Interim Results Announcement for the Six Months Ended 30 June 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Congressional-Executive Commission on China Annual

CONGRESSIONAL-EXECUTIVE COMMISSION ON CHINA ANNUAL REPORT 2016 ONE HUNDRED FOURTEENTH CONGRESS SECOND SESSION OCTOBER 6, 2016 Printed for the use of the Congressional-Executive Commission on China ( Available via the World Wide Web: http://www.cecc.gov U.S. GOVERNMENT PUBLISHING OFFICE 21–471 PDF WASHINGTON : 2016 For sale by the Superintendent of Documents, U.S. Government Publishing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Mar 15 2010 19:58 Oct 05, 2016 Jkt 000000 PO 00000 Frm 00003 Fmt 5011 Sfmt 5011 U:\DOCS\AR16 NEW\21471.TXT DEIDRE CONGRESSIONAL-EXECUTIVE COMMISSION ON CHINA LEGISLATIVE BRANCH COMMISSIONERS House Senate CHRISTOPHER H. SMITH, New Jersey, MARCO RUBIO, Florida, Cochairman Chairman JAMES LANKFORD, Oklahoma ROBERT PITTENGER, North Carolina TOM COTTON, Arkansas TRENT FRANKS, Arizona STEVE DAINES, Montana RANDY HULTGREN, Illinois BEN SASSE, Nebraska DIANE BLACK, Tennessee DIANNE FEINSTEIN, California TIMOTHY J. WALZ, Minnesota JEFF MERKLEY, Oregon MARCY KAPTUR, Ohio GARY PETERS, Michigan MICHAEL M. HONDA, California TED LIEU, California EXECUTIVE BRANCH COMMISSIONERS CHRISTOPHER P. LU, Department of Labor SARAH SEWALL, Department of State DANIEL R. RUSSEL, Department of State TOM MALINOWSKI, Department of State PAUL B. PROTIC, Staff Director ELYSE B. ANDERSON, Deputy Staff Director (II) VerDate Mar 15 2010 19:58 Oct 05, 2016 Jkt 000000 PO 00000 Frm 00004 Fmt 0486 Sfmt 0486 U:\DOCS\AR16 NEW\21471.TXT DEIDRE C O N T E N T S Page I. Executive Summary ............................................................................................. 1 Introduction ...................................................................................................... 1 Overview ............................................................................................................ 5 Recommendations to Congress and the Administration .............................. -

Introduction

Notes Introduction 1. Hobsbawm 1990, 66. 2. Diamond 1998, 322–33. 3. Fairbank 1992, 44–45. 4. Fei Xiaotong 1989, 1–2. 5. Diamond 1998, 323, original emphasis. 6. Crossley 1999; Di Cosmo 1998; Purdue 2005a; Lavely and Wong 1998, 717. 7. Richards 2003, 112–47; Lattimore 1937; Pan Chia-lin and Taeuber 1952. 8. My usage of the term “geo-body” follows Thongchai 1994. 9. B. Anderson 1991, 86. 10. Purdue 2001, 304. 11. Dreyer 2006, 279–80; Fei Xiaotong 1981, 23–25. 12. Jiang Ping 1994, 16. 13. Morris-Suzuki 1998, 4; Duara 2003; Handler 1988, 6–9. 14. Duara 1995; Duara 2003. 15. Turner 1962, 3. 16. Adelman and Aron 1999, 816. 17. M. Anderson 1996, 4, Anderson’s italics. 18. Fitzgerald 1996a: 136. 19. Ibid., 107. 20. Tsu Jing 2005. 21. R. Wong 2006, 95. 22. Chatterjee (1986) was the first to theorize colonial nationalism as a “derivative discourse” of Western Orientalism. 23. Gladney 1994, 92–95; Harrell 1995a; Schein 2000. 24. Fei Xiaotong 1989, 1. 25. Cohen 1991, 114–25; Schwarcz 1986; Tu Wei-ming 1994. 26. Harrison 2000, 240–43, 83–85; Harrison 2001. 27. Harrison 2000, 83–85; Cohen 1991, 126. 186 • Notes 28. Duara 2003, 9–40. 29. See, for example, Lattimore 1940 and 1962; Forbes 1986; Goldstein 1989; Benson 1990; Lipman 1998; Millward 1998; Purdue 2005a; Mitter 2000; Atwood 2002; Tighe 2005; Reardon-Anderson 2005; Giersch 2006; Crossley, Siu, and Sutton 2006; Gladney 1991, 1994, and 1996; Harrell 1995a and 2001; Brown 1996 and 2004; Cheung Siu-woo 1995 and 2003; Schein 2000; Kulp 2000; Bulag 2002 and 2006; Rossabi 2004. -

Marriage Practice of the Chinese Communist Party in Modern Era, 1910S-1950S

Western University Scholarship@Western Electronic Thesis and Dissertation Repository 8-23-2011 12:00 AM From Marriage Revolution to Revolutionary Marriage: Marriage Practice of the Chinese Communist Party in Modern Era, 1910s-1950s Wei Xu The University of Western Ontario Supervisor James Flath The University of Western Ontario Graduate Program in History A thesis submitted in partial fulfillment of the equirr ements for the degree in Doctor of Philosophy © Wei Xu 2011 Follow this and additional works at: https://ir.lib.uwo.ca/etd Part of the Asian History Commons, Chinese Studies Commons, Cultural History Commons, Family, Life Course, and Society Commons, Gender and Sexuality Commons, History of Gender Commons, Inequality and Stratification Commons, Social Control, Law, Crime, and Deviance Commons, Social History Commons, Women's History Commons, and the Women's Studies Commons Recommended Citation Xu, Wei, "From Marriage Revolution to Revolutionary Marriage: Marriage Practice of the Chinese Communist Party in Modern Era, 1910s-1950s" (2011). Electronic Thesis and Dissertation Repository. 232. https://ir.lib.uwo.ca/etd/232 This Dissertation/Thesis is brought to you for free and open access by Scholarship@Western. It has been accepted for inclusion in Electronic Thesis and Dissertation Repository by an authorized administrator of Scholarship@Western. For more information, please contact [email protected]. FROM MARRIAGE REVOLUTION TO REVOLUTIONARY MARRIAGE: MARRIAGE PRACTICE OF THE CHINESE COMMUNIST PARTY IN MODERN ERA 1910s-1950s (Spine -

Building a Modern Energy System Improving the Quality of Life 創建現代能源體系 ENN Energy Holdings Limited 新奧能源控股有限公司 提高人民生活品質 (Stock Code 股份代號: 2688)

Building a Modern Energy System Improving the Quality of Life 創建現代能源體系 ENN Energy Holdings Limited 新奧能源控股有限公司 提高人民生活品質 (Stock code 股份代號: 2688) INTERIM REPORT 2018 二零一八年中期業績報告 CONTENTS 02 Financial and Operational Highlights 03 Management Discussion and Analysis 15 Corporate Governance and Other Information 23 Report on Review of Condensed Consolidated Financial Statements 24 Condensed Consolidated Statement of Profit or Loss and Other Comprehensive Income 25 Condensed Consolidated Statement of Financial Position 27 Condensed Consolidated Statement of Changes in Equity 29 Condensed Consolidated Statement of Cash Flows 30 Notes to the Condensed Consolidated Financial Statements 02 FINANCIAL AND OPERATIONAL HIGHLIGHTS The major results and operational data of the Group for the period together with the comparative figures for the corresponding period last year are as follows: Six months ended 30 June Increased/ 2018 2017 (Decreased) by (Unaudited) (Unaudited) Results Revenue (RMB million) 26,530 21,424 23.8% Gross profit (RMB million) 4,662 3,873 20.4% Profit attributable to owners of the Company (RMB million) 1,782 1,649 8.1% Earnings per share – Basic (RMB) 1.64 1.52 7.9% Operational data# Number of city-gas projects in China 178 165 13 Urban population coverage (thousand) 88,609 78,090 13.5% Residential households coverage (thousand) 29,536 26,030 13.5% New natural gas customers developed during the period: – residential households (thousand) 1,078 951 13.4% – C/I customers (sites) 10,764 9,650 1,114 – installed designed daily capacity -

Copyright by James Joshua Hudson 2015

Copyright by James Joshua Hudson 2015 The Dissertation Committee for James Joshua Hudson Certifies that this is the approved version of the following dissertation: River Sands/Urban Spaces: Changsha in Modern Chinese History Committee: Huaiyin Li, Supervisor Mark Metzler Mary Neuburger David Sena William Hurst River Sands/Urban Spaces: Changsha in Modern Chinese History by James Joshua Hudson, B.A.; M.A. Dissertation Presented to the Faculty of the Graduate School of The University of Texas at Austin in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy The University of Texas at Austin May 2015 Dedication For my good friend Hou Xiaohua River Sands/Urban Spaces: Changsha in Modern Chinese History James Joshua Hudson, PhD. The University of Texas at Austin, 2015 Supervisor: Huaiyin Li This work is a modern history of Changsha, the capital city of Hunan province, from the late nineteenth to mid twentieth centuries. The story begins by discussing a battle that occurred in the city during the Taiping Rebellion (1850-1864), a civil war that erupted in China during the mid nineteenth century. The events of this battle, but especially its memorialization in local temples in the years following the rebellion, established a local identity of resistance to Christianity and western imperialism. By the 1890’s this culture of resistance contributed to a series of riots that erupted in south China, related to the distribution of anti-Christian tracts and placards from publishing houses in Changsha. During these years a local gentry named Ye Dehui (1864-1927) emerged as a prominent businessman, grain merchant, and community leader. -

Heritage and Romantic Consumption in China Consumption Romantic in and Heritage

ASIAN HERITAGES Zhu Heritage and in Romantic Consumption China Yujie Zhu Heritage and Romantic Consumption in China Heritage and Romantic Consumption in China Publications The International Institute for Asian Studies (IIAS) is a research and exchange platform based in Leiden, the Netherlands. Its objective is to encourage the interdisciplinary and comparative study of Asia and to promote (inter)national cooperation. IIAS focuses on the humanities and social sciences and on their interaction with other sciences. It stimulates scholarship on Asia and is instrumental in forging research networks among Asia Scholars. Its main research interests are reflected in the three book series published with Amsterdam University Press: Global Asia, Asian Heritages and Asian Cities. IIAS acts as an international mediator, bringing together various parties in Asia and other parts of the world. The Institute works as a clearinghouse of knowledge and information. This entails activities such as providing information services, the construction and support of international networks and cooperative projects, and the organization of seminars and conferences. In this way, IIAS functions as a window on Europe for non-European scholars and contributes to the cultural rapprochement between Europe and Asia. IIAS Publications Officer: Paul van der Velde IIAS Assistant Publications Officer: Mary Lynn van Dijk Asian Heritages The Asian Heritages series explores the notions of heritage as they have evolved from European based concepts, mainly associated with architecture and monumental archaeology, to incorporate a broader diversity of cultural forms and value. This includes a critical exploration of the politics of heritage and its categories, such as the contested distinction ‘tangible’ and ‘intangible’ heritages; the analysis of the conflicts triggered by competing agendas and interests in the heritage field; and the productive assessment of management measures in the context of Asia. -

Characteristic Towns Attracting Tourism, Greater Development Hunan Highlights Heritage, Cherished Cultural Differences of Its Ethnic Groups

12 | Wednesday, August 26, 2020 HONG KONG EDITION | CHINA DAILY Characteristic towns attracting tourism, greater development Hunan highlights heritage, cherished cultural differences of its ethnic groups Located in Zixing, a countylevel city under Hunan’s Chenzhou city, Huangcao town is a nationally famous tourist destination with impressive landscape. PHOTOS PROVIDED TO CHINA DAILY Fascinating places offer multitude of historical sites and experiences Miaoertan town Huaihua city, and has won the honorary titles mote its high-quality development, Luyuan of Hunan’s beautiful town, Hunan’s ecologi- town welcomed 1.37 million tourists last year, cal town and Hunan’s characteristic cultural achieving tourism revenue worth 756 million tourism town. Beidouxi town is working on yuan. promoting its homestay travel, study travel and special agricultural products. In 2019, Huangcao town Beidouxi town received 300,000 tourists, with tourism revenue reaching 60 million yuan. It is estimated that in three years, the town will welcome 1 million visitors and achieve a total tourism revenue of 200 mil- lion yuan. The Hunan province launches 10 new characteristic cultural Located in Longshan county, Xiangxi Tujia tourism towns for 2020, on July 15 in Changsha. and Miao autonomous prefecture, Miaoertan Hongjiaguan Bai town is notable for its traditional Tujia culture ethnic group township and diverse intangible cultural heritage, includ- By ZHANG DANDAN percent year-on-year, according to ing the Tujia dialect folk song, Tujia traditional [email protected] the local government. dance and Tujia brocade. In 2019, the town Located in Zixing, a county-level city under Furong town in Yongshun coun- received 450,000 tourists, achieving a tourism Chenzhou city, Huangcao town is a national The Hunan Provincial Depart- ty, Xiangxi Tujia and Miao autono- revenue worth 90 million yuan ($13 million). -

Annual Report 2016

CONGRESSIONAL-EXECUTIVE COMMISSION ON CHINA ANNUAL REPORT 2016 ONE HUNDRED FOURTEENTH CONGRESS SECOND SESSION OCTOBER 6, 2016 Printed for the use of the Congressional-Executive Commission on China ( Available via the World Wide Web: http://www.cecc.gov VerDate Mar 15 2010 10:00 Oct 06, 2016 Jkt 000000 PO 00000 Frm 00001 Fmt 6011 Sfmt 5011 U:\DOCS\AR16 NEW\21471.TXT DEIDRE 2016 ANNUAL REPORT VerDate Mar 15 2010 10:00 Oct 06, 2016 Jkt 000000 PO 00000 Frm 00002 Fmt 6019 Sfmt 6019 U:\DOCS\AR16 NEW\21471.TXT DEIDRE CONGRESSIONAL-EXECUTIVE COMMISSION ON CHINA ANNUAL REPORT 2016 ONE HUNDRED FOURTEENTH CONGRESS SECOND SESSION OCTOBER 6, 2016 Printed for the use of the Congressional-Executive Commission on China ( Available via the World Wide Web: http://www.cecc.gov U.S. GOVERNMENT PUBLISHING OFFICE 21–471 PDF WASHINGTON : 2016 For sale by the Superintendent of Documents, U.S. Government Publishing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Mar 15 2010 10:00 Oct 06, 2016 Jkt 000000 PO 00000 Frm 00003 Fmt 5011 Sfmt 5011 U:\DOCS\AR16 NEW\21471.TXT DEIDRE CONGRESSIONAL-EXECUTIVE COMMISSION ON CHINA LEGISLATIVE BRANCH COMMISSIONERS House Senate CHRISTOPHER H. SMITH, New Jersey, MARCO RUBIO, Florida, Cochairman Chairman JAMES LANKFORD, Oklahoma ROBERT PITTENGER, North Carolina TOM COTTON, Arkansas TRENT FRANKS, Arizona STEVE DAINES, Montana RANDY HULTGREN, Illinois BEN SASSE, Nebraska DIANE BLACK, Tennessee DIANNE FEINSTEIN, California TIMOTHY J. WALZ, Minnesota JEFF MERKLEY, Oregon MARCY KAPTUR, Ohio GARY PETERS, Michigan MICHAEL M. -

Resettlement Action Plan

RP-11 VOL.-2 Public Disclosure Authorized Hubei--Hunan Expressway Corridor Project Hunan Section (National Highway IV) Public Disclosure Authorized Resettiement Action Plan (thi Fifth Edition) I ;- Lfl 9.0 Public Disclosure Authorized C,7 Resettlement Office of HYmii:nPr3-vincia! T'tcheng--Ci 1,-s'sha Expressway lIunan Academy of'SocialSc;ience Public Disclosure Authorized December, 1998 I I Hubei--Hunan Expressway Corridor Project Hunan Section (National Highway IV) Resettlement Action Plan (the Fifth Edition) ResettlementOffice of HunanProvincial Tucheng--Changsha Expressway HunanAcademy of SocialScience December,1998 A 4 STAFF AND UNITS Heads: Zhao Dezhi Hunan Academy of Social Science Professor Ma Qiwei Hunan Provincial Expressway Construction & DevelopmentCo. SeniorEngineer Chiefs: Shi Yongming Hunan Academy of Social Science AssociatedProfessor Wang Yi Hunan Academy of Social Science AssociatedProfessor Wang Yong Xi Hunan Academy of Social Science AssociatedProfessor Tang Shengde Hunan ProvincialExpressway Construction & DevelopmentCo. Senior Engineer Lv Xingxi Hunan ProvincialExpressway Construction& Development Co. Senior Engineer Wang Xifan Hunan Provincial Expressway Construction & DevelopmentCo. Engineer Yi Meixun Hunan Provincial Expressway Construction & Development Co. Engineer Wang Jia Hunan Provincial Expressway Construction & DevelopmentCo. Assistant Economist Wen Xianghong Hunan Provincial Expressway Construction & DevelopmentCo. Assistant Accountant Associated Units: Hunan Provincial CommunicationsSurvey & Design Institute -

A Sheffield Hallam University Thesis

Tourists’ Responses to Government Intentions for Red Tourism In China WAN, Xiang Available from the Sheffield Hallam University Research Archive (SHURA) at: http://shura.shu.ac.uk/17301/ A Sheffield Hallam University thesis This thesis is protected by copyright which belongs to the author. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the author. When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given. Please visit http://shura.shu.ac.uk/17301/ and http://shura.shu.ac.uk/information.html for further details about copyright and re-use permissions. Tourists’ Responses to Government Intentions for Red Tourism In China Xiang Wan A thesis submitted in partial fulfilment of the requirements of Sheffield Hallam University For the degree of Doctor of Philosophy February 2017 1 Abstract This study analyses the Chinese government’s involvement in Red Tourism, with a special focus on the government’s political intentions in conveying messages at Red Tourism sites, and, critically, how tourists respond to the messages presented there. There are two separate identifiable phases in the development of Red Tourism since 2004. The first phase is from 2004 to 2010 and the second one is from 2011 to 2015. Shaoshan, the birthplace of Mao Zedong, and Zhijiang, which is dedicated to commemorating the surrender of the Japanese Imperial Army, are selected to examine the government’s political intentions behind the messages presented at these two Red Tourism sites. The former is the best example from the first phase, while the latter is one of the most important in the second phase. -

Information to Users

INFORMATION TO USERS This manuscript has been reproduced from the microfilm master. UMI films the text directly from the original or copy submitted. Thus, some thesis and dissertation copies are in typewriter face, while others may be from any type of computer printer. The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indistinct print, colored or poor quality illustrations and photographs, print bleedthrough, substandard margins, and improper alignment can adversely affect reproduction. In the unlikely event that the author did not send UMI a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion. Oversize materials (e.g., maps, drawings, charts) are reproduced by sectioning the original, beginning at the upper left-hand comer and continuing from left to right in equal sections with small overlaps. Photographs included in the original manuscript have been reproduced xerographically in this copy. Higher quality 6” x 9" black and white photographic prints are available for any photographs or illustrations appearing in this copy for an additional charge. Contact UMI directly to order. ProQuest Information and Learning 300 North Zeeb Road, Ann Arbor, Ml 48106-1346 USA 800-521-0600 UMÏ RED GENESIS: THE HUNAN FIRST NORMAL SCHOOL AND THE CREATION OF CHINESE COMÜNISM, 1903-1921 DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Liyan Liu, B.A., M.A. ***** The Ohio State University 2001 Dissertation Committee: Approved by Professor James R. -

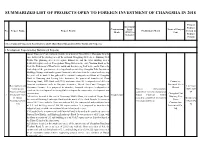

Summarized List of Projects Open to Foreign Investment of Changsha in 2018

SUMMARIZED LIST OF PROJECTS OPEN TO FOREIGN INVESTMENT OF CHANGSHA IN 2018 Project Investment Contact Cooperation Funds Name of Project No. Project Name Project Profile Preliminary Work Person & Mode (RMB Ten Unit Thousand ) Contact Person I. Development Projects in Key Districts and Urban-Rural Integration Pilot Towns (22 Projects) 1. Development Projects in Key Districts (18 Projects) Hunan Financial Center is located at the west bank of Xiang River, Changsha. It is the core district of the starting area of the national Xiangjiang New Area - Binjiang New Town. The planning area is 2.8 square kilometers, and the total building area is 6,800,000 square meters. It neighbors Xiang River in the east, Yinshan Road in the west, the Fisherman’s Wharf in the south and Beijincheng Park in the north. Under the leadership of the government, developed and operated by Changsha Pilot Investment Holdings Group, a national regional financial center based on the central and covering the west will be built. It has gathered the national headquarters of Bank of Changsha, Bank of Sanxiang and Jixiang Life Insurance, the provincial branches of China Minsheng Bank, SPD Bank and CGB, and more than 20 headquarters of different Commerce financial institutions such as Kaiyuan Securities, Orient Asset and Changyin 58 Bureau of Yuelu Development and Lin Yuan Consumer Finance. It is proposed to introduce financial enterprise headquarters to District Construction Project infrastructure 152111247 reside in for development or strengthful developers for cooperative development and Project of Hunan completed; Concept planning of 09 construction. Changsha Pilot 1 Financial Center Cooperation / Hunan Financial Center A4 block is located at the east of Xiaoxiang Middle Road, the south of Guyue Road, Binjiang New in Hunan basically completed; investment Wang Lang the west of Binjiang Landscape Road and the north of the Sixth Branch.