Greater Downtown Miami Annual Residential Market Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Florida Baptist Heritage

Published by the FLORIDA BAPTIST HISTORICAL SOCIETY Dr. Mark A. Rathel Secretary-Treasurer 5400 College Drive Graceville, Florida 32440 (850) 263-3261 Fax: (850) 263-7506 E-mail: [email protected] Board of Directors The State Board of Missions of the Florida Baptist Convention elects the Board of Directors. Dr. John Sullivan Executive Director, Florida Baptist Convention Dr. Irvin Murrell Director of Library Services The Baptist College of Florida Curator, Florida Baptist Historical Collection Dr. R. C. Hammack, Chairman Administrative Vice-President The Baptist College of Florida Dr. Fred Donehoo, Vice-Chairman Christian School Consultant, Lake Placid Mrs. Toni Clevenger Pensacola Mrs. Patricia Parks School Superintendent, Hamilton County Journal of the Florida Baptist Historical Society Rev. John Hillhouse Florida Baptist Heritage Journalist, Lighthouse Point Mrs. Debbie Gillette Church Secretary, Indian Rocks, Largo Dr. David Gasperson Sherbrooke Baptist Church, Lake Worth Page 3 EDITORIAL Mark A. Rathel Page 5 A HISTORY OF AFRICAN AMERICANS FLORIDA BAPTISTS Sid Smith Page 29 A HISTORY OF NATIVE AMERICANS IN FLORIDA John C. Hillhouse, Jr. Page 42 FLORIDA BAPTIST Contents HISPANIC HERITAGE Milton S. Leach, Jr. Page 56 A HISTORY OF HAITIAN SOUTHERN BAPTIST CHURCHES IN FLORIDA Lulrick Balzora EDITORIAL PERSPECTIVE Mark Rathel Secretary Treasurer Florida Baptist Historical Society Welcome to the Second Issue of The Journal of Florida Baptist Heritage! Florida Baptists are a rich mosaic of cultures, traditions, and languages. Indeed, Florida Baptists minister in a context of international missions within the state boundaries. This second volume attempts to celebrate our diversity by reflecting on the history of selected ethnic groups in Florida Baptist life. -

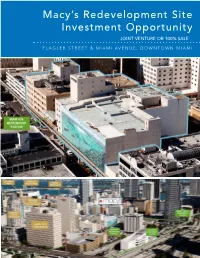

Macy's Redevelopment Site Investment Opportunity

Macy’s Redevelopment Site Investment Opportunity JOINT VENTURE OR 100% SALE FLAGLER STREET & MIAMI AVENUE, DOWNTOWN MIAMI CLAUDE PEPPER FEDERAL BUILDING TABLE OF CONTENTS EXECUTIVE SUMMARY 3 PROPERTY DESCRIPTION 13 CENTRAL BUSINESS DISTRICT OVERVIEW 24 MARKET OVERVIEW 42 ZONING AND DEVELOPMENT 57 DEVELOPMENT SCENARIO 64 FINANCIAL OVERVIEW 68 LEASE ABSTRACT 71 FOR MORE INFORMATION, CONTACT: PRIMARY CONTACT: ADDITIONAL CONTACT: JOHN F. BELL MARIANO PEREZ Managing Director Senior Associate [email protected] [email protected] Direct: 305.808.7820 Direct: 305.808.7314 Cell: 305.798.7438 Cell: 305.542.2700 100 SE 2ND STREET, SUITE 3100 MIAMI, FLORIDA 33131 305.961.2223 www.transwestern.com/miami NO WARRANTY OR REPRESENTATION, EXPRESS OR IMPLIED, IS MADE AS TO THE ACCURACY OF THE INFORMATION CONTAINED HEREIN, AND SAME IS SUBMITTED SUBJECT TO OMISSIONS, CHANGE OF PRICE, RENTAL OR OTHER CONDITION, WITHOUT NOTICE, AND TO ANY LISTING CONDITIONS, IMPOSED BY THE OWNER. EXECUTIVE SUMMARY MACY’S SITE MIAMI, FLORIDA EXECUTIVE SUMMARY Downtown Miami CBD Redevelopment Opportunity - JV or 100% Sale Residential/Office/Hotel /Retail Development Allowed POTENTIAL FOR UNIT SALES IN EXCESS OF $985 MILLION The Macy’s Site represents 1.79 acres of prime development MACY’S PROJECT land situated on two parcels located at the Main and Main Price Unpriced center of Downtown Miami, the intersection of Flagler Street 22 E. Flagler St. 332,920 SF and Miami Avenue. Macy’s currently has a store on the site, Size encompassing 522,965 square feet of commercial space at 8 W. Flagler St. 189,945 SF 8 West Flagler Street (“West Building”) and 22 East Flagler Total Project 522,865 SF Street (“Store Building”) that are collectively referred to as the 22 E. -

ZOM Living Buys Land, Scores Financing for Luma at Miami Worldcenter

SOUTH FLORIDA REAL ESTATE NEWS ZOM Living buys land, scores financing for Luma at Miami Worldcenter ZOM plans a 43-story apartment tower with 434 units By Keith Larsen | April 18, 2019 11:36AM ZOM Living bought the land and scored a $119 million construction loan to build a 43-story apartment tower at Miami Worldcenter. Records show ZOM bought the property near Northeast First Avenue and Northeast Eighth Street for $19.5 million. The Orlando-based developer secured the loan from the New York-based Moinian Group, records show. The Moinian Group will also be a partner in the project, according to a press release. The new apartments will be a center point of the 27-acre, $4 billion Miami Worldcenter project, led by developers Nitin Motwani and Art Falcone. Greg West CEO of ZOM Living and a rendering of Luma (Credit: LinkedIn) Luma will have 434 apartments, which will span 556 square feet to 1,808 square feet. Amenities will include a wellness center, a sundry shop, speakeasy, dog salon, fitness club with a classroom, and a pool. Construction is expected to begin in July and will take about 30 months, according to ZOM Living CEO Greg West. The development group behind Miami Worldcenter also secured a $34.7 million loan from Bank OZK for a parking garage that will be used for the Luma. Cushman & Wakefield Robert Given and Robert Kaplan secured equity and debt financing on behalf of ZOM Living and the Moinian Group. Miami Worldcenter, a mix of retail, residential, hotels and office space, is among the biggest real estate projects on the East Coast. -

Wynwood Development Table of Contents 03 Project Overview

TOTAL AREA: 60,238 SQ.FT. Wynwood Development Table of Contents 03 Project Overview 15 Conceptual Drawings 17 Location 20 Demographics 23 Site Plan 26 Building Efficiency 29 RelatedISG Project Overview Project This featured property is centrally located in one of Miami’s hottest and trendiest neighborhood, Wynwood. The 60,238 SF site offers the unique possibility to develop one of South Florida’s most ground-breaking projects. There has only been a select amount of land deals in the past few years available in this neighborhood, and it is not common to find anything over 20,000 SF on average. With its desirable size and mixed use zoning, one can develop over 300 units with a retail component. Wynwood has experienced some of the highest rental rates of any area of South Florida, exceeding $3 per SF, and retail rates exceeding $100 SF. As the area continues to grow and evolve into a world renowned destination, it is forecasted that both residential and retail rental rates will keep increasing. Major landmark projects such as the Florida Brightline and Society Wynwood, as well as major groups such as Goldman Sachs, Zafra Bank, Thor Equity and Related Group investing here, it is positioned to keep growing at an unprecedented rate. Name Wynwood Development Style Development Site Location Edgewater - Miami 51 NE 22th Street Miami, FL 33137 Total Size 60,238 SQ. FT. (1.3829 ACRES) Lot A 50 NE 23nd STREET Folio # 01-3125-015-0140 Lot B 60 NE 23nd STREET Folio 01-3125-011-0330 Lot C 68 NE 23rd STREET Folio 01-3125-011-0320 Lot D 76 NE 23rd STREET Folio 01-3125-011-0310 Lot E 49 NE 23rd STREET Folio 01-3125-015-0140 Lot F 51 NE 23rd STREET Folio 01-3125-015-0130 Zoning T6-8-O URBAN CORE TRANSECT ZONE 04 Development Regulations And Area Requirements DEVELOPMENT REGULATIONS AND AREA REQUIREMENTS DESCRIPTION VALUE CODE SECTION REQUIRED PERMITTED PROVIDED CATEGORY RESIDENTIAL PERMITTED COMMERCIAL LODGING RESIDENTIAL COMMERCIAL LODGING RESIDENTIAL LODGING PERMITTED GENERAL COMMERCIAL PERMITTED LOT AREA / DENSITY MIN.5,000 SF LOT AREA MAX. -

RKW RESIDENTIAL Continues South Florida Growth with Edgewater

Media Contact: Eric Kalis, BoardroomPR [email protected] 954-370-8999 RIVERGATE KW RESIDENTIAL Continues South Florida Growth with Edgewater Community Leading property management company tapped for lease up and management of 2500 Biscayne MIAMI (Oct. 3, 2017) — RIVERGATE KW RESIDENTIAL, a leading multifamily property management company, has expanded its South Florida portfolio as exclusive property manager and leasing agents for 2500 Biscayne in Miami’s Edgewater neighborhood. The brand new apartment tower will begin leasing in later this month. One- and two-bedroom units at 2500 Biscayne are designed with open floor layouts that include chef-inspired kitchens with European cabinets, quartz countertops, walk-in closets, private patios and balconies, in-unit washer and dryers, porcelain tile floors, energy-efficient stainless steel appliances and oversized windows to maximize natural light. Residents of the sleek, pet-friendly, 19-story apartment tower can enjoy a rooftop lounge, views of Biscayne Bay, a saltwater pool, private cabanas, lounge with coffee bar, and fitness center. “2500 Biscayne is a premier property in one of Miami’s most desirable neighborhoods that offers a mix of amenities, retail and culture, and we are excited to contribute to its success,” said Marcie Williams, president of RIVERGATE KW RESIDENTIAL. “We look forward to the opportunity to work with Greystone Development on this stunning community.” Surrounding neighborhoods include Wynwood, Brickell and Downtown, making local attractions such as the Wynwood Farmers’ Market, Margaret Pace Park, the Design District and other shopping, dining, theaters and bars easily accessible. “With the opening of 2500 Biscayne, we are thrilled to bring on RIVERGATE KW Residential to bring the property to market with a rapid lease-up,” said Jeff Simpson of Greystone Development. -

Miami-Dade County Commission on Ethics and Public Trust

Biscayne Building 19 West Flagler Street Miami-Dade County Suite 220 Miami, Florida 33130 Commission on Ethics Phone: (305) 579-2594 Fax: (305) 579-2656 and Public Trust Memo To: Mike Murawski, independent ethics advocate Cc: Manny Diaz, ethics investigator From: Karl Ross, ethics investigator Date: Nov. 14, 2007 Re: K07-097, ABDA/ Allapattah Construction Inc. Investigative findings: Following the June 11, 2007, release of Audit No. 07-009 by the city of Miami’s Office of Independent Auditor General, COE reviewed the report for potential violations of the Miami-Dade ethics ordinance. This review prompted the opening of two ethics cases – one leading to a complaint against Mr. Sergio Rok for an apparent voting conflict – and the second ethics case captioned above involving Allapattah Construction Inc., a for-profit subsidiary of the Allapattah Business Development Authority. At issue is whether executives at ABDA including now Miami City Commissioner Angel Gonzalez improperly awarded a contract to Allapattah Construction in connection with federal affordable housing grants awarded through the city’s housing arm, the Department of Community Development. ABDA is a not-for-profit social services agency, and appeared to pay itself as much as $196,000 in profit and overhead in connection with the Ralph Plaza I and II projects, according to documents obtained from the auditor general. The city first awarded federal Home Investment Partnership Program (HOME) funds to ABDA on April 15, 1998, in the amount of $500,000 in connection with Ralph Plaza phase II. On Dec. 17, 2002, the city again awarded federal grant monies to ABDA in the amount of $730,000 in HOME funds for Ralph Plaza phase II. -

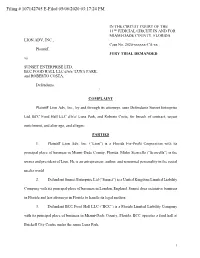

Filing # 107142705 E-Filed 05/06/2020 03:17:24 PM

Filing # 107142705 E-Filed 05/06/2020 03:17:24 PM IN THE CIRCUIT COURT OF THE 11TH JUDICIAL CIRCUIT IN AND FOR MIAMI-DADE COUNTY, FLORIDA LION ADV, INC., Case No. 2020-xxxxxx-CA-xx Plaintiff, JURY TRIAL DEMANDED vs. SUNSET ENTERPRISE LTD, BCC FOOD HALL LLC d/b/a/ LUNA PARK, and ROBERTO COSTA, Defendants. ______________________________________/ COMPLAINT Plaintiff Lion Adv, Inc., by and through its attorneys, sues Defendants Sunset Enterprise Ltd, BCC Food Hall LLC d/b/a/ Luna Park, and Roberto Costa, for breach of contract, unjust enrichment, and alter ego, and alleges: PARTIES 1. Plaintiff Lion Adv, Inc. (“Lion”) is a Florida For-Profit Corporation with its principal place of business in Miami-Dade County, Florida. Mirko Scarcella (“Scarcella”) is the owner and president of Lion. He is an entrepreneur, author, and renowned personality in the social media world. 2. Defendant Sunset Enterprise Ltd (“Sunset”) is a United Kingdom Limited Liability Company with its principal place of business in London, England. Sunset does extensive business in Florida and has attorneys in Florida to handle its legal matters. 3. Defendant BCC Food Hall LLC (“BCC”) is a Florida Limited Liability Company with its principal place of business in Miami-Dade County, Florida. BCC operates a food hall at Brickell City Centre under the name Luna Park. 1 4. Defendant Roberto Costa (“Costa”) is the owner of BCC. Costa also owns eleven other restaurants around the world. RELEVANT NON-PARTY WITNESSES 5. Walter Gumina (“Mr. Gumina”) is an employee or agent of BCC. 6. Muhammad Asif (“Mr. Asif”) is the CFO of G-Life Corp., another Costa company. -

Miami Condos Most at Risk Sea Level Rise

MIAMI CONDOS MIAMI CONDOS MOST AT RISK www.emiami.condos SEA LEVEL RISE RED ZONE 2’ 3’ 4’ Miami Beach Miami Beach Miami Beach Venetian Isle Apartments - Venetian Isle Apartments - Venetian Isle Apartments - Island Terrace Condominium - Island Terrace Condominium - Island Terrace Condominium - Costa Brava Condominium - -Costa Brava Condominium - -Costa Brava Condominium - Alton Park Condo - Alton Park Condo - Alton Park Condo - Mirador 1000 Condo - Mirador 1000 Condo - Mirador 1000 Condo - Floridian Condominiums - Floridian Condominiums - Floridian Condominiums - South Beach Bayside Condominium - South Beach Bayside Condominium - South Beach Bayside Condominium - Portugal Tower Condominium - Portugal Tower Condominium - Portugal Tower Condominium - La Tour Condominium - La Tour Condominium - La Tour Condominium - Sunset Beach Condominiums - Sunset Beach Condominiums - Sunset Beach Condominiums - Tower 41 Condominium - Tower 41 Condominium - Tower 41 Condominium - Eden Roc Miami Beach - Eden Roc Miami Beach - Eden Roc Miami Beach - Mimosa Condominium - Mimosa Condominium - Mimosa Condominium - Carriage Club Condominium - Carriage Club Condominium - Carriage Club Condominium - Marlborough House - Marlborough House - Marlborough House - Grandview - Grandview - Grandview - Monte Carlo Miami Beach - Monte Carlo Miami Beach - Monte Carlo Miami Beach - Sherry Frontenac - Sherry Frontenac - Sherry Frontenac - Carillon - Carillon - Carillon - Ritz Carlton Bal Harbour - Ritz Carlton Bal Harbour - Ritz Carlton Bal Harbour - Harbor House - Harbor House -

First Came Brickell, Then Came the Bay-View Towers on Biscayne Boulevard

June 24, 2021 First came Brickell, then came the bay-view towers on Biscayne Boulevard. Increasingly, the blocks between them are filling in with rentals and condos — a decided departure from the courthouses, Miami Dade College buildings and discount shops that have long lined these streets. The latest is the 501 First Residences, a 40-story condo at 501 NE First Ave. that will be home to 448 fully furnished condo units. Prices will start at $300,000 for a 400-square-foot studio; a two- bedroom, two-bath twice that size will go for $800,000, according to Peggy Olin, CEO of the Fort Lauderdale-based brokerage firm OneWorld Properties. Don’t call the moving truck just yet. Construction is anticipated to start in the first quarter of 2022 and be completed by late 2024, said David Arditi, principal and co-founder of the Edgewater-based Aria Development Group, the firm behind the project. The project will be the firm’s second in the area — after YotelPad Miami — and more are already in the works, Arditi said. Aria Development Group is working on three more residential projects in Downtown Miami. Despite the prime location near Brickell Avenue, downtown cultural venues and the FTX (formerly AmericanAirlines) Arena, the blocks west of Biscayne Boulevard have been slow to draw residential development. But investments by the Miami Downtown Development Authority and private enterprise including Brightline and Miami Worldcenter have led to new projects, including the now-opened Paramount, the planned Legacy Residences and E11EVEN Hotel & Residences. Arditi credits the commuter Brightline service from Miami to West Palm Beach as a key component. -

Locator Keys Identify Sites on This Map, 23 Heading NW from the Confluence of the P Miami River and Biscayne Bay

A NOTE USING THIS GUIDE… Locator keys identify sites on this map, 23 heading NW from the confluence of the P Miami River and Biscayne Bay. Locator keys are in one of the following four 21 categories: HISTORIC SITES: Blue numbers 22 RIVER BRIDGES: Blue letters POINTS OF INTEREST: Green numbers AREA BUSINESSES: Red numbers MIAMI RIVER BRIDGE Bascule (B); Fixed (F) 3 Brickell Bridge (B) . A 19 27 Metro Mover Bridge (F) . B South Miami Avenue (B) . C 2021 O Metrorail (F) . .D S .W . 2nd Avenue (B) . E Interstate I-95 (3F) . F 14 N S .W . First Street (B) . G West Flagler Street (B) . .H 15 N .W . 5th Street (B) . I 24 N .W . 12th Avenue (B) . J 18 19 S .R . 836/Dolphin Expwy . (F) . K 16 14 N .W . 17th Avenue (B) . L M 12 N .W . 22nd Avenue (B) . M 13 N .W . 27th Avenue (B) . N 16 N .W . South River Dr . (B) . O Railroad (B) . P 12 13 L 32 30 POINTS OF INTEREST 4 Beginning of Miami River Greenway . 1 K 10 34 27 James L . Knight Convention Center . 2 J Metro-Mover “Fifth Street” Station .3 26 34 11 Metro-Mover “Riverwalk” Station . 4 MIAMI RIVER BUSINESSES 22 12 Metro-Rail “Brickell” Station . 5 1 5TH STREET MARINA 11 DOWNTOWN DEVELOPMENT AUTHORITY 21 MARITIME AGENCY INC 32 RIVER LANDING Miami-Dade Cultural Center . 6 Marina To grow, strengthen & promote Downtown Miami International Shipping Terminal Retail, Restaurants, Residential 341 NW South River Dr. Miami 33128 (305) 579-6675 3630 NW North River Dr. -

Curriculum Vitae

Curriculum Vitae JEFF CHOOPANI AIA HIGHER EDUCATION Institutional: Florida International Bachelor of Architectural Technology 1988 (Civil Engineering Minor) West Stark Community College Ft Smith, Arkansas Associate in Arts 1979 Certifications: Post-Disaster Safety Assessment Evaluator Training 2009 Members: (AIA) American Institute of Architects (ASTM) American Society for Testing and Materials (BOMA) Building Owners and Managers Association EXPERIENCE QUALIFICATIONS. Knowledgeable and experienced within all aspects of Exterior Wall (Structural and Conventional Panel Systems, Stick Systems, Doors, Windows, Storefronts and Masonry Systems. With over 20 years of experience in providing Exterior Wall Testing Laboratory services inspections. I have 12 years of experience in waterproofing systems (above and below grade); concrete restoration and exterior field applied insulated finishes systems (convention or panel systems). PROFESSIONAL Miami Curtain Wall Consultants, Corp Current Principal, Senior Consultant, Founding Member Client Representative: Produce specifications for the exterior (i.e., Curtain walls, window walls, cladding, masonry, masonry/ stone composite walls) for project construction documents. Provide a full range of Quality Control Procedures on significant buildings. Organized and coordinated the quality control procedures utilized on building systems for manufacturing, delivery, final erection and testing. Witnessed construction of full scale project mock-ups and issued test reports. Provided remedial solutions to problems during testing that where later implemented in buildings already under construction. Reviewed architectural and shop drawings for inadequacies in the areas of water penetration, condensation, vapor penetration, anti-terrorism, and structural performance during design development and construction document phase of projects. Supervised inspections conducted daily in the field and shop. Observed and recorded day to day operations between architects, engineers and contractors. -

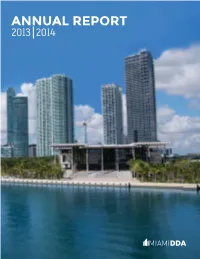

Annual Report 2013 2014 Message to Our About Us

ANNUAL REPORT 2013 2014 MESSAGE TO OUR ABOUT US: The Miami Downtown Development Authority is an independent agency of the City of Miami DWNTWNRS funded by a special tax levy on properties within its district boundaries. The agency is governed by a 15-member board of directors, which includes three public appointees and 12 downtown property As we look back on the past year and embark on the one ahead, the facts are undeniable: Downtown Miami owners, business owners, and/or residents. The board sets policy direction, which is implemented by continues to defy expectations as one of the largest and most viable urban centers in the country. With dozens of a multi-disciplinary team under the oversight of the executive director. cranes proliferating our skyline and new construction on the rise, a livable and walkable urban core has gone from being a promise to a reality. Today, Downtown Miami stands tall with more than 220,000 people working and 80,750 people living in the district. This marks a population growth of more than 100 percent over the past decade – painting a picture of one of the fastest growing and youngest demographics in the country. Although the past year has welcomed a flurry of exciting developments, next year holds even more promise. Yet, we don’t need to tell you of this transformation; you see it unfold each and every day. From the launch of Pérez Art Museum Miami, to the soon-to-be-completed Patricia and Phillip Frost Museum of Science, to the successful Adrienne Arsht Center for the Performing Arts and the AmericanAirlines Arena, Downtown Miami is earning its reputation as an epicenter for arts and culture.