1899 Phone: 651-366-3000 Toll-Free: 1-800-657-3774 TTY, Voice or ASCII: 1-800-627-3529 In collaboration with the Metropolitan Council 390 Robert St. North St. Paul, MN 55101-1805 Phone: 651-602-1000 To request this document in an alternative format Please call 651-366-4718 or 1-800-657-3774 (Greater Minnesota). You may also send an email to [email protected]. Cover Photos: Northstar commuter rail train Source: Metro Council Green Line LRT Source: Streets MN Red Line BRT Source: Metro Council 2 Guideway Status Report November 2015 Contents Contents ......................................................................................................................................................... 3 Legislative Request........................................................................................................................................ 6 Statutory Requirement .................................................................................................................... 6 Introduction ................................................................................................................................................... 8 Statewide Planning ........................................................................................................................ -

8. South Central Minnesota Passenger Rail Initiative.Pdf

8. Council Work Session Memorandum TO: City Council FROM: Tim Murray, City Administrator MEETING DATE: April 6, 2021 SUBJECT: South Central Minnesota Passenger Rail Initiative Discussion: A bill was introduced by Rep. Todd Lippert of Northfield this legislative session (HF 1393) that is requesting $500,000 in funding to prepare a feasibility study and alternatives analysis of a passenger rail corridor connecting Minneapolis and St. Paul to Albert Lea on existing rail line and passing through Faribault and Northfield. Northfield City Councilmember Suzie Nakasian recently reached out to Mayor Voracek regarding this initiative, and Northfield City Administrator Ben Martig has provided the materials they prepared in support of the bill. They are requesting that the Faribault City Council consider adopting a resolution to be submitted in support of the bill. A similar rail proposal was discussed in 2015, but was never funded so a feasibility study was never completed. Support for that proposal included the City of Faribault as well as 40+/- other stakeholders. Attachments: • HF 1393 and memo • Northfield 2021-03-16 Council Packet materials • 2021-03-09 Letter to Senator Draheim w/ attachments • Email correspondence 02/11/21 REVISOR KRB/LG 21-02773 This Document can be made available in alternative formats upon request State of Minnesota HOUSE OF REPRESENTATIVES NINETY-SECOND SESSION H. F. No. 1393 02/22/2021 Authored by Lippert and Hausman The bill was read for the first time and referred to the Committee on Transportation Finance and Policy 1.1 A bill for an act 1.2 relating to transportation; appropriating money for a passenger rail feasibility study 1.3 in southern Minnesota. 1.4 BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF MINNESOTA: 1.5 Section 1. -

November 15, 2017 the Honorable Paul

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp November 15, 2017 The Honorable Paul Torkelson, Chair The Honorable Scott Newman, Chair House Transportation Finance Committee Senate Transportation Finance & Policy Committee 381 State Office Building 3105 Minnesota Senate Building Saint Paul, MN 55155 Saint Paul, MN 55155 The Honorable Linda Runbeck, Chair The Honorable Scott Dibble House Transportation & Regional Governance Policy Ranking Minority Member Committee Senate Transportation Finance & Policy Committee 417 State Office Building 2213 Minnesota Senate Building Saint Paul, MN 55155 Saint Paul, MN 55155 The Honorable Frank Hornstein, DFL Lead The Honorable Connie Bernardy, DFL Lead House Transportation Policy & Finance Committee House Transportation & Regional Governance Policy 243 State Office Building Committee Saint Paul, MN 55155 253 State Office Building Saint Paul, MN 55155 RE: 2017 Guideway Status report Dear Legislators: The Minnesota Department of Transportation, in collaboration with the Metropolitan Council, is pleased to provide the 2017 Guideway Status report as required under 2016 Minnesota Statutes 174.93, subdivision 2. This report updates information for eight guideway corridors currently in operation, construction or design, and thirteen more that are in planning or analysis phase, or that were at the time of the last report in 2015. The capacity analysis looks at regional guideway funding needs and resources related to capital, operations and capital maintenance for the next ten years. If you have specific questions about this report or want additional information, please contact MnDOT’s Brian Isaacson at [email protected] or at 651 234-7783; or, you can contact Met Council’s Cole Hiniker at [email protected] or at 651 602-1748. -

Guideway Status November 2013

2013 Legislative Report Guideway Status November 2013 Prepared by The Minnesota Department of Transportation 395 John Ireland Boulevard Saint Paul, Minnesota 55155-1899 Phone: 651-366-3000 Toll-Free: 1-800-657-3774 TTY, Voice or ASCII: 1-800-627-3529 In collaboration with the Metropolitan Council 390 Robert St. North St. Paul, MN 55101-1805 Phone: 651-602-1000 To request this document in an alternative format Please call 651-366-4718 or 1-800-657-3774 (Greater Minnesota). You may also send an email to [email protected]. Cover Photos: Northstar commuter rail train Red Line (Cedar BRT) vehicle on at Target Field opening day Source: Metro Council Source: Metro Council Green Line (Central Corridor LRT) Blue Line (Hiawatha LRT) in vehicle on tracks for testing operation Source: Streets MN Source: Metro Council 2 Guideway Status Report November 2013 Contents Contents .............................................................................................................................................................. 3 Legislative Request............................................................................................................................................. 5 Statutory Requirement ......................................................................................................................... 5 Cost of Report ...................................................................................................................................... 6 Introduction ....................................................................................................................................................... -

SPEEDLINES, Issue #14, HSIPR COMMITTEE

SECTION NAME 1 International National » p. 18 » p. 6 Different HSR » p. 13 Passenger & Freight Approaches Operations HIGH-SPEED INTERCITY PASSENGER RAIL SPEEDLINES MARCH 2015 ISSUE #14 OF HIGH-SPEED RAIL “CELEBRATE THE PAST, DESIGN THE FUTURE.” Centered around a gigantic complex of railway terminals used by a mind-boggling 3.5 million commuters daily, Shinjuku has everything a megalopolis needs — world-class skyscrapers, shopping and night-time entertainment spots. Shinjuku Station, Tokyo, Japan 2 CONTENTS HIGH-SPEED INTERCITY PASSENGER RAIL SPEEDLINES MAGAZINE 3 CHAIRMAN’S LETTER 4 TOKYO’S 9TH WORLD CONGRESS 5 HUB OF BRITISH RAILWAYS SPEEDLINES 6 PASSENGER & FREIGHT RAIL 9 LEGISLATIVE NEWS 11 CALIFORNIA HSR MOVES AHEAD » p. 4 15 DIFFERENT HSR APPROACHES On the front cover: 17 PASSENGER RAIL PROGRESS The station consists of ten platforms that serve 20 tracks and 12 train links. It has 200 exits including an underground arcade. The JR-East system includes 22 IN THE SPOTLIGHT Yamanote Line, Chūō Main Line, Chūō Rapid Line, Chūō-Sōbu Line, Shōnan-Shinjuku Line and Saikyō Line. Odakyu Electric Railway includes the Odakyu Odawara 23 NEC INSIDER Line while Keio Corporation includes the Keiō and Keiō lines. Tokyo Metro includes the Marunouchi Line and Toei Subway includes the Toei Shinjuku and Toei Ōedo lines. 26 AMERICA CONNECTED The east of Shinjuku station is dedicated for shopping and includes restaurants, department stores and kiosks. 28 RAILROAD HISTORY CHAIR: PETER GERTLER VICE CHAIR: AL ENGEL SECRETARY: ANNA BARRY OFFICER AT LARGE: DAVID CAMERON IMMEDIATE PAST-CHAIR: DAVID KUTROSKY EDITOR: WENDY WENNER PUBLISHER: AL ENGEL ASSOCIATE PUBLISHER: KENNETH SISLAK LAYOUT DESIGNER: WENDY WENNER © 2011-2015 APTA - ALL RIGHTS RESERVED Bustling SPEEDLINES is published in cooperation with the High-Speed & Intercity Passenger Rail of: American Public Transportation Association SHINJUKU 1666 K Street NW People walk through an Washington, DC 20006 underground passage at JR Shinjuku Station, Tokyo, Japan Shinjuku Station. -

State Rail Plan

State Rail Plan DRAFT MARCH 2015 CONTACT LIST MnDOT Dave Christianson, Project Manager Office of Freight and Commercial Vehicle Operations [email protected] 651-366-3710 Dan Krom, Director Passenger Rail Office [email protected] 651-366-3193 Consultant Team Andreas Aeppli, Project Manager Cambridge Systematics, Inc. [email protected] 617-234-0433 Brian Smalkoski Kimley-Horn and Associates, Inc. [email protected] 651-643-0472 MINNESOTA GO STATEWIDE RAIL PLAN Draft Plan PAGE i TABLE OF CONTENTS CONTACT LIST ............................................................................................................................................. I TABLE OF CONTENTS ................................................................................................................................ II EXECUTIVE SUMMARY ............................................................................................................................. VII Overview of the Study .................................................................................................................................... vii Context of the 2015 Rail Plan Update ........................................................................................................... viii The Vision for Minnesota’s Multimodal Transportation System ...................................................................... ix Minnesota’s Existing and Future Rail System ................................................................................................. -

Grants to Political Subdivisions This Document Is Made Available

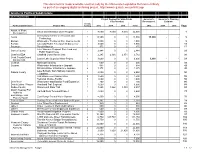

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Grants to Political Subdivisions ($ in Thousands) Project Request for State Funds Governor’s Governor’s Planning ($ by Session) Recommend. Estimate Priority Political Subdivision Project Title Ranking 2012 2014 2016 Total 2012 2014 2016 Page Assoc. of Metro Inflow and Infiltration Grant Program 1 8,000 8,000 8,000 24,000 1 Municipalities International Center of Research and Austin 1 13,500 0 0 13,500 13,500 - - 5 Technology Backus Wastewater Treatment Fac. Improvements 1 1,000 0 0 1,000 9 Bemidji Lakeland Public Television Media Center 1 3,000 0 0 3,000 13 Brownton Flood Mitigation 1 375 0 0 375 17 Lake Waconia Regional Park Land and Carver County 1 2,848 0 0 2,848 22 Public Boat Access Chatfield EDA Chatfield Center for the Arts 1 2,245 2,166 2,371 6,782 26 Cook County/Grand Lutsen Lake Superior Water Project 1 3,600 0 0 3,600 3,600 - - 33 Marais EDA Cosmos Municipal Building 1 600 0 0 600 38 Cuyuna Wastewater Infrastructure Upgrade 1 988 0 0 988 42 Drinking Water Infrastructure Upgrade 2 1,375 0 0 1,375 45 Lake Byllesby Dam Spillway Capacity Dakota County 1 2,050 0 0 2,050 50 Upgrade Trail Bridge over Cannon River 2 1,500 0 0 1,500 53 Regional Morgue Facility 3 7,000 0 0 7,000 56 Deer River Wastewater Stabilization Pond Expansion 1 700 0 0 700 60 Detroit Lakes / Frazee Heartland Trail Segment 1 3,000 0 0 3,000 64 Dodge County Stagecoach State Trail 1 3,245 1,862 3,880 8,987 68 Duluth Seaway Port Garfield Dock Terminal Phase I 1 4,000 0 0 4,000 73 Authority East Range Joint East Range Central Water System 1 4,500 0 0 4,500 76 Powers Board Federal Dam Sanitary Sewer Collection System Replace. -

Ramsey County Regional Railroad Authority 2016-2017 Proposed Budget

Ramsey County Regional Railroad Authority 2016-2017 Proposed Budget Presented to the Regional Railroad Authority for Consideration August 4, 2015 2016-2017 RCRRA Proposed Budget Ramsey County Vision A vibrant community where all are valued and thrive Ramsey County Mission A county of excellence working with you to enhance our quality of life 2 2016-2017 RCRRA Proposed Budget Ramsey County Goals • Strengthen individual, family and community health, safety and well- being through effective safety-net services, innovative programming, prevention and early intervention, and environmental stewardship • Cultivate economic prosperity and invest in neighborhoods with concentrated financial poverty through proactive leadership and inclusive initiatives that engage all communities in decisions about our future • Enhance access to opportunity and mobility for all residents and businesses through connections to education, employment and economic development throughout our region • Model forward-thinking investment, fiscal accountability and transparency through professional operational and financial management. 3 Community Needs The proposed 2016-2017 RCRRA budget is responsive to community needs and Ramsey County goals: • Maintains and nurtures our quality of life by developing a long-range vision of transit services to meet changing needs of the community, ease congestion, improve travel between work and entertainment and increase the economic competitiveness of the county • Provides important services that support a vibrant community at Union Depot, -

2015 Metropolitan Council Performance Evaluation Report

2015 PERFORMANCE EVALUATION REPORT REPORT TO THE MINNESOTA LEGISLATURE May 2016 The Council’s mission is to foster efficient and economic growth for a prosperous metropolitan region. Metropolitan Council Members Cara Letofsky-District 8 Adam Duininck-Chair Edward Reynoso-District 9 Katie Rodriguez-District 1 Marie McCarthy-District 10 Lona Schreiber-District 2 Sandy Rummel-District 11 Jennifer Munt-District 3 Harry Melander-District 12 Deb Barber-District 4 Richard Kramer-District 13 Steve Elkins-District 5 Jon Commers-District 14 Gail Dorfman-District 6 Steven T. Chávez-District 15 Gary L. Cunningham-District 7 Wendy Wulff-District 16 The Metropolitan Council is the regional planning organization for the seven-county Twin Cities area. The Council operates the regional bus and rail system, collects and treats wastewater, coordinates regional water resources, plans and helps fund regional parks, and administers federal funds that provide housing opportunities for low- and moderate- income individuals and families. The 17-member Council board is appointed by and serves at the pleasure of the governor. This publication is printed on recycled paper. On request, this publication will be made available in alternative formats to people with disabilities. Call Metropolitan Council information at 651- 602-1140 or TTY 651-291-0904. Metropolitan Council 2015 Performance Evaluation Report About This Report The Metropolitan Council recognizes performance evaluation as a key tool to ensure that its functions meet their objectives in a timely and cost-effective -

California High-Speed Rail: Die Erste Hochgeschwindigkeitsbahn Der USA Michael Steiner, 14-913-651

Die "Zukunftsmaschine" Eisenbahn; FS 18; Dr. phil. Gisela Hurlimann¨ California High-Speed Rail: Die erste Hochgeschwindigkeitsbahn der USA Michael Steiner, 14-913-651 Einleitung: In der Vorlesung Die \Zukunftsmaschine\ Eisenbahn: Zur Geschichte von Bahn- verkehr und -technologie seit 1950 behandelten wir unter anderem Beispiele von der Planung und Entstehung von Grossprojekten. Beim Beispiel der Metro in Ho Chi Minh gab es diverse Schwierig- keiten, wie beispielsweise die Finanzierung, Koordination oder Probleme bei der Landenteignung. Beim Beispiel der chinesischen Hochgeschwindigkeitsbahn hingegen wurde das Projekt von einer autorit¨aren Regierungen durchgesetzt. Deshalb interessierte ich mich besonders fur¨ die Entste- hung eines Grossprojektes in den USA, einem Land, das auf der einen Seite hoch fortgeschritten, wohlhabend und demokratisch ist, auf der anderen Seite aber bekannt als Autoland und, im Vergleich zu Europa, sehr kritisch dem Staat gegenuber,¨ was sich wohl auch auf Grossprojekte auswirkt. Tats¨achlich gibt es bis heute keine Hochgeschwindigkeitszuge¨ in den USA. Das in die- ser Projektskizze beschriebene Projekt der Hochgeschwindigkeitsbahn in Kalifornien (California High-Speed Rail; CaHSR) ist das erste seiner Art. Grunds¨atzlich w¨aren die Voraussetzungen fur¨ das Projekt gut: ein starkes Bev¨olkerungswachstum ubt¨ Druck auf bestehende Infrastruktur aus, Kalifornien gilt als wohlhabend und ist bekannt fur¨ seine globalen Firmen und die Distanz von Los Angeles nach San Francisco ist ideal fur¨ eine Hochgeschwindigkeitsbahn. Denn die Strecke ist zu weit, um mit dem Auto zu pendeln, und zu kurz fur¨ das Flugzeug. Mit dem Auto h¨atte man rund 6 Stunden, allerdings sind die Strassen h¨aufig uberlastet,¨ und rund 40% der Fluge¨ verkehren mit Versp¨atung. -

State Rail Plan

State Rail Plan DRAFT MARCH 2015 CONTACT LIST MnDOT Dave Christianson, Project Manager Office of Freight and Commercial Vehicle Operations [email protected] 651-366-3710 Dan Krom, Director Passenger Rail Office [email protected] 651-366-3193 Consultant Team Andreas Aeppli, Project Manager Cambridge Systematics, Inc. [email protected] 617-234-0433 Brian Smalkoski Kimley-Horn and Associates, Inc. [email protected] 651-643-0472 MINNESOTA GO STATEWIDE RAIL PLAN Draft Plan PAGE i TABLE OF CONTENTS CONTACT LIST ............................................................................................................................................. I TABLE OF CONTENTS ................................................................................................................................ II EXECUTIVE SUMMARY .............................................................................................................................. VI Overview of the Study ..................................................................................................................................... vi Context of the 2015 Rail Plan Update ............................................................................................................. vi The Vision for Minnesota’s Multimodal Transportation System ..................................................................... vii Minnesota’s Existing and Future Rail System ................................................................................................ -

Passenger Rail Corridor Investment Plan and Tier 1 EIS Appendix A: DRAFT Scoping Decision Document

In the Tier 1 EIS, the technical analysis is PREFACE less detailed and considers impacts to the The Federal Railroad Administration (FRA), corridor as a whole and evaluation of the Minnesota Department of Transportation impacts at a qualitative level. A Tier 1 EIS (MnDOT), and the Olmsted County addresses questions related to the type of Regional Railroad Authority (OCRRA) have service being proposed, including cities and initiated the environmental review process stations served, route alternatives, service for the Rochester-Twin Cities Passenger levels, type of operations, ridership Rail Corridor (Zip Rail). Federal funding will projections and major infrastructure be pursued for this project from the FRA. As components. Environmental analysis is a result the FRA, as the lead federal agency completed at a higher level, but detailed site for this project, is required to undertake information is conducted at the Tier 2 environmental review in compliance with the environmental level, when the alignment National Environmental Policy Act (NEPA). and related service information has been determined and more specific project As the local public agency sponsoring the boundaries can be developed to determine project, MnDOT, as the Responsible effects. Governmental Unit (RGU), and OCRRA must also comply with the requirements of The tiered environmental review process the Minnesota Environmental Policy Act used by the Federal Railroad Administration (MEPA). The FRA, MnDOT, and OCRRA (FRA) reflects that the scale and scope of have determined that the Zip Rail project most rail projects are typically very large. As may have significant environmental impacts. a result, it is more practical to conduct a two-step environmental review with step 1 (Tier 1) staying at a higher level and step 2 REGULATORY BACKGROUND (Tier 2) focused on a more refined This booklet summarizes the regulations assessment.