The Dupont Proxy Battle: Successful Defense Measures Against Shareholder Activism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Appendix Wuthering Heights Screen Adaptations

Appendix Wuthering Heights Screen Adaptations Abismos de Pasión (1953) Directed by Luis Buñuel [Film]. Mexico: Producciones Tepeyac. Arashi Ga Oka (1988) Directed by Kiju Yoshida [Film]. Japan: Mediactuel, Saison Group, Seiyu Production, Toho. Cime Tempestose (2004) Directed by Fabrizio Costa [Television serial]. Italy: Titanus. Cumbres Borrascosas (1979) Directed by Ernesto Alonso and Karlos Velázquez [Telenovela]. Mexico: Televisa S. A. de C. V. Dil Diya Dard Liya (1966) Directed by Abdul Rashid Kardar [Film]. India: Kary Productions. Emily Brontë’s Wuthering Heights (1992) Directed by Peter Kosminsky [Film]. UK/USA: Paramount Pictures. Emily Brontë’s Wuthering Heights (1998) Directed by David Skynner [Television serial]. UK: ITV, Masterpiece Theatre, PBS. Hihintayin Kita Sa Langit (1991) Directed by Carlos Siguion-Reyna [Film]. Philippines: Reynafilms. Hurlevent (1985) Directed by Jacques Rivette [Film]. France: La Cécilia, Renn Productions, Ministère de la Culture de la Republique Française. Ölmeyen Ask (1966) Directed by Metin Erksan [Film]. Turkey: Arzu Film. ‘The Spanish Inquisition’ [episode 15] (1970). Monty Python’s Flying Circus [Television series]. Directed by Ian MacNaughton. UK: BBC. Wuthering Heights (1920) Directed by A. V. Bramble [Film]. UK: Ideal Films Ltd. Wuthering Heights (1939) Directed by William Wyler [Film]. USA: United Artists/ MGM. Wuthering Heights (1948) Directed by George More O’Ferrall [Television serial]. UK: BBC. Wuthering Heights (1953) Directed by Rudolph Cartier [Television serial]. UK: BBC. Wuthering Heights (1962) Directed by Rudolph Cartier [Television serial]. UK: BBC. Wuthering Heights (1967) Directed by Peter Sasdy [Television serial]. UK: BBC. Wuthering Heights (1970) Directed by Robert Fuest [Film]. UK: American International Pictures. Wuthering Heights (1978) Directed by Peter Hammond [Television serial]. -

Man of La Mancha

STUDY GUIDE MAN OF LA MANCHA DIRECTED BY JULIA RODRIGUEZ-ELLIOTT MAR.5 – MAY 20, 2017 Study Guides from A Noise Within A rich resource for teachers of English, reading arts, and drama education. Dear Reader, We’re delighted you’re interested in our study guides, designed to provide a full range of information on our plays to teachers of all grade levels. A Noise Within’s study guides include: • General information about the play (characters, synopsis, timeline, and more) • Playwright biography and literary analysis • Historical content of the play • Scholarly articles • Production information (costumes, lights, direction, etc.) • Suggested classroom activities • Related resources (videos, books, etc.) • Discussion themes • Background on verse and prose (for Shakespeare’s plays) Our study guides allow you to review and share information with students to enhance both lesson plans and pupils’ theatrical experience and appreciation. They are designed to let you extrapolate articles and other information that best align with your own curricula and pedagogic goals. More information? It would be our pleasure. We’re here to make your students’ learning experience as rewarding and memorable as it can be! All the best, Alicia Green Pictured: Donnla Hughes, Romeo and Juliet, 2016. PHOTO BY CRAIG SCHWARTZ. DIRECTOR OF EDUCATION Man of La Mancha TABLE OF Character List ...........................4 CONTENTS Musical Numbers ........................................5 Synopsis ...............................................6 Playwright, Lyricist, Composer -

![2021 Proxy Statement | 1 [THIS PAGE INTENTIONALLY LEFT BLANK] PROXY STATEMENT SUMMARY](https://docslib.b-cdn.net/cover/9961/2021-proxy-statement-1-this-page-intentionally-left-blank-proxy-statement-summary-1989961.webp)

2021 Proxy Statement | 1 [THIS PAGE INTENTIONALLY LEFT BLANK] PROXY STATEMENT SUMMARY

974 Centre Road Wilmington, DE 19805 March 26, 2021 LETTER FROM CHAIRMAN AND CHIEF EXECUTIVE OFFICER Dear Investor: On behalf of the Board of Directors (the “Board”), we invite you to attend the Annual Stockholder Meeting of Corteva, Inc. (“Annual Meeting”), which will be held on May 7, 2021 at 10:00 a.m. Eastern Daylight Time. Please see instructions below regarding how to attend and vote your shares. Our Plan Is Working Since Corteva was launched as a leading global agriculture company in June 2019, our strategy has focused on delivering value to our stockholders by generating advanced innovations for growers through our industry-leading pipeline, leveraging our unparalleled route-to-market, enhancing our product mix, advancing cost and productivity actions, and maintaining a balanced approach to capital allocation. Our strong results for the fourth quarter and the full year 2020 demonstrate that our plan is working. We know we have more work to do and 2021 is the year we expect our top line and cost initiatives will accelerate their impact on earnings, and put us fully on-track to achieve mid-term targets. Sustainability is Our Foundation As an agriculture company, our innovation on behalf of customers and our commitment to help them do more with less is the foundation of our ability to deliver long-term value for our stockholders and help sustain the planet. We are proud to contribute concretely to the many communities where we operate and to dedicate our scientific resources to generating a safe, secure food supply now and for the future. -

Richard Harris Pdf, Epub, Ebook

RICHARD HARRIS PDF, EPUB, EBOOK Michael Feeney Callan | 256 pages | 30 Nov 2004 | PAVILION BOOKS | 9781861057662 | English | London, United Kingdom RICHARD HARRIS PDF Book Around the time of his death, he worried he'd only be remembered for his role as Professor Dumbledore in the first two Harry Potter movies. Print Cite. Trojan Eddie John Power If ever I was miscast in my life, it was in the role of husband. Self uncredited. In , while looking for a bedsit in London, he saw a board behind the window of a shop that listed all the rooms it had for rent. The British Heroes Box Set. Star Sign: Libra. The DuPont Show of the Month Flip the Bird? Grizzly Falls Old Harry New This Month. Greatest Ever Heroic Movies Collection. He described the shoot as "nightmarish" and called the film "a total fucking disaster". Harris took the role because the money was too good to pass up. British Actor. He caught the eye of critic Kenneth Tynan who once bracketed him with Albert Finney and Peter O'Toole as one of the three best young actors on the British stage. Birth Name: Richard St. Alive and Kicking. Advising BT Financial Group in relation to its successful defence of the landmark ASIC prosecution concerning the delineation between personal and general advice with widespread ramifications for the wealth and financial advice industry. What's New to Stream in January. Share this page:. In Act V, Macbeth turns to him and says, "Wherefore was that cry? More TV Picks. However, his breakthrough performance was as the quintessential "angry young man" in the sensational drama This Sporting Life , which scored him an Oscar nomination. -

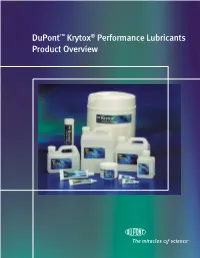

Dupont™ Krytox® Performance Lubricants Product Overview

DuPont™ Krytox® Performance Lubricants Product Overview Krytox® Oils and Greases Product Overview Selection of the best lubricant involves analyzing Typical Applications your operating conditions and choosing from the Aerospace many synthetic and petroleum based products. Most • Bearing Lubricant petroleum products begin to degrade before 99°C • Sealant (210°F) and cease turning at temperatures just • O-Ring Lubricant below –18°C (0°F). Krytox® synthetic lubricants • Oxygen Systems have operating ranges from <–70 to 316°C (<–94 to 600°F). Industrial Krytox® oils and greases are the products of choice • Paper Corrugating Bearings for applications where complete nonflammability, • Chemical Plant Maintenance oxygen compatibility, and resistance to aggressive • Valve Lubricant chemicals are requirements. These synthetic • High-Temperature Equipment lubricants provide superior performance and • Clean Rooms extended life as lubricants, sealants, and dielectrics. • Chlorine and Oxygen Service • Textile Equipment Cost-Effectiveness Automotive As Table 1 demonstrates, Krytox® lubricants are cost-effective across a wide range of applications, • Bearing Lubricant because of their long, useful life relative to tradi- • CV Joints tional hydrocarbons. • Weatherstrip Lubricant • Antilock Braking Systems Table 1 Vacuum Systems Life/Cost/Reliability • Vacuum Pump Fluids Typical Hydrocarbon Application Lubricant Krytox® • High-Vacuum Greases • Vacuum System Sealant Electric Motor 5 days 9 months 227°C (440°F), 1,750 rpm Heated Rolls 8 months 24 months 199°C (390°F), 5,000 rpm Textile Roll 1 month 24 months 225°C (437°F), 5,400 rpm Pressure Relief Valves 50% failures Less than 1% failures Paper Corrugating $144,000 $3,000 Machine 1 Applications Krytox® oils are available in a variety of viscosities. -

View 1963 Cynic (PDF)

Comprehensive Coverage Of Serving UVM For 81 Years Campus News 1883-1963 VOL. 81 UNIVERSITY OF VERMONT, BURLINGTON, VERMONT november 21 , 1963 NO. 19 Theodore Bikel Featured Vt.Conference Stresses Nov. 25 On Lane Series Olivier offered him the role of Vt. Role In Rights Struggle Mitch in A Streetcar Named De sire. After the long run of that James Farmer: Louis Lomax: hit play, he went into Peter Us John Lewis: tinov's The Love of Four Colo Won't Give Up Humans First Non-violence nels. by James L, Sealy by Carolyn Seigel by Joan Klonsky Theodore Bike! came to the It was a rainy. solemn Tuesday, Louis Lomax said in a speech On Thursday evening, Novem United States in 1954 to appear Nov. 12, 1963, which ushered In Wednesday night that Negroes ber 14, the final speaker for on Broadway in Tonight in So- the !st day of Vermont Confer and whites are "inextricably bound VVermontConference was John markand. His other Broadway ence. It almost seemed as if the together.'' He added that one race Lewis, who, at only 25, is the credits include The lark with weather had recognized the cannot rise without the other and youngest leader of a major civil Julie Harris, _The Rope Dancers significance of the event about to that we must save each other to rights organization in the United with Art Carney and Siobhan take place, and decided to set the save ourselves. Lomax said that States (SNICK). Although Mr. McKenna. and, of course, Sound proper atmosphere. This was the he is trying to involve us, as of Music. -

Rr F4nn&Uhti*T$>

/ <y%^ MERC1AD VOL. XXX^No. 6 MERCYHURST COLLEGE, ERIE, PENNA. April 22, 1959 Ellie Cavanaugh Will Crown Leaders Meet Our Lady Of Mercy Statue For Discussion Traditional May Day ceremonies will be held May 10 on front campus. At 3 p.m. Eleanor Cavanaugh, May Queen, attended by Both this year's and next year's Cynthia Ryan and Dorie Andre, will crown the statue of Our Lady of officers will meet to discuss in Mercy. ternational student affairs on The elected f May Queen for 1959 comes from Johnstown, Pa. Sunday, May 3, from 11:30 ja.m. Eleanor, who majors in chemistry, is this year's Y. C. S. Campus Chair to 5:00 p.m. in the Senior Lounge man. Maids-of-honor, Cynthia Ryan from Youngstown, Ohio, and Dorie at McAuley Hall. Thespians (1. to r.) Robert Smith, Marilyn Millard, Lolly Lockhart, Andre from Far re 11, Pa., are respectively Sodality Prefect and Home A panel of five students from Patti Carlile, Sue McCartney, and Kathy Reid imitate inanimate Economics Club President. Cyn-I different countries will compare objects in their roles as Bohemian students in the April 25, 26 thia majors in elementary edu student life in their own countries "Stardust" production. cation and Dorie inf home eco to student life in the United nomics. States. Welling Chang from For ft Senior class members, forming mosa, Lurline By grave of Jamaica, Cast To Offer "Stardust Eleanor's court, will follow the Hungary's Maria Jalics, Carmen student body leading It he proces Olivera from Puerto Rico, and sion to the traditional "Pomp Jean Reynolds of Erie are panel Friday Saturday Nites 22—American Chemical So- members. -

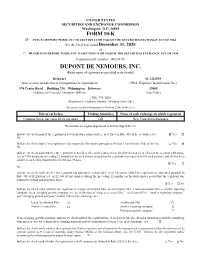

Corteva, Inc. E. I. Du Pont De Nemours and Company

2020 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 ____________________________________________________________________________ Commission File Number 001-38710 Corteva, Inc. (Exact Name of Registrant as Specified in Its Charter) Delaware 82-4979096 (State or other Jurisdiction of Incorporation or Organization) (I.R.S. Employer Identification No.) 974 Centre Road, Wilmington, Delaware 19805 (302) 485-3000 (Address of Principal Executive Offices) (Zip Code) (Registrant’s Telephone Number, including area code) Commission File Number 1-815 E. I. du Pont de Nemours and Company (Exact Name of Registrant as Specified in Its Charter) Delaware 51-0014090 (State or other Jurisdiction of Incorporation or Organization) (I.R.S. Employer Identification No.) 974 Centre Road, Wilmington, Delaware 19805 (302) 485-3000 (Address of Principal Executive Offices) (Zip Code) (Registrant’s Telephone Number, including area code) Securities registered pursuant to Section 12(b) of the Act for Corteva, Inc.: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, par value $0.01 per share CTVA New York Stock Exchange Securities registered pursuant to Section 12(b) of the Act for E. I. du Pont de Nemours and Company: Title of each class Trading Symbol(s) Name of each exchange on which registered $3.50 Series Preferred Stock CTAPrA New York Stock Exchange $4.50 Series Preferred Stock CTAPrB New York Stock Exchange No securities are registered pursuant to Section 12(g) of the Act. -

Evaluation of Seals and Lubricants Used on the Long Duration Exposure Facility

NASA Contractor Report 4604 Evaluation of Seals and Lubricants Used on the Long Duration Exposure Facility H. W. Dursch, B. K. Keough, and H. G. Pippin Contracts NAS1-18224 and NAS1-19247 Prepared for Langley Research Center d NASA Contractor Report 4604 Evaluation of Seals and Lubricants Used on the Long Duration Exposure Facility Y. W. Dursch, B. K. Keough, and H. G. Pippin 3oeing Defense €2 Space Group o Seattle, Washington National Aeronautics and Space Administration Prepared for Langley Research Center Langley Research Center o Hampton, Virginia 23681- 0001 under Contracts NAS1-18224 and NAS1-19247 ~- June 1994 d EVALUATION OF SEALS AND LUBRICANTS USED ON LDEF FOREWORD This report describes the results from the testing and analysis of lubricants and seals flown on the Long Duration Exposure Facility (LDEF). Boeing Defense & Space Group's activities were supported by the following NASA Langley Research Center Contracts (LaRC); "LDEF Special Investigation Group Support" contracts NAS 1- 18224, Tasks 12 and 15 (October 1989 through January 1991), NAS1-19247 Tasks 1 & 2 (May 1991 through October 1992), and NAS 1-19247 Task 8 (initiated October 1992). Sponsorship for these programs was provided by National Aeronautics and Space Administration, Langley Research Center, Hampton, Virginia, and The Strategic Defense Initiative Organization, Key Technologies Office, Washington, D.C. Mr. Lou Teichman, NASA LaRC, was the initial NASA Task Technical Monitor. Following Mr. Teichman's retirement, Ms. Joan Funk, NASA LaRC, became the Task Technical Monitor. The Materials & Processes Technology organization of the Boeing Defense & Space Group performed the five contract tasks with the following Boeing personnel providing critical support throughout the program. -

Ralph Nelson Papers, 1940-1983

http://oac.cdlib.org/findaid/ark:/13030/kt4489n6wm No online items Finding Aid for the Ralph Nelson Papers, 1940-1983 Processed by Manuscripts Division staff and Brooke Whiting; machine-readable finding aid created by Caroline Cubé and edited by Josh Fiala. UCLA Library, Department of Special Collections Manuscripts Division Room A1713, Charles E. Young Research Library Box 951575 Los Angeles, CA 90095-1575 Email: [email protected] URL: http://www.library.ucla.edu/libraries/special/scweb/ © 2002 The Regents of the University of California. All rights reserved. Finding Aid for the Ralph Nelson 875 1 Papers, 1940-1983 Descriptive Summary Title: Ralph Nelson Papers, Date (inclusive): 1940-1983 Collection number: 875 Creator: Nelson, Ralph, 1916- Extent: 116 boxes (58 linear ft.)7 cartons (7 linear ft.)25 oversize boxes Abstract: Ralph Nelson (1916-1987) was an actor, director, producer, and playwright. He wrote the play Mail call (winner of the 1943 John Golden prize and National Theatre awards), and won National Theatre awards for Angels weep and The wind is ninety. In 1956, he won a Emmy award for direction of Requiem for a heavyweight (1956), and in 1964, the Golden Globes Humanitarian award for directing Lilies of the field. The collection consists of television and motion picture shooting scripts, production files, films, tape recordings, phonograph records, scrapbooks, prints, personal memorabilia, and related printed material of Ralph Nelson. Scripts include Requiem for a heavyweight, The director, Father Goose, and Lilies of the field. Repository: University of California, Los Angeles. Library. Department of Special Collections. Los Angeles, California 90095-1575 Physical location: Stored off-site at SRLF. -

Download Proceedings

AIC 2004 Color and Paints Interim Meeting of the International Color Association Porto Alegre, Brazil, November 3-5, 2004 Proceedings edited by José Luis Caivano 2005 AIC 2004 “Color and Paints” was organized by the Brazilian Color Association (ABCor, Associação Brasileira da Cor) on behalf of the International Color Association (AIC, Association Internationale de la Couleur) AIC 2004 Color and Paints, Proceedings of the Interim Meeting of the International Color Association, Porto Alegre, Brazil, 3-5 November 2004 The proceedings include: invited lectures, oral papers, posters. Reference to papers in this book should be made as follows: For the electronic version on the Internet: Author(s). 2005. “Title of the paper”. In AIC 2004 Color and Paints, Proceedings of the Interim Meeting of the International Color Association, Porto Alegre, Brazil, 3-5 November 2004, ed. by José Luis Caivano. In www.fadu.uba.ar/sicyt/color/aic2004.htm, pp. X-X [first and last page of the article]. For the printed version: Author(s). 2005. “Title of the paper”. In AIC 2004 Color and Paints, Proceedings of the Interim Meeting of the International Color Association, Porto Alegre, Brazil, 3-5 November 2004, ed. by José Luis Caivano and Hanns-Peter Struck. Porto Alegre, Brazil: Associação Brasileira da Cor, pp. X-X [first and last page of the article]. AIC 2004 Scientific Committee AIC 2004 Organizing Committee Argentina: José Luis Caivano (chair) President: Roberto Daniel Lozano Hanns-Peter Struck María L. F. de Mattiello General Secretary and Treasurer: Austria: Leonhard Oberascher Maira Knop Brazil: Nelson Bavaresco General Chair: Robert Hirschler Nelson Petzold Marcos Quindici Secretary of the Event: Hanns-Peter Struck Catia Brach Monser England: John Hutchings Exhibition Chair: Ming Ronnier Luo Roberto Ilhescas Lindsay MacDonald Event Chair: Michael Pointer Erni Clovis Gil Germany: Klaus Witt Publicity and Publications Chair: Italy: Osvaldo da Pos Norton Eduardo S. -

Dupont 2020 10-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number: 001-38196 DUPONT DE NEMOURS, INC. (Exact name of registrant as specified in its charter) Delaware 81-1224539 State or other jurisdiction of incorporation or organization (I.R.S. Employer Identification No.) 974 Centre Road Building 730 Wilmington Delaware 19805 (Address of Principal Executive Offices) (Zip Code) (302) 774-3034 (Registrant’s Telephone Number, Including Area Code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, par value $0.01 per share DD New York Stock Exchange No securities are registered pursuant to Section 12(g) of the Act. _____________________________________________________ Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. þ Yes ¨ No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes þ No Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.