Chairman's Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Games Workshop Group Plc

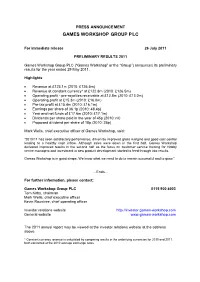

PRESS ANNOUNCEMENT GAMES WORKSHOP GROUP PLC For immediate release 26 July 2011 PRELIMINARY RESULTS 2011 Games Workshop Group PLC (“Games Workshop” or the “Group”) announces its preliminary results for the year ended 29 May 2011. Highlights • Revenue at £123.1m (2010: £126.5m) • Revenue at constant currency* at £122.8m (2010: £126.5m) • Operating profit - pre-royalties receivable at £12.8m (2010: £13.0m) • Operating profit at £15.3m (2010: £16.0m) • Pre-tax profit at £15.4m (2010: £16.1m) • Earnings per share of 36.1p (2010: 48.4p) • Year end net funds of £17.6m (2010: £17.1m) • Dividends per share paid in the year of 45p (2010: nil) • Proposed dividend per share of 18p (2010: 25p) Mark Wells, chief executive officer of Games Workshop, said: “2010/11 has seen satisfactory performance, driven by improved gross margins and good cost control leading to a healthy cash inflow. Although sales were down in the first half, Games Workshop delivered improved results in the second half as the focus on customer service training for Hobby centre managers and investment in new product development started to feed through into results. Games Workshop is in good shape. We know what we need to do to remain successful and to grow.” …Ends… For further information, please contact: Games Workshop Group PLC 0115 900 4003 Tom Kirby, chairman Mark Wells, chief executive officer Kevin Rountree, chief operating officer Investor relations website http://investor.games-workshop.com General website www.games-workshop.com The 2011 annual report may be viewed at the investor relations website at the address above. -

Fictional Reality Issue 8

Fictional Reality June 2002 Issue 08 Table of Contents Ah, Summer in Texas. Actually, it’s not to bad right now, but by August we’ll be just dripping with sweat. I guess I’ll have to spend more time inside painting figures and Editorial / TOC 1 playing games. Well, that’s not all that will be taking up Standing Orders: Age of Battles 2 my free hours during the Summer. Baby Megan is Miniature Reviews preparing for her arrival and will join the rest of the brood Wizards of the Coast: Chainmail 5 sometime in late August or early September. That puts a Excelsior: Iron Claw 7 wee dent into my gaming and painting schedules, but also nixes any plans I had of attending Gen Con this year. If Rackham: Confrontation 8 anyone that gets to Gen Con this year would like to write Holistic Design: Fantasy Encounters 9 up a report I’d love to put it in the next issue. Next year Mithril: Lord of the Rings 10 may work out better for me anyway. My oldest son, Excalibur Miniaturen: Fearless 12 Bradley, has been gaming with my Dungeons and Pulp Figures: Lost Tribes / Personalities 15 Dragons group for a while now and has also been trying Reaper Miniatures 16 his hand at some painting. He’s getting the hang of things Larry Leadhead 11 and by next year he should be a pro. Ok, next year will be Game Reviews a go. We should actually start planning for it now. Road Games Workshop: Warhammer Skirmish 17 trip or catch a plane? Excalibur Miniaturen: Magic Challenge 18 Holistic Design: Fading Suns d20 RPG 19 Planning is a huge part of a rather large terrain building article this issue. -

Players Helped Develop Computer Games in Britain(Paul Mason)

A Case Study of the Influence of Fandom: How Role-players Helped Develop Computer Games in Britain(Paul Mason) A Case Study of the InÀuence of Fandom: How Role- players Helped Develop Computer Games in Britain Paul Mason Abstract Fandom is widely regarded as a form of excessive consumption, an essentially reactive activity. Work in the ¿eld of fan studies has drawn attention to its creative aspects, but these are still often deemed to be expanding on or embellishing the work of creative professionals. The present study explores the ambiguity of the boundary between fan creators and professional creators in order to illustrate how fans were instrumental in the creation of a new form of expression. It charts aspects of the history of computer games development in the UK, and shows how that development was driven by the interplay between fans and professionals in related ¿elds. Introduction In a basement room at a school in Britain in the early 1970s sits a strange machine. At ¿rst glance it seems to be a large typewriter, but closer inspection reveals it to be a teleprinter. It is connected to the mainframe computer of the city treasurer’s department. A schoolboy is operating the teleprinter, periodically typing in short commands, and then watching intently as the results of those commands are printed out: a grid formed of dots occasionally replaced by other symbols, with some terse accompanying text and data. The boy is playing Blake's 7, attempting to steer the spaceship Liberator and successfully defeat pursuing Federation craft. The teachers at the school are aware of student use of the computer terminal and its teleprinter, but allow it, perhaps because they are unaware that it is being used to play a game, or even because the whole concept of games using computers is so new that it has not yet been recognized as a bad thing. -

Campaigns of Legend Think ‘Battle of Legend’ but Even Bigger! by Ken South

Campaigns of Legend Think ‘Battle of Legend’ but even bigger! By Ken South With the Warmaster battles of legend series being a popular part 1 There will be no army definitive lists as such but there will be of the Fanatic literary arsenal I thought that it might well be notes of army sizes as well as sections covering special rules worth exploring the history of the Warhammer world and along with special units and special characters for each battle recreating some of the campaigns that have helped shape the in the campaign. Warhammer world, as we know it. 2 The battles and encounters featured in the col have all been Bearing that in mind I delved into deleted army books and referenced from existing Games Workshop material and as thumb worn copies of White Dwarf to find accounts of battles such was initially designed for Warhammer so although some long since forgot about yet so important to the world that is of the units mentioned may not be available you could convert Warhammer. or repaint existing models in the Warmaster range. The relentless wars of the Empire and the Orcs have been retold 3 The campaign system used to link the battles within the and reinvented since the earliest editions of the Warhammer campaign is the Warmaster adaptation of the Mighty Empires game so I thought that this would be a good place to start my that the late Steve Hambrook worked on. research and after reading trough many books now sadly out of 4 There will also appear army and allies rules this is to allow for print I came across the name Azhag. -

White Dwarf Index

NOTES ON THIS INDEX This Index lists the most important articles that have been published in White Dwarf from issue 68 to issue 251. There are several points that I would like to make about this Index. • The Index only lists the main articles published in each issue, it does not list the Games Workshop News, Mail Order or What’s Happening at the GW Stores (as features in these articles will be out of date and largely irrelevant). • From Issues 110 onwards all of the articles are categorised according to which game they are relevant to, there is a column for Warhammer 40,000 (commonly referred to as WH40K) articles, a column for Warhammer Fantasy Battle (referred to as WHFB or just Warhammer), one for Various Games (all of the other games WD features), one for Terrain articles (just terrain, not painting guides) and one for Miscellaneous Articles and Battle reports. For issues 102 and earlier there are only three columns. One for Various Games that are featured (including Warhammer 40,000 and Warhammer Fantasy Battle) one for Roleplay Games like Warhammer Fantasy Roleplay (commonly referred to as WFRP) and lastly, one for Miscellaneous Articles and Battle reports. This is because, back then, there wasn’t always a WH40K and/or WHFB article. There was however, a plethora of other games produced by other companies as well as lots of Roleplay games that are just never seen now. If things carry on as they are, I might have to change the columns from Issues 248 onward to just include just WH40K, WHFB and Miscellaneous Articles, because that’s what White Dwarf seems to be completely dedicating itself to these days… • Since Games Workshop re-releases games every so often (generally Warhammer 40,000 and Warhammer Fantasy Battle), articles about such games are only relevant to the edition of the game that was around at the time when that issue was printed. -

The Newsletter Chief Muppet Managed to Survive Have Ended up Being Pushed As Always I’M on the Look out Christmas with My Sanity Back About a Month

The Sad Muppet Society presents... Issue 21, Winter 2005 T HE NEWSL ETTER THE MARATHON OF GLEBE THE SAD MUPPET SOCIETY G AMESDAY VI|NEWBURY NECRONS|CHEF’ S COOKER|THE LEAGUE 2004 O PEN TOURNAMENT II|GLEBE WARS|SQUIGGOTH 101 Page 2 Issue 21, Winter 2005 EDITIORAL Contents (THE RAT’ S RAMBLINGS) The Rat’s Ramblings 2 Happy New Year and Freeth for winning best I’m back! More rubbish welcome to the first sportsman in the 2004 from Chief Muppet Newsletter of 2005! league, and Matthew Pinto In order to work around a for finally claiming the Pixie Events Diary 3 few other things in my life Jam Trophy! Incoming 4 (Christmas, work, college, Well done guys! Regarding Retribution etc, etc), the publishing Richard Kerry and ASMOH 05 Despite everything, I’ve dates for the Newsletter Chief Muppet managed to survive have ended up being pushed As always I’m on the look out Christmas with my sanity back about a month. So the Muppet Army 6 for more articles so if you’ve intact, and Halo 2 finished! spring edition should be Got a painted army? got any new rules to test out, However, ten days away from rolling out in April, the Earn the kudos you want to review something, the office and I’ve managed Summer edition in July, and deserve! write a story, or have any to paint approximately one the Autumn edition in other interesting article in Gamesday 6 7 model. October. Sorry about that buts that’s the way the mop mind, email me and you Nick examines the Hum, that next army may might see it in here next flops. -

Dragon Magazine #169

SPECIAL ATTRACTIONS Issue #169 Vol. XV, No. 12 Preparation is everything May 1991 9 A collection of helpful hints for AD&D® game heroes. New Weapons For Old Jordan Clarke Hayes Publisher 10 Get a claymore for your dwarf and a flamberge for your fighter! James M. Ward Creative Casting Joel E. Roosa Editor 16 Tensers floating disk as a flying missile platform? You bet! Roger E. Moore Learn Something New Every Day Gordon R. Menzies Fiction editor 20 Whether youd like to learn alchemy or street fighting, heres the Barbara G. Young article you need. The Strategy of Tactics Jordan Clarke Hayes Assistant editor 26 Should you bash the ogre or back off a bit? New melee tactics for the Dale A. Donovan AD&D® game. Art director Larry W. Smith O THER FEATURES Production staff Gaye OKeefe Angelika Lokotz The Voyage of the Princess Ark Bruce A. Heard Tracey Zamagne 41 Nothing went right in Jahoreuntil the Princess and crew appeared. Subscriptions The Role of Books John C. Bunnell Janet L. Winters 50 The last of the unicorns returns in a new edition. The MARVEL® Phile Dale A. Donovan U.S. advertising 55 Whos the cycle-riding, flaming-skulled hero we all know and love? Roseann Schnering The Role of Computers Hartley, Patricia, and Kirk Lesser U.K. correspondent 61 Elvira needs your help! You see, theres this old haunted mansion. and U.K. advertising Bronwen Livermore Swordfish and Saucery fiction by Deborah Millitello 66 Even the cleverest of spells sometimes has a little catch. Role-playing Reviews Ken Rolston 72 How do you spell magic? A look at some all-new magic supplements for gaming. -

Best Of... Warmaster Campaign

WM_Annual_072_085 7/20/04 12:17 PM Page 72 WARMASTER CAMPAIGN By David Simpson & Friends THE TALE OF A LARGE MAP, SMALL Empire general that I was, I jumped at the MODELS AND THE MEN THAT PLAY chance to show the superior firepower of the WITH THEM Empire’s artillery and took part with great It’s not what you think, nothing to do with gusto and enthusiasm. catwalks and supermodel abduction plots for Well anyway, so as not to veer too far off the nefarious purposes. This is in fact the story of subject I have always loved map based an ongoing Warmaster campaign that was run campaigns and when I saw the first preview at the Brent Cross GW store. pictures of Warmaster in White Dwarf I started Firstly, I suppose I should introduce myself, I going a bit loopy with visions of masses of am David Simpson and have been playing with troops stoically marching over the massacred toy soldiers for about ten years which is almost bodies of their foes conquering all opposition. as long as some of the younger sprogs have When I finally got my hands on a copy of been alive. Conversely, there are even a few Warmaster I realised just how perfect a game it rare examples of regulars (or GW staff) that was to be integrated into a campaign. So my have been playing with little painted men for mate Dan and I started to pester Dean, the longer than I myself have graced this earth, a store manager, for a Warmaster campaign. -

1 in the United States District Court for The

Case: 1:10-cv-08103 Document #: 147 Filed: 01/19/12 Page 1 of 25 PageID #:1533 IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS EASTERN DIVISION GAMES WORKSHOP LIMITED, Plaintiff, Civil Action No. 1:10-cv-8103 v. CHAPTERHOUSE STUDIOS LLC and JON JURY TRIAL DEMANDED PAULSON d/b/a PAULSON GAMES Defendants. SECOND AMENDED COMPLAINT FOR COPYRIGHT INFRINGEMENT, TRADEMARK INFRINGEMENT, TRADEMARK DILUTION, UNFAIR AND DECEPTIVE TRADE PRACTICES, AND UNFAIR COMPETITION Games Workshop Limited, by its attorneys, FOLEY & LARDNER LLP, for its First Amended Complaint against Chapterhouse Studios LLC and Jon Paulson (collectively “Defendants”), alleges as follows: PARTIES AND JURISDICTION 1. Games Workshop Limited is a United Kingdom corporation and a subsidiary of Games Workshop Group, plc, which has numerous store locations in and around Chicago, Illinois, which is its single largest selling market in the United States. 2. Upon information and belief, Chapterhouse Studios LLC is a Texas limited liability company with offices at 3930 Glade Road, Suite 108 #174, Colleyville, Texas, 76034. 3. Upon information and belief, Jon Paulson is an individual and the principal owner of Paulson Games, having an address at 2232 College Road, Downers Grove, Illinois, 60516. 1 4847-7177-8316 Case: 1:10-cv-08103 Document #: 147 Filed: 01/19/12 Page 2 of 25 PageID #:1534 4. This is an action for copyright infringement under 17 U.S.C. § 101 et seq.; trademark infringement under 15 U.S.C. § 1114(1) and Illinois common law; for use of false designations of origin under 15 U.S.C. § 1125(a); for dilution under 15 U.S.C. -

The Science Fiction and Fantasy Games Magazine

Issue No.1 June/July 1977 60p ($2.00) 2nd Reprint August 1979 The Science Fiction and Fantasy Games Magazine THE MONSTERMARK METAMORPHOSIS ALPHA COMPETITIVE D&D Issue * Monster MalignitY in D&D * Review and sucJgactions * An Introduction Thane Tostl'g The Ultimate fighting man A new fantasy game from the Company that brought you Olympians, Heroes and Horrors. Send 15p for lists . Tostig fantasy rules available in June - 70p inc. p&p. Minot's Miniature Armoury P.O. Box 25 Borehamwood Herts WD6 3BP. (Tel : 01-953 4107) U .S.A. & Canada : Barry Minot Miniatures Corp. P.O. Box 124 Garden City New York 11530 U .S.A. EVIL, MEAN, AND ROTTEN. A fantasy game for the bad guys? Yea, verily. Monsters! Monsters! is the new fantasy role-playing game from Metagaming Concepts . No more good-guy heroes . In Monsters! Monsters!, you become a monster character - come up from the dungeons - stalk into town - and wreak havoc . The eviller you are, the more experience points you'll earn . CHRIS HARtEY would like to wish WHITE DWARF a happy first issue and a prosperous future . but since we have a little space left (sorry 'bout the pun) FOR ONLY £2.25 You can get 1) Five issues of OVERKILL 2) A free mailing service giving immediate news of new SF and fantasy games on the market probably before anyone else gets them. (e.g . we were selling GODSFIRE in Feb.) 3) A 5%t, discount on any order off the manufacturers retail price for GDW, FACT And FANTASY, METAGAMING, TSR, FANTASY GAMES UNLIMITED and lots of others. -

Games Day Programme 2010 Update

LG ARENA PAVILION hoose your battle cry, pledge your allegiance and prepare for a filled with their range of resin miniatures, vehicles and more. The Forge he Pavilion is the creative hub of Games Day; where artists, It takes a whole team of talented individuals to produce our books, fight to the death! The LG Arena plays host to our participation World Studio team will also be on hand to answer your questions. painters, sculptors and designers come together to deliver a truly magazines and miniatures, and Games Day is your opportunity to meet gaming this year, and our stores and clubs have pulled out all the awe-inspiring show. these clever guys and gals face to face. So, if you’ve ever wanted to quiz an At the Black Library stand, all the latest titles will be on sale and you’ll be stops to make sure these battles are ones to be remembered. This ‘Eavy Metal painter on blending techniques, or ask one of our Games able to meet your favourite authors and cover artists in the signing area. Golden Demon is first on many a person’s must-see list, and it’s is also the place to play your Bring and Battle games this year, so T Developers in-depth questions about your favourite army, then the Design C not difficult to see why. Rarely will you be able to experience such an array find yourself an opponent and ready your troops… Games Day wouldn’t be complete without the Hobby Zones. Whether you of exquisitely painted miniatures up close and personal, and whether you Studio area is the place for you. -

General Historical Topics’, Such As Campaign Dynamics and Ancient Historiography

SLINGSHOT INDEX INTRODUCTION This index is based on the Slingshot Index 1965-1995 compiled by Philip Sabin and Derek Whittenbury. This has been updated to include all articles from 1996-2007 by Richard Jeffrey-Cook. It is arranged by Subjects and gives full page references to indicate the length of articles. It gives details of authors and titles, and so offers a clearer sense of the content of individual contributions. Indexing Slingshot is a subjective process. Individual contributions often range over multiple subjects in history and wargaming, making them very hard to classify under a single heading. Debates and ideas bounce back and forth from issue to issue, rather than being neatly summarised in a single specific piece. Some letters or reviews may be longer and more detailed than some formal articles, while even short notes may contain invaluable corrections or other nuggets of information. Some material becomes dated and irrelevant almost immediately, while other material (even from the earliest issues) has a timeless value and significance. In the face of these problems, the following Index eschews firm rules and embodies some highly subjective judgements in order to make the material more traceable. The basic principle is a two-tier approach, including all pieces of around one page or more. From issue 153, a second layer of detail is added, including shorter and more ephemeral pieces. The index is organised on regional, chronological and thematic rather than alphabetic lines. It is organised in ten sections that move broadly from historical through to wargaming topics, though many pieces include an element of both.