Qingdao City Construction Investment (Group) Limited Initial Issuer Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

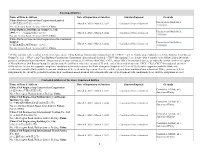

Sanctioned Entities Name of Firm & Address Date

Sanctioned Entities Name of Firm & Address Date of Imposition of Sanction Sanction Imposed Grounds China Railway Construction Corporation Limited Procurement Guidelines, (中国铁建股份有限公司)*38 March 4, 2020 - March 3, 2022 Conditional Non-debarment 1.16(a)(ii) No. 40, Fuxing Road, Beijing 100855, China China Railway 23rd Bureau Group Co., Ltd. Procurement Guidelines, (中铁二十三局集团有限公司)*38 March 4, 2020 - March 3, 2022 Conditional Non-debarment 1.16(a)(ii) No. 40, Fuxing Road, Beijing 100855, China China Railway Construction Corporation (International) Limited Procurement Guidelines, March 4, 2020 - March 3, 2022 Conditional Non-debarment (中国铁建国际集团有限公司)*38 1.16(a)(ii) No. 40, Fuxing Road, Beijing 100855, China *38 This sanction is the result of a Settlement Agreement. China Railway Construction Corporation Ltd. (“CRCC”) and its wholly-owned subsidiaries, China Railway 23rd Bureau Group Co., Ltd. (“CR23”) and China Railway Construction Corporation (International) Limited (“CRCC International”), are debarred for 9 months, to be followed by a 24- month period of conditional non-debarment. This period of sanction extends to all affiliates that CRCC, CR23, and/or CRCC International directly or indirectly control, with the exception of China Railway 20th Bureau Group Co. and its controlled affiliates, which are exempted. If, at the end of the period of sanction, CRCC, CR23, CRCC International, and their affiliates have (a) met the corporate compliance conditions to the satisfaction of the Bank’s Integrity Compliance Officer (ICO); (b) fully cooperated with the Bank; and (c) otherwise complied fully with the terms and conditions of the Settlement Agreement, then they will be released from conditional non-debarment. If they do not meet these obligations by the end of the period of sanction, their conditional non-debarment will automatically convert to debarment with conditional release until the obligations are met. -

Land Acquisition ◆ in April 2020, the Group Completed the Following Land Acquisitions

2020 Corporate Monthly Newsletter APRIL CIFI’s Contracted Sales of RMB13.00B in April 2020 and RMB35.40B in First Four Months ◆ In April 2020, the Group achieved the contracted sales of RMB13.00 billion. Contracted GFA amounted to approximately 815,900 sq.m. Contracted ASP was approximately RMB15,900/sq.m. in April 2020. ◆ From January to April 2020, the Group achieved contracted sales of RMB35.40 billion. Contracted GFA amounted to approximately 2,204,800 sq.m. Contracted ASP was approximately RMB16,100/sq.m. from January to April 2020. Land Acquisition ◆ In April 2020, the Group completed the following land acquisitions: Average Group’s Total Planned Group’s Land Cost Current Intended Site GFA Attributable (Excluding City Project Equity Primary Area (Excluding Consideration Carpark) Interest Use (sq.m.) Carpark) (RMB) (RMB/ (sq.m.) sq.m.) Miyun District, Beijing Tanying Town, 6023 22.5% Residential 60,600 124,400 336,600,000 12,027 Project Jimo District, Qingdao Zaohang 100% Residential 59,500 141,800 252,570,000 1,781 Resettlement Project Jimo District, Qingdao Zaohang 100% Residential 111,900 241,700 654,390,000 2,708 Development Project Economic Development Zone, Residential, Nanchang 100% 415,700 498,800 2,020,090,000 4,050 No. DAGJ2020004 Commercial Project Page 1 of 4 2020 Corporate Monthly Newsletter APRIL (Cont’d) Average Group’s Total Planned Group’s Land Cost Current Intended Site GFA Attributable (Excluding City Project Equity Primary Area (Excluding Consideration Carpark) Interest Use (sq.m.) Carpar) (RMB) (RMB/ (sq.m.) sq.m.) Banan District, Yudong Yunzhuan Chongqing 51% Residential 37,500 82,500 141,430,000 3,362 Mountain, P07-03-01 Project Jiangyin City, Yunting Street, Experimental Wuxi 33% Residential 46,000 81,800 256,460,000 9,498 Primary School North Project Company News ◆ In April 2020, Moody’s reaffirmed CIFI’s “Ba3” issuer rating with outlook positive. -

TIER2 SITE NAME ADDRESS PROCESS M Ns Garments Printing & Embroidery

TIER 2 MANUFACTURING SITES - Produced July 2021 TIER2 SITE NAME ADDRESS PROCESS Bangladesh Mns Garments Printing & Embroidery (Unit 2) House 305 Road 34 Hazirpukur Choydana National University Gazipur Manufacturer/Processor (A&E) American & Efird (Bd) Ltd Plot 659 & 660 93 Islampur Gazipur Manufacturer/Processor A G Dresses Ltd Ag Tower Plot 09 Block C Tongi Industrial Area Himardighi Gazipur Next Branded Component Abanti Colour Tex Ltd Plot S A 646 Shashongaon Enayetnagar Fatullah Narayanganj Manufacturer/Processor Aboni Knitwear Ltd Plot 169 171 Tetulzhora Hemayetpur Savar Dhaka 1340 Manufacturer/Processor Afrah Washing Industries Ltd Maizpara Taxi Track Area Pan - 4 Patenga Chottogram Manufacturer/Processor AKM Knit Wear Limited Holding No 14 Gedda Cornopara Ulail Savar Dhaka Next Branded Component Aleya Embroidery & Aleya Design Hose 40 Plot 808 Iqbal Bhaban Dhour Nishat Nagar Turag Dhaka 1230 Manufacturer/Processor Alim Knit (Bd) Ltd Nayapara Kashimpur Gazipur 1750 Manufacturer/Processor Aman Fashions & Designs Ltd Nalam Mirzanagar Asulia Savar Manufacturer/Processor Aman Graphics & Design Ltd Nazimnagar Hemayetpur Savar Dhaka Manufacturer/Processor Aman Sweaters Ltd Rajaghat Road Rajfulbaria Savar Dhaka Manufacturer/Processor Aman Winter Wears Ltd Singair Road Hemayetpur Savar Dhaka Manufacturer/Processor Amann Bd Plot No Rs 2497-98 Tapirbari Tengra Mawna Shreepur Gazipur Next Branded Component Amantex Limited Boiragirchala Sreepur Gazipur Manufacturer/Processor Ananta Apparels Ltd - Adamjee Epz Plot 246 - 249 Adamjee Epz Narayanganj -

Tier 1 Manufacturing Sites

TIER 1 MANUFACTURING SITES - Produced January 2021 SUPPLIER NAME MANUFACTURING SITE NAME ADDRESS PRODUCT TYPE No of EMPLOYEES Albania Calzaturificio Maritan Spa George & Alex 4 Street Of Shijak Durres Apparel 100 - 500 Calzificio Eire Srl Italstyle Shpk Kombinati Tekstileve 5000 Berat Apparel 100 - 500 Extreme Sa Extreme Korca Bul 6 Deshmoret L7Nr 1 Korce Apparel 100 - 500 Bangladesh Acs Textiles (Bangladesh) Ltd Acs Textiles & Towel (Bangladesh) Tetlabo Ward 3 Parabo Narayangonj Rupgonj 1460 Home 1000 - PLUS Akh Eco Apparels Ltd Akh Eco Apparels Ltd 495 Balitha Shah Belishwer Dhamrai Dhaka 1800 Apparel 1000 - PLUS Albion Apparel Group Ltd Thianis Apparels Ltd Unit Fs Fb3 Road No2 Cepz Chittagong Apparel 1000 - PLUS Asmara International Ltd Artistic Design Ltd 232 233 Narasinghpur Savar Dhaka Ashulia Apparel 1000 - PLUS Asmara International Ltd Hameem - Creative Wash (Laundry) Nishat Nagar Tongi Gazipur Apparel 1000 - PLUS Aykroyd & Sons Ltd Taqwa Fabrics Ltd Kewa Boherarchala Gila Beradeed Sreepur Gazipur Apparel 500 - 1000 Bespoke By Ges Unip Lda Panasia Clothing Ltd Aziz Chowdhury Complex 2 Vogra Joydebpur Gazipur Apparel 1000 - PLUS Bm Fashions (Uk) Ltd Amantex Limited Boiragirchala Sreepur Gazipur Apparel 1000 - PLUS Bm Fashions (Uk) Ltd Asrotex Ltd Betjuri Naun Bazar Sreepur Gazipur Apparel 500 - 1000 Bm Fashions (Uk) Ltd Metro Knitting & Dyeing Mills Ltd (Factory-02) Charabag Ashulia Savar Dhaka Apparel 1000 - PLUS Bm Fashions (Uk) Ltd Tanzila Textile Ltd Baroipara Ashulia Savar Dhaka Apparel 1000 - PLUS Bm Fashions (Uk) Ltd Taqwa -

CHINA VANKE CO., LTD.* 萬科企業股份有限公司 (A Joint Stock Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 2202)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. CHINA VANKE CO., LTD.* 萬科企業股份有限公司 (A joint stock company incorporated in the People’s Republic of China with limited liability) (Stock Code: 2202) 2019 ANNUAL RESULTS ANNOUNCEMENT The board of directors (the “Board”) of China Vanke Co., Ltd.* (the “Company”) is pleased to announce the audited results of the Company and its subsidiaries for the year ended 31 December 2019. This announcement, containing the full text of the 2019 Annual Report of the Company, complies with the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to information to accompany preliminary announcement of annual results. Printed version of the Company’s 2019 Annual Report will be delivered to the H-Share Holders of the Company and available for viewing on the websites of The Stock Exchange of Hong Kong Limited (www.hkexnews.hk) and of the Company (www.vanke.com) in April 2020. Both the Chinese and English versions of this results announcement are available on the websites of the Company (www.vanke.com) and The Stock Exchange of Hong Kong Limited (www.hkexnews.hk). In the event of any discrepancies in interpretations between the English version and Chinese version, the Chinese version shall prevail, except for the financial report prepared in accordance with International Financial Reporting Standards, of which the English version shall prevail. -

Faurecia Invoicing Fiscal Names and Addresses List – 01/2021

Smarter Procurement Together Faurecia Invoicing Fiscal Names and Addresses list – 01/2021 Faurecia Bill-to Fiscal name and address by ordering site + PDF ingestion email Pay attention: Names and addresses below are NOT the mail to postal boxes to which you can send your invoices (if processed in paper) The list of names and addresses below correspond to Faurecia Bill-to fiscal names and addresses under which your invoices must be established. We highly recommend using Ariba PDF invoice channel, invoices list csv upload, Ariba PO flip capabilities or PDF email ingestion process to send your invoices. Please consider the following points: - The Faurecia bill-to fiscal ID (country tax ID, VAT registration number) must be checked on FAURECIA Purchase Order - Strictly avoid using paper invoice submission through postal mail boxes - Consider your country specific regulation to process your invoices Faurecia Fiscal Name and address to receive the invoice Faurecia Invoice to be send to Email company Legal entity fiscal name Country Fiscal Address 1 Fiscal Address 2 Address 3 Zip Code City State for automatic ingestion code FAURECIA SISTEMAS DE ESCAPE ARGENTINA AR02 Not Activated Argentina c/o Abeledo Gottheil Abogados Av Eduardo Madero 1020 5 ° piso 1106 Buenos Aires S.A. AR05 Not Activated FAURECIA ARGENTINA S.A. Argentina c/o Abeledo Gottheil Abogados Av Eduardo Madero 1020 5 ° piso Buenos Aires Provincia de AR08 Not Activated SAS Automotriz Argentina S.A. Argentina A. General Roca1865 1650 San Martin Buenos Aires AT01 [email protected] FAURECIA ANGELL-DEMMEL GmbH Austria Hofsteigstrasse 7 Werk II 6921 Kennelbach BE01 [email protected] FAURECIA AUTOMOTIVE BELGIUM SA. -

Bestseller Factory List

BESTSELLER FACTORY LIST LAST UPDATED: 21.05.2021 It is imperative for us to work with our partners in an open and honest way. We continuously seek to create more transparency in our supply chain to address risks and promote positive change. In light of this, and to provide increased transparency, we are making supplier factory information publicly available. The factory list includes the name, address, product type and number of workers of all tier 1 manufacturing factories (cut-make-trim) of apparel, footwear and accessories. The list will be updated twice a year. As changes occur in our supply chain with new partners, new factories onboarded, or factories being phased out, such alterations will be collected and published in the next supplier factory list update. FACTORY NAME ADDRESS MALE FEMALE NO. OF POSTAL CITY REGION COUNTRY PRODUCT EMPLOYEE EMPLOYEE EMPLOYEES CODE TYPES % % Almeg Shoes No. 14 Rruga Albania 5 95 <500 2000 Durres Durres ALBANIA Footwear Aba Fashions Ltd. No. 521/1 Gacha, Gazipur City Corporation 35 65 1001-5000 1704 Gazipur Dhaka BANGLADESH Apparel ABM Fashions Ltd. No.1143 &1145 Kashimpur Road, Konabari, Gazipur 30 70 1001-5000 1700 Dhaka Dhaka BANGLADESH Apparel Agami Apparels Ltd. Nayapara, Kathgara, Ashulia 40 60 5001-10000 1344 Savar Dhaka BANGLADESH Apparel Agami Fashions Ltd. Abdus Sattar Road, Pallibiduyt, Holding No. 79/1 30 70 1001-5000 1751 Gazipur Dhaka BANGLADESH Apparel AKM Knit Wear Ltd. No. 14 Gedda Karnapara, Ulail, Savar 35 65 >10000 1340 Dhaka Dhaka BANGLADESH Apparel Al-Muslim Apparels Ltd. No. 12 Nischintapur 25 75 <500 1341 Ashulia Dhaka BANGLADESH Apparel Aman Tex Ltd. -

Como Parte Fundamental Del Compromiso De MANGO Con La

LISTA DE FÁBRICAS DE PRODUCCIÓN DE MANGO Como parte fundamental del compromiso de MANGO con la sostenibilidad MANGO da respuesta así al compromiso adquirido con CCOO Industria en es esencial establecer una gestión responsable de nuestra cadena de el “Acuerdo Bilateral Global para garantizar las normas internacionales en la suministro que, junto con la participación de determinados grupos de interés, cadena de suministro de MANGO” y a los requerimientos del Transparency contribuye a la transparencia y es clave en la debida diligencia hacia Pledge Standard, que insta a las marcas a hacer público el nombre, dirección nuestros proveedores. Priorizamos una relación de confianza con ellos, y otros detalles de las fábricas de producción. asegurando que están alineados con nuestros propios compromisos, Cabe destacar que MANGO no posee ninguna fábrica en propiedad y contribuyendo así a asegurar los derechos humanos de los trabajadores y a ninguna trabaja en exclusiva para nuestra organización. Algunas de ellas fortalecer la industria textil a nivel global. pueden utilizarse de forma discontinua en el tiempo en función de las Así pues, conscientes de la importancia de ser transparentes y de facilitar el características del producto por lo que la lista se actualizará mínimo dos acceso a la información para asegurar este compromiso, hacemos pública a veces al año. Asimismo, se irán ampliando progresivamente los datos través de nuestra página web la lista de fábricas de nivel 1 (tier 1) que han aportados sobre nuestra cadena de suministro. producido para MANGO en el presente año 2020. País Fábrica Dirección Ciudad Categoría Nº Empleados ALBANIA DONA ELEGANT SHPK Rruga Vangjel Noti, Ambiente Edil Tirane Complementos < 1000 Centro, Kapanoni 1, Uz 2000, 1029 BANGLADESH A.K.M. -

Annual Report 2018

CHINA VANKE CO., LTD.* (a joint stock company incorporated in the People’s Republic of China with limited liability) (Stock code: 2202) ANNUAL REPORT 2018 *For identification purpose only Important Notice: 1. The Board, the Supervisory Committee and the Directors, members of the Supervisory Committee and senior management of the Company warrant that in respect of the information contained in 2018 Annual Report (the “Report”, or “Annual Report”), there are no misrepresentations, misleading statements or material omission, and individually and collectively accept full responsibility for the authenticity, accuracy and completeness of the information contained in the Report. 2. The Report has been approved by the 18th meeting of the 18th session of the Board (the “Meeting”) convened on 25 March 2019. Mr. LIN Maode, vice chairman of the Board and a non-executive director, did not attend the Meeting due to business engagement, and had authorized Mr. CHEN Xianjun, a non-executive director, to attend the Meeting and execute voting rights on his behalf. All other directors attended the Meeting in person. 3. The Company’s proposal on dividend distribution for the year of 2018: The total amount of cash dividends proposed for distribution for 2018 will be RMB11,811,892,641.07 (inclusive of tax), accounting for 34.97% of the net profit for the year attributable to equity shareholders of the Company for 2018, without any bonus shares or transfer of equity reserve to the share capital. Based on the Company’s total number of 11,039,152,001 shares at the end of 2018, a cash dividend of RMB10.7 (inclusive of tax) will be distributed for each 10 shares. -

CHINA the Church of Almighty God: Prisoners Database (1663 Cases)

CHINA The Church of Almighty God: Prisoners Database (1663 cases) Prison term: 15 years HE Zhexun Date of birth: On 18th September 1963 Date and place of arrest: On 10th March 2009, in Xuchang City, Henan Province Charges: Disturbing social order and using a Xie Jiao organization to undermine law enforcement because of being an upper-level leader of The Church of Almighty God in mainland China, who was responsible for the overall work of the church Statement of the defendant: He disagreed with the decision and said what he believed in is not a Xie Jiao. Court decision: In February 2010, he was sentenced to 15 years in prison by the Zhongyuan District People’s Court of Zhengzhou City, Henan Province. Place of imprisonment: No. 1 Prison of Henan Province Other information: He was regarded by the Chinese authorities as a major criminal of the state and had long been on the wanted list. To arrest him, authorities offered 500,000 RMB as a reward to informers who gave tips leading to his arrest to police. He was arrested at the home of a Christian in Xuchang City, Henan Province. Based on the information from a Christian serving his sentence in the same prison, HE Zhexun was imprisoned in a separate area and not allowed to contact other prisoners. XIE Gao, ZOU Yuxiong, SONG Xinling and GAO Qinlin were arrested in succession alongside him and sentenced to prison terms ranging from 11 to 12 years. Source: https://goo.gl/aGkHBj Prison term: 14 years MENG Xiumei Age: Forty-one years old Date and place of arrest: On 14th August 2014, in Xinjiang Uyghur Autonomous Region Charges: Using a Xie Jiao organization to undermine law enforcement because of being a leader of The Church of Almighty God and organizing gatherings for Christians and the work of preaching the gospel in Ili prefecture Statement of the defendant: She claimed that her act did not constitute crimes. -

The Warehouse Ethical Sourcing Report 2021

ETHICAL SOURCING REPORT 2021 2 CONTENTS INTRODUCTION APPENDICES 04. CEO introduction 22. 2019 – 2020 KPI table 05. Programme at a glance 23. Factory policy poster 06. Top 20 source countries 24. Apparel tier 1 factory list 2020 SUMMARY 26. Apparel tier 2 factory list 08. 2020 summary 36. Apparel brand list 10. Her Project updates 37. Other categories factory list Getting the most from this report 12. COVID-19 updates 49. Country wage & working hour table A brief overview of our programme and progress in 2020 can be viewed on pages 5 and 8. Our key areas of focus 13. Responding to forced labour risks and achievements can be found on pages 10 to 20. SUSTAINABLE MATERIALS Finally, the appendices from page 22 reveal performance trends over the past two years, and feature our factory 16. Better Cotton Initiative policy poster, brand and factory lists and source country wage and working hour data. 17. Forest Stewardship Council OUR POLICY IN PRACTICE 19. Policy in practice ETHICAL SOURCING REPORT 2021 INTRODUCTION. ETHICAL SOURCING REPORT 2021 4 CEO’S INTRODUCTION. APPENDICES programme. I believe, given our scale and challenges and achievements to date, diversity, this is the leading programme as well the road ahead. We invite both of its kind within the New Zealand retail your encouragement and suggestions for Ethical Sourcing is just one programme sector. improvement. within The Warehouse’s suite of “Sustainable & affordable” initiatives. Within The Warehouse Group’s 2020 Finally, I want to express my sincere Sustainable & affordable is The POLICY IN PRACTICE POLICY Annual Report, I pledged that COVID-19 gratitude to our ethical sourcing Warehouse’s guiding statement and will not slow down our commitment specialists and their colleagues within branding device representing our to becoming one of New Zealand’s our 200 person strong sourcing team. -

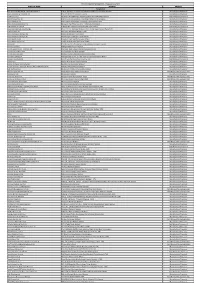

中国(偶蹄類の加熱処理肉等) 2021/5/25通知 No. NAME

中国(偶蹄類の加熱処理肉等) 2021/5/25通知 No. NAME ADDRESS TEMPORARY HUANG GANG NO.670, SHUN HUANG ROAD, SUN HE 1100/03009 BEIJING HORMEL FOODS CO.,LTD. COUNTY, CHAOYANG DISTRICT, BEIJING, CHINA 1100/03015 BEIJING DAFA CHIA TAI CO.,LTD YANGZHEN DUZHUANG, SHUNYI DISTRICT, BEIJING CITY, CHINA 1100/03039 BEIJING JIAYI FOOD JOINT FACTORY XIAOTANGSHAN TOWN, CHANGPING DISTRICT, BEIJING BEIJING ER SHANG MOQI ZHONGHONG FOODS NO. 233 NANGAO VILLAGE CUIGEZHUANG TOWNSHIP CHAOYANG 1100/15006 CO.,LTD. DISTRICT BEIJING, CHINA 1200/01025 TIANJIN LINGCHUAN FOOD CO.,LTD XINKOU INDUSTRIAL ZONE BY ROAD NO.18, XIQING DISTRICT, TIANJIN TIANJIN 3RD FOOD PRODUCTS PROCESSING 1200/03001 HANJIASHU, BEICHEN DISTRICT, TIANJIN FACTORY 1200/03008 TIANJIN MEAT PRODUCTS PROCESSING COMPLEX NO.8, YUEJIN ROAD, DONGLI DISTRICT, TIANJIN NO.8 XINWANG ROAD, SHUANGQIAOHE TOWN, JINNAN DISTRICT, 1200/03009 TIANJIN DONGTIAN FOODS PROCESSING CO., LTD TIANJIN, CHINA TIANJIN TEDA TIANQUAN QUICK FROZEN 1200/29002 NO.11, JINGU ROAD, TANGGU DISTRICT, TIANJIN FOODSTUFFS CO.,LTD. 1200/29005 TIANJIN GUOSHI FOOD CO., LTD. LANGYUAN VILLAGE, BEICHEN DISTRICT, TIANJIN 1200/29012 TIANJIN SHIYOU FOODSTUFFS CO.,LTD. SICUNDIAN, WUQING COUNTY, TIANJIN 1200/29016 TIANJIN NICKY FOODSTUFFS CO., LTD. 13 STREET, EXPORT PROCESSING ZONE, TIANJIN NO.171, MUSLIM BUSINESS TRADE STREET, XIADIAN TOWN, DACHANG 1300/03105 HEBEI SUPERB FOODS CO., LTD HUI AUTONOMY COUNTY, HEBEI PROVINCE, CHINA KANGBAO BAILU MEAT CO., LTD. THE SECOND 1300/03152 NO.134, GONGYE STREET, KANGBAO COUNTY, HEBEI FACTORY NO.9 HEBIN ROAD, LUANPINGTOWN, LUANPING COUNTY, CHENGDE 1300/03158 LUANPING HUADU JIAYI FOOD JOINT FACTORY CITY, HEBEI PROVINCE SHIJIAZHUANG DEYUAN FOOD CO.,LTD. 1300/03160 NO.77, XINYUANXI ROAD, LUANCHENG DISTRICT, SHIJIAZHUANG, HEBEI LUANCHENG BRANCH 1300/08040 SHIJIAZHUANG HUIKANG FOOD CO.,LTD.