City and County of Denver, Colorado 2010 Disclosure Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Meeting & Exposition Annual

Vol. 9, No. 6 June 1999 GSA TODAY A Publication of the Geological Society of America 1999 Annual Meeting & Exposition Colorado ConvenConventiontion CenterCenter HyattHyatt RegencyRegency HotelHotel MarriottMarriott CityCity CenterCenter HotelHotel OctoberOctober 25–28,25–28, 19991999 Denver,Denver, ColoradoColorado Table of Contents Crossing Divides Abstracts with Programs . 32 Convenience Information . 26 Employment Service . 22 World Wide Web Exhibits . 20 Visit the GSA Web site to obtain more details and to get the latest information on the Annual Meeting. Field Trips . 13 www.geosociety.org Graduate School Information Forum . 23 Guest Activities . 24 Deadlines Hot Topics at Noon . 9 Abstracts due July 12 Housing . 28 Preregistration and Housing due September 17 (forms(forms enclosed)enclosed) How to Submit Your Abstract . 12 Institute for Earth Science and the Environment . 22 For More Information Call: (303) 447-2020 or 1-800-472-1988 International Program . 6 Call: (303) 447-2020 or 1-800-472-1988 Fax: 303-447-0648 K–16 Education Program . 18 E-mail: [email protected] Membership . 30 Web: www.geosociety.org Registration . 30 Short Courses . 16 Cover photos by John A. Karachewski: Large photo shows the Special Events . 23 Continental Divide—Sawatch Range, Collegiate Peaks Wilderness, Special Programs . 22 Colorado; small photo taken near James Peak, Colorado Technical Program . 3 Travel . 25 Crossing Divides Annual Meeting Committee General Co-Chairs: Mary Kraus, David Budd, University of Colorado Technical Program Co-Chairs: -

Sports 05/24

FREEPRESS Page 6 Colby Free Press Thursday, May 24, 2001 SSSPORTSPORTS College The winner’s circle Vets prepare rookies for ‘big zoo’ DENVER (AP) — The Western Colorado’s 2-1 overtime victory finals appearance came in 1993, when Conference trophy presentation had against the St. Louis Blues was his he and the Los Angeles Kings were inks Hoxie hardly ended when Colorado Ava- ninth goal of the playoffs, while Roy defeated by Roy and the Montreal lanche defenseman Adam Foote began Canadiens. prepping his younger teammates for “You look to guys like Joe and speedster the chaos to come. Patrick and Ray for guidance and ad- “It’s a big zoo,” Foote said after vice going into the Stanley Cup finals,” James White, head track coach at Colorado advanced to the Stanley Cup Blake said. “They are the guys that all Colby Community finals Monday night. “The finals are a of us are following, there’s no doubt College, has an- circus, and as a player, you just have to about it.” nounced that remember all the things you do right Colorado also will draw inspiration Clayton Hill, and keep it as simple as possible.” from forward Peter Forsberg, out for Hoxie, has signed a Foote speaks from experience. He is the season after having his ruptured national letter of in- one of six Avalanche players remain- spleen removed May 10. Forsberg re- tent to run track for ing from Colorado’s 1996 title team turned to the arena as a spectator Mon- the Trojans. that swept the Florida Panthers to cap- lowered his goals-against average to a day night and watched the Avalanche Hill has been a ture Denver’s first major professional career-best 1.74. -

Summer Sessions• Survive•

Marshall University Marshall Digital Scholar The Parthenon University Archives Spring 3-27-1990 The Parthenon, March 27, 1990 Marshall University Follow this and additional works at: https://mds.marshall.edu/parthenon Recommended Citation Marshall University, "The Parthenon, March 27, 1990" (1990). The Parthenon. 2787. https://mds.marshall.edu/parthenon/2787 This Newspaper is brought to you for free and open access by the University Archives at Marshall Digital Scholar. It has been accepted for inclusion in The Parthenon by an authorized administrator of Marshall Digital Scholar. For more information, please contact [email protected]. ------ ~ --·---- • Marshall" University enon Tuesday. L1mc h 27. 1990 HUNTINGTON. V/ VA Vol 90. No 85 COB fee proposal drawing mixed reactions By Ric A. Massie the students paying for accreditation are personnel needs," Gould said. Such im disadvantage, so the administration should Reporter not necessarily the ones who will reap the provements would include hiring additional look elsewhere for the funding," said Tim benefits." faculty or increasing salaries to keep qual Beverly, Beckley senior. A recent recommendation by Marshall's "Ifthe per student funding for the College ity faculty, he said. Cindy Warner, Culloden sophomore, said, student body president-elect for a fee in ofB usiness was as equitable as it should be, Gould said the money would be regulated "Even though there might be an increase, crease for students in the College of Busi no special assessment would be needed," by "earmarking" it for COB use only. there's no guarantee of accreditation." ness is receiving diverse reactions from said Dr. Robert P. Alexander, COB dean. -

The Moody Blues Tour / Set List Project - Updated April 9, 2006

The Moody Blues Tour / Set List Project - updated April 9, 2006 compiled by Linda Bangert Please send any additions or corrections to Linda Bangert ([email protected]) and notice of any broken links to Neil Ottenstein ([email protected]). This listing of tour dates, set lists, opening acts, additional musicians was derived from many sources, as noted on each file. Of particular help were "Higher and Higher" magazine and their website at www.moodies- magazine.com and the Moody Blues Official Fan Club (OFC) Newsletters. For a complete listing of people who contributed, click here. Particular thanks go to Neil Ottenstein, who hosts these pages, and to Bob Hardy, who helped me get these pages converted to html. One-off live performances, either of the band as a whole or of individual members, are not included in this listing, but generally can be found in the Moody Blues FAQ in Section 8.7 - What guest appearances have the band members made on albums, television, concerts, music videos or print media? under the sub-headings of "Visual Appearances" or "Charity Appearances". The current version of the FAQ can be found at www.toadmail.com/~notten/FAQ-TOC.htm I've construed "additional musicians" to be those who played on stage in addition to the members of the Moody Blues. Although Patrick Moraz was legally determined to be a contract player, and not a member of the Moody Blues, I have omitted him from the listing of additional musicians for brevity. Moraz toured with the Moody Blues from 1978 through 1990. From 1965-1966 The Moody Blues were Denny Laine, Clint Warwick, Mike Pinder, Ray Thomas and Graeme Edge, although Warwick left the band sometime in 1966 and was briefly replaced with Rod Clarke. -

Real Estate This Week

» - MANCHESTER HERALD. Friduy. Jiin. 27. 1984 bank in downtown Bristol to meet needs of the city's large blue-collar population. Citytrust takes on IBM, Wang Business Robert F. Festa. one of the organizers and lorm er president of Terryville Trust Co., would Woeful Indians In Brief Sbe the new bunk's president and chief executive BRIDGEPORT (UPI) - In a "W e feel it fills a very important mine needs of clients and recom Cut your own taxes: Bond commission OK’s officer. sharp departure from traditional void in the market," said Jonathai], mend hardware and software that Cigna chairman resigns The bank would sell 250,000 shares of common banking services, Citytrust plans A. Cunitz, managing director of the might be purchased from any of Deductions can add up new highway funding bow to ECHS slock to the public at SIO each to raise $2.5 million lo battle computer giants such as new service. "W e hold their hand the leading computer companies. Bl.OOMFlELD — Cigna Corp has confirmed in start-up capital. IBM and Wang Corp. to design throughout the entire process. You The center will be based in ... page 2 ... page 10 .. page 16 Ralph S. Saul will resign as chairman lo be It plans to start with nine employees, add seven computer systems for profession can make mistakes in this area and Westport and concentrate on Fair- succeeded by Roberl D. Kilpatrick who will more in the second year and four more in the third als and smaller companies. it can lead to bud results." field, Litchfield and New Haven continue as president and chief executive officer. -

2015-16 UTSA Roadrunners Men's Basketball Almanac

2015-16 UTSA Roadrunners Men’s Basketball Almanac Table of Contents Season Outlook _____________________________2-3 General Information Roster _____________________________________4-5 Location ______________________ San Antonio, Texas Schedule ____________________________________ 6 Enrollment _________ 28,628 (24,342 undergraduate) Media Information ____________________________ 7 Founded _________________________________1969 goUTSA.com _________________________________ 8 Meet The Roadrunners Nickname __________________________Roadrunners George Matthews ____________________________ 10 Colors _____ Navy blue (289), orange (1665) and white Gino Littles _________________________________ 11 Home Court __________________Convocation Center Christian Wilson _____________________________ 12 Capacity ______________________2,650 (temporary) Austin Karrer _______________________________ 13 Ryan Bowie _________________________________ 14 Conference _____________________ Conference USA Lucas O’Brien _______________________________ 15 Affiliation ______________________ NCAA Division I Phillip Jones ________________________________ 16 Athletic Director _____________________ Lynn Hickey James Ringholt ______________________________ 17 President _______________________Dr. Ricardo Romo Terrell Scruggs/J.R. Harris _____________________ 18 Kyle Massie/Ömer Alp Aksu __________________ 19 Athletic Department Phone _________ 210-458-4161 Garrett Thibodeaux/Nick Allen ________________ 20 Ticket Office Phone _______________ 210-458-UTSA A.J. Cockrell/Nick Billingsley -

New York City, New York Star Sound Studios

Shows the Eventide was used at LOVE GUN TOUR REHEARSALS 06/20/77 06/21/77 06/22/77 06/23/77 06/24/77 New York City, New York Star Sound Studios 06/25/77 06/26/77 06/27/77 06/28/77 06/29/77 06/30/77 07/01/77 07/02/77 Newburgh, New York Theatre Techniques, Hanger E, Stewart AFB 07/07/77 Halifax, Nova Scotia Halifax Forum LOVE GUN TOUR DATES Date City Country Venue Opening band 07/08/77 Halifax, Nova Scotia Halifax Forum 07/09/77 Moncton, New Brunswick Moncton Coliseum 07/12/77 Montreal, Quebec Montreal Forum 07/14/77 Ottawa, Ontario Ottawa Civic Centre 07/16/77 Kitchener, Ontario Kitchener Memorial Auditorium 07/18/77 London, Ontario London Gardens 07/19/77 Sudbury, Ontario Sudbury Community Arena 07/21/77 Winnipeg, Manitoba Winnipeg Arena 07/24/77 Vancouver, British Columbia Pacific Coliseum 07/27/77 Edmonton, Alberta Northlands Coliseum 07/28/77 Lethbridge, Alberta Canada Games Sportsplex 07/31/77 Calgary, Alberta Stampede Corral 08/02/77 Regina, Saskatchewan Agridome 08/04/77 Salt Lake City, Utah Salt Palace 08/07/77 Billings, Montana MetraPark Arena 08/08/77 Rapid City, South Dakota Rushmore Plaza Civic Center 08/11/77 Spokane, Washington Spokane Coliseum 08/12/77 Seattle, Washington Seattle Center Coliseum 08/13/77 Portland, Oregon Portland Memorial Coliseum 08/16/77 Daly City, California Cow Palace 08/17/77 Fresno, California Selland Arena 08/19/77 San Diego, California San Diego Sports Arena 08/21/77 Tucson, Arizona Tucson Convention Center 08/22/77 Phoenix, Arizona Arizona Veterans Memorial Coliseum * 08/26/77 * 08/27/77 Inglewood, -

The Broward County Civic Arena: 2 History, Facts and Opportunities

Contributors Purvi Bhogaita, Director of Real Property Public Works Department Leah Brasso, Assistant to the Department Director Finance and Administrative Services Monica Cepero, Assistant County Administrator County Administration Marcie Gelman, Assistant Budget Director Office of Management and Budget Services Roberto Hernandez, Deputy County Administrator County Administration Carol Hudson, Vice President, Sports Development Greater Fort Lauderdale Visitors & Convention Bureau Izadora Isidore-Thomas, Graduate Intern Office of the County Administrator Scott Miller, Chief Financial Officer Finance and Administrative Services Bob Miracle, Deputy Chief Financial Officer Finance and Administrative Services Noel Pfeffer, Deputy County Attorney Office of the County Attorney Henry Sniezek, Director of Planning and Redevelopment Environmental Protection and Growth Management Department We also appreciate assistance provided by the County Attorney’s Office, the County Auditor’s Office, and the Office of Public Communications. The Broward County Civic Arena: 2 History, Facts and Opportunities EXECUTIVE SUMMARY In September 2013, the Florida Panthers hockey team was sold for the fourth time in its twenty-year history. The new owners, assumed responsibility for the team’s parent company – Sunrise Sports & Entertainment and several of its subsidiaries, including, the Arena Operating Company (AOC), the Arena Development Company (ADC) and the Florida Panthers Hockey Club. Immediately upon the sale, SSE approached Broward County with a request to -

2019 UTSA Men S Basketball

2 3 5 10 11 Jhivvan Jackson • G Byron Frohnen • F Makani Whiteside • G Erik Czumbel • G Adokiye Iyaye • G 6-0 • 170 • Jr.-1L 6-6 • 230 • Sr.-3L 6-4 • 190 • Fr.-HS 6-3 • 185 • Fr.-HS 6-3 • 180 • So.-1L Bayamón, Puerto Rico Las Vegas, Nev. Madera, Calif. Verona, Italy Oklahoma City, Okla. 12 21 22 23 24 Phoenix Ford • F Knox Hellums • G Keaton Wallace • G Atem Bior • F Jacob Germany • C 6-8 • 230 • R-So.-TR 6-5 • 205 • R-Jr.-TR 6-3 • 185 • Jr.-2L 6-7 • 225 • Sr.-1L 6-11 • 220 • Fr.-HS St. Petersburg, Fla. Tomball, Texas Dallas, Texas Brisbane, Australia Kingston, Okla. 25 32 44 Adrian Rodriguez • F Austin Timperman • F Luka Barisic • F 6-7 • 245 • R-So.-1L 6-9 • 190 • Fr.-RS 6-10 • 240 • Jr.-TR Tulsa, Okla. The Woodlands, Texas Oijek, Croatia Steve Henson Mike Peck Scott Thompson Adam Hood Jeff Luster Head Coach Associate Head Coach Assistant Coach Assistant Coach Director of Operations Kansas State, 1990 Northwood, 1993 Mississippi, 2002 Air Force, 2008 Tabor College, 1996 2019-20 MEN’S BASKETBALL ROADRUNNERS TABLE OF CONTENTS QUICK FACTS QUICK FACTS SEASON OUTLOOK GENERAL INFORMATION Roster 2-3 Name of Institution The University of Texas at San Antonio Schedule 4 Location San Antonio, Texas Media Information 5 Founded 1969 Coaching Staff 6 Enrollment 32,101 Nickname Roadrunners MEET THE ROADRUNNERS School Colors Navy Blue (PMS 289), Orange (PMS 1665) and White Jhivvan Jackson 8-9 Arena (Capacity) Convocation Center (2,650) Byron Frohnen 10-11 Year Opened 1975 Makani Whiteside/Erik Czumbel 12 Conference Conference USA Adokiye Iyaye 13 President T. -

Address List of Sports Teams All Ages Basketball Teams: Mens

ADDRESS LIST OF SPORTS TEAMS (*This list is current as of January, 2003. Check to see if mailing and website addresses, and phone numbers have not changed from year to year. Womens’ basketball teams are marked with a (W) after the team name.) ALL AGES BASKETBALL TEAMS: MENS’ AND WOMENS’ Atlanta Hawks RE: Free Stuff for Kids Cleveland Rockers One CNN Center, Ste. 405 Gund Arena Atlanta, GA 30303 One Center Court http://nba.com/hawks Cleveland, OH 44115 http://wnba.com/rockers Boston Celtics 151 Merrimac Street Dallas Mavericks 5th Floor Reunion Arena Boston, MA 02114 777 Sports Street http://nba.com/celtics Dallas, TX 75207 http://nba.com/mavericks Charlotte Hornets 100 High Drive Denver Nuggets Charlotte, NC 28217 1635 Clay Street http://nba.com/hornets PO Box 4658 Denver, CO 80204-0658 Charlotte Sting (W) http://nba.com/nuggets 3308 Oak Lake Boulevard Ste. B Detroit Pistons Charlotte, NC 28208 The Palace of Auburn Hills http://wnba.com/sting 2 Championship Drive Auburn Hills, MI 48326 Chicago Bulls http://nba.com/pistons 1901 West Madison Chicago, IL 60612 Detroit Shock (W) http://nba.com/bulls The Palace of Auburn Hills 2 Championship Drive Cleveland Cavaliers Auburn Hills, MI 48326 Gund Arena http://wnba.com/shock One Center Court Cleveland, OH 44115 http://nba.com/cavaliers 8 Golden State Warriors Milwaukee Bucks 1221 Broadway The Bradley Center 20th Floor 1001 N. Fourth Street Oakland, CA 94612 Milwaukee, WI 53203-1312 http://nba.com/warriors http://nba.com/bucks Houston Comets (W) Minnesota Timberwolves Two Greenway Plaza Target Center Houston, TX 77046 600 First Avenue N http://wnba.com/comets Minneapolis, MN 55403 http://nba.com/timberwolves Houston Rockets Two Greenway Plaza New Jersey Nets Houston, TX 77046 405 Murray Hill Parkway http://nba.com/rockets East Rutherford, NJ 07l73 http://nba.com/nets Indiana Pacers 300 E. -

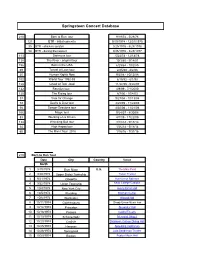

Springsteen Concert Database

Springsteen Concert Database 210 Born to Run tour 9/19/74 - 5/28/76 121 BTR - initial concerts 9/19/1974 - 12/31/1975 35 BTR - chicken scratch 3/25/1976 - 5/28/1976 54 BTR - during the lawsuit 9/26/1976 - 3/25/1977 113 Darkness tour 5/23/78 - 12/18/78 138 The River - original tour 10/3/80 - 9/14/81 156 Born in the USA 6/29/84 - 10/2/85 69 Tunnel of Love tour 2/25/88 - 8/2/88 20 Human Rights Now 9/2/88 - 10/15/88 102 World Tour 1992-93 6/15/92 - 6/1/93 128 Ghost of Tom Joad 11/22/95 - 5/26/97 132 Reunion tour 4/9/99 - 7/1/2000 120 The Rising tour 8/7/00 - 10/4/03 37 Vote for Change 9/27/04 - 10/13/04 72 Devils & Dust tour 4/25/05 - 11/22/05 56 Seeger Sessions tour 4/30/06 - 11/21/06 106 Magic tour 9/24/07 - 8/30/08 83 Working on a Dream 4/1/09 - 11/22/09 134 Wrecking Ball tour 3/18/12 - 9/18/13 34 High Hopes tour 1/26/14 - 5/18/14 65 The River Tour 2016 1/16/16 - 7/31/16 210 Born to Run Tour Date City Country Venue North America 1 9/19/1974 Bryn Mawr U.S. The Main Point 2 9/20/1974 Upper Darby Township Tower Theater 3 9/21/1974 Oneonta Hunt Union Ballroom 4 9/22/1974 Union Township Kean College Campus Grounds 5 10/4/1974 New York City Avery Fisher Hall 6 10/5/1974 Reading Bollman Center 7 10/6/1974 Worcester Atwood Hall 8 10/11/1974 Gaithersburg Shady Grove Music Fair 9 10/12/1974 Princeton Alexander Hall 10 10/18/1974 Passaic Capitol Theatre 11 10/19/1974 Schenectady Memorial Chapel 12 10/20/1974 Carlisle Dickinson College Dining Hall 13 10/25/1974 Hanover Spaulding Auditorium 14 10/26/1974 Springfield Julia Sanderson Theater 15 10/29/1974 Boston Boston Music Hall 16 11/1/1974 Upper Darby Tower Theater 17 11/2/1974 18 11/6/1974 Austin Armadillo World Headquarters 19 11/7/1974 20 11/8/1974 Corpus Christi Ritz Music Hall 21 11/9/1974 Houston Houston Music Hall 22 11/15/1974 Easton Kirby Field House 23 11/16/1974 Washington, D.C. -

KISS Bootlegs

Sten1972's KISS Live Recordings (updated 131209) DVD CD MP3 Audio NCB rating Comment Pre Album Shows 1973 6 16 Amityville, The Daisy X 1973 12 21 New York, Coventry X 1,5 tracks is filmed 1973 12 22 New York, Coventry X 4 Released on DVD 1973 12 31 New York, Academy Of Music X 2 Remastered version, missing a few seconds of "Deuce" "Kiss" Tour 1974 2 17 Long Beach, Civic Auditorium X 3 7- KISS Vision Remaster, not with original audio 1974 2 21 Los Angeles, Aquarius Theater X 5 Released on DVD The ABC In Concert, broadcasted 740329. Best version on Kissology 1974 3 25 Washington, Bayou Theater X 4 The 10.30 PM show. 2nd or 3rd gen upgrade (Tolvis) 1974 4 7 Detroit, Michigan Palace X 5 FM broadcast Master upgrade 1974 4 18 Memphis, La Fayette Music Hall X 4 FM broadcast Good recording but a lot of wobble. From silver CD + speed corrected 1974 4 29 Philadelphia, KYW-TV Studios X 5 Released on DVD The Mike Douglas show 1974 5 31 Long Beach, Civic Auditorium X X 4 FM broadcast My CD-version (vinyl transfer from 2010) doesn't include "Baby Let Me Go" 1974 7 16 Baton Rouge, Independence Hall X 4 Master upgrade 1974 8 4 South Bend, Morris Civic Auditorium X 3 Master upgrade, re-pitched "Hotter Than Hell" Tour 1974 10 18 Hammond, The Parthenon Theatre X 4 1974 10 21 East Lansing, The Brewery X 5 1974 10 25 Passaic, Capitol Theatre X PRO-shot This was filmed in B&W according to the owner of the club 1975 1 10 Portland, Paramount Theater X PRO-shot 1975 1 31 San Francisco, Winterland Ballroom X 5 10- Released on DVD Dodo's Upgrade from august 2006, better than the official release "Dressed To Kill" Tour 1975 3 21 New York, Beacon Theater X 2 Fasterpdiddy's cassette transfer from 2011, the 7.30 PM show 1975 3 24 Portland, Paramount Theater X PRO-shot 1975 4 1 California, NBC Studios X X 5 TV broadcast NBC Midnight Special 1975 4 19 Palatine, Fremd High School Gymnasium X 2 Tolvis version.