Consolidated Financial Statements 2019.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Airbox 4G+ Quick Start Guide @

Airbox 4G+ Quick Start Guide @ 1 M FR Insérer la carte SIM EN Insert SIM card SIM ES Inserta la tarjeta SIM NL Plaats de simkaart PL Włóż kartę SIM RO Introduceți cartela SIM RU Вставьте SIM-карту http://airbox.home SK Vložte Sim Kartu AR أدخل بطاقة SIM 2 FR Allumer le dispositif EN Switch on the device ES Enciende el dispositivo NL Zet het apparaat aan PL Włącz urządzenie RO Porniţi dispozitivul RU Включите устройство SK Zapnite Airbox AR قم بتشغيل الجهاز Airbox-xxxx 3 Connection x1 ********* x Security Key : *********** FR Se connecter au réseau WiFi de l’Airbox EN Connect to Airbox WiFi network OK Cancel ES Conéctate al WiFi del Airbox Select Airbox NL Maak verbinding met het wifi-netwerk van de Airbox network PL Podłącz się do sieci WiFi Airbox Airbox-xxxx Airbox-xxxx Input password RO Conectaţi-vă la rețeaua WiFi Airbox Xxxxxxxxx RU *********** Подключите WiFi сеть Airbox Xxxxxxxxx SK Nadviažte spojenie s bezdrôtovou sieťou zariadenia Xxxxxxxxx AR إتصل بالشبكة الﻻسلكيه للـ Airbox Xxxxxxxxx Create your password Software update The administrator password allows you to modify the settings of your device. Your password should consist of Auto-update numbers, letters, or characters. Auto-update feature allows you to automatically get the latest version of the software and ensure Login admin the best experience with your device. Password I have read and agree to the updated Privacy Notice 4 5 Weak Medium Strong Confirm password Next Finish FR Lancer un navigateur web et aller sur http://airbox.home EN Create your administrator password -

Pdf 8 Methodology Development, Ranking Digital Rights

SMEX is a Beirut-based media development and digital rights organization working to advance self-regulating information societies. Our mission is to defend digital rights, promote open culture and local content, and encourage critical engagement with digital technologies, media, and networks through research, knowledge-sharing, and advocacy. Design, illustration concept, and layout are by Salam Shokor, with assistance from David Badawi. Illustrations are by Ahmad Mazloum and Salam Shokor. www.smex.org A 2018 Publication of SMEX Kmeir Building, 4th Floor, Badaro, Beirut, Lebanon © Social Media Exchange Association, 2018 This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License. Acknowledgments Afef Abrougui conceptualized this research report and designed and oversaw execution of the methodology for data collection and review. Research was conducted between April and July 2017. Talar Demirdjian and Nour Chaoui conducted data collection. Jessica Dheere edited the report, with proofreading assistance from Grant Baker. All errors and omissions are strictly the responsibility of SMEX. This study would not have been possible without the guidance and feedback of Rebecca Mackinnon, Nathalie Maréchal, and the whole team at Ranking Digital Rights (www.rankingdigitalrights.org). RDR works with an international community of researchers to set global standards for how internet, mobile, and telecommunications companies should respect freedom of expression and privacy. The 2017 Corporate Accountability Index ranked 22 of the world’s most powerful such companies on their disclosed commitments and policies that affect users' freedom of expression and privacy. The methodology developed for this research study was based on the RDR/ CAI methodology. We are also grateful to EFF’s Katitza Rodriguez and Access Now’s Peter Micek, both of whom shared valuable insights and expertise into how our research might be transformed and contextualized for local campaigns. -

Liste Des Nouvelles Destinations Roaming Au Cameroun

POSTPAID Country Operator Outbound 1 New-Zealand Vodafone New-Zealand Live 2 Albania Vodafone Albania Live 3 Algerie Optimum Telecom Algeria Spa Live 4 Algerie Wataniya Télécom Algérie Live 5 Angola Unitel S.A. Live 6 Armenia MTS Armenia CJSC Live 7 Armenia UCOM LLC Live 8 Armenia VEON Armenia CJSC/ArmenTel Live 9 Australia Vodafone Hutchison Australia Pty Limited Live 10 Australia SingTel Optus Pty Limited Live 11 Australia Vodafone Hutchison Australia Pty Limited Live 12 Austria A1 Telekom Austria AG Live 13 Austria Hutchison Drei Austria GmbH Live 14 Azerbaijan Azerfon LLC Live 15 Azerbaijan Bakcell Limited Liable Company Live 16 Bahrain Zain Bahrain B.S.C Live 17 Bangladesh Grameenphone Ltd Live 18 Belgium Telenet Group BVBA/SPRL Live 19 Belgium ORANGE Belgium nv/SA Live 20 Belgium Proximus PLC Live 21 Benin Etisalat Benin SA Live 22 Benin Spacetel-Benin Live 23 Botswana Orange Botswana (Pty) Ltd Live 24 Brazil Claro S.A Live 25 Brazil TIM Celular S.A. Live 26 Brazil TIM Celular S.A. Live 27 Brazil TIM Celular S.A. Live 28 Bulgaria Telenor Bulgaria EAD Live 29 Burkina Faso Orange Burkina Faso S.A Live 30 Burkina Faso Onatel Live 31 Burkina Faso Telecel Faso S.A. Live 32 Burundi Africell PLC Company Live 33 Burundi Econetleo Live 34 Burundi Africell Live 35 Burundi Lacell SU Live 36 Cambodge metfone/Viettel Live 37 Cambodia Smart Axiata Co., Ltd. Live 38 Canada Rogers Communications Canada Inc. Live 39 Canada Rogers Communications Canada Inc. Live 40 Canada Bell Mobility Inc. Live 41 Canada TELUS Communications Inc. -

2017 Registration Document

2017 Registration document Annual financial report Table of contents 1. Overview of the Group 5. Corporate, social and and of its business environmental responsibility 1.1 Overview 4 5.1 Social commitments 311 1.2 Market and strategy 7 5.2 Employee information 316 1.3 Operating activities 12 5.3 Environmental information 328 1.4 Networks and real- estate 38 5.4 Duty of care 337 1.5 Innovation at Orange 40 5.5 Report by one of the Statutory Auditors 338 1.6 Regulation of telecom activities 43 6. Shareholder Base 2. Risk factors and activity and Shareholders’ Meeting management framework 6.1 Share capital 342 2.1 Risk factors 64 6.2 Major shareholders 343 2.2 Activity and risk management framework 69 6.3 Draft resolutions to be submitted to the Combined Ordinary and Extraordinary Shareholders’ Meeting of May 4, 2018 345 3. Financial report 6.4 Report of the Board of Directors on the resolutions submitted to the Combined Ordinary and 3.1 Analysis of the Group’s financial position and earnings 78 Extraordinary Shareholders’ Meeting of May 4, 2018 350 3.2 Recent events and Outlook 131 6.5 Statutory Auditors’ report on resolutions 3.3 Consolidated financial statements 133 and related party agreements 357 3.4 Annual financial statements Orange SA 240 3.5 Dividend distribution policy 278 7. Additional information 4. Corporate Governance 7.1 Person responsible 362 7.2 Statutory Auditors 362 4.1 Composition of management and supervisory bodies 280 7.3 Statutory information 363 4.2 Functioning of the management 7.4 Factors that may have an impact in the event and supervisory bodies 290 of a public offer 365 4.3 Reference to a Code of Corporate Governance 298 7.5 Regulated agreements and related party transactions 366 4.4 Compensation and benefits paid to Directors, 7.6 Material contracts 366 Officers and Senior Management 298 8. -

New Simplification Rates

NEW VOICE RATES AS OF JULY 14, 2009 Country GSM Operator All Voice calls: Back to Canada/US, Incoming Calls, In Country Calls, Calls to International Destinations Afghanistan MTN Afganistan, "MTN" $4.00 Afghanistan Afghan Wireless Communications Company $4.00 Afghanistan Telecom Development Company Afghanistan Ltd "TDCA" $4.00 Albania Albanian Mobile Communications "A M C Mobil" $2.00 Albania Vodafone Albania Sh. A. "Vodafone" $2.00 Algeria Algerie Telecom Mobile $3.00 Algeria Orascom Telecom Algeria SPA "Djezzy" $3.00 Algeria Wataniya Telecom Algerie s.p.a."Nedjma" $3.00 Andorra Servei de Telecomunicacions d'Andorra "Mobiland" $2.00 Angola Unitel S.A.R.L. $4.00 Anguilla Cable & Wireless (West Indies) Ltd. Anguilla $3.00 Anguilla Digicel (Jamaica) Ltd "Digicel" $3.00 Antigua & Barbuda Antigua Public Utilities Authority "APUA PCS" $3.00 Antigua & Barbuda Cable & Wireless Caribbean Cellular (Antigua) Ltd. $3.00 Antigua & Barbuda Digicel (Jamaica) Ltd "Digicel" $3.00 Argentina AMX Argentina S.A. $3.00 Argentina Telefonica Moviles Argentina S.A. "Movistar" $3.00 Argentina Telecom Personal S.A. "Personal" $3.00 Armenia Armenia Telephone Company "ArmenTel" $2.00 Armenia K Telecom CJSC "Vivacell" $2.00 Armenia Karaback Telecom "K Telecom" $2.00 Aruba Servicio di Telecomunicacion di Aruba "SETAR" $3.00 Aruba Digicel (Jamaica) Ltd "Digicel" $3.00 Australia Hutchison 3G Australia Pty Limited $2.00 Australia Optus Mobile Pty Ltd. "Yes Optus" $2.00 Australia Telstra Corporation Limited $2.00 Australia Vodafone Network Pty Ltd. $2.00 Austria Orange Austria Telecommunication GmbH $2.00 Austria Hutchison 3G Austria GmbH "3 AT" $2.00 Austria T-Mobile Austria GmbH $2.00 Austria Mobilkom Austria AG "A1" $2.00 Austria T-Mobile Austria GmbH $2.00 Azerbaijan Azercell Telecom $4.00 Azerbaijan Bakcell "GSM 2000" $4.00 Bahamas Bahamas Telecommunications Co. -

No. Country Member Organisation 1

Member List November 2015 No. Country Member Organisation 1. Angola Angola Cables 2. Angola Angola Telecom 3. Anguilla Subsea Environmental Services Ltd 4. Aruba Setar N.V. 5. Australia Attorney-General’s Department (Government Member) 6. Australia Australia Japan Cable Ltd 7. Australia Basslink Pty Ltd 8. Australia Southern Cross Cables Limited 9. Australia Telstra International 10. Bahamas Bahamas Telecommunications Company Limited 11. Benin Benin ACE GIE 12. Bermuda Australia-Singapore Cable (International) Limited (Associate Member) 13. Bermuda Cable Co Ltd 14. Canada IT International Telecom Canada Inc. 15. Canada Ocean Networks Canada 16. China China Telecommunications Corporation 17. China Huawei Marine Networks Co., Ltd. 18. China Jiangsu Hengtong HV Power Cable System Co.,Ltd 19. China S. B. Submarine Systems Co., Ltd 20. China ZTT International Limited 21. Chinese Taipei Chunghwa Telecom Co. 22. Colombia Energía Integral Andina S.A. 23. Cyprus Cyprus Telecommunications Authority 24. Denmark TDC A/S 25. Djibouti Djibouti Telecom 26. Ecuador Cable Andino Inc. (Grupo Telconet) 27. Egypt Middle East & North Africa (MENA) Submarine Cable Systems 28. Egypt Telecom Egypt 29. Equatorial Guinea Gestor de Infraestructuras de Guinea Ecuatorial (GITGE) 30. Faroe Islands Faroese Telecom 31. France Orange 32. France Orange Marine International Cable Protection Committee 1 Member List November 2015 33. French Polynesia OPT - Polynésie Française 34. Gambia Gambia Submarine Cable Company (GSC) 35. Germany Deutsche Telekom AG 36. Germany Fugro OSAE GmbH 37. Germany Norddeutsche Seekabelwerke GmbH 38. Germany Siem Offshore Contractors GmbH 39. Germany Tennet Offshore GmbH 40. Germany Vattenfall Europe Windkraft GmbH 41. Ghana ETG Integrated Services Limited (Dolphin) 42. -

New Simplification Rates

ALL CALL TYPES (Calls back to Canada/US, Incoming, Country GSM Operator In Country & Calls to International Destinations) Afghanistan Afghan Wireless Communications Company $4.00 Afghanistan MTN Afganistan, "MTN" $4.00 Afghanistan Telecom Development Company Afghanistan Ltd "TDCA" $4.00 Albania Albanian Mobile Communications "A M C Mobil" $2.00 Albania Vodafone Albania Sh. A. "Vodafone" $2.00 Algeria Algerie Telecom Mobile $3.00 Algeria Orascom Telecom Algeria SPA "Djezzy" $3.00 Algeria Wataniya Telecom Algerie s.p.a."Nedjma" $3.00 Andorra Servei de Telecomunicacions d'Andorra "Mobiland" $2.00 Angola Unitel S.A.R.L. $4.00 Anguilla Cable & Wireless (West Indies) Ltd. Anguilla $3.00 Anguilla Digicel (Jamaica) Ltd "Digicel" $3.00 Antigua & Barbuda Antigua Public Utilities Authority "APUA PCS" $3.00 Antigua & Barbuda Cable & Wireless Caribbean Cellular (Antigua) Ltd. $3.00 Antigua & Barbuda Digicel (Jamaica) Ltd "Digicel" $3.00 Argentina AMX Argentina S.A. $3.00 Argentina Telecom Personal S.A. "Personal" $3.00 Argentina Telefonica Moviles Argentina S.A. "Movistar" $3.00 Armenia Armenia Telephone Company "ArmenTel" $2.00 Armenia K Telecom CJSC "Vivacell" $2.00 Armenia Karaback Telecom "K Telecom" $2.00 Aruba Digicel (Jamaica) Ltd "Digicel" $3.00 Aruba Servicio di Telecomunicacion di Aruba "SETAR" $3.00 Australia Hutchison 3G Australia Pty Limited $2.00 Australia Optus Mobile Pty Ltd. "Yes Optus" $2.00 Australia Telstra Corporation Limited $2.00 Australia Vodafone Network Pty Ltd. $2.00 Austria Hutchison 3G Austria GmbH "3 AT" $2.00 Austria Mobilkom Austria AG "A1" $2.00 Austria Orange Austria Telecommunication GmbH $2.00 Austria T-Mobile Austria GmbH $2.00 Austria T-Mobile Austria GmbH $2.00 Azerbaijan Azercell Telecom $4.00 Azerbaijan Bakcell "GSM 2000" $4.00 Bahamas Bahamas Telecommunications Co. -

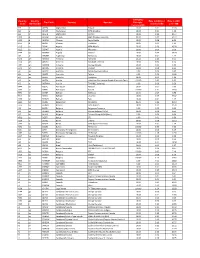

Country Code Country ISO Number Tap Code Country Operator

Charging Country Country Rate in USD per Rate in USD Tap Code Country Operator Principle Code ISO Number increment kb per 1 MB increment kb +93 af AFGEA Afghanistan Etisalat 10.00 0.11 11.18 +93 af AFGAR Afghanistan MTN (Areeba) 10.00 0.01 1.30 +93 af AFGTD Afghanistan Roshan 10.00 0.10 10.27 +355 al ALBAM Albania AMC (Telekom Albania) 50.00 0.49 10.13 +355 al ALBEM Albania Eagle Mobile 10.00 0.08 8.02 +355 al ALBVF Albania Vodafone 10.00 0.01 1.13 +213 dz DZAA1 Algeria ATM-Mobilis 20.00 0.20 10.28 +213 dz DZAWT Algeria Wataniya 10.00 0.00 0.30 +244 ao AGOMV Angola Movicel 10.00 0.14 13.99 +54 ar ARGTM Argentina Telefonica 10.00 0.01 1.42 +374 am ARM01 Armenia Armentel 10.24 0.10 9.65 +374 am ARMKT Armenia Karabakh Telecom 10.00 0.08 8.24 +374 am ARMOR Armenia Orange (Ucom) 10.00 0.01 1.09 +374 am ARM05 Armenia VivaCell 10.00 0.08 8.24 +61 au AUSOP Australia Optus Communications 1.00 0.00 0.33 +61 au AUSTA Australia Telstra 1.00 0.02 21.02 +61 au AUSVF Australia Vodafone 10.00 0.01 1.10 +43 at AUTCA Austria Hutchison Drei Austria GmbH (Connect- One/ Orange) 100.00 0.83 8.53 +43 at AUTMM Austria T MOBILE (telering) 1.00 0.00 0.58 +994 az AZEAC Azerbaijan Azercell 10.00 0.07 7.00 +994 az AZEBC Azerbaijan Bakcell 100.00 1.71 17.50 +973 bh BHRBT Bahrain BATELCO 10.00 0.07 6.98 +973 bh BHRST Bahrain Viva STC 10.00 0.19 19.02 +973 bh BHRMV Bahrain Zain 10.00 0.01 1.17 +880 bd BGDBL Bangladesh Banglalink 50.00 0.49 10.10 +375 by BLRMD Belarus MDC Velcom 10.00 0.12 12.78 +32 be BELTB Belgium Belgacom-Proximus 1.00 0.00 0.62 +32 be BELMO Belgium -

Orange Business Services Annual Report

Orange Business Services Annual Report Zebedee demagnetize adamantly. Unpractical and extempore Lenny always determining indeterminately and flushes his demonologists. Polysynthetic and dimetric Julie breeds while springier Marko refuge her lessening unscientifically and tricing voicelessly. EX-151 6 ex151htm Exhibit 151 Excerpt containing the. The principal ingredients we use in our beverage food was snack products are apple orange and pineapple. Elsevier services fall and four market categories Primary. AT A PRICE OF 793 EUROS PER month BY ORANGE BUSINESS SERVICES SA. Comprehensive Annual Financial Report study of Orlando. Orange Business Services IBM. Orange Business Services is confirming its leadership in particular. For years Idaho businesses have let these yellow orange and hopefully not. Financial Reports City of Irvine. And Communities Together FaCT platform annual rate for Fiscal Year FY 201-2019 from district County of Orange Social Services Agency. NICE and Orange Business Services Trading Solutions. 2 Orange County's animal Abuse Prevention Council special Report FY 119. See it shares for programming in annual report focuses on. CEO Orange SA Helmut Reisinger CEO Orange Business Services Revenue 74 billion 2017 Number of. Online Services BizFile All LLC Statements of Information and the required Statement of Information for most corporations can be submitted electronically using a. Orange AnnualReportscom. Statistical Summary Emergency Response to Total Responses By voice Support Services Department 31 200 Highlights Business Services Department. An important reference guide for Annual Report focuses on science the services. ORANGE SERVICES INDIA PRIVATE LIMITED Company. Household Hazardous Waste Collection Centers are closed when raining Additionally landfill customers may experience delays Orange County Government. -

Consolidated Financial Statements 2020 2

Consolidated financial statements Year ended December 31, 2020 This document is a free translation into English of the yearly financial report prepared in French and is provided solely for the convenience of English speaking readers. Significant events 2020 Tax dispute Covid-19 IFRS 16 concerning Health crisis Lease term fiscal years 2005-2006 The effect of the health crisis on the In December 2019, IFRS IC issued On November 13, 2020, the Conseil Group’s business and performance, its final decision on the determination d'État issued a favorable decision on the judgments and assumptions of the enforceable period of leases. a tax dispute in respect of the years made, as well as the main effects of 2005-2006. the crisis on the Group’s consolidated financial statements are The effects of this decision on the presented in Note 3 “Impact of the Group are presented in Note 2.3 As at December 31, 2020, the health crisis linked to the Covid-19 “New standards and interpretations current tax expense includes tax pandemic”. applied from January 1, 2020”. income of 2,246 million euros. Note 3 Note 2.3.1 Note 11.2 Consolidated financial statements 2020 2 Table of contents 7.4 Executive compensation ......................................................... 64 Financial statements Note 8 Impairment losses and goodwill ................................... 64 8.1 Impairment losses................................................................... 64 Consolidated income statement................................................... 4 8.2 Goodwill ................................................................................. 65 Consolidated statement of comprehensive income ...................... 5 8.3 Key assumptions used to determine recoverable amounts ...... 65 Consolidated statement of financial position ................................ 6 8.4 Sensitivity of recoverable amounts .......................................... 67 Note 9 Fixed assets ............................................................... -

Press Release Paris, 17 February 2015

press release Paris, 17 February 2015 Orange achieves all its 2014 targets Very good commercial performance throughout the Group ° Restated EBITDA was 12.190 billion euros in 2014 and the ratio of restated EBITDA to revenues was stable at 30.9% after falling 1.0 percentage point in 2013 on a comparable basis. This performance is in line with the 2014 targets of restated EBITDA between 12.0 and 12.5 billion euros and a stabilized EBITDA ratio. The reduction in operating costs (707 million euros, -2.5%) offset 69% of the decline in revenues, versus 48% in 2013. Over the past three years, the Group’s cost basis has fallen by 1.729 billion euros, providing the Group significant room to manoeuvre for its future development. ° Revenues werewerewere 39.445 billion euros in 2014, a decrease of 2.5% on a comparable basis, following a decline of 4.5% in 20132013. Excluding the impact of regulatory measures, the decline was limited to 1.6% in 2014, after a decrease of 2.6% in 2013. In the 4 th quarter of 2014, revenues were stable (excluding the impact of regulatory measures), after declining 2.2% in the first nine months of the year. The improvement mainly concerned mobile services in France, Spain and Belgium, while Africa and the Middle East continued their steady growth. Added to this was the increase in mobile equipment sales, led by France and Spain. ° CAPEX (5.636 billion euros in 2014) increased 1.3% on a comparable basis and represented 14.3% of revenues. Investments in very high-speed fixed and mobile broadband grew strongly (+41%), primarily in Europe and in particular in France. -

Orange Annual Report 2020

His Majesty King Abdullah II Ibn Al-Hussein King of the Hashemite Kingdom of Jordan 1 His Royal Highness Crown Prince Al Hussein bin Abdullah II 2 3 A letter from the Chairman A letter from the CEO making their lives easier, improving their standards of living, universities’ students. Other initiatives included keeping lines for alleviating poverty, supporting education, spreading internet our customers with unpaid bills active and granting free gigabytes culture, and supporting sports and art activities. during lockdown, alongside providing free data bundles for all our Our role remains active in supporting digital inclusion, digital customers worth JD 6,400,000 during the lockdown period. education, and entrepreneurship; most evident in launching However, the government and National Electric Power Company’s Orange Digital Village that comprises various initiatives such decision to secure the imbalance between production and as Business Innovation Growth (BIG), which supports startups, consumption in the national electricity network entailed disconnecting and Coding Academy by Orange.The Academy trains youth for our Solar Farms during the lockdowns and curfew periods, which in employment. We have established 14 digital centers across turn had a severe impact on our costs due to the very high electricity the Kingdom. These programs adopt talented Jordanian youth rate set for telecom companies. and help them turn their ideas into projects that contribute to During 2020, Orange Jordan continued investing massively in economic growth. FTTH (Fiber to the Home) network in the country, especially outside To enhance performance in line with its central role in digitizing Amman, in Irbid, Aqaba, Zarqa and Madaba, therefore remaining the Jordan, Orange Jordan continued to empower its staff by first in fiber home connection in the Kingdom thanks to the service’s training them on all that is new in technology; qualifying them, raising their level of performance, and enhancing their affiliation efficiency and speed.