Federal Reserve Bulletin October 1961

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

17 Octobre 2001, L'histoire D'une Commemoration

Brigitte Jelen Ph.D. student Department of History 200 Murray Krieger Hall University of California, Irvine Irvine, CA 92697-3275 Phone: (949) 824-6521 Fax: (949) 824-2865 Email: [email protected] Conference Paper: France and the Memory of the Algerian war: The Ambiguous Commemoration of October 17, 1961. Note: the original version of this essay, entitled “17 octobre 1961 - 17 octobre 2001: Une commémoration ambiguë” is being published in the spring 2002 issue of the journal French Politics, Culture, and Society. France and the Memory of the Algerian war: The Ambiguous Commemoration of October 17, 1961. (Translations from the original French text are mine) On May 9, 2001, the French daily Libération published the results of an opinion poll on “torture during the French-Algerian war.” In this poll, 56% of those questioned declared being favorable to an official apology to the Algerian people from the French President or Prime minister. To the question: “according to you, who are the main parties responsible for the use of torture during the French-Algerian war?” 50% of the French placed the blame on the political authorities at the time, while 31% placed the blame on the military. In addition, 56% wanted to see the officers who had used torture brought to justice. (This poll followed the publication in May 2001 of a book by General Aussaresses condoning the use of torture during the war). According to this poll, a majority of the French population seems ready to face the painful memories of the French-Algerian war, and is not afraid to engage the responsibility of the French state in the crimes that took place at the time. -

MC0014 1 Local History Collection South Pasadena Public Library

MC0014 Local History Collection South Pasadena Public Library South Pasadena, California Parent Teacher Association (PTA) Archive Name: Parent Teacher Association (PTA) Archive MC0014 Materials: Manuscript, Budget Reports, Certificates, Membership Information, Newsletters, Bound Volumes, Plaques Dates: 1911-1984 Volume: 1.528 cubic feet (3 standard document boxes) Donation: N/A Usage: Unless otherwise stated by SPPL staff, these records are open for research without restrictions. Historical Note The National Parent Teacher Association (PTA) began in 1897 with the help of over 2,000 parents, teachers, legislators, and laborers. Currently, the PTA is the largest volunteer child advocacy organization in the nation. The National PTA has established programs for the creation of kindergarten classes, child labor laws, public health service, lunch programs, juvenile justice system, mandatory immunization, arts in education, and school safety. Collection Description This collection contains objects and documents related to PTA organizations within the South Pasadena Unified School District. Items in this collection include manuscript, budget reports, certificates, membership information, newsletters, bound volumes, plaques, and more. Series and Subseries I. Certificates 1 box Framed charter certificate establishing the El Centro School PTA. Dated 1911. II. Parent Teacher Association (PTA) Board Meeting Minutes 1 folder Various PTA Board Meeting Minutes from schools in South Pasadena, California. Dated 1978 to 1979. 1 MC0014 III. Parent Teacher Association (PTA) Membership 2 folders Documents related to PTA membership and membership drives. Dated 1911 to 1980. IV. Parent Teacher Association (PTA) Annual Reports 10 folders This series contains annual reports from El Centro PTA. Dated from 1911 to 1979. V. Budgets 1 folder This series contains PTA budget reports, Treasurer’s Reports, and Auditor’s Reports. -

Commandant's Annual Report, 1961-1962

COMMANDANT'S ANNUAL REPORT 1961 ... 1962 The Judge Advocate General's School United States Army Charlottesville, Virginia FOREWORD It is with great pleasure and much satisfaction that I present the Commandant's Annual Report for Fiscal Year 1962. Al though this represents the first report of this type published by The Judge Advocate General's School, it is intended that it become an integral feature in chronicling the continuing development of the Army's military law center. The report has a three-fold purpose: --- 1. To summarize the operations of the School during the past fiscal year. ---------2. To preserve in printed form a record of the School, its staff and faculty, students, and enlisted personnel. ~ To describe the various courses of instruction offered at - The Judge Advocate General's School. ThiE report reflects continued progress on the part of The Judge Advocate General's School. The value of any educational institution, however, is measured by how well it prepares its student body for the roles which await them upon graduation. Accordingly, our goal, as in the past, is to increase and make more effective our services to the Army by thorough preparation of officers for service in the Judge Advocate General's Corps. JOHN F. T. MURRAY Colonel, J AGC Commandant i COMMANDANT'S ANNUAL REPORT FISCAL YEAR 1962 TABLE OF CONTENTS Page Section I -The Judge Advocate General's School Today ....................... 1 Mission ............... 1 History ..... 3 Section II -Organization of The Judge Advocate General's School ............ .......... 5 Academic Department ................ 5 Nonresident Training Department 5 Research and Publications Department 5 Office of School Secretary . -

The General Assembly, Having Received the Recommendation of the Security Council of 4 October 1962 That the Democratic and Popul

Resolution, adopted without reference to a Committee 71 1754 (XVII). Admission of the Democratic and 1758 (XVII). Admission of Uganda to member Popular Republic of Algeria to membership ship in the United Nations in the United Nations The General Assembly, The General Assembly, Having received the recommendation of the Security Having received the recommendation of the Security Council of 15 October 1962 that Uganda should be Council of 4 October 1962 that the Democratic and admitted to membership in the United Nations,12 Popular Republic of Algeria should be admitted to Having considered the application for membership membership in the United Nations,10 of Uganda,13 Having considered the application for membership Decides to admit Uganda to membership in the of the Democratic and Popular Republic of Algeria,11 United Nations. Decides to admit the Democratic and Popular Re 1158th plenary meeting, public of Algeria to membership in the United Nations. 25 October 1962. 1146th plenary meeting, 1759 (XVII). Report of the Commission of in 8 October 1962. vestigation into the conditions and circum stances resulting in the tragic death of 1756 (XVII). Report of the Committee on ar• Mr. Dag Hammarskjold and of members rangements for a conference for the purpose of the party accompanying him of reviewing the Charter The General Assembly, The General Assembly, Recalling its resolution 1628 (XVI) of 26 October Recalling the provisions of its resolutions 992 (X) 1961 in which it decided to appoint a Commission of five of 21 November 1955, 1136 (XII) of 14 October 1957, eminent persons to carry out an investigation into the 1381 (XIV) of 20 November 1959 and 1670 (XVI) circumstances surrounding the tragic death of Mr. -

The October 1963 Eruption of Kilauea Volcano Hawaii

The October 1963 Eruption of Kilauea Volcano Hawaii GEOLOGICAL SURVEY PROFESSIONAL PAPER 614-C The October 1963 Eruption of Kilauea Volcano Hawaii By JAMES G. MOORE and ROBERT Y. KOYANAGI SHORTER CONTRIBUTIONS TO GENERAL GEOLOGY GEOLOGICAL SURVEY PROFESSIONAL PAPER 614-C UNITED STATES GOVERNMENT PRINTING OFFICE, WASHINGTON : 1969 UNITED STATES DEPARTMENT OF THE INTERIOR WALTER J. HICKEL, Secretary GEOLOGICAL SURVEY William T. Pecora, Director For sale by the Superintendent of Documents, U.S. Government Printing Office Washington, D.C. 20402 CONTENTS Page Abstract._______________________________________ Cl Introduction ____________________________________ 1 Distribution of volcanic activity on the east rift zone- 1 Events of 1963 preceding the eruption___--_-_-_--_. 5 Description of the eruption__---_-_-_-_------------ 5 Lava flows_-__---_--____________---_____---____- 7 Earthquakes, tremor, and tilting...-______-___--_-_ 10 Petrology of the lavas. _________________-------_-- 11 References cited _________________________________ 13 ILLUSTRATIONS Page PLATE 1. Geologic map of the central part of the east rift zone of Kilauea Volcano.______________--__-___-_---_--- In pocket FIGURE 1. Map showing the summit region of Kilauea Volcano_________________-__-__.-___._________-_---_--------- C2 2. Diagram showing the longitudinal distribution of eruptive vents on the east rift zone of Kilauea Volcano from 1954 to 1965___________________________________________-_____________--___----_-_-----_--------- :$ 3. Graph showing relations of Kilauean eruptions and collapses, ground tilting, and earthquakes._________---___- "> 4. Graph showing chronology of events during the October 1963 Kilauea east rift eruption.______-___.___._-___- 6 5. Oblique aerial photograph of eruptive vents extending east of Napau Crater_______-_-__---____-_-__-_-_--_- S 6. -

Author Index

AUTHOR INDEX A E ADRIAN, F. J.- See COCHRAN, E. L. ELDER, S. A.- Physicists and Fipple Flutes at APL, AKRIDGE, J. M.- See HILL, M. L. 3,3, January-February 1964, pp. 15-18 APEL, J. R.- Ways and M eans of Boat Design) 5, EVANS , R. C.- The APL R esistance W elder and 2, November-December. 1965, pp. 18-23 I ts Role in Satellite R eliability, 5, 1, September - - -, E. P. GRAY, and A. M. SToNE- Beam October 1965, pp. 2-7 Plasma Interactions, 3, 5, May-June 1964, pp. 2-11 F AVERY, W. H.- Status and Future Trends in High FASTIE, W. G.-Rockets and the Aurora Borealis, S peed Chemical Propulsion, 4, 6, July- August 5, 5, May-June 1966, pp. 5-10 1965, pp. 2- 9 FEHLNER, L. F.- Improved Data for the Classical --- See HILL, M. L. Determination of Radar Detection Range, 3 , 2, November- December 1963, pp. 17-24 B FISCHELL, R. E.-The TRAAC Satellite, I , 3, BEAL, R. C.-Design and Performance of the January-February 1962, pp. 2-9 DODGE Cameras, 6, 5, May-June 1967, pp. - - - Effect of the Artificial Radiation Belt on 9-14 Solar Power Systems, 2, 2, November-December 1962, pp. 8-13 BERGIN, T. G.- For A Space Prob er, 2, 2, Novem- - -- Gravity Gradient Stabili<. ation of Earth ber-December 1962, p. 2 Satellites, 3, 5, May-June 1964, pp. 12- 21 BILLERBECK, W. J. - See OAKES, B. J. --- Spin Control for Earth Satellites, 5, 1, BOSTROM , C. O.-See WILLIAMS, D. -

48597.Pdf (213.3Kb)

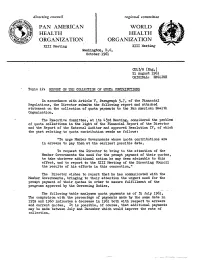

directing council regional committee '/g,/r PAN AMERICAN WORLD ,-, ) HEALTH HEALTH , ORGANIZATION ORGANIZATION XIII Meeting XIII Meeting Washington, D.C. October 1961 cD13/8 (Eng.) 21 August 1961 ORIGINAL: ENGLISH Topic 12: REPORT ON THE COLLECTION OF QUOTA CONTRIBUTIONS In accordance with Article V, Paragraph 5.7, of the Financial Regulations, the Director submits the following report and attached statement on the collection of quota payments to the Pan American Health Organization. The Executive Committee, at its 43rd Meeting, considered the problem of quota collections in the light of the Financial Report of the Director and the Report of the External Auditor and approved Resolution IV, of which the part relating to quota contribution reads as follows: "To urge Member Governments whose quota contributions are in arrears to pay them at the earliest possible date. To request the Director to bring to the attention of the Member Governments the need for the prompt payment of their quotas, to take whatever additional action he may deem advisable to this effect, and to report to the XIII Meeting of the Directing Council the results of his efforts in this connection." The Director wishes to report that he has communicated with the Member Governments, bringing to their attention the urgent need for the prompt payment of their quotas in order to assure fulfillment of the programs approved by the Governing Bodies. The following table analyzes quota payments as of 31 July 1961. The comparison with the percentage of payments made by the same date in 1959 and 1960 indicates a decrease in 1961 both with respect to arrears and current quotas. -

United Nations Conference on the Elimination Or Reduction of Future Statelessness

United Nations Conference on the Elimination or Reduction of Future Statelessness Geneva, 1959 and New York, 1961 Document:- A/CONF.9/SR.21 Summary Records, 21st Plenary meeting Copyright © United Nations 2009 UNITED NATIONS Distr. GENERAL GENERAL A/C0NF.9/SR.21 11 October 1961 ASSEMBLY ENGLISH ORIGINAL: FRENCH UNITED NATIONS CONFERENCE ON THE ELIMINATION OR REDUCTION OF FUTURE STATELESSNESS SUMMARY RECORD OF THE TWENTY-FIRST PLENARY MEETING Held at Headquarters, New York, on Thursday, 24 August 1961, at 1O.3O a.m. CONTENTS Presentation of credentials Examination of the question of the elimination or reduction of future statelessness (A/CONF.9/10 and Add.l to 3, A/CONF.9/10, A/C0NF.9/l2; A/CONF.9/L.86;L.87) (continued): Article 8 of the Draft Convention (continued) President: Mr. RIPHAGEN (Netherlands) Secretariat: Mr. STAVR0P0ULC5 Legal Counsel, Representative of the Secretary-General Mr. LIANG Executive Secretary of the Conference 61-23549 /... A/C0KP.9/SR.21 English Page 2 PRESENTATION OF CREDENTIALS The PRESIDENT, referring to rule 3 of the rules of procedure, invited representatives who had not yet submitted their credentials to do so without delay, so as to enable the President and the Vice-President to present their report to the Conference. EXAMINATION OF THE QUESTION OF THE ELIMINATION OR REDUCTION OF FUTURE STATELESSNESS (A/CONF.9/10 and Add.l to 3, A/CONF.9/II, A/CONF.9/l2; A/CONF.9/L.86-L.87) (continued) Article 8 of the Draft Convention (continued) The PRESIDENT drew the attention of the Conference to the Yugoslav amendments to article 8, the text of which had just been circulated (A/CONF.9/L.87). -

![Jockeying for Leadership: Mao and the Sino-Soviet Split, October 1961 – July 1964.” [27 October 2015]](https://docslib.b-cdn.net/cover/1645/jockeying-for-leadership-mao-and-the-sino-soviet-split-october-1961-july-1964-27-october-2015-3761645.webp)

Jockeying for Leadership: Mao and the Sino-Soviet Split, October 1961 – July 1964.” [27 October 2015]

H-Diplo H-Diplo Article Review 562 on “Jockeying for Leadership: Mao and the Sino-Soviet Split, October 1961 – July 1964.” [27 October 2015] Discussion published by George Fujii on Tuesday, October 27, 2015 H-Diplo Article Reviews No. 562 Published on 27 October 2015 H-Diplo Article Review Editors: Thomas Maddux and Diane Labrosse Web and Production Editor: George Fujii Commissioned for H-Diplo by Thomas Maddux Danhui Li and Yafeng Xia.“Jockeying for Leadership: Mao and the Sino-Soviet Split, October 1961 – July 1964.” Journal of Cold War Studies, 16:1 (Winter 2014): 24-60. DOI: 10.1162/JCWS_a_00430. http://dx.doi.org/10.1162/JCWS_a_00430 URL: http://tiny.cc/AR562 Review by Avram Agov, Langara College, Vancouver Danhui Li and Yafeng Xia do an outstanding job of examining the origins of the Sino-Soviet split. Their article offers one of the most comprehensive analyses of the critical crossroad of international communist movement in the early 1960s. The two authors start with a review of the main scholarly interpretations of the reasons for the Sino-Soviet conflict, ranging from ideological divergence to differing national interests and personal tensions. Li and Xia argue that the clash of national interests was the result, rather than the cause, of the conflict between the two socialist neighbors, and that their ideological dispute was for “appearance’s sake;” instead, the root cause of the split was the competition between the Soviet Union and China for leadership of the international communist movement. (26) A major contribution of the article is the use of a collection of documents from the Chinese Ministry of Foreign Affairs as well as documents from internal party meetings and local archives, which illuminate the Chinese side of the dispute. -

The John F. Kennedy National Security Files, 1961–1963 Western Europe First Supplement

A Guide to the Microfilm Edition of The John F. Kennedy National Security Files, 1961–1963 Western Europe First Supplement A UPA Collection from Cover: Map of Europe courtesy of the Central Intelligence Agency World Factbook. National Security Files General Editor George C. Herring The John F. Kennedy National Security Files, 1961–1963 Western Europe First Supplement Guide by Dan Elasky A UPA Collection from 7500 Old Georgetown Road ● Bethesda, MD 20814-6126 Library of Congress Cataloging-in-Publication Data The John F. Kennedy national security files, 1961–1963. Western Europe. First supplement [microform] / project coordinator, Robert E. Lester. microfilm reels ; 35 mm. –– (National security files) “Microfilmed from the holdings of the John F. Kennedy Library, Boston, Massachusetts.” Accompanied by a printed guide, entitled: A guide to the microfilm edition of the John F. Kennedy national security files, 1961–1963. Western Europe. First supplement ISBN 1-55655-881-3 1. United States––Foreign relations––Europe, Western––Sources. 2. Europe, Western ––Foreign relations––United States––Sources. 3. United States––Foreign relations––1963–1969–– Sources. 4. National security––United States––History––Sources. 5. Western Europe––Foreign relations––1945–1989. I. Lester, Robert. II. John F. Kennedy Library. III. University Publications of America (Firm) IV. Series. Microfilm XXXXX 327.7304––dc22 2008063101 Copyright © 2009 LexisNexis, a division of Reed Elsevier Inc. All rights reserved. ISBN 1-55655-881-3. TABLE OF CONTENTS Scope and Content Note -

Conflict and Confrontation in South East Asia, 1961–1965

Conflict and Confrontation in South East Asia, 1961–1965 Britain, the United States and the Creation of Malaysia Matthew Jones PUBLISHED BY THE PRESS SYNDICATE OF THE UNIVERSITY OF CAMBRIDGE The Pitt Building, Trumpington Street, Cambridge, United Kingdom CAMBRIDGE UNIVERSITY PRESS The Edinburgh Building, Cambridge CB2 2RU, UK 40 West 20th Street, New York, NY 10011-4211, USA 10 Stamford Road, Oakleigh, VIC 3166, Australia Ruiz de Alarc´on 13, 28014 Madrid, Spain Dock House, The Waterfront, Cape Town 8001, South Africa http://www.cambridge.org C Matthew Jones 2002 This book is in copyright. Subject to statutory exception and to the provisions of relevant collective licensing agreements, no reproduction of any part may take place without the written permission of Cambridge University Press. First published 2002 Printed in the United Kingdom at the University Press, Cambridge Typeface Plantin 10/12 pt. System LATEX2ε [TB] A catalogue record for this book is available from the British Library Library of Congress Cataloguing in Publication Data Jones, Matthew, 1966– Conflict and confrontation in South East Asia, 1961–1965 : Britain, the United States and the Creation of Malaysia / Matthew Jones. p. cm. Includes bibliographical references and index. ISBN 0 521 80111 7 hardback 1. Asia, Southeastern – Foreign relations – Great Britain. 2. Great Britain – Foreign relations – Asia, Southeastern. 3. Asia, Southeastern – Foreign relations – United States. 4. United States – Foreign relations – Asia, Southeastern. 5. Indonesia – Foreign relations – -

A Brief History of the Berlin Crisis of 1961

A Brief History of the Berlin Crisis of 1961 Neil Carmichael National Declassification Center National Records and Archives Administration Autumn 2011 marks the 50th anniversary of the political crisis that resulted in the erection of the Berlin Wall which divided that German city for 28 years. The National Declassification Center of the National Archives and Records Administration and the Historical Collections Division of the Central Intelligence Agency have partnered to publish newly declassified documents that reveal intimate details of the five month Berlin Crisis of 1961. Included in this joint publication are newly released documents that show behind-the-scenes security discussions and planning. The Department of State has added a contemporary 600- page report, never before disclosed, on the impact of the events surrounding the crisis and the deepening of the Cold War. Other documents explain the looming threat the crisis represented to the legal status and rights of the three Western Powers in Berlin; Britain, France and the United States, and provides a sense of the real-time spiral of statements, military acts, parry and feints, that led to international brinksmanship as the West went toe-to-toe with a USSR ready to annex or asphyxiate Berlin. Events leading up to the Crisis 1958-1960 From the end of World War II in 1945, the question of Berlin’s status 90 miles within the Deutsche Demokratische Republik (East Germany) and the Soviet Unions’ zone of occupation, along with the status of Germany among the community of nations, remained a source of tension between the East and West. Premier Khrushchev continued to push President Eisenhower and the other Western leaders for resolution of the issue In November 1958, Khrushchev issued an ultimatum giving the Western Powers six months to agree to withdraw from Berlin and make it a free, demilitarized city.