Portland Kachkanar

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

We Want to Help the World Reach Net Zero and Improve People's Lives

BP Sustainability Report 2019 Our purpose is reimagining energy for people and our planet. We want to help the world reach net zero and improve people’s lives. We will aim to dramatically reduce carbon in our operations and production and grow new low carbon businesses, products and services. We will advocate for fundamental and rapid progress towards Paris and strive to be a leader in transparency. We know we don’t have all the answers and will listen to and work with others. We want to be an energy company with purpose; one that is trusted by society, valued by shareholders and motivating for everyone who works at BP. We believe we have the experience and expertise, the relationships and the reach, the skill and the will, to do this. Introduction Message from Bernard Looney 2 Our ambition 4 2019 at a glance Energy in context 8 Sustainability at BP UN Sustainable Development Goals 11 Sustainability at BP 11 Key sustainability issues 14 Our focus areas Climate change and the energy transition 16 Our role in the energy transition 18 Our ‘reduce, improve, create’ framework 20 Accrediting our lower carbon activities 22 Reducing emissions in our operations 23 Improving our products 26 Creating low carbon businesses 30 Safety 36 Process safety 38 Personal safety 39 Safety performance 41 Our value to society 42 Creating social value 44 Social investment 45 Local workers and suppliers 46 Human rights 47 Community engagement 48 Our impact on communities 49 Labour rights 50 Doing business responsibly Environment 54 People 60 Business ethics 68 Navigating our reports Governance Our quick read Human rights governance 74 provides a summary of the Executive oversight of sustainability 74 Sustainability Report, including key Managing risks 75 highlights and performance in 2019. -

FTSE Factsheet

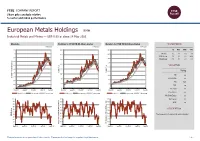

FTSE COMPANY REPORT Share price analysis relative to sector and index performance European Metals Holdings EMH Industrial Metals and Mining — GBP 0.69 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 1.1 450 900 1D WTD MTD YTD 1 Absolute 0.0 -6.8 -4.2 7.8 400 800 Rel.Sector 1.2 -2.9 -7.5 -20.3 0.9 700 Rel.Market -1.1 -5.5 -4.8 -1.3 350 0.8 600 300 0.7 VALUATION 500 0.6 250 400 Trailing Relative Price Relative 0.5 Price Relative 200 300 PE -ve 0.4 Absolute Price (local currency) (local Price Absolute 150 EV/EBITDA -ve 200 0.3 PB 12.3 100 0.2 100 PCF -ve 0.1 50 0 Div Yield 0.0 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales +ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.0 100 90 90 Div Payout 0.0 90 80 80 ROE -ve 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 40 The Company is focusing in tin mining industry. -

Prospectus Front and Back 2016

IMPORTANT NOTICE THE PROSPECTUS (THE “PROSPECTUS”) FOLLOWING THIS PAGE MAY ONLY BE DISTRIBUTED TO PERSONS WHO ARE EITHER (1) QUALIFIED INSTITUTIONAL BUYERS (“QIBs”) WITHIN THE MEANING OF RULE 144A (“RULE 144A”) UNDER THE U.S. SECURITIES ACT OF 1933 (THE “SECURITIES ACT”), OR (2) NON-U.S. PERSONS OUTSIDE THE UNITED STAT ES WITHIN THE MEANING OF REGULATION S (“REGULATION S”) UNDER THE SECURITIES ACT. IMPORTANT: You must read the following before continuing. The following applies to the Prospectus following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of this document. In accessing the Prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. RESTRICTIONS: NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER TO SELL OR A SOLICITAT ION OF AN OFFER TO BUY THE NOTES IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. ANY NOTE TO BE ISSUED HAS NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACT, OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OF THE UNITED STATES OR OTHER JURISDICTION. THE NOTES MAY NOT BE OFFERED, SOLD, PLEDGED OR OTHERWISE TRANSFERRED DIRECTLY OR INDIRECTLY WITHIN THE UNITED STAT ES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S) EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. -

ACQUIRING FAITH a Siberian Childhood

A JOURNAL OF ORTHODOX FAITH AND CULTURE ROAD TO EMMAUS Help support Road to Emmaus Journal. The Road to Emmaus staff hopes that you find our journal inspiring and useful. While we offer our past articles on-line free of charge, we would warmly appreciate your help in covering the costs of producing this non-profit journal, so that we may continue to bring you quality articles on Orthodox Christianity, past and present, around the world. Thank you for your support. Please consider a donation to Road to Emmaus by visiting the Donate page on our website. ACQUIRING FAITH A Siberian Childhood by Nina Kartasheva The compelling story of a Soviet childhood through the eyes of a woman born to Orthodox exiles in the Ural town of Verkhoturye. Nina Kartasheva’s childhood recollections are offset by her account of a later critical illness and the miraculous intervention of the last Russian Royal Family. “The rule of faith and the model of meekness...” I’m reading, as I often do, the troparion to St. Nicholas and remembering the days of my childhood in the far-away Northern Urals, in Verkhoturye, where both my grandmoth- ers were exiled in the 30’s with their children, who afterwards became my parents. I appeared at a later, calmer time when there were no repressions and no one considered my grandmothers to be exiles. Under Krushchev, however, the attitude towards the faith again became blasphemous, to put it mildly, and intolerant if we choose to use harder and more truthful words. Despite everything, traditions were kept up in the old Russian families, along with religious practices and the faith itself. -

1 Adcmemorial.Org Alternative Report on the Russian Federation's

adcmemorial.org Alternative Report on the Russian Federation’s Implementation of the International Covenant on Economic, Social and Cultural Rights in Connection with the Consideration of the Sixth Periodic State Report (2016) by the UN Committee on Economic, Social and Cultural Rights For the Pre-Sessional Working Group of the 60th Session of the CESCR 27 February – 3 March 2017 года The Russian Federation: Violation of the Economic and Social Rights of Roma and Indigenous Minorities; Employment Discrimination against Vulnerable Groups 1 CONTENTS PREAMBLE……………………………………………………………………………………………….3 VIOLATION OF THE RIGHTS OF ROMA AND INDIGENOUS PEOPLES……………………….4 Problem: demolition of housing in dense Roma settlements, eviction of residents, deprivation of access to resources………………………………………………………………….4 Problem: violation of the rights of Roma children to education – segregation into separate “Roma” classes and schools, difficulties accessing preschool education, lack of educational opportunities for people who left or never attended school at all for various reasons………………………………………………………………………………………….6 Problem: absence of a comprehensive government strategy to overcome structural discrimination of the Roma population in the Russian Federation……………………………7 Problem: violation of the economic, social and cultural rights of indigenous peoples – seizure of territories where these peoples traditionally live and maintain their households by mining and oil and gas companies; removal of self-government bodies of indigenous peoples; repression of activists and employees of social organizations, including the fabrication of criminal cases………………………………………………………………………….7 EMPLOYMENT DISCRIMINATION OF VULNERABLE GROUPS……………………………….11 Problem: the existence of the “list of professions banned for women” results in employment discrimination against women; the Russian Federation is not implementing the recommendations and rulings of international institutions (CEDAW) to abolish this list. -

DISCOVER URAL Ekaterinburg, 22 Vokzalnaya Irbit, 2 Proletarskaya Street Sysert, 51, Bykova St

Alapayevsk Kamyshlov Sysert Ski resort ‘Gora Belaya’ The history of Kamyshlov is an The only porcelain In winter ‘Gora Belaya’ becomes one of the best skiing Alapayevsk, one of the old town, interesting by works in the Urals, resort holidays in Russia – either in the quality of its ski oldest metallurgical its merchants’ houses, whose exclusive faience runs, the service quality or the variety of facilities on centres of the region, which are preserved until iconostases decorate offer. You can rent cross-country skis, you can skate or dozens of churches around where the most do snowtubing, you can visit a swimming-pool or do rope- honorable industrial nowadays. The main sight the world, is a most valid building of the Middle 26 of Kamyshlov is two-floored 35 reason to visit the town of 44 climbing park. In summer there is a range of active sports Urals stands today, is Pokrovsky cathedral Sysert. You can go to the to do – carting, bicycling and paintball. You can also take inseparably connected (1821), founded in honor works with an excursion and the lifter to the top of Belaya Mountain. with the names of many of victory over Napoleon’s try your hand at painting 180 km from Ekaterinburg, 1Р-352 Highway faience pieces. You can also extend your visit with memorial great people. The elegant Trinity Church was reconstructed army. Every august the jazz festival UralTerraJazz, one of the through the settlement of Uraletz by the direction by the renowned architect M.P. Malakhov, and its burial places of industrial history – the dam and the workshop 53 top-10 most popular open-air fests in Russia, takes place in sign ‘Gora Belaya’ + 7 (3435) 48-56-19, gorabelaya.ru vaults serve as a shelter for the Romanov Princes – the Kamyshlov. -

Information for Persons Who Wish to Seek Asylum in the Russian Federation

INFORMATION FOR PERSONS WHO WISH TO SEEK ASYLUM IN THE RUSSIAN FEDERATION “Everyone has the right to seek and to enjoy in the other countries asylum from persecution”. Article 14 Universal Declaration of Human Rights I. Who is a refugee? According to Article 1 of the Federal Law “On Refugees”, a refugee is: “a person who, owing to well‑founded fear of being persecuted for reasons of race, religion, nationality, membership of particular social group or politi‑ cal opinion, is outside the country of his nationality and is unable or, owing to such fear, is unwilling to avail himself of the protection of that country”. If you consider yourself a refugee, you should apply for Refugee Status in the Russian Federation and obtain protection from the state. If you consider that you may not meet the refugee definition or you have already been rejected for refugee status, but, nevertheless you can not re‑ turn to your country of origin for humanitarian reasons, you have the right to submit an application for Temporary Asylum status, in accordance to the Article 12 of the Federal Law “On refugees”. Humanitarian reasons may con‑ stitute the following: being subjected to tortures, arbitrary deprivation of life and freedom, and access to emergency medical assistance in case of danger‑ ous disease / illness. II. Who is responsible for determining Refugee status? The responsibility for determining refugee status and providing le‑ gal protection as well as protection against forced return to the country of origin lies with the host state. Refugee status determination in the Russian Federation is conducted by the Federal Migration Service (FMS of Russia) through its territorial branches. -

2019 Annual Report

Table of Contents A Message from the Chairman.............................................................. 1 A Message from the President .............................................................. 3 Our Impact .................................................................................... 4 What’s Unique About Sister Cities International?....................................... 5 Global Leaders Circle............................................................................... 6 2018 Activities....................................................................................... 7 Where We Are (Partnership Maps) ........................................................ 14 Membership with Sister Cities International ........................................... 18 Looking for a Sister City Partner?......................................................... 19 Membership Resources and Discounts ................................................. 20 Youth Leadership Programs ............................................................... 21 YAAS 2018 Winners & Finalists ............................................................ 23 2018 Youth Leadership Summit .......................................................... 24 Sister Cities International’s 2018 Annual Conference in Aurora, Colorado.......................................................................... 26 Annual Awards Program Winners......................................................... 27 Special Education and Virtual Learning in the United States and Palestine (SEVLUP) -

Systemic Criteria for the Evaluation of the Role of Monofunctional Towns in the Formation of Local Urban Agglomerations

ISSN 2007-9737 Systemic Criteria for the Evaluation of the Role of Monofunctional Towns in the Formation of Local Urban Agglomerations Pavel P. Makagonov1, Lyudmila V. Tokun2, Liliana Chanona Hernández3, Edith Adriana Jiménez Contreras4 1 Russian Presidential Academy of National Economy and Public Administration, Russia 2 State University of Management, Finance and Credit Department, Russia 3 Instituto Politécnico Nacional, Escuela Superior de Ingeniería Mecánica y Eléctrica, Mexico 4 Instituto Politécnico Nacional, Escuela Superior de Cómputo, Mexico [email protected], [email protected], [email protected] Abstract. There exist various federal and regional monotowns do not possess any distinguishing self- programs aimed at solving the problem of organization peculiarities in comparison to other monofunctional towns in the periods of economic small towns. stagnation and structural unemployment occurrence. Nevertheless, people living in such towns can find Keywords. Systemic analysis, labor migration, labor solutions to the existing problems with the help of self- market, agglomeration process criterion, self- organization including diurnal labor commuting migration organization of monotown population. to the nearest towns with a more stable economic situation. This accounts for the initial reason for agglomeration processes in regions with a large number 1 Introduction of monotowns. Experimental models of the rank distribution of towns in a system (region) and evolution In this paper, we discuss the problems of criteria of such systems from basic ones to agglomerations are explored in order to assess the monotown population using as an example several intensity of agglomeration processes in the systems of monotowns located in Siberia (Russia). In 2014 the towns in the Middle and Southern Urals (the Sverdlovsk Government of the Russian Federation issued two and Chelyabinsk regions of Russia). -

P4 Prime Minister Launches the Aberdare Trust - P8

THE NEWSLETTER OF THE RHINO ARK CHARITABLE TRUST NO. 41 NOVEMBER 2012 RHINO CHARGE 2012 REsults - p4 PRImE mINIstER lAuNCHEs tHE AbERdARE tRust - P8 FINANCE mINIstER lAuNCHEs tHE mt KENyA FENCE - P9 2012 AbERdARE FENCE RuN GEts ROyAl NOd - P24 The Winning Team BRAEBURN’SEBURN’S CAR 49, CAPTAINED BY PATRICK GARNER AND TERRY CHILDS,CHILDS WONWON THE 2012 RHINO CHARGE. Winning is a goal we all strive for, but howw wewe achieve that goal is perhaps even more important. Those that make it to the totopp need real determination to keep going when things getet tough;tough; they need a “can-do” sort of attitude and a desire to deal with diffi culties head-on and not try to skirt around them or take the easy wayway out. Determination, a positive mindset, an ability to work with others as a team to support, encourage and be encouraged are the characteracter traits that success in all walks of life are built on. We all face challenges at different stages of our life; it is how we deal with these challengeslenges that will gauge how successful we will go on to be. The Braeburn Group of International Schools boasts an ethos of nurturing personal growthth byby providing a friendly and supportive environment in all our schools in East Africa. Early years, primary and secondary students develop thehe skills,skills, attitudes andan awareness necessary to become successful learners, confi dent individuals and responsible citizens. We congratulate the whole team! Rhino Ark Objectives Rhino Ark seeks solutions in the mountain range ecosystems of Executive Director’s view Kenya and for the benefit of Eastern s ht Africa generally to: rec At the crossroad… Christian Lamb • Conserve such ecologically precious indigenous forests and their provision of vital During the last 24 years, rarely have so many changes have taken place environmental services; in only a few months. -

View Annual Report

2015 Annual Report & Accounts MAKING THE WORLD STRONGER Report This annual report (“the Report”) presents the results for EVRAZ plc and its subsidiaries for 2015, divided into segments: Steel, Steel North America and Coal. It details the Group’s operational and financial results and corporate social responsibility activities in 2015. The Report has been prepared in accordance with the information disclosure requirements of the United Kingdom and the Financial Conduct Authority: Č the Companies Act 2006; Č the Listing Rules; Č the Disclosure and Transparency Rules; Č Competition and Market Authority Order. The Report has also been prepared on the basis of the International Integrated Reporting Framework and the GRI G4 Sustainability Reporting Guidelines and contains elements of an integrated and a sustainability report. It has been approved by the Board of Directors. The main theme of the Report is value creation, as detailed in the EVRAZ Business Model section. On 13 April 2015, Evraz Highveld Steel and Vanadium Ltd. (“EHS”) implemented a business rescue procedure and the regulator appointed an external business rescue practitioner to EHS. As of 13 April 2015, control over EHS passed to the business rescue practitioner, and EVRAZ has no influence over the executives or management of EHS and does not have ongoing access to information about its current activities. The Group has relinquished control over and deconsolidated EHS. Information about EHS for the period to 13 April 2015 was disclosed in corresponding disclosure announcements. -

Vanishing Worlds ______THESIS TITLE

Vanishing Worlds ____________________________________________ THESIS TITLE (Choose fiction or non-fiction, then select the genre that best describes your thesis from the dropdown menu) Fiction: Novel Stories Other: Nonfiction: Memoir Stories X Essays Other: by Sam Keck Scott _____________________ STUDENT NAME A CREATIVE THESIS submitted to Southern New Hampshire University in partial fulfillment of the requirements for the degree of Master of Fine Arts in Creative Writing School of Liberal Arts May 18, 2021 _____________________ DATE OF THESIS COMPLETION This thesis has been examined and approved. Lydia Peelle _____________________________________ Thesis Director’s Name Mark Sundeen ______________________________________ Second Reader’s Name Vanishing Worlds A Collection of Essays By Sam Keck Scott Final Thesis Sam Keck Scott 2 Table of Contents The Fire Flowers of Malta ----------------------------------------------------------------------- 5 Red Sea Blue -------------------------------------------------------------------------------------- 20 Searching for Lost Worlds --------------------------------------------------------------------- 38 Living Light --------------------------------------------------------------------------------------- 61 Dreaming of Water with Tiger Salamanders ---------------------------------------------- 64 Sea Stars Disappearing, Reappearing ------------------------------------------------------- 80 Final Thesis Sam Keck Scott 3 Author’s Note: The essays compiled in this collection are each meant to stand on