Sovereign Wealth Funds and Innovation Investing in an Era of Mounting Uncertainty

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Limits and Contradictions of Labour Investment Funds

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by R-libre Managing Workers’ Capital? Limits and Contradictions of Labour Investment Funds Ian Thomas MacDonald is Assistant Professor in the School of Industrial Relations at Université de Montréal. His research interests include labour organizing strategies, labour politics and radical political economy. His work has appeared in Labor Studies Journal, Socialist Register, and the British Journal of Industrial Relations. He is the editor of Unions and the City: Negotiating Urban Change (Cornell ILR Press, 2017). Mathieu Dupuis: is Assistant professor in labor relations, TÉLUQ Montréal – University of Québec. He is conducting research on trade unions, comparative employment relations, multinational corporations, and the manufacturing sector. Recent publication: 2018. “Crafting alternatives to corporate restructuring: Politics, institutions and union power in France and Canada” European Journal of Industrial Relations, 24(1): 39-54. Abstract: Labour-controlled investment is often touted as an alternative, pro-worker form of finance. Since 1983, the province of Québec in Canada has experimented with workers participation in the form of workers funds controlled by the two major trade union federations. Drawing on research from secondary sources, archival material and semi-structured interviews, this paper offers a comprehensive portrait of one of Québec main workers’ funds, the FTQ Solidarity Fund. To date very little has been said about the impact of workers funds on firm governance, employment quality and labour relations. We argue that any attempt to use investment to shape firm behaviour in the interests of workers and local unions is a limited and contradictory project. -

Financing Growth in Innovative Firms: Consultation

Financing growth in innovative frms: consultation August 2017 Financing growth in innovative frms: consultation August 2017 © Crown copyright 2017 This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: [email protected]. Where we have identifed any third party copyright information you will need to obtain permission from the copyright holders concerned. This publication is available at www.gov.uk/government/publications Any enquiries regarding this publication should be sent to us at [email protected] ISBN 978-1-912225-08-8 PU2095 Contents Page Foreword 3 Executive summary 5 Chapter 1 Introduction 7 Chapter 2 The patient capital gap 9 Chapter 3 Strengths and weaknesses in patient capital 17 Chapter 4 Root causes (1): deployment of / demand for patient capital 29 Chapter 5 Root causes (2): supply of capital 35 Chapter 6 Current interventions 43 Chapter 7 Implications for policy 51 Annex A List of consultation questions 61 Annex B Terms of reference for the review 63 Annex C Terms of reference for and members of the Industry Panel 65 Annex D Data sources 69 1 Foreword Productivity is important. As I set out in my speech at the Mansion House earlier this summer, improvements in productivity ultimately drive higher wages and living standards. This makes it much more than just another metric of economic performance. -

Impact Bonds in Developing Countries

IMPACT BONDS IN DEVELOPING COUNTRIES: Early Learnings from the Field 2 | IMPACT BONDS IN DEVELOPING COUNTRIES IMPACT BONDS IN DEVELOPING COUNTRIES: Early Learnings from the Field SEPTEMBER 2017 Emily Gustafsson-Wright is a fellow at the Center for Universal Education at Brookings Izzy Boggild-Jones is a research analyst at the Center for Universal Education at Brookings Dean Segell is a manager at Convergence Justice Durland is a knowledge associate at Convergence ACKNOWLEDGEMENTS The authors would like to thank Brookings gratefully acknowledges many people for their contributions the program support provided to the to this study. First, Alison Bukhari, Center for Universal Education by the Toby Eccles, Safeena Husain, Jane Government of Norway. Newman, Peter Vanderwal and Maya Ziswiler for their helpful comments, Brookings recognizes that feedback and insight on earlier drafts the value it provides is in its of the report. In addition, we would absolute commitment to quality, like to thank all those who supported independence, and impact. Activities with data collection for the Deal Book, and provided real time updates on the supported by its donors reflect this factsheets for each deal. We would commitment. also like to acknowledge those who participated in the impact bonds workshop in London in November 2016, whose valuable insights have Convergence is an institution that formed the core of this report. We connects, educates, and supports are particularly grateful for the investors to execute blended finance contributions of stakeholders involved transactions that increase private in the contracted impact bonds with sector investment in emerging whom we have had more in-depth markets. -

Structured Finance

Financial Institutions U.S.A. Investcorp Bank B.S.C. Full Rating Report Ratings Key Rating Drivers Investcorp Bank B.S.C. Strong Gulf Franchise: The ratings of Investcorp B.S.C. (Investcorp, or the company) reflect Long-Term IDR BB Short-Term IDR B the company’s strong client franchise in the Gulf, established track record in private equity (PE) Viability Rating bb and commercial real estate investment, strong capital levels and solid funding profile. Rating constraints include sizable balance sheet co-investments and potential earnings volatility and Investcorp S.A. Investcorp Capital Ltd. placement risks presented by the business model, which could pressure interest coverage. Long-Term IDR BB Short-Term IDR B Gulf Institutional Owners Positive: The Positive Rating Outlook reflects franchise and Senior Unsecured Debt BB earnings benefits that may accrue to Investcorp from the 20% strategic equity stake sale to Support Rating Floor NF Mubadala Development Co. (Mubadala) in March 2017, a sovereign wealth fund of Abu Dhabi. This follows a 9.99% equity stake sale to another Gulf-based institution in 2015. Fitch Ratings Rating Outlook Positive views these transactions favorably, as the relationships may give Investcorp expanded access to potential new investors as well as a more stable equity base. 3i Business Diversifies AUM: The cash-funded acquisition of 3i Debt Management (3iDM) in March 2017 added $10.8 billion in AUM and is expected to be accretive for Investcorp, adding Financial Data stable management fee income. However, the acquired co-investment assets and ongoing risk Investcorp Bank B.S.C. retention requirements do increase Investcorp’s balance sheet risk exposure. -

Dear Fellow Shareholders

Dear Fellow Shareholders: At Evercore, we aspire to be the most respected independent investment banking advi- sory firm globally. Our overarching objective is to help a growing base of clients achieve superior results through trusted independent and innovative advice, provided by excep- tional professionals who bring to our clients diverse perspectives and experiences. Our clients include multinational corporations, financial sponsors, institutional investors, sov- ereign wealth funds, and wealthy individuals and family offices. Achieving this objective requires that we steadily build our team by recruiting the best, from those beginning their professional careers to veterans with decades of experience. We are deliberate in selecting and developing the members of our team, seeking to attract individuals who share our Core Values: Client Focus, Integrity, Excellence, Respect, Investment in People and Partnership. Our values are the defining elements of our culture, telling our clients and current and future generations of partners and employees what they can expect from our firm. Realizing our aspiration also requires that we deliver attractive financial results over time. Strong financial results create the opportunity to invest and grow, enabling us to serve more clients and enhance the range of services we offer. The environment for our business was generally favorable in 2017, providing both good opportunities and a few challenges: • Advisory Services: Demand for strategic corporate and capital markets advisory services remains strong. The appeal of purely independent, unconflicted advice continues to grow and the opportunities and challenges facing our clients are broad, as economic conditions, globalization, technology and regulation drive strategic change. We believe that we are well positioned here. -

Accelerating Energy Access

ACUMEN 2018 ACCELERATING ENERGY ACCESS: THE ROLE OF PATIENT CAPITAL ACUMEN WOULD LIKE TO ACKNOWLEDGE OUR PARTNERS THAT GENEROUSLY SUPPORT THE PIONEER ENERGY INVESTMENT INITIATIVE STEVE ROSS & THE BERNARD & ANNE SPITZER SHELLEY SCHERER CHARITABLE TRUST GLOBAL OFFICES SPECIAL THANKS ACCRA, GHANA Special thanks to our peer reviewers Saad Ahmad, David Aitken, Magdalena Banasiak, Morgan DeFoort, Fabio De Pascale, BOGOTÁ, COLOMBIA Christine Eibs-Singer, Peter George, Steven Hunt, Neha Juneja, KARACHI, PAKISTAN Jill Macari, Damian Miller, Jesse Moore, Willem Nolens, Steve Ross, LONDON, ENGLAND Peter Scott, Ajaita Shah, Manoj Sinha, Ned Tozun, Nico Tyabji, MUMBAI, INDIA Hugh Whalan, and David Woolnough NAIROBI, KENYA Special thanks to Carlyle Singer for her strategic guidance and NEW YORK, U.S.A. Harsha Mishra for his analytical research. Additional thanks SAN FRANCISCO, U.S.A. to the Acumen team: Sasha Dichter, Kat Harrison, Kate Montgomery, Jacqueline Novogratz, Sachindra Rudra, and Yasmina Zaidman Lead Authors: Leslie Labruto and Esha Mufti Table of Contents FOREWORD 02 EXECUTIVE SUMMARY 04 INTRODUCTION 06 1. ENERGY SNAPSHOT: 08 ACUMEN’S TRACK RECORD FOR INVESTING IN ENERGY ACCESS 2. THE PIONEER GAP: 12 HOW HAS THE INFLUX OF CAPITAL AFFECTED ENTREPRENEURS? 3. NEED FOR CAPITAL: 16 FILLING GAPS IN OFF-GRID ENERGY MARKETS TODAY 4. THE BIG PICTURE: 26 WHAT IS THE OPTIMAL MIX FOR SCALING ENERGY ACCESS COMPANIES? 5. REACHING THE POOR: 38 USING PATIENT CAPITAL TO ACCELERATE IMPACT 6. BEYOND CAPITAL: 46 WHAT DO ENERGY ACCESS STARTUPS NEED? 7. FACILITATING EXITS: 48 SENDING THE RIGHT MARKET SIGNALS 8. CONCLUSION: 56 WORKING TOGETHER TO CATALYZE ENERGY ACCESS APPENDIX 58 CASEFOREWORD STUDY Jacqueline Novogratz FOUNDER & CEO Dear Reader, I am pleased to share Acumen’s Accelerating Energy Access: The Role of Patient Capital report with you. -

Sovereign Wealth Funds As Sustainability Instruments? Disclosure of Sustainability Criteria in Worldwide Comparison

sustainability Article Sovereign Wealth Funds as Sustainability Instruments? Disclosure of Sustainability Criteria in Worldwide Comparison Stefan Wurster * and Steffen Johannes Schlosser TUM School of Governance, Technical University Munich, 80333 Munich, Germany * Correspondence: [email protected] Abstract: Sovereign wealth funds (SWFs) are state-owned investment vehicles intended to pursue national objectives. Their nature as long-term investors combined with their political mandate could make SWFs an instrument suited to promote sustainability. As an essential precondition, it is important for SWFs to commit to sustainability criteria as part of an overarching strategy. In the article, we present the sustainability disclosure index (SDI), an original new dataset for a selection of over 50 SWFs to investigate whether SWFs disclose sustainability criteria covering environmental, social, economic, and governance aspects into their mandate. In addition to an empirical measurement of the disclosure rate, we conduct multiple regressions to analyze what factors help to explain the variance between SWFs. We see that a majority of SWFs disclose at least some of the sustainability criteria. However, until today, only a small minority address a broad selection as a possible basis for a comprehensive sustainability strategy. While a high-state capacity and a young population in a country as well as a commitment to the international Santiago Principles are positively associated with a higher disclosure rate, we find no evidence for strong effects of the economic development level, the resource abundance, and the degree of democratization of a country or of the specific size and structure of a fund. Identifying favorable conditions for a higher commitment of SWFs could Citation: Wurster, S.; Schlosser, S.J. -

Sovereign Wealth Funds": Regulatory Issues, Financial Stability and Prudential Supervision

EUROPEAN ECONOMY Economic Papers 378| April 2009 The so-called "Sovereign Wealth Funds": regulatory issues, financial stability and prudential supervision Simone Mezzacapo EUROPEAN COMMISSION Economic Papers are written by the Staff of the Directorate-General for Economic and Financial Affairs, or by experts working in association with them. The Papers are intended to increase awareness of the technical work being done by staff and to seek comments and suggestions for further analysis. The views expressed are the author’s alone and do not necessarily correspond to those of the European Commission. Comments and enquiries should be addressed to: European Commission Directorate-General for Economic and Financial Affairs Publications B-1049 Brussels Belgium E-mail: [email protected] This paper exists in English only and can be downloaded from the website http://ec.europa.eu/economy_finance/publications A great deal of additional information is available on the Internet. It can be accessed through the Europa server (http://europa.eu ) KC-AI-09-378-EN-N ISSN 1725-3187 ISBN 978-92-79-11189-1 DOI 10.2765/36156 © European Communities, 2009 THE SO-CALLED "SOVEREIGN WEALTH FUNDS": REGULATORY ISSUES, FINANCIAL STABILITY, AND PRUDENTIAL SUPERVISION By Simone Mezzacapo* University of Perugia Abstract This paper aims to contribute to the debate on the regulatory and economic issues raised by the recent gain in prominence of the so-called “Sovereign Wealth Funds” (SWFs), by first trying to better identify the actual legal and economic nature of such “special purpose” government investment vehicles. SWFs are generally deemed to bring significant benefits to global capital markets. -

Alternative Perspectives on Challenges and Opportunities of Financing Development

FINANCING FOR DEVELOPMENT Alternative Perspectives on Challenges and Opportunities of Financing Development ORGANISATION OF ISLAMIC COOPERATION STATISTICAL, ECONOMIC AND SOCIAL RESEARCH AND TRAINING CENTRE FOR ISLAMIC COUNTRIES Financing for Development Alternative Perspectives on Challenges and Opportunities of Financing Development Editors: Kenan Bağcı and Erhan Türbedar ORGANIZATION OF ISLAMIC COOPERATION THE STATISTICAL, ECONOMIC AND SOCIAL RESEARCH AND TRAINING CENTRE FOR ISLAMIC COUNTRIES (SESRIC) © May 2019 | Statistical, Economic and Social Research and Training Centre for Islamic Countries (SESRIC) Editors: Kenan Bağcı and Erhan Türbedar Kudüs Cad. No: 9, Diplomatik Site, 06450 Oran, Ankara –Turkey Telephone +90–312–468 6172 Internet www.sesric.org E-mail [email protected] The material presented in this publication is copyrighted. The authors give the permission to view, copy, download, and print the material presented provided that these materials are not going to be reused, on whatsoever condition, for commercial purposes. For permission to reproduce or reprint any part of this publication, please send a request with complete information to the Publication Department of SESRIC. All queries on rights and licenses should be addressed to the Publication Department, SESRIC, at the aforementioned address. The responsibility for the content, the views, interpretations and conditions expressed herein rests solely with the authors and can in no way be taken to reflect the views of the SESRIC or its Member States, partners, or of the OIC. The boundaries, colours and other information shown on any map in this work do not imply any judgment on the part of the SESRIC concerning the legal status of any territory or the endorsement of such boundaries. -

Sovereign Wealth Funds 2019 Managing Continuity, Embracing Change

SOVEREIGN WEALTH FUNDS 2019 MANAGING CONTINUITY, EMBRACING CHANGE SOVEREIGN WEALTH FUNDS 2019 Editor: Javier Capapé, PhD Director, Sovereign Wealth Research, IE Center for the Governance of Change Adjunct Professor, IE University 6 SOVEREIGN WEALTH FUNDS 2019. PREFACE Index 11 Executive Summary. Sovereign Wealth Funds 2019 23 Managing Continuity...Embracing Change: Sovereign Wealth Fund Direct Investments in 2018-2019 37 Technology, Venture Capital and SWFs: The Role of the Government Forging Innovation and Change 55 SWFs in a Bad Year: Challenges, Reporting, and Responses to a Low Return Environment 65 The Sustainable Development Goals and the Market for Sustainable Sovereign Investments 83 SWFs In-Depth. Mubadala: The 360-degree Sovereign Wealth Fund 97 Annex 1. Sovereign Wealth Research Ranking 2019 103 Annex 2. Sovereign Wealth Funds in Spain PREFACE 8 SOVEREIGN WEALTH FUNDS 2019. PREFACE Preface In 2019, the growth of the world economy slowed by very little margin for stimulating the economy to 2.9%, the lowest annual rate recorded since the through the fiscal and monetary policy strategies. subprime crisis. This was a year in which the ele- In any case, the developed world is undergoing its ments of uncertainty that had previously threate- tenth consecutive year of expansion, and the risks ned the stability of the cycle began to have a more of relapsing into a recessive cycle appear to have serious effect on economic expansion. Among these been allayed in view of the fact that, in spite of re- elements, there are essentially two – both of a poli- cord low interest rates, inflation and debt remain at tical nature – that stand out from the rest. -

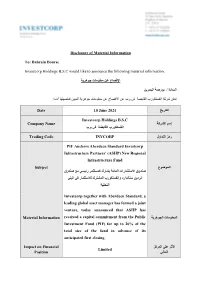

Disclosure of Material Information To: Bahrain Bourse Investcorp Holdings B.S.C Would Like to Announce the Following Material In

Disclosure of Material Information To: Bahrain Bourse Investcorp Holdings B.S.C would like to announce the following material information: اﻹفصاح عن معلومات جوهرية السادة / بورصة البحرين تعلن شركة إنفستكورب القابضة ش.م.ب عن اﻹفصاح عن معلومات جوهرية المبين تفاصيلها أدناه: التاريخ Date 10 June 2021 Investcorp Holdings B.S.C إسم الشركة Company Name إنفستكورب القابضة ش.م.ب رمز التداول Trading Code INVCORP PIF Anchors Aberdeen Standard Investcorp Infrastructure Partners’ (ASIIP) New Regional Infrastructure Fund الموضوع Subject صندوق اﻻستثمارات العامة يشارك كمستثمر رئيسي مع صندوق أبردين ستاندارد وإنفستكورب المشترك لﻻستثمار في البنى التحتية Investcorp together with Aberdeen Standard, a leading global asset manager has formed a joint venture, today announced that ASIIP has المعلومات الجوهرية Material Information received a capital commitment from the Public Investment Fund (PIF) for up to 20% of the total size of the fund in advance of its anticipated first closing. اﻷثر على المركز Impact on Financial Limited المالي Position إفصاحات سابقة ذات Previous relevant صلة )إن ُوجدت( (disclosures (if any ا ﻹسم Name Hazem Ben-Gacem المسمى الوظيفي Title Co-Chief Executive Officer of Investcorp التوقيع Signature ختم الشركة Company Seal PIF Anchors Aberdeen Standard Investcorp Infrastructure Partners’ (ASIIP) New Regional Infrastructure Fund Bahrain, 10th June 2021 – Investcorp together with Aberdeen Standard Investments, a leading global asset manager has formed a joint venture, today announced that ASIIP has received a capital commitment from the Public Investment Fund (PIF) for up to 20% of the total size of the fund in advance of its anticipated first closing. The fund has also received board approval from the Asian Infrastructure Investment Bank (AIIB) to commit US $90 million. -

Marxism and the Solidarity Economy: Toward a New Theory of Revolution

Class, Race and Corporate Power Volume 9 Issue 1 Article 2 2021 Marxism and the Solidarity Economy: Toward a New Theory of Revolution Chris Wright [email protected] Follow this and additional works at: https://digitalcommons.fiu.edu/classracecorporatepower Part of the Political Science Commons Recommended Citation Wright, Chris (2021) "Marxism and the Solidarity Economy: Toward a New Theory of Revolution," Class, Race and Corporate Power: Vol. 9 : Iss. 1 , Article 2. DOI: 10.25148/CRCP.9.1.009647 Available at: https://digitalcommons.fiu.edu/classracecorporatepower/vol9/iss1/2 This work is brought to you for free and open access by the College of Arts, Sciences & Education at FIU Digital Commons. It has been accepted for inclusion in Class, Race and Corporate Power by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. Marxism and the Solidarity Economy: Toward a New Theory of Revolution Abstract In the twenty-first century, it is time that Marxists updated the conception of socialist revolution they have inherited from Marx, Engels, and Lenin. Slogans about the “dictatorship of the proletariat” “smashing the capitalist state” and carrying out a social revolution from the commanding heights of a reconstituted state are completely obsolete. In this article I propose a reconceptualization that accomplishes several purposes: first, it explains the logical and empirical problems with Marx’s classical theory of revolution; second, it revises the classical theory to make it, for the first time, logically consistent with the premises of historical materialism; third, it provides a (Marxist) theoretical grounding for activism in the solidarity economy, and thus partially reconciles Marxism with anarchism; fourth, it accounts for the long-term failure of all attempts at socialist revolution so far.