Classical Music Consumer Segmentation Study How Americans Relate to Classical Music and Their Local Orchestras Commissioned by 15 American Orchestras and the John S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In Texas 1 º the First Group of German Settlers to German Settlers of Group First the 1

Heide: Celebrating "Das Deutsche Lied" in Texas Celebrating Texas in “Das Deutsche Lied” Celebrating “Das Deutsche Lied” in º Druck der “Freie Presse fuer Texas” Ad from the 49th Annual Singing Festival of the Texas Hill Country Singers’ League commemorating the Texas Centennial 1836-1936. Courtesy of Beethoven Maennerchor Archives Towards the end of the Republic of Texas and in the early days of statehood, German settlers began arriving at the Ports of Galveston and Indianola. They were coming to Texas largely because of promises made to them for a better political and economic life by the Society for the Protection of German Immigrants in Texas, the Adelsverein. The Adelsverein was an organization formed in 1842 by German noblemen who wanted to create prosperous new settlements in what is now central Texas.1 The first group of German settlers to arrive under the auspices of the Adelsverein was led by Prince Carl of Solms- Braunfels. On March 21, 1845, the Adelsverein established its first community in central Texas and named it “New Braunfels” in honor of the Prince’s estate Produced by The Berkeley Electronic Press, 2003 1 Journal of Texas Music History, Vol. 3 [2003], Iss. 2, Art. 4 Celebrating “Das Deutsche Lied” in Texas in “Das Deutsche Lied” Celebrating Painting of Germania Gesangverein Neu Braunfels,Texas, courtesy of RABA Studio and Beethoven Maennerchor Archives The first year in the new homeland was tenuous. Original plans with a reliable food supply and new homes, the settlers had time made by the Adelsverein for the settlers provisions and welfare to channel their energies into developing these esteemed pastimes. -

Resolution Number 171--2018 Resolution of the Council of the City of Lambertville Adopting an "Affirmative Marketing Plan" for the City of Lambertville

QCttpof ][ambertbHle RESOLUTION NUMBER 171--2018 RESOLUTION OF THE COUNCIL OF THE CITY OF LAMBERTVILLE ADOPTING AN "AFFIRMATIVE MARKETING PLAN" FOR THE CITY OF LAMBERTVILLE WHEREAS, in accordance with applicable Council on Affordable Housing ("COAH") regulations, the New Jersey Uniform Housing Affordability Controls ("UHAC")(N.J.A.C. 5:80- 26., et seq.), and the terms of a Settlement Agreement between the City of Lambertville and Fair Share Housing Center ("FSHC"), which was entered into as part of the City's Declaratory Judgment action entitled In the Matter of the Application f U1 City of Lambertville. C unty of Hunterdon, Docket No. HUN-L-000311-15, which was filed in response to Supreme Court decision In re N.J.A. 5: 6 and 5:97, 221 N.J. 1, 30 (2015) ("Mount Laurel N"), the City of Lambertville is required to adopt an Affirmative Marketing Plan to ensure that all affordable housing units created, including those created by the rehabilitation of rental housing units within the City of Lambertville, are affim1atively marketed to low and moderate income households, particularly those living and/or working within Housing Region 3, the COAH Housing Region encompassing the City of Lambertville. NOW, THEREFORE, BE IT RESOLVED, that the Mayor and Council of the City of Lambertville, County of Hunterdon, State of New Jersey, do hereby adopt the following Affirmative Marketing Plan: Affirmative Mark ting Plan A. All affordable housing units in the City of Lambertville shall be marketed in accordance with the provisions herein. B. The City of Lambertville does not have a Prior Round obligation and a Third Round obligation covering the years from 1999-2025. -

PROGRAM NOTES Witold Lutosławski Concerto for Orchestra

PROGRAM NOTES by Phillip Huscher Witold Lutosławski Born January 25, 1913, Warsaw, Poland. Died February 7, 1994, Warsaw, Poland. Concerto for Orchestra Lutosławski began this work in 1950 and completed it in 1954. The first performance was given on November 26, 1954, in Warsaw. The score calls for three flutes and two piccolos, three oboes and english horn, three clarinets and bass clarinet, three bassoons and contrabassoon, four horns, four trumpets, four trombones and tuba, timpani, snare drum, side drums, tenor drum, bass drum, cymbals, tam-tam, tambourine, xylophone, bells, celesta, two harps, piano, and strings. Performance time is approximately twenty-eight minutes. The Chicago Symphony Orchestra's first subscription concert performances of Lutosławski's Concerto for Orchestra were given at Orchestra Hall on February 6, 7, and 8, 1964, with Paul Kletzki conducting. Our most recent subscription concert performance was given November 7, 8, and 9, 2002, with Christoph von Dohnányi conducting. The Orchestra has performed this concerto at the Ravinia Festival only once, on June 28, 1970, with Seiji Ozawa conducting. For the record The Orchestra recorded Lutosławski's Concerto for Orchestra in 1970 under Seiji Ozawa for Angel, and in 1992 under Daniel Barenboim for Erato. To most musicians today, as to Witold Lutosławski in 1954, the title “concerto for orchestra” suggests Béla Bartók's landmark 1943 score of that name. Bartók's is the most celebrated, but it's neither the first nor the last work with this title. Paul Hindemith, Walter Piston, and Zoltán Kodály all wrote concertos for orchestra before Bartók, and Witold Lutosławski, Michael Tippett, Elliott Carter, and Shulamit Ran are among those who have done so after his famous example. -

Arkansas Symphony Rockefeller and Quapaw String Quartets Present "The Art of the String Quartet" at Clinton Presidential Center

PRESS RELEASE: FOR IMMEDIATE RELEASE Press Contact: Brandon Dorris Office: (501)666-1761, ext. 118 Mobile: (501)650-2260 Fax: (501)666-3193 Email: [email protected] Arkansas Symphony Rockefeller and Quapaw String Quartets Present "The Art of the String Quartet" at Clinton Presidential Center Little Rock, ARK, Feb. 7, 2019 - The Arkansas Symphony Orchestra, Philip Mann, Music Director and Conductor, presents the fourth concert of the 2018-2019 River Rhapsodies Chamber Music season with The Art of the String Quartet, Tuesday, Feb. 26th at 7:00 p.m. at the Clinton Presidential Center. ASO's resident string quartets, Rockefeller String Quartet and Quapaw String Quartet, will perform Janáček's "Kreutzer Sonata," Mozart's String Quartet No. 12, along with Puccini and Verdi's string quartets. Arkansas Symphony Orchestra's Quapaw String Quartet was founded in 1980 as the ASO resident string quartet. Responding to what was clearly a statewide need, the ASO and Winthrop Rockefeller Foundation began a partnership in 2000 to form the Rockefeller String Quartet. The quartets have developed a reputation for providing quality school programming, as well as performing statewide as a chamber ensemble and with the Arkansas Symphony. The quartets’ primary responsibilities include string education and outreach throughout the state reaching more than 26,000 Arkansas school children each year. River Rhapsodies Chamber Music Concerts are held in the intimate setting of the Clinton Presidential Center's Great Hall. A cash bar is open before the concert and at intermission, and patrons are invited to carry drinks into the concert. The Media Sponsor for the River Rhapsodies Chamber Music Series is UA Little Rock Public Radio. -

Concerts in the Park Concerts in the Park String Quartet String Quartet

HARTMAN FOUNDATION HARTMAN FOUNDATION CONCERTS IN THE PARK CONCERTS IN THE PARK STRING QUARTET STRING QUARTET Sunday, July 18, 2021, 7:30 p.m. Sunday, July 18, 2021, 7:30 p.m. H-E-B Terrace at the Long Center for the Performing Arts H-E-B Terrace at the Long Center for the Performing Arts Karen Stiles, violin Karen Stiles, violin Richard Kilmer, violin Richard Kilmer, violin Blake Turner, viola Blake Turner, viola Muriel Sanders, cello Muriel Sanders, cello PROGRAM PROGRAM FRANZ JOSEPH HAYDN String Quartet No. 5 in D Major, Op. 64, The Lark FRANZ JOSEPH HAYDN String Quartet No. 5 in D Major, Op. 64, The Lark I. Allegro moderato I. Allegro moderato II. Adagio cantabile II. Adagio cantabile III. Menuetto (Allegretto) III. Menuetto (Allegretto) IV. Finale (Vivace) IV. Finale (Vivace) LUDWIG VAN BEETHOVEN Allegro ma non tanto from String Quartet No. 4 LUDWIG VAN BEETHOVEN Allegro ma non tanto from String Quartet No. 4 in C Minor, Op. 18 in C Minor, Op. 18 FRANZ JOSEPH HAYDN Presto (Scherzando) from String Quartet No. 4 FRANZ JOSEPH HAYDN Presto (Scherzando) from String Quartet No. 4 in D Major, Op. 20 in D Major, Op. 20 VARIOUS A selection of pop music VARIOUS A selection of pop music Visit austinsymphony.org/events for upcoming events. Visit austinsymphony.org/events for upcoming events. ———————————————— ———————————————— The Austin Symphony Orchestra wishes to thank The Hartman Family Foundation The Austin Symphony Orchestra wishes to thank The Hartman Family Foundation for making the Concerts in the Park possible. for making the Concerts in the Park possible. -

INAUGURAL GALA and CONCERT Honorary Chairs: Joan and Irwin Jacobs Co-Chairs: Una Davis and Jack Mcgrory, Karen and Kit Sickels, Kathy Taylor and Terry Atkinson

LETIT’S THETIME MUSIC TO CELEBRATE BEGIN PLEASE JOIN US ON FRIDAY, AUGUST 6TH AT 5PM THE RADY SHELL AT JACOBS PARK™ INAUGURAL GALA AND CONCERT Honorary Chairs: Joan and Irwin Jacobs Co-Chairs: Una Davis and Jack McGrory, Karen and Kit Sickels, Kathy Taylor and Terry Atkinson PURCHASE TICKETS THE EVENING Please join us at the San Diego Symphony Inaugural Gala and Concert, a once-in-a-lifetime celebration, at The Rady Shell at Jacobs Park™. Be among the very first guests to come together at this iconic new bayside performance venue and San Diego landmark. Be front and center as Rafael Payare and the musicians of the San Diego Symphony, as well as special world-renowned guest artists, all take the stage for a breathtaking concert experience. Support the Symphony's artistic, learning and community engagement programs by attending this spectacular evening, which kicks off an electrifying new era for the San Diego Symphony – and all of us. SCHEDULE COCKTAIL RECEPTION 5:00 pm – 6:00 pm Guests begin the evening at a beautiful cocktail reception bayside. DINNER 6:00 pm – 7:30 pm Celebrity Chef Richard Blais will curate a delectable dinner exclusively crafted for Gala attendees. CONCERT 7:30 pm – 10:00 pm The evening will culminate with a breathtaking concert, followed by a spectacular display of light and sound. TICKET LEVELS & BENEFITS DIAMOND LEVEL PLATINUM LEVEL GOLD LEVEL SILVER LEVEL TABLE OF 4 | $40,000 TABLE OF 4 | $25,000 TABLE OF 4 | $20,000 TABLE OF 4 | $10,000 INDIVIDUAL TICKETS | INDIVIDUAL TICKETS | INDIVIDUAL TICKETS | INDIVIDUAL -

EAST AMWELL TOWNSHIP FEBRUARY 11, 2021 the Regular

EAST AMWELL TOWNSHIP FEBRUARY 11, 2021 The regular meeting of the East Amwell Township Committee was called to order at 7:30 p.m. Present were Mayor Richard Wolfe, Deputy Mayor Mark Castellano, and Committee members Chris Sobieski, Tara Ramsey and John Mills. In compliance with the Open Public Meetings Act, Acting Clerk Krista Parsons announced that this is a regularly scheduled meeting, pursuant to the resolution adopted on January 4, 2021 with a meeting notice published in the Hunterdon County Democrat issue of January 14, 2021. A copy of the agenda for this meeting was forwarded to the Hunterdon County Democrat, Times of Trenton, Star Ledger, Courier News, posted on the Township website, and filed in the Township Clerk’s Office on February 8, 2021. ****************************************************************************** RESOLUTION #34-21 WHEREAS, the Open Public Meetings Act, P.L. 1975, Chapter 231 permits the exclusion of the public from a meeting in certain circumstances; and WHEREAS, East Amwell Township Committee is of the opinion that circumstances presently exist; and WHEREAS, the governing body of the Township of East Amwell wishes to discuss litigation; and WHEREAS, minutes will be kept and once the matter involving the confidentiality of the above no longer requires that confidentiality, then minutes can be made public; and NOW, THEREFORE, BE IT RESOLVED, that the public be excluded from this meeting. I, Krista M. Parsons, Acting Municipal Clerk, hereby certify that the foregoing resolution is a true and accurate copy of a resolution adopted by the Township Committee of East Amwell at a regular and duly convened meeting held on February 11, 2021. -

Ludwig Van Beethoven a Brilliant Pianist, but When Born: December 16, 1770 He Was Around 30 Years Old Died: March 26, 1827 Beethoven Began Going Deaf

SymphonySecond No. Movement 8 in F Major Ludwig van Beethoven a brilliant pianist, but when Born: December 16, 1770 he was around 30 years old Died: March 26, 1827 Beethoven began going deaf. Even though he could no Ludwig van Beethoven was longer hear well enough to born in Bonn, Germany. His play the piano, Beethoven father, who was a singer, composed some of his best was his first teacher. After a music after he lost his while, even though he was hearing! still only a boy, Ludwig became a traveling Beethoven is considered performer, and soon he was one of the greatest musical supporting his family. geniuses who ever lived. He may be most famous for his In his early twenties nine symphonies, but he also Beethoven moved to Vienna, wrote many other kinds of where he spent the rest of music: chamber and choral his life. Beethoven was one pieces, piano works, string of the first composers to quartets, and an opera. make a living without being employed by the church or a member of the nobility. At first, he was known as Beethoven’s Music Listen to the second movement of Beethoven’s 8th Symphony, then answer the questions below. 1. How many “ticks” do you hear before the melody begins? a. 2 b. 5 c. 7 d. 8 2. What instrument plays the melody first? a. violin b. viola c. cello d. bass 3. Does the orchestra get loud suddenly? a. yes b. no 4. Does the music sound like it’s jumping around the orchestra? a. -

Kick-Off Summary Report

KICK-OFF EVENT SUMMARY REPORT SUBMITTED TO: City of San Antonio Transportation & Capital Improvements Department SUBMITTED BY: Parsons Brinckerhoff SUBMITTED ON: May 18, 2015 City of San Antonio Department of Transportation and Capital Improvements 114 West Commerce St. | San Antonio, TX 78283-3966 | 210-207-8987 | SATomorrow.com INTRODUCTION ...................................................................................................... 2 OUTREACH .............................................................................................................. 3 E-Blast ..................................................................................................................... 3 Advertisements ....................................................................................................... 3 Social Media............................................................................................................ 4 Media Relations ...................................................................................................... 8 Flyer Distribution ..................................................................................................... 8 Attendance .............................................................................................................. 9 OPEN HOUSE SUMMARY ...................................................................................... 10 SA Tomorrow Station ............................................................................................ 10 The Comprehensive Plan .................................................................................... -

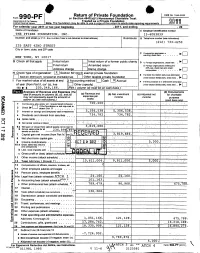

Return of Private Foundation CT' 10 201Z '

Return of Private Foundation OMB No 1545-0052 Form 990 -PF or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirem M11 For calendar year 20 11 or tax year beainnina . 2011. and ending . 20 Name of foundation A Employer Identification number THE PFIZER FOUNDATION, INC. 13-6083839 Number and street (or P 0 box number If mail is not delivered to street address ) Room/suite B Telephone number (see instructions) (212) 733-4250 235 EAST 42ND STREET City or town, state, and ZIP code q C If exemption application is ► pending, check here • • • • • . NEW YORK, NY 10017 G Check all that apply Initial return Initial return of a former public charity D q 1 . Foreign organizations , check here . ► Final return Amended return 2. Foreign organizations meeting the 85% test, check here and attach Address chang e Name change computation . 10. H Check type of organization' X Section 501( exempt private foundation E If private foundation status was terminated Section 4947 ( a)( 1 ) nonexem pt charitable trust Other taxable p rivate foundation q 19 under section 507(b )( 1)(A) , check here . ► Fair market value of all assets at end J Accounting method Cash X Accrual F If the foundation is in a60-month termination of year (from Part Il, col (c), line Other ( specify ) ---- -- ------ ---------- under section 507(b)(1)(B),check here , q 205, 8, 166. 16) ► $ 04 (Part 1, column (d) must be on cash basis) Analysis of Revenue and Expenses (The (d) Disbursements total of amounts in columns (b), (c), and (d) (a) Revenue and (b) Net investment (c) Adjusted net for charitable may not necessanly equal the amounts in expenses per income income Y books purposes C^7 column (a) (see instructions) .) (cash basis only) I Contribution s odt s, grants etc. -

President's Newsletter

President’s Message Volume 4, Issue 2—April 2011 Greetings friends, alumni, faculty, staff and students. “A Point of Pride in the Community” Temperatures in San Antonio cooled off in February and March, but President’s Newsletter not the excitement and activity at St. Philip’s College. While students and faculty were settling SPC celebrates 113th in for a new semester of scholastic pursuit, anniversary the context around them was alive with St. Philip’s College celebrated the 113th energy. anniversary of its founding on Tuesday, March February brought a vibrant Black History 1 with a reception at the college’s Center for Month observance. One of our first fine Health Professions atrium. arts graduates, John Coleman, exhibited his critically acclaimed work at the Morgan More than 100 attendees witnessed the Gallery. recognition of corporate partner AT&T, which donated an original art work collection March was a celebration of 113 years valued at nearly $100,000 to the college. The of providing educational access. It was AT&T Vice President for External Affairs observed in fine fashion, with a reception 25-piece collection is displayed at the college’s Michelle Thomas and Lisa Soto admire the thanking AT&T for its donation of a three newest buildings—the Welcome Center, anniversary cake at the 113th anniversary valuable art collection to the college. The the Center for Health Professions and the celebration with Chef Cynthia de la Fuente. event was also a showcase for our fine arts Center for Learning Resources. talent. Ivy Taylor, Alamo Colleges Trustee James Among the community leaders and educators Rindfuss and Chancellor Bruce Leslie, Pastor On March 4, we held our 3rd annual present were Michelle Thomas and Larry Tony Regist from St. -

Music Tech-1

Radnor Middle School Course Overview Music Technology I. Course Description Music Technology is offered as an eighth grade music elective, meeting three times a cycle. Students will be introduced to the study of music technology and music fundamentals. Areas of instruction will include instrument and equipment care, beginning level music literacy (reading and writing music), keyboard performance skills, music technology related history, concepts, terminology and experience with a variety of applications. II. Resources, Materials , Equipment • iMacs • GarageBand • Korg K61p MIDI Studio Contoller Keyboards • Student Journals III. Course Goals, Objectives (Essential Questions, Enduring Understandings) Students will be able to: 1. Accurately perform melody, harmony and rhythm parts of a composition and record the parts separately into the sequencer of the keyboard. 2. Accurately perform melody, harmony and rhythm parts of their own composition and record the parts separately into the sequencer of the keyboard. 3. Record multiple parts to an electronic “sound piece” using non-traditional instrument timbres and effects. 4. Orchestrate and perform three- and four-part synthesizer ensemble pieces within expected performance parameters for their individual levels of expertise. 5. Transfer sequenced MIDI files from the keyboard disk into the computer and, using appropriate software, edit needed corrections, format, and print out the composition. 6. Change instrumentation using an existing music composition stored as MIDI data; and alter tempo, range, and dynamics during the course of the piece, while still maintaining the original integrity of the composition. 7. Compose a four-part electronic sound piece using varied timbre (tone), texture, and dynamics of at least three minute length. Students may incorporate digitally recorded audio sounds into this piece.