H2O Retailing / 8242

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

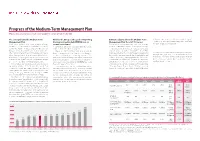

Progress of the Medium-Term Management Plan Making Steady Progress to Reach Our Management Goals Ahead of Schedule

Interview with the President Progress of the Medium-Term Management Plan Making steady progress to reach our management goals ahead of schedule The concept behind the Medium-Term Why has the Group set the goal of improving Estimates adjusted from the Medium-Term fiscal 2016 is expected to exceed the previous plan’s target of Management Plan the interest-bearing debt/EBITDA ratio to Management Plan: fiscal 2016 forecast 7.0 times to 6.8 times. We are steadily taking steps to reach these On the occasion of the management integration of Hankyu around seven times? Current estimates indicate that we will achieve our goals slightly management goals as early as possible. and Hanshin, the Group formulated and announced the six- To answer this question, I will once again explain the manage- ahead of schedule and forecasts have been adjusted accordingly. year Hankyu Hanshin Holdings Group 2007 Medium-Term ment indicators that the Group is aiming for. Operating income for the fiscal 2016 target year is forecast to Management Plan (fiscal 2008–fiscal 2013), for which we estab- The Group’s mainstay railway and real estate leasing surpass the previous plan (¥83.0 billion) by ¥2.0 billion to ¥85.0 Over six years have passed since the management integration lished yearly adjusted estimates and implemented initiatives to businesses generate stable cash flows. Yet, these businesses billion, reflecting currently robust railway operation revenue and of Hankyu Holdings, Inc. and Hanshin Electric Railway Co., Ltd. in achieve the plan’s targets. This plan was intended to clarify the are characterized by the need to own large amounts of fixed higher rental income mainly from the Umeda Hankyu Building. -

H2o Retailing Corporation Financial Report 2020

H2O RETAILING CORPORATION FINANCIAL REPORT 2020 Contents FINANCIAL REPORT for the 101st fiscal term I. Overview of the Company .........................................................................................................................................2 1. Summary of business results ............................................................................................................................................. 2 2. History ............................................................................................................................................................................... 4 3. Description of business ...................................................................................................................................................... 6 4. Overview of subsidiaries and associates............................................................................................................................ 9 5. Information about employees .......................................................................................................................................... 12 II. Overview of Business .............................................................................................................................................14 1. Management policies, management environment and issues to be resolved, etc. ......................................................14 2. Business risk ......................................................................................................................................................15 -

12. Development of Kansai Urban Area (PDF, 113KB)

CORPORATE OPERATING WEST JAPAN RAILWAY COMPANY CONTENTS BUSINESS事事 DATA OTHER OVERVIEW ENVIRONMENT 12 Business Development of Kansai Urban Area DEVELOPMENT OF KANSAI URBAN AREA *New station names are provisional. (As of May 2015) DEVELOPMENT OF THE DISTRICTS AROUND OSAKA STATION Tanigawa JR-West Group Medium-Term Management Plan 2017 Update JR Shichijyo* New station Spring 2019 Yamashina New “LUCUA osaka” Ibaraki Station Kyoto Kusatsu improvement and Kyoto Objectives Revenue target: Total of ¥77.0 billion for LUCUA 1100 and LUCUA development inside New Railway (FY2016) Visitor number target: 70.0 million station Spring 2018 Musuem Spring 2016 • Renovation of the OSAKA STATION CITY North Gate Building Himeji Maya* Nara Line • Securing wide range of customers through superiority of location and New station Shin-Osaka Takatsuki Station Double track Spring 2016 improvement Spring 2023 scale (largest concentration of commercial facilities in Osaka/Umeda Kakogawa Spring 2016 area) and through suitability for excursions • Leveraging promotional system and ability to attract highly popular JR Soujiji* Shin-Kobe specialty stores, cultivated through shopping center operations Kyobashi New station Higashi Himeji* Sannomiya Spring 2018 • Opening stores by Isetan in LUCUA 1100 specializing in fashion and New station Amagasaki Nara sundries, in which Isetan has strength Spring 2016 Kobe Nishi-Akashi Osaka Tennoji • Synergies with railway operations • Taking steps to enhance transport services, such as new rolling stock Oji introduction and timetables -

FTSE Publications

2 FTSE Russell Publications 20 May 2020 FTSE Japan Indicative Index Weight Data as at Closing on 31 March 2020 Constituent Index weight (%) Country Constituent Index weight (%) Country Constituent Index weight (%) Country 77 Bank 0.03 JAPAN Denso Corporation 0.45 JAPAN Isetan Mitsukoshi Holdings 0.06 JAPAN ABC-Mart 0.04 JAPAN Dentsu Inc 0.13 JAPAN Isuzu Motors 0.1 JAPAN Acom 0.05 JAPAN DIC 0.06 JAPAN Ito En 0.09 JAPAN Advantest Corp 0.24 JAPAN Disco 0.17 JAPAN Itochu Corp 0.87 JAPAN Aeon 0.48 JAPAN DMG Mori Seiki 0.03 JAPAN Itochu Techno Solutions 0.08 JAPAN AEON Financial Service 0.04 JAPAN Dowa Holdings 0.04 JAPAN Itoham Yonekyu Holdings 0.02 JAPAN Aeon Mall 0.05 JAPAN East Japan Railway 0.84 JAPAN Iyo Bank 0.04 JAPAN AGC 0.14 JAPAN Ebara 0.06 JAPAN Izumi Co Ltd 0.03 JAPAN Aica Kogyo 0.05 JAPAN Eisai 0.6 JAPAN J Front Retailing 0.06 JAPAN Ain Pharmaciez 0.05 JAPAN Electric Power Development 0.1 JAPAN Japan Airlines 0.06 JAPAN Air Water 0.08 JAPAN Ezaki Glico 0.07 JAPAN Japan Airport Terminal 0.06 JAPAN Aisin Seiki Co 0.13 JAPAN FamilyMart 0.13 JAPAN Japan Aviation Electronics 0.02 JAPAN Ajinomoto Co 0.28 JAPAN Fancl Corp 0.05 JAPAN Japan Exchange Group 0.29 JAPAN Alfresa Holdings 0.1 JAPAN Fanuc 0.8 JAPAN Japan Petroleum Exploration 0.02 JAPAN Alps Alpine 0.06 JAPAN Fast Retailing 0.65 JAPAN Japan Post Bank 0.12 JAPAN Amada 0.08 JAPAN FP Corporation 0.05 JAPAN Japan Post Holdings 0.32 JAPAN Amano Corp 0.05 JAPAN Fuji Electric 0.09 JAPAN Japan Post Insurance 0.07 JAPAN ANA Holdings 0.08 JAPAN Fuji Media Holdings 0.01 JAPAN Japan Steel -

Hallyeo National Marine Park View Ropeway, Tongyeong City, South Korea TOURISM SCOPE a Contents

2015. Vol. 34 ISSN 1739-5089 The Official Magazine of the Tourism Promotion Organization for Asia Pacific Cities Hallyeo National Marine Park View Ropeway, Tongyeong city, South Korea TOURISM SCOPE A Contents 02 Special Theme Exploration of Ho Chi Minh City 06 City Inside Yogjakarta, Encounter with Ancient Java 10 Focus On Walking Trail of Ulsan Yeongnam Alps 14 Concept Travel Heaven for Shopaholics The Best Shopping Malls of the World 18 TPO People Mr. Kim Dong-Jin, Mayor of Tongyeong city, South Korea 20 TPO News & Info 22 Zoom in Festival Tourism Promotion Organization for Asia Pacific Cities TPO is a network among cities in the Asia Pacific region and is an international tourism organization established for the development of the tourism industry. TPO exchanges tourism information between member cities to promote the tourism industry, and also carries out projects including tourism product development, joint marketing projects, and tourism industry education as well as human resources development. 75 city governments and 38 Industry members currently participate in as members of the TPO. Industry members consist of travel industry related associations, research institutes, and destination marketing organizations(DMO). TPO strives for the development of sustainable tourism and city tourism within the Asia Pacific region. TOURISM SCOPE 01 SPECIAL Exploration of Ho Chi Minh City A colony of France in the past, the city is full of vintage architectures and tasty food that is loved by people all over the world. With beautiful tree-lined street sceneries, it is also known as the ‘Paris of the East’. The city which is also the center of the financial district of Vietnam is called Ho Chi Minh City About Ho Chi Minh City Location 100km North West of Cap Saint Jacque, South of Annamese Cordillera in Southern Vietnam Area 2,099km2 Population 7,396,446 (2010) Weather A year-long hot weather with extremely high temperature and humidity. -

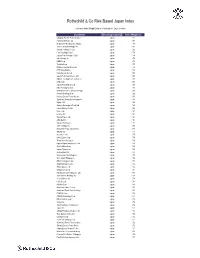

Rothschild & Co Risk-Based Japan Index

Rothschild & Co Risk-Based Japan Index Indicative Index Weight Data as of January 31, 2020 on close Constituent Exchange Country Index Weight (%) Chugoku Electric Power Co Inc/ Japan 1.01 Yamada Denki Co Ltd Japan 0.91 McDonald's Holdings Co Japan L Japan 0.88 Sushiro Global Holdings Ltd Japan 0.82 Skylark Holdings Co Ltd Japan 0.82 Fast Retailing Co Ltd Japan 0.78 Japan Post Holdings Co Ltd Japan 0.78 Ain Holdings Inc Japan 0.78 KDDI Corp Japan 0.77 Toshiba Corp Japan 0.75 Mizuho Financial Group Inc Japan 0.74 NTT DOCOMO Inc Japan 0.73 Kobe Bussan Co Ltd Japan 0.72 Japan Post Insurance Co Ltd Japan 0.69 Nippon Telegraph & Telephone C Japan 0.69 LINE Corp Japan 0.69 Japan Post Bank Co Ltd Japan 0.68 Nitori Holdings Co Ltd Japan 0.67 MS&AD Insurance Group Holdings Japan 0.66 Konami Holdings Corp Japan 0.66 Kyushu Electric Power Co Inc Japan 0.65 Sumitomo Realty & Development Japan 0.65 Fujitsu Ltd Japan 0.63 Suntory Beverage & Food Ltd Japan 0.63 Japan Airlines Co Ltd Japan 0.62 NEC Corp Japan 0.61 Lawson Inc Japan 0.60 Sekisui House Ltd Japan 0.60 ABC-Mart Inc Japan 0.60 Kyushu Railway Co Japan 0.60 ANA Holdings Inc Japan 0.59 Mitsubishi Heavy Industries Lt Japan 0.58 ORIX Corp Japan 0.57 Secom Co Ltd Japan 0.57 Seiko Epson Corp Japan 0.56 Trend Micro Inc/Japan Japan 0.56 Nippon Paper Industries Co Ltd Japan 0.56 Suzuki Motor Corp Japan 0.56 Japan Tobacco Inc Japan 0.55 Aozora Bank Ltd Japan 0.55 Sony Financial Holdings Inc Japan 0.55 West Japan Railway Co Japan 0.54 MEIJI Holdings Co Ltd Japan 0.54 Sugi Holdings Co Ltd Japan 0.54 Tokyo -

H2O Retailing / 8242

H2O Retailing / 8242 COVERAGE INITIATED ON: 2020.04.30 LAST UPDATE: 2021.07.15 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. H2O Retailing / 8242 RCoverageCoverage LAST UPDATE: 2021.07.15 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 6 -

Fuji Media Holdings, Inc. (The "Company") Will Be Held As Described Below and You Are Cordially Invited to Attend the Meeting

(Translation) Securities Code: 4676 June 1, 2017 To the Shareholders: NOTICE OF THE 76TH ORDINARY GENERAL MEETING OF SHAREHOLDERS Dear Shareholders: We would like to express our appreciation for your continued good offices. Please take notice that the 76th Ordinary General Meeting of Shareholders of Fuji Media Holdings, Inc. (the "Company") will be held as described below and you are cordially invited to attend the meeting. Since voting rights can be exercised in writing or via the Internet even if you are not present at the meeting, please go over the Reference Documents for the General Meeting of Shareholders set forth below and exercise your voting rights. Yours very truly, Hisashi Hieda, Chairman and Chief Executive Officer Fuji Media Holdings, Inc. 4-8, Daiba 2-chome, Minato-ku, Tokyo Description 1. Date and hour: June 28 (Wednesday), 2017, at 10:00 a.m. (Reception will start at 9:00 a.m.) 2. Place: Grand Nikko Tokyo Daiba (Formerly called Hotel Grand Pacific Le Daiba) B1, Palais Royal 6-1, Daiba 2-chome, Minato-ku, Tokyo 3. Matters forming the objects of the meeting: Matters to be reported: 1. Report on the business report, the consolidated financial statements and the results of audit of the consolidated financial statements by the account auditors and the Audit & Supervisory Board for the 76th fiscal year (from April 1, 2016 to March 31, 2017) 2. Report on the non-consolidated financial statements for the 76th fiscal year (from April 1, 2016 to March 31, 2017) Matters to be resolved: Proposition No. 1: Appropriation of retained earnings Proposition No. -

H2O Retailing / 8242

R H2O Retailing / 8242 COVERAGE INITIATED ON: 2020.04.30 LAST UPDATE: 2021.09.01 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. H2O Retailing / 8242 RCoverageCoverage LAST UPDATE: 2021.09.01 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- -

January 22, 2014 Update Financial Results Briefing Materials for The

Table of Contents 1. Executive Summary ・・・・・・・・・・ ・・・・・・・・・ 2 2. External Growth Strategies ・・・・・・・・・・・・・・・・ 11 3. Internal Growth Strategies・・・・・・・・・・・・・・・・・ 20 4. Financial Strategies ・・・・・・・・・・・・・・・・・・・ 28 5. Overview of Financial Results for the 17th Fiscal Period ・・・・ 33 6. APPENDIX・・・・・・・・・・・・・・・・・・・・・・・・ 40 This material includes forward-looking statements based on present assumptions and future outlook. Actual results may differ from the forward-looking statement values due to various factors. This material is not intended as a solicitation to acquire investment securities of Hankyu REIT nor is it intended as a solicitation to sign contracts relating to transactions of other financial instruments. When undertaking any investment, please do so based on your own judgment and responsibility as an investor. Before purchasing investment securities of Hankyu REIT, please consult with a securities company that is a “Type I Financial Instruments Business Operator.” This material is an English translation of the original, which was issued in the Japanese language. There are sections that display property names in abbreviated form. 1 1. Executive Summary 2 1-1. Towards the Growth Path April 2013 November 2013 Asset replacements Acquisition of new properties Improvement of Continuous acquisition of properties portfolio’s health 127.8 billion yen Acquisition of Kita-Aoyama 3 cho-me 121.3 billion yen Building HEP (part), NU sold 116.1 billion yen 18.8bn 17.3bn 50.9bn 41.2bn Acquisition of Hankyu Corporation Head Office Building 41.1bn June 2013 2nd PO Return to growth path 13.0bn 30.9bn Acquisition of AEON MALL 13.0bn SAKAIKITAHANADA and MANDAI Toyonaka Honan Store Acquisition of HANKYU 13.0bn NISHINOMIYA GARDENS 54.6bn 44.6bn 26.3bn Asst size (total acquisition price) End of 15th FP End of 16th FP End of 17th FP (End of Nov. -

The Railway Market in Japan

www.EUbusinessinJapan.eu The Railway Market in Japan September 2016 Lyckle Griek EU-JAPAN CENTRE FOR INDUSTRIAL COOPERATION - Head office in Japan EU-JAPAN CENTRE FOR INDUSTRIAL COOPERATION - OFFICE in the EU Shirokane-Takanawa Station bldg 4F Rue Marie de Bourgogne, 52/2 1-27-6 Shirokane, Minato-ku, Tokyo 108-0072, JAPAN B-1000 Brussels, BELGIUM Tel: +81 3 6408 0281 - Fax: +81 3 6408 0283 - [email protected] Tel : +32 2 282 0040 –Fax : +32 2 282 0045 - [email protected] http://www.eu-japan.eu / http://www.EUbusinessinJapan.eu / http://www.een-japan.eu www.EUbusinessinJapan.eu Contents 1. Executive summary .................................................................................................................................................... 2 2. Introduction ............................................................................................................................................................... 3 3. Market structure........................................................................................................................................................ 4 a. Network overview (technical characteristics) ...................................................................................................... 4 b. Public & private operators .................................................................................................................................... 6 c. Large operators ................................................................................................................................................... -

Message to Our Shareholders 2007

Message to Our Shareholders 2007 Hankyu Department Stores, Inc. Contents ・To Our Shareholders ・The shift to a holding company structure ・Management integration with Hanshin Department Store ・Topics ・Redevelopment project near JR Oimachi Station ・Uni-President Hankyu Department Store in Kaohsiung, Taiwan ・Preparing to expand the scale of supermarket operations ・Launch of joint use of Persona Card and Hanshin's Emerald Card ・Settlement report (from 1st April 2006 to 31st March 2007) ・Corporate data To Our Shareholders During fiscal 2006, our Group saw both revenues and earnings increase. Performance was driven by curtailment of revenue losses arising from diminished sales space following the launch of reconstruction works at Umeda Main Store in the previous fiscal year, by increased revenues at other branches, and by opening of new supermarkets and the acquisition of retailer Nissho Corp. (now Hankyu Nissho Store). We made steady progress in the development of business infrastructure and expansion of operational scale as we pursued long-term business goals, grouped as the Grand Prix 10 (GP10) Plan. In addition to the acquisition of Nissho, we decided to open a new store in New Hakata Station Building, scheduled to open its doors in the spring of 2011, and rebuild multiple-use buildings within the redevelopment project near JR Oimachi Station in Tokyo’s Shinagawa Ward. We also established of Hanshoku Co., Ltd. as an President and Representative Director intermediary holding company to oversee our growing supermarket operations. Nobuaki Nitta In negotiations launched in September 2006 for our business alliance with The Hanshin Department Store, Ltd., we came to the conclusion that integrating our businesses would be the most efficient way forward for both of us.