1990 0101 DTCAR.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

International Bond Markets

4/15/2021 International Bond Markets (for private use, not to be posted/shared online) • Last Class • International Equity Markets - Differences - Investments Vehicles: Dual Listings (ADR), International ETFs - Valuation Methods (DDM, Discounting Free CFs, Multiples) • International Diversification pays • Returns in International Equity Markets - Huge dispersion in ERP across markets. Not easy to explain with existing models (CAPM, Fama-French Factors, etc.) - Many proposed factors to explain ERPs. 1 4/15/2021 • This Class • International Bond Markets ⋄ Organization and Issuing Techniques ⋄ Different Instruments ⋄ Valuation ⋄ Examples • CASE 6: Brady Bonds (due next Thursday, April 22) Group: Dixit, Erick International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell debt securities, usually bonds. Size of the world bond market (’20 debt outstanding): USD 128 trillion. - Governments and International Organizations: USD 87 trillion (68%). - U.S. bond market debt: USD 49.8 trillion (38%). Organization - Decentralized, OTC market, with brokers and dealers. - Small issues may be traded in exchanges. - Daily trading volume in the U.S.: USD 822 billion - Government debt dominates the market. - Used to indicate the shape of the yield curve. 2 4/15/2021 • Evolution of Global Bond Market: Huge increase in issuance in 2020 (pandemic & very low interest rates) • Evolution of Global Bond Market EM issues have significantly increased over the past 20 year. EM play a significant role. 3 4/15/2021 • U.S. Bond Market Dominated by Government & Corporate Debt, & MBS. • Typical Bond Market: Canada Dominated by government issues. 4 4/15/2021 • The world bond market is divided into three segments: - Domestic bonds: Issued locally by a domestic borrower. -

Ubs India Securities Private Limited

Swiss_company in India_Book fin.qxd 3/17/07 5:25 PM Page 92 UBS INDIA SECURITIES PRIVATE LIMITED UBS is one of the leading financial firms in the world, Swiss business unit network ran to 357 branches with offices in 50 countries and business organised with a further 82 branches abroad. into key distinct areas of equities - fixed income, rates and currencies, and investment banking On 3rd November 2000, UBS AG merged with PaineWebber Inc., a full-service securities firm Global Overview of UBS AG located in New York and founded in 1879. UBS AG was created on July 1, 1998, with the Today UBS is one of the leading financial firms merger of Union Bank of Switzerland (based in the world, serving discerning clients globally. in Zurich) and Swiss Bank Corporation (based in As an organisation, it combines financial strength Basel). Swiss Bank Corporation (SBC) was founded with an international culture that embraces change. in 1872 under the name Basler Bankverein and in An integrated firm, UBS creates added value for 1945 it took over the troubled Basler Handelsbank, clients by drawing on the combined resources and one of Switzerland's large banks, founded in 1862. expertise of all its businesses. It is the leading global In the last decade of the twentieth century, SBC wealth manager, a top-tier investment banking and strengthened its international orientation again securities firm, and one of the largest global asset by taking over several foreign finance firms managers. (O'Connor & Associates, Chicago; Brinson Partners, Inc., Chicago; S.G.Warburg Plc, London). UBS Investment Bank is headquartered in London By 1997, the Swiss network comprised 288 and New York and employs 18,200 people in branches with 77 offices outside Switzerland. -

Federal Reserve Bank of Chicago Annual Report

7 OPERATION OF FEDERAL RESERVE BANK OF CHICAGO 1931 SEVENTH FEDERAL RESERVE DISTRICT SEVENTEENTH ANNUAL REPORT TO THE FEDERAL RESERVE BOARD Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis OPERATION OF FEDERAL RESERVE BANK OF CHICAGO 1931 SEVENTH FEDERAL RESERVE DISTRICT SEVENTEENTH ANNUAL REPORT TO THE FEDERAL RESERVE BOARD Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis FEDERAL RESERVE BANK OF CHICAGO Directors and Officers for 1932 CLASS A—DIRECTORS JAMES B. MCDOUGAL, Governor GEORGE J. SCHALLER, Storm Lake, Iowa JOHN H. BLAIR, Deputy Governor (1932) CHARLES R. MCKAY, Deputy Governor President, Citizens First National Bank JAMES H. DILLARD, Deputy Governor GEORGE M. REYNOLDS, Chicago, Illinois (1933) WILLIAM C. BACHMAN, Assistant Dep- Chairman, Executive Committee, Continental Illinois Bank and Trust Company uty Governor EDWARD R. ESTBERG, Waukesha, Wiscon- EUGENE A. DELANEY, Assistant Deputy sin (1934) Governor President, Waukesha National Bank DON A. JONES, Assistant Deputy Gov- CLASS B—DIRECTORS ernor ROBERT M. FEUSTEL, Fort Wayne, In- OTTO J. NETTERSTROM, Assistant Deputy diana (1932) Governor President, Public Service Company of Indiana MAX W. BABB, Milwaukee, Wisconsin FRED BATEMAN, Manager, Securities De- H933) partment Vice-President, Allis-Chalmers Manufacturing Company JOSEPH C. CALLAHAN, Manager, Member STANFORD T. CRAPO, Detroit, Michigan Bank Accounts Department (1934) ROBERT E. COULTER, Manager, Cash Cus- Secretary and Treasurer, Huron Portland Cement tody Department Company ALBA W. DAZEY, Manager, Investment CLASS C—DIRECTORS Department JAMES SIMPSON, Chicago, Illinois (1932) IRVING FISCHER, Manager, Check Depart- Chairman of Board, Marshall Field and Company ment EUGENE M. STEVENS, Evanston, Illinois ROBERT J. -

UBS AG (Registrant’S Name)

6-K Page 1 of 5 6-K 1 d642077d6k.htm 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934 Date: December 5, 2013 Commission File Number: 1-15060 UBS AG (Registrant’s Name) Bahnhofstrasse 45, Zurich, Switzerland, and Aeschenvorstadt 1, Basel, Switzerland (Address of principal executive office) Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F. Form 20-F Form 40-F ! This Form 6-K consists of the news release of UBS AG, which appears immediately following this page. http://www.sec.gov/Archives/edgar/data/1114446/000119312513462992/d642077d6k... 13/12/2013 6-K Page 2 of 5 UBS announces changes to Group Executive Board and Corporate Center Zurich/Basel | 05 Dec 2013, 06:45 | Price Sensitive Information John Fraser to retire as CEO Global Asset Management business, retaining his position as its Chairman, Ulrich Koerner to become CEO Global Asset Management, Tom Naratil to become Group Chief Operating Officer in addition to current position as Group Chief Financial Officer. Zurich/Basel, 05 December 2013 – UBS today announced a number of changes to its senior leadership team and Corporate Center structure. John Fraser, who has been Chairman and CEO Global Asset Management since 2001, has decided to retire from his CEO role and as a member of UBS’s Group Executive Board, effective 31 December 2013. This follows a long and distinguished career at UBS and in finance which began in the Australian Treasury and has spanned five decades. -

1999-2000 SAR Guide

A Guide to 1999-2000 SARs and ISIRs APPENDIX C NSLDS FINANCIAL AID HISTORY/NSLDS MATCH FLAGS NSLDS Financial Aid History The “Loan Satisfactory Repayment Arrange- 1999-2000 ments” flag reflects the status of loans with a “DX” (Defaulted, satisfactory arrangements Changes to NSLDS data since previous made including six consecutive monthly pay- Prescreening ments). If this flag is set to “Y” a comment will be included on the SAR/ISIR informing the student and the school of that status, but no “C” flag will An indicator will inform schools where NSLDS be set. information provided on a SAR/ISIR has changed since the last CPS transaction. A “#” sign will Aggregate Amounts for FFELP/Direct Loans print in front of the status field for Overpayments, Defaulted Loans, Discharged Loans, Loan Satis- Section factory Repayment Arrangements, or Active Bankruptcy if there has been a change in that The Unsubsidized Loans field has been deleted status since the last CPS transaction. and replaced with a Combined Loans field, which reflects the total amount of subsidized and The “#” sign will also print in front of the Aggre- unsubsidized loans the student has borrowed. gate Amount for FFELP/Direct Loans, Cumula- This change is consistent with guidance provided tive Perkins Loans, or the 1999-2000 Pell Pay- in Dear Colleague Letter, GEN-97-3, which was ment Data sections when information within that published in May 1997. In addition, the Consoli- section has changed since the last CPS transaction. dated Loans field has been renamed FFEL Con- Finally, a “#” sign will print in front of each solidated Loans, and will only include amounts of reported loan in the Loan Detail section when FFEL Consolidated Loans. -

Banking and Insurance - Should Ever the Twain Meet? Emeric Fischer William & Mary Law School

College of William & Mary Law School William & Mary Law School Scholarship Repository Faculty Publications Faculty and Deans 1992 Banking and Insurance - Should Ever the Twain Meet? Emeric Fischer William & Mary Law School Repository Citation Fischer, Emeric, "Banking and Insurance - Should Ever the Twain Meet?" (1992). Faculty Publications. 485. https://scholarship.law.wm.edu/facpubs/485 Copyright c 1992 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository. https://scholarship.law.wm.edu/facpubs Emeric Fischer* Banking and Insurance-Should Ever the Twain Meet? TABLE OF CONTENTS I. Introduction . 727 II. Evolution of Banking in the United States . 731 A. Banking Prior to the Civil War .. .. .. .. .. .. .. .. .. .. 731 1. From the Revolutionary War to 1836 . 731 2. The State Free Banking System, 1837 to 1864 . 733 B. The National Free Banking System, 1864 to 1933 . 734 1. Prior to 1913 . .. .. .. .. .. .. .. .. .. .. 734 2. Mter 1913 . 735 III. Regulation of Banking . 737 A. The Glass-Steagall Act and the FDIC . 737 B. Policy Goals of Federal Regulation. 738 1. The Broad Goals . 739 2. General Constraints on Federal Banking Policy . 739 C. The Policy Implementing Tools (Regulatory Mechanisms) . 741 1. Entry Restrictions .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 741 2. Capitalization Requirements..................... 743 3. Limitation of and Prohibition Against Specific Activities. 744 4. Restrictions on Mfiliations and Geographic Expansion . 749 5. Lending and Borrowing Limitations . 750 * R. Hugh and Nolie A. Haynes Professor of Law, William and Mary School of Law. B.S. University of South Carolina 1951; J.D. 1963 and M.L.&T. 1964 College of William and Mary, Marshall-Wythe School of Law. -

JP Morgan Investment Management Inc. | Client Relationship Summary

J.P. MORGAN INVESTMENT MANAGEMENT INC. JULY 9, 2021 Client Relationship Summary The best relationships are built on trust and transparency. That’s why, at J.P. Morgan Investment Management Inc. (“JPMIM”, “our”, “we”, or “us”), we want you to fully understand the ways you can invest with us. This Form CRS gives you important information about our wrap fee programs, short-term fixed income and private equity separately managed accounts (“SMAs”). We are registered with the Securities and Exchange Commission (“SEC”) as an investment adviser. Brokerage and investment advisory services and fees differ, and it is important for retail investors (“you”) to understand the differences. Free and simple tools are available for you to research firms and financial professionals at Investor.gov/CRS, which also provides educational materials about broker-dealers, investment advisers, and investing. WHAT INVESTMENT SERVICES AND ADVICE CAN YOU PROVIDE ME? We have minimum account requirements, and for Private Equity SMAs, Wrap Fee and Other Similar Managed Account Programs clients must generally satisfy certain investor sophistication requirements. We offer investment advisory services to retail investors through SMAs More detailed information about our services is available at available within wrap fee and other similar managed account programs. www.jpmorgan.com/form-crs-adv. These programs are offered by certain financial institutions, including our affiliates ("Sponsors"). Depending on the SMA strategy, these accounts invest in individual securities (such as stocks and bonds), exchange-traded funds CONVERSATION STARTERS (“ETFs”) and/or mutual funds. Throughout this Client Relationship Summary we’ve included When we act as your discretionary investment manager, you give us “Conversation Starters.” These are questions that the SEC thinks you authority to make investment and trading decisions for your account without should consider asking your financial professional. -

Download Testimony

Testimony of Ina R. Drew Former Head of the Chief Investment Office, JPMorgan Chase & Co. Before the U.S. Senate Permanent Subcommittee on Investigations Washington, D.C. March 15, 2013 Good morning, Chairman Levin, Ranking Member McCain, and members of the Subcommittee. Thank you for the opportunity to meet and discuss with you my perspective on the losses incurred last year in JPMorgan Chase’s synthetic credit portfolio, one of many portfolios managed by the Company’s Chief Investment Office (CIO) when I was the head of that office. I am greatly saddened by the entire episode, which has caused financial and reputational harm to JPMorgan Chase and a large number of people with whom I was honored to work, and I deeply regret that the losses occurred on my watch. I am also saddened that the losses led to my departure from the Company, to which I had devoted 30 years of my life. Before I address the synthetic credit portfolio, I believe it would be useful for the Subcommittee to know about my background and career and about the range of asset-liability management activities of the CIO at JPMorgan Chase. My background and career at JPMorgan Chase After attending public schools, I graduated from The Johns Hopkins University, as part of only the fourth class that admitted women, with a degree in international studies. I went on to earn a master’s in international affairs from Columbia University. I have been a member of the Board of Trustees of The Johns Hopkins University for the past twelve years. -

Rule D4 Institution Numbers and Clearing Agency/Representative Arrangements

RULE D4 INSTITUTION NUMBERS AND CLEARING AGENCY/REPRESENTATIVE ARRANGEMENTS 2021CANADIAN PAYMENTS ASSOCIATION This Rule is copyrighted by the Canadian Payments Association. All rights reserved, including the right of reproduction in whole or in part, without express written permission by the Canadian Payments Association. Payments Canada is the operating brand name of the Canadian Payments Association (CPA). For legal purposes we continue to use “Canadian Payments Association” (or the Association) in these rules and in information related to rules, by-laws, and standards. RULE D4 – INSTITUTION NUMBERS AND CLEARING AGENCY/REPRESENTATIVE ARRANGEMENTS TABLE OF CONTENTS IMPLEMENTED ............................................................................................... 3 AMENDMENTS PRE-NOVEMBER 2003 ........................................................ 3 AMENDMENTS POST-NOVEMBER 2003 ..................................................... 3 INTRODUCTION ................................................................................................................. 6 ELIGIBILITY......................................................................................................................... 6 INSTITUTION NUMBERS ................................................................................................... 6 AMALGAMATION AND ACQUISITION .............................................................................. 6 NON-MEMBER ENTITIES .................................................................................................. -

1985 0101 NSCCAR.Pdf

National Securities Clearing Corporation Corporate Office 55 Water Street New York, New York 10041 (212) 510-0400 Boston One Boston Place Boston, Massachusetts 02108 Chicago 135 South LaSalle Street Chicago, Illinois 60603 Cleveland 900 Euclid Avenue Cleveland, Ohio 44101 Dallas Plaza of the Americas TCBTower Dallas, Texas 75201 Denver Dominion Plaza Table of Contents 600 17th Street Denver, Colorado 80202 To NSCC Participants 2 Detroit NSCC Board of Directors 4 3153 Penobscot Building Detroit, Michigan 48226 NSCC Officers 8 Jersey City Introduction 9 One Exchange Place Jersey City, New Jersey 07302 The Year in Review 10 Los Angeles Municipal Bond Program 12 615 South Flower Street Los Angeles, California 9001.7 Fund/SERV 14 Milwaukee Automated Customer Account Transfer Service 16 777 East Wisconsin Avenue Milwaukee, Wisconsin 53202 International Securities Clearing Corporation 18 Minneapolis Audited Financial Statements 20 IDS Center 80 South 8th Street Participating Organizations 26 Minneapolis, Minnesota 55402 New York 55 Water Street New York, New York 10041 St. Louis One Mercantile Tower Cover: 1985 was a year during which NSCC anticipated and St. Louis, Missouri 63101 responded to the expanding needs of the financial services San Francisco industry ... 50 California Street • As marketplace self-regulatory organizations, represented San Francisco, California 94111 here by a New York Stock Exchange Guide/Constitution Toronto and Rules, proposed new rules on broker-dealers' transfer Two First Canadian Place of client accounts, NSCC implemented the Automated Toronto, Ontario, Canada M5X lA9 Customer Account Transfer Service. • While continuing to serve its traditional equity, corporate bond and municipal bond marketplaces, represented by volume charts on the computer screen, NSCC expanded its comparison services to include municipal bond syndi cates, when-issued and extended-settlement trades. -

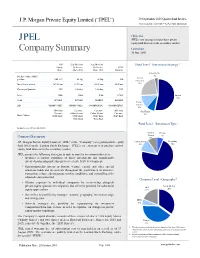

JPEL Company Summary

J.P. Morgan Private Equity Limited (“JPEL”) 30 September 2010 Quarter End Review Professional Investors Only – Not For Public Distribution Objective JPEL JPEL’s core strategy is to purchase private equity fund interests in the secondary market. Company Summary Launched 30 June 2005 US$ Zero Dividend Zero Dividend Fund Level – Investment Strategy1,2 Equity Preference Preference JPEL Share Share 2013 Share 2015 Warrants Infrastructure Net Asset Value (“NAV”) 3% Special per share US$ 1.29 60.15p 56.50p N/A Situations No. of shares in issue 367.88 mm 63.37 mm 69.42 mm 58.08 mm 23% Currency of Quotation US$ £ Sterling £ Sterling US$ Ticker JPEL JPEZ JPZZ JPWW Buyout 53% Sedol B07V0H2 B07V0R2 B00DDT8 B60XDY5 Venture ISIN GB00B07V0H27 GB00B07V0R25 GG00B00DDT81 GG00B60XDY53 Capital 13% ABN Amro Cazenove Cazenove ABN Amro Real Estate Cazenove Collins Stewart Collins Stewart Cazenove 8% Market Makers HSBC Bank HSBC Bank HSBC Bank HSBC Bank Winterflood Winterflood Fund Level – Investment Type1 All figures as at 30 September 2010. Funded Primary Primary 6% Company Description 10% J.P. Morgan Private Equity Limited (“JPEL” or the “Company”) is a global private equity Co-Investment Secondary 72% fund listed on the London Stock Exchange. JPEL’s core strategy is to purchase private 12% equity fund interests in the secondary market. JPEL pursues the following strategies to seek to meet its investment objectives •Acquires secondary portfolios of direct investments and siggynificantly invested partnership investments to accelerate NAV development. • Opportunistically invests in buyout, venture capital, and other special situations funds and investments throughout the world based on attractive transaction values, advantageous market conditions, and compelling risk- adjusted return potential. -

Interstate Banking Developments in Florida: Pushing Through Legal Barriers and Toward a Level Playing Field

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by NSU Works Nova Law Review Volume 9, Issue 1 1984 Article 1 Interstate Banking Developments in Florida: Pushing Through Legal Barriers and Toward a Level Playing Field Scott W. Dunlap∗ ∗ Copyright c 1984 by the authors. Nova Law Review is produced by The Berkeley Electronic Press (bepress). https://nsuworks.nova.edu/nlr Interstate Banking Developments in Florida: Pushing Through Legal Barriers and Toward a Level Playing Field Scott W. Dunlap Abstract The Florida banking market is one of the most coveted in the country. KEYWORDS: Banking, Florida, Legal Barriers Dunlap: Interstate Banking Developments in Florida: Pushing Through Legal Interstate Banking Developments in Florida: Pushing Through Legal Barriers and Toward a Level Playing Field Scott W. Dunlap* I. Introduction The Florida banking market is one of the most coveted in the country.1 The Sunshine State is one of the fastest growing states in the nation,2 and this growth provides increased deposits in the State's' banks. As long as this growth continues, new businesses which need funds to begin operations will be attracted to Florida. In short, the in- flux of people and businesses into the state insure that Florida will re- main a deposit-rich state, requiring large amounts of capital to fund its continued growth. Because banks depend on both obtaining deposits and making loans for their existence, the Florida banking market is quite attractive. Until recently, Florida excluded out-of-state banks and bank hold- ing companies3 from its retail banking market.4 This did not mean that * B.S., University of North Carolina; J.D., University of Florida.