Ppbs and the Choice of Policy Alternatives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Rhetoric of Trade and the Pragmatism of Policy: Canadian and New Zealand Commercial Relations with Britain, 1920-1950 Francine Mckenzie [email protected]

Western University Scholarship@Western History Publications History Department 2010 The Rhetoric of Trade and the Pragmatism of Policy: Canadian and New Zealand Commercial Relations with Britain, 1920-1950 Francine McKenzie [email protected] Follow this and additional works at: https://ir.lib.uwo.ca/historypub Part of the History Commons Citation of this paper: McKenzie, Francine, "The Rhetoric of Trade and the Pragmatism of Policy: Canadian and New Zealand Commercial Relations with Britain, 1920-1950" (2010). History Publications. 390. https://ir.lib.uwo.ca/historypub/390 THE RHETORIC OF TRADE AND THE PRAGMATISM OF POLICY: CANADIAN AND NEW ZEALAND COMMERCIAL RELATIONS WITH BRITAIN, 1920-1950 Francine McKenzie Department of History The University of Western Ontario INTRODUCTION In April 1948 Prime Minister Mackenzie King pulled Canada out of secret free trade negotiations with the United States. Although many officials in the Department of External Affairs believed that a continental free trade agreement was in Canada’s best interests, King confided to his diary that he could not let the negotiations go forward because a successful outcome would destroy the British Empire and Commonwealth: ‘I am sure in so doing, I have made one of the most important decisions for Canada, for the British Commonwealth of Nations that has been made at any time.’1 In October 1949, while being fêted in London, Prime Minister Sydney Holland of New Zealand, made one of his characteristic spontaneous and ill considered statements. He declared, ‘I want the people of Britain to know that we will send all the food that they need, even if we have to send it free’.2 These two stories tell historians a lot. -

A Post-Mercantilist Trade and Productivity Agenda for Canada

Institut C.D. HOWE Institute commentary NO. 357 Breaking Free: A Post-mercantilist Trade and Productivity Agenda for Canada Canada’s declining trade performance has been matched by an equally anemic productivity performance. To revitalize both, Canadians will have to be prepared to address remaining barriers to greater global engagement. Michael Hart The Institute’s Commitment to Quality About The C.D. Howe Institute publications undergo rigorous external review Author by academics and independent experts drawn from the public and private sectors. Michael Hart holds the Simon Reisman The Institute’s peer review process ensures the quality, integrity and Chair in Trade Policy at objectivity of its policy research. The Institute will not publish any the Norman Paterson School study that, in its view, fails to meet the standards of the review process. of International Affairs, The Institute requires that its authors publicly disclose any actual or Carleton University, potential conflicts of interest of which they are aware. and a Research Fellow, C. D. Howe Institute. In its mission to educate and foster debate on essential public policy issues, the C.D. Howe Institute provides nonpartisan policy advice to interested parties on a non-exclusive basis. The Institute will not endorse any political party, elected official, candidate for elected office, or interest group. As a registered Canadian charity, the C.D. Howe Institute as a matter of course accepts donations from individuals, private and public organizations, charitable foundations and others, by way of general and project support. The Institute will not accept any donation that stipulates a predetermined result or policy stance or otherwise inhibits its independence, or that of its staff and authors, in pursuing scholarly activities or disseminating research results. -

January/February 2020 Tevet/Shevat/Adar 5780

Temple Israel the BULLETIN January/February 2020 Tevet/Shevat/Adar 5780 TU B’SHEVAT Monday, February 10, 2020 The “birthday of the trees” is a time for seders, tree-planting and more. Worship Schedule Holiday Dates Times SHABBAT Friday, January 3 6:15 pm Kabbalat Shabbat Service Saturday, January 4 10:15 am Shabbat Service, Parsha Vayigash SHABBAT Thursday, January 9 7:30 am Morning Minyan Friday, January 10 6:15 pm Kabbalat Shabbat Service 7:00 pm Bring your own dinner Saturday, January 11 10:15 am Shabbat Service, Parsha Vayechi Services led by TIRS Grade 7, Musical Guest Daniel Geigerman SHABBAT Friday, January 17 6:15 pm Kabbalat Shabbat Service Saturday, January 18 10:15 am Shabbat Service, Parsha Shemot Thursday, January 23 7:30 am Morning Minyan SHABBAT Friday, January 24 5:30 pm TOTally Shabbat 6:30 pm Kabbalat Shabbat Service Saturday, January 25 10:15 am Shabbat Service, Parsha Va’era SHABBAT Friday, January 31 6:15 pm Kabbalat Shabbat Service Saturday, February 1 10:15 am Shabbat Service, Parsha Bo SHABBAT Friday, February 7 6:15 pm Kabbalat Shabbat Service Saturday, February 8 10:15 am Shabbat Service, Parsha Beshalach Musical Guest Daniel Geigerman & Temple Liturgical Choir Thursday, February 13 7:30 am Morning Minyan SHABBAT Friday, February 14 6:15 pm Kabbalat Shabbat Service 7:00 pm Bring your own dinner Saturday, February 15 10:15 am Shabbat Service, Parsha Yitro SHABBAT Friday, February 21 6:15 pm Kabbalat Shabbat Service Saturday, February 22 10:15 am Shabbat Service, Parsha Mishpatim Shabbat Shekalim Thursday, February -

Eulogy for William Krehm 2 SNC-Lavalin and the Rule of Law Canada’S SNC-Lavalin Affair: by Jonathan Krehm Capital

THE JOURNAL OF THE COMMITTEE ON MONETARY AND ECONOMIC REFORM $3.95 Vol. 31, No. 1 • JANUARY–FEBRUARY 2019 CONTENTS Eulogy for William Krehm 2 SNC-Lavalin and the Rule of Law Canada’s SNC-Lavalin Affair: By Jonathan Krehm Capital. Unfortunately, as a teenager with The Site C Dam Project and My father passed away peacefully at my head on fire – these were the opening Bulk Water Export home on Friday, April 19, at 11 pm, in his years of the Depression – I could not avoid Canada’s Corrupt Foreign Policy 106th year. He had an amazing full life. We polemicizing against Winston Churchill on Come Home to Roost were blessed that he enjoyed relatively good my exam paper on history. Obviously this The Real SNC-Lavalin Issues health until the end. and the diverted time His generation is did not help my chanc- Why Wilson-Raybould Was Right now gone. His pass- es for a scholarship, Sordid SNC-Lavalin Affair ing marks the end of which in fact I didn’t Exposes Canada as a Plutocracy, an era. Not just for us get. So I spent two Not a Democracy here gathered, but also years in a mathemat- Neoliberal Fascism and the Echoes for those who remem- ics and physics courses of History, Part II ber the struggles of the without money to buy A General Comment about the past. He was the last books. It did nothing Inquiry living North American for my chances of be- A Comment about Paradigm Shift who went to Spain to coming a physicist or 19 BC Leads the Way to a Better support the Spanish Re- a mathematician. -

Backgrounder No

C.D. Howe Institute Backgrounder www.cdhowe.org No. 90, April 2005 Great Wine, Better Cheese How Canada Can Escape the Trap of Agricultural Supply Management Michael Hart The Backgrounder in Brief Canada's current supply management system for dairy and poul- try farmers, who account for about 0.6 percent of the country's gross domestic product, is unfair to consumers, other farmers and food processors. There are ways to dismantle the process, and precedents from Canada’s wine and Australia’s dairy sectors to guide policymakers who must undertake the task. About the Author Michael Hart, a former federal trade official, holds the Simon Reisman Chair in Trade Policy at the Norman Paterson School of International Affairs at Carleton University. He is spending the 2004/2005 academic year in Washington as a Fulbright Fellow at American University and the Woodrow Wilson International Center for Scholars. The C.D. Howe Institute The C.D. Howe Institute is a national, nonpartisan, nonprofit organization that aims to improve Canadians’ standard of living by fostering sound economic and social policy. The Institute promotes the application of independent research and analysis to major economic and social issues affecting the quality of life of Canadians in all regions of the country. It takes a global perspective by considering the impact of international factors on Canada and bringing insights from other jurisdictions to the discussion of Canadian public policy. Policy recommendations in the Institute’s publications are founded on quality research conducted by leading experts and subject to rigorous peer review. The Institute communicates clearly the analysis and recommendations arising from its work to the general public, the media, academia, experts, and policymakers. -

Canada: Still Open for Business?

CANADA: STILL OPEN FOR BUSINESS? Report of the Standing Senate Committee on Banking, Trade and Commerce The Honourable Senator Doug Black, Q.C., Chair The Honourable Senator Carolyn Stewart Olsen, Deputy Chair 1 OCTOBER 2018 For more information please contact us: by email: [email protected] by mail: The Standing Senate Committee on Banking, Trade and Commerce Senate, Ottawa, Ontario, Canada, K1A 0A4 This report can be downloaded at: www.senate-senat.ca/ The Senate is on Twitter: @SenateCA, follow the committee using the hashtag #BANC Ce rapport est également offert en français 2 The Standing Senate Committee on Banking, Trade and Commerce TABLE OF CONTENTS COMMITTEE MEMBERSHIP ........................................................................................ 4 ORDER OF REFERENCE ............................................................................................ 5 LIST OF RECOMMENDATIONS ................................................................................... 6 INTRODUCTION ...................................................................................................... 7 FIXING CANADA’S TAX SYSTEM ................................................................................ 9 A. Royal Commission on Taxation .................................................................... 10 B. Immediate Measures to Improve Canada’s Tax Competitiveness ...................... 11 CREATING REGULATORY CERTAINTY FOR INVESTORS ............................................... 14 REMOVING BARRIERS TO SUCCESS FOR CANADIAN -

The Free Trade Roller Coaster BOOK EXCERPT PASSAGES

BOOK EXCERPT PASSAGES The free trade roller coaster Brian Mulroney In this exclusive excerpt from his book, Memoirs, the former prime minister recounts the tense month of negotiations and stalemated talks with the United States before the dramatic agreement at the 11th hour of the last day — October 3, 1987. Dans ce passage exclusif de ses Mémoires, l’ancien premier ministre décrit les tensions d’un mois complet de négociations et l’impasse dans laquelle se trouvaient les discussions avec les États-Unis avant la conclusion de l’entente survenue in extremis le 3 octobre 1987, une heure avant l’échéance finale. ith the close of the believe goes to the heart of the negoti- series of special committee and Francophonie Summit I ations, it would be prudent to know A full cabinet sessions in early W had to face the alarming soon so that we may take appropriate September had revealed clearly to us fact that the end point for a successful action. (I would note here that the all that the negotiations were at a conclusion to the free trade talks was prime minister will meet all ten standstill, in large part over Canada’s only a month away, with a deadline of Canadian premiers to review these demand for relief from arbitrary October 3, at midnight. US negotiator negotiations on September 14.)” American trade remedy decisions. Peter Murphy still hadn’t revealed any- Howard Baker replied three days Equally, our negotiators had refused to thing worth Canada’s while in regard later, saying that the administration budge on the bottom-line concern of to our key demand: a binding dispute wouldn’t admit the talks could fail. -

Uofcpress Nationalinterest 201

University of Calgary PRISM: University of Calgary's Digital Repository University of Calgary Press University of Calgary Press Open Access Books 2011 In the National Interest: Canadian Foreign Policy and the Department of Foreign Affairs and International Trade, 1909–2009 University of Calgary Press Donaghy, G., & Carroll, M. (Eds.). (2011). In the National Interest: Canadian Foreign Policy and the Department of Foreign Affairs and International Trade, 1909-2009. Calgary, Alberta, Canada: University of Calgary Press. http://hdl.handle.net/1880/48549 book http://creativecommons.org/licenses/by-nc-nd/3.0/ Attribution Non-Commercial No Derivatives 3.0 Unported Downloaded from PRISM: https://prism.ucalgary.ca University of Calgary Press www.uofcpress.com IN THE NATIONAL INTEREST Canadian Foreign Policy and the Department of Foreign Affairs and International Trade, 1909–2009 Greg Donaghy and Michael K. Carroll, Editors ISBN 978-1-55238-561-6 THIS BOOK IS AN OPEN ACCESS E-BOOK. It is an electronic version of a book that can be purchased in physical form through any bookseller or on-line retailer, or from our distributors. Please support this open access publication by requesting that your university purchase a print copy of this book, or by purchasing a copy yourself. If you have any questions, please contact us at [email protected] Cover Art: The artwork on the cover of this book is not open access and falls under traditional copyright provisions; it cannot be reproduced in any way without written permission of the artists and their agents. The cover can be displayed as a complete cover image for the purposes of publicizing this work, but the artwork cannot be extracted from the context of the cover of this specific work without breaching the artist’s copyright. -

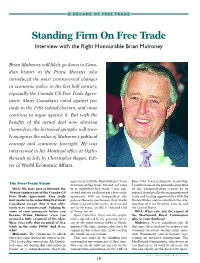

Standing Firm on Free Trade Interview with the Right Honourable Brian Mulroney

A DECADE OF FREE TRADE Standing Firm On Free Trade Interview with the Right Honourable Brian Mulroney Brian Mulroney will likely go down in Cana- dian history as the Prime Minister who introduced the most controversial changes in economic policy in the last half century, especially the Canada-US Free Trade Agree- ment. Many Canadians voted against free trade in the 1988 federal election, and some continue to argue against it. But with the benefits of the actual deal now showing themselves, the historical epitaphs will sure- ly recognise the value of Mulroney’s political courage and economic foresight. He was interviewed in his Montreal office at Ogilvy Renault in July by Christopher Ragan, Edi- tor of World Economic Affairs. agreement with the United States. I was June 1983. I was seeking the leadership. The Free-Trade Vision in favour of free trade, but not, as I refer I said that one of the principle objectives WEA: We have just celebrated the to it, unfettered free trade. I was con- of my administration would be to 10-year anniversary of the Canada-US cerned that we could not get a free-trade expand dramatically the management of Free Trade Agreement. Free trade agreement with an independent dis- trade and trading opportunities with the now seems to be something that most pute-settlement mechanism that would United States and to refurbish the rela- Canadians accept. But it was obvi- allow us to even the scales. As it turned tionship of trust between Canada and ously very controversial. Judging by out in the event, we did. -

The Framework and Process of Canada-United States Trade Liberalization

Canada-United States Law Journal Volume 10 Issue Article 36 January 1988 The Framework and Process of Canada-United States Trade Liberalization Frank Stone Follow this and additional works at: https://scholarlycommons.law.case.edu/cuslj Part of the Transnational Law Commons Recommended Citation Frank Stone, The Framework and Process of Canada-United States Trade Liberalization, 10 Can.-U.S. L.J. 245 (1985) Available at: https://scholarlycommons.law.case.edu/cuslj/vol10/iss/36 This Article is brought to you for free and open access by the Student Journals at Case Western Reserve University School of Law Scholarly Commons. It has been accepted for inclusion in Canada-United States Law Journal by an authorized administrator of Case Western Reserve University School of Law Scholarly Commons. The Framework and Process of Canada-United States Trade Liberalization** by Frank Stone * I. INTRODUCTION The Declaration on Trade made by Prime Minister Mulroney and Presi- dent Reagan at their meeting in Quebec City on March 17-18, 1985, could lead to developments of historic importance in Canada-United States trade relations. The two leaders agreed on the objective of reduc- ing and removing tariff and other barriers to cross-border trade, and called for a report within six months "on all possible ways" to achieve this objective. They also committed themselves to halt protectionism in cross-border trade in goods and services. They announced the resolution of a number of existing irritants in bilateral trade, or action aimed at resolving them. And, -

Water and Social Activism in Canada

Water and Social Activism in Canada by Kelly Busch B.A. University of Victoria, 1992 A thesis Submitted in Partial Fulfillment of the Requirements for the Degree of MASTER OF ARTS in Interdisciplinary Studies We accept this thesis as conforming to the required standard Dr. Rennie Warburton, Supervisor (Department of Sociology) Dr. Peter Stephenson, Committee Member (Department of Anthropology) Dr. Ken Hatt, Committee Member (Department of Sociology) Dr. Honore France, Committee Member (Faculty of Education) Dr. Pamela Moss, External Examiner (Faculty of Human and Social Development) © Kelly Busch UNIVERSITY OF VICTORIA All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. ii ABSTRACT: This thesis on water and social activism in Canada is a journey into the realm of shared social understanding. Water is too precious to all forms of life to simply permit commodification for the benefit of a few at the expense of the many. The Sun Belt case adjudicated under the North American Free Trade Agreement (NAFTA) when compared with what prevailed under previous Canadian national law reveals severe limits to state sovereignty. A high measure of support has already been manifest around concerns and considerations which pertain to water and the potential for the growth of social activism with reference to water may well be unprecedented in Canada. There are fundamental inequalities found within the Sun Belt case. Current international trade policy coupled with private banking practices does not value the principles of sustainability, equality and justice because it is committed to the commodification of the “commons”. -

Canadian Federalism and International Trade Agreements: Evaluating Three Policy Options for Mitigating Federal-Provincial Conflict

CANADIAN FEDERALISM AND INTERNATIONAL TRADE AGREEMENTS: EVALUATING THREE POLICY OPTIONS FOR MITIGATING FEDERAL-PROVINCIAL CONFLICT by Jennifer Keefe Bachelor ofArts, Simon Fraser University, 2005 THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS In the Department ofPolitical Science © Jennifer Keefe 2008 SIMON FRASER UNIVERSITY Spring 2008 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission ofthe author. APPROVAL Name: Jennifer Keefe Degree: Master ofArts, Department ofPolitical Science Title ofThesis: Canadian Federalism and International Trade Agreements: Evaluating Three Policy Options for Mitigating Federal-Provincial Conflict Examining Committee: Chair: Dr. Lynda Erickson, Professor Department of Political Science, Simon Fraser University Dr. Stephen McBride, Professor Senior Supervisor Department ofPolitical Science, Simon Fraser University Dr. Daniel Cohn, Assistant Professor Supervisor School of Public Policy and Administration, and The Department of Political Science, York University Dr. Karl Froschauer, Associate Professor External Examiner Department of Sociology, Simon Fraser University Date Defended/Approved: 11 SIMON FRASER UNIVERSITY LIBRARY Declaration of Partial Copyright Licence The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial