Guardian Media Group Plc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Guardian News & Media

Response to Ofcom consultations on the BBC’s commercial activities and assessing the impact of the BBC’s public service activities About Guardian News & Media Guardian Media Group (GMG), a leading commercial media organisation, is the owner of Guardian News & Media (GNM) which publishes theguardian.com and the Guardian and Observer newspapers. Wholly owned by The Scott Trust Ltd, which exists to secure the financial and editorial independence of the Guardian in perpetuity, GMG is one of the few British-owned newspaper companies and is one of Britain's most successful global digital businesses, with operations in the USA and Australia and a rapidly growing audience around the world. As well as being a leading national quality newspapers, the Guardian and The Observer have championed a highly distinctive, open approach to publishing on the web and have sought global audience growth as a priority. A key consequence of this approach has been a huge growth in global readership, as theguardian.com has grown to become one of the world’s leading quality English language newspaper website in the world, with over 156 million monthly unique browsers. From its roots as a regional news brand, the Guardian now flies the flag for Britain and its media industry on the global stage. Introduction GMG is a strong supporter of the BBC, its core values of public service and its contribution to British public life. GMG supports the fundamentals of the BBC in its current form and a universal service funded through a universal levy, at least for the period covered by the next BBC Charter. -

Annual Report and Accounts 2004

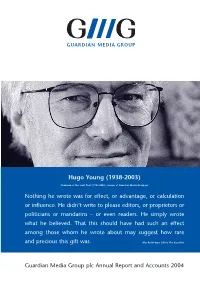

Hugo Young (1938-2003) Chairman of the Scott Trust (1989-2003), owners of Guardian Media Group plc Nothing he wrote was for effect, or advantage, or calculation or influence. He didn’t write to please editors, or proprietors or politicians or mandarins – or even readers. He simply wrote what he believed. That this should have had such an effect among those whom he wrote about may suggest how rare and precious this gift was. Alan Rusbridger, Editor, The Guardian Guardian Media Group plc Annual Report and Accounts 2004 1 Introduction Guardian Media Group plc is a UK media 2 Guardian Media Group plc structure 3 Chairman's statement business with interests in national newspapers, 6 Guardian Media Group plc Board of directors 8 Chief Executive’s review of operations community newspapers, magazines, radio 12 The Scott Trust 14 Corporate social responsibility 18 Financial review and internet businesses. The company is 20 Corporate governance 24 Report of the directors wholly-owned by the Scott Trust. 27 Independent auditors’ report 28 Group profit and loss account 29 Group balance sheet 30 Company balance sheet 31 Group statement of total recognised gains and losses The Scott Trust was created in 1936 to 32 Group cash flow statement 33 Cash flow reconciliations secure the financial and editorial 34 Notes relating to the 2004 financial statements 55 Group five year review independence of the Guardian in perpetuity. 56 Financial advisers Financial highlights 2004 73.5 67.3 634.8 62.1 43.6 526.0 456.4 47.4 36.9 439.0 437.4 29.4 29.8 9.8 1.6 2000 2001 2002 2003 2004 2000 2001 2002 2003 2004 2000 2001 2002 2003 2004 Turnover including share of Total group operating profit Profit before taxation. -

Community Credit in Here Children’S Drawings on Display at the Big Draw Event at the Newsroom

Community credit in here Children’s drawings on display at the Big Draw event at the Newsroom. Photograph: David Levene 40 Living our values It is not only in our editorial coverage that we have an influence over people’s lives. As a company with around 1,500 employees and an ability to tap into a wealth of resources, we are also having a direct impact on the communities we serve. This includes support for schools and journalism projects across the world, as well as HIV projects in Africa The common good The Scott Trust Foundation The range of community activities has become Guardian’s training scheme for young journal- and the War on Terror. One-off workshops also so numerous that we have spent the last year ists in South Africa, the Foundation has run in conjunction with the Newsroom’s rolling putting a more strategic focus on what we do. developed partnerships in some new countries. programme of exhibitions. This has resulted in the creation of the Scott For example, it went to Ukraine to run a sem- The adjoining archive preserves the heritage Trust Foundation, an umbrella organisation for inar on the art of reporting the EU, and invited of our papers and enables others to share our all the activities taking place under the direc- a group of dynamic young Albanians to London history. Researchers can access material rang- tion of our owner, the Scott Trust. to find out about the mechanics of setting up ing from correspondence and photographs to The Scott Trust Foundation’s central remit re- their own newspaper. -

Register of Journalists' Interests

REGISTER OF JOURNALISTS’ INTERESTS (As at 14 June 2019) INTRODUCTION Purpose and Form of the Register Pursuant to a Resolution made by the House of Commons on 17 December 1985, holders of photo- identity passes as lobby journalists accredited to the Parliamentary Press Gallery or for parliamentary broadcasting are required to register: ‘Any occupation or employment for which you receive over £795 from the same source in the course of a calendar year, if that occupation or employment is in any way advantaged by the privileged access to Parliament afforded by your pass.’ Administration and Inspection of the Register The Register is compiled and maintained by the Office of the Parliamentary Commissioner for Standards. Anyone whose details are entered on the Register is required to notify that office of any change in their registrable interests within 28 days of such a change arising. An updated edition of the Register is published approximately every 6 weeks when the House is sitting. Changes to the rules governing the Register are determined by the Committee on Standards in the House of Commons, although where such changes are substantial they are put by the Committee to the House for approval before being implemented. Complaints Complaints, whether from Members, the public or anyone else alleging that a journalist is in breach of the rules governing the Register, should in the first instance be sent to the Registrar of Members’ Financial Interests in the Office of the Parliamentary Commissioner for Standards. Where possible the Registrar will seek to resolve the complaint informally. In more serious cases the Parliamentary Commissioner for Standards may undertake a formal investigation and either rectify the matter or refer it to the Committee on Standards. -

Top Right Group Rebrands to Ascential Monday 14 December

Top Right Group rebrands to Ascential Monday 14 December: Top Right Group today announces it has rebranded its group operations to Ascential: the global provider of exhibitions and festivals and information services for business professionals. Today’s rebrand follows the successful completion of the three year turnaround of the group which began in 2012, and signals a clear purpose for the future of the group which is now focused on two key areas: Exhibitions & Festivals and Information Services. Duncan Painter, CEO, Ascential, said: “We are targeting to become the global leader in large-scale live events and the digital information services industry and our new name and strong brand identity reflects the exciting future we see ahead. “The Top Right Group brand was the right identity for us when our focus was on transforming and turning around our operating companies. Over the past three years, those operating companies have performed well financially and it is now time to move the group brand forward. Our successful new business model provides the confidence that we are stronger as a group than as individual standalone operating companies. “The Ascential name and brand crystallises our constant focus on growing our customers’ success by creating more essential products and services for them, building greater value for our shareholders and an aspirational future for our business.” -Ends- For more information please contact Sarah Kemp on 07738 740 831 or at [email protected] www.ascential.com Notes to Editors Ascential informs and connects business professionals in 150 countries through market-leading Exhibitions and Festivals, and Information Services. -

New News, Future News the Challenges for Television News After Digital Switch-Over

New News, Future News The challenges for television news after Digital Switch-over An Ofcom discussion document Publication date: 26 June 2007 Foreword The prospects for television news in a fully digital era are a central element in any consideration of the future of public service broadcasting (PSB). News is regarded by viewers as the most important of all the PSB genres, and television remains by far the most used source of news for UK citizens. The role of news and information as part of the democratic process is long established, and its status is specifically underpinned in the Communications Act 2003. This report, New News, Future News, is one of a series of Ofcom studies focussing on individual topics identified in the PSB Review of 2004/05, and further discussed in the Digital PSB report of July 2006. The others are on the provision of children’s programmes and on the prospects for a Public Service Publisher. All three studies are linked to areas of particular PSB concern for the future, and set out a framework for policy consideration ahead of the next full PSB review. Other Ofcom work of relevance includes the review of Channel 4’s funding. It has not been the role of this report to come up with solutions, and no policy recommendations are put forward. Instead, the report examines the environment in which television news currently operates, and assesses how that may change in future (after digital switch-over and, in 2014, the expiry of current Channel 3 and Channel 5 licences) . It identifies particular issues that will need to be addressed and suggests some specific questions that may need to be answered. -

Florida State University Libraries

Florida State University Libraries Electronic Theses, Treatises and Dissertations The Graduate School You Belong among the Wildlowers... Unless You're an Instagrammer: The Political Economy of the Instagram Effect iMnich etlhle Gera Nce Perewsleys Follow this and additional works at the DigiNole: FSU's Digital Repository. For more information, please contact [email protected] FLORIDA STATE UNIVERSITY COLLEGE OF COMMUNICATION AND INFORMATION YOU BELONG AMONG THE WILDFLOWERS... UNLESS YOU’RE AN INSTAGRAMMER: THE POLITICAL ECONOMY OF THE INSTAGRAM EFFECT IN THE NEWS By MICHELLE PRESLEY A Thesis submitted to the School of Communication in fulfillment of the requirements for the degree of Master of Arts 2020 Michelle Presley defended this thesis on April 6, 2020. The members of the supervisory committee were: Jennifer Proffitt Professor Directing Thesis Andy Opel Committee Member Brian Graves Committee Member The Graduate School has verified and approved the above-named committee members, and certifies that the thesis has been approved in accordance with university requirements. ii For my husband, Troy. And for those vast, quiet corners of the world, the wildernesses large and small, that I have had the privilege of exploring. From the salty mangroves of my Florida home to the pinon forests of my beloved high desert, these wild slices have had a hand in shaping everything I am. To these lands and the indigenous hands that have cared for them since time immemorial – thank you from the bottom of my heart. iii ACKNOWLEDGMENTS Words cannot express my gratitude for the mentorship of Dr. Jennifer Proffitt. This project would not have been possible without her feedback and guidance and I am so thankful for her support throughout writing this thesis and in my master’s career. -

Global Entertainment & Media Outlook 2018 –2022

Perspectives from the Global Entertainment & Media Outlook 2018–2022 Trending now: convergence, connections and trust www.pwc.com/outlook PwcOutlook18_042718_lj_FC-17-se_lj-ej_lj.indd 1 4/27/18 4:59 PM About this report Welcome to this year’s special report on when faith in many industries is at an the findings of our Global Entertainment historically low ebb and regulators are & Media Outlook. Every year we take a targeting media businesses’ use of data, deep dive into the data and analysis that the ability to build and sustain consumer our team of researchers and industry trust is becoming a vital differentiator. specialists have unearthed – with the aim of providing fresh perspectives and The result? To succeed in the future actionable insights. that’s taking shape, companies must reenvision every aspect of what they do Our comprehensive data and projections and how they do it. It’s about having, or on the 15 defined segments across 53 having access to, the right technology territories are just the start in creating and excellent content, which is delivered these insights. As in previous years, in a cost-effective manner to an engaged Ennèl van Eeden our authors have blended the data with audience that trusts the brand. For their own observations, experiences and those able to execute successfully, the examples to turn raw information into opportunities are legion. true intelligence. Writing this report was an exciting What’s trending now? It’s clear we’re in a and energising experience – and we rapidly evolving media ecosystem that’s hope these qualities shine through. -

CAPSTONE 19-4 Indo-Pacific Field Study

CAPSTONE 19-4 Indo-Pacific Field Study Subject Page Combatant Command ................................................ 3 New Zealand .............................................................. 53 India ........................................................................... 123 China .......................................................................... 189 National Security Strategy .......................................... 267 National Defense Strategy ......................................... 319 Charting a Course, Chapter 9 (Asia Pacific) .............. 333 1 This page intentionally blank 2 U.S. INDO-PACIFIC Command Subject Page Admiral Philip S. Davidson ....................................... 4 USINDOPACOM History .......................................... 7 USINDOPACOM AOR ............................................. 9 2019 Posture Statement .......................................... 11 3 Commander, U.S. Indo-Pacific Command Admiral Philip S. Davidson, U.S. Navy Photos Admiral Philip S. Davidson (Photo by File Photo) Adm. Phil Davidson is the 25th Commander of United States Indo-Pacific Command (USINDOPACOM), America’s oldest and largest military combatant command, based in Hawai’i. USINDOPACOM includes 380,000 Soldiers, Sailors, Marines, Airmen, Coast Guardsmen and Department of Defense civilians and is responsible for all U.S. military activities in the Indo-Pacific, covering 36 nations, 14 time zones, and more than 50 percent of the world’s population. Prior to becoming CDRUSINDOPACOM on May 30, 2018, he served as -

By Global Radio

Annexes to the report on the Global Radio/GMG Radio public interest test Report on public interest test on the acquisition of Guardian Media Group’s radio stations (Real and Smooth) by Global Radio ANNEXES 0 Annexes to the report on the Global Radio/GMG Radio public interest test Contents 1 Annex 1: Glossary Annex 2: Summary of stakeholder representations 2 Annex 3: Information received from OFT Annex 4: Area by area analysis 1 Annexes to the report on the Global Radio/GMG Radio public interest test Annex 1 3 Glossary BARB Broadcasters Audience Research Board. The pan-industry body that measures television viewing. Broadband A service or connection generally defined as being ‘always on’ and providing a bandwidth greater than narrowband. Communications Act Communications Act 2003, which came into force in July 2003. ‘Connected’ TV A television that is broadband-enabled to allow viewers to access internet content. DAB Digital audio broadcasting. A set of internationally-accepted standards for the technology by which terrestrial digital radio multiplex services are broadcast in the UK. DCMS Department for Culture, Media and Sport Digital switchover The process of switching over the analogue television or radio broadcasting system to digital. DTT Digital terrestrial television. The television technology that carries the Freeview service. First-run acquisitions A ready-made programme bought by a broadcaster from another rights holder and broadcast for the first time in the UK during the reference year. First-run originations Programmes commissioned by or for a licensed public service channel with a view to their first showing on television in the United Kingdom in the reference year. -

Guardian Media Group Sensitive

Guardian Media Group Certified B Corporation SCORE COMPLETION VERSION YEAR SECTOR SIZE 86.2 100% 6 2019 Service 1000+ As wholly-owned subsidiary of Scott Trust Limited, The Guardian is required to make it's full B Impact Assessment transparent. The PDF contains a completed B Impact Assesment that has been reviewed by B Lab with The Guardian as part of their certification as a B Corporation. Answers to questions that would reveal sensitive information (e.g. that would advantage competitors or prejudice litigation) are covered as such: / Governance Mission & Engagement Level of Impact Focus Describe your company's approach to creating positive impact. This is an unweighted question that will not impact your score and is asked only for research/benchmarking purposes. Creating positive social or environmental impact is not a focus for our business We occasionally think about the social and environmental impact of some aspects of our business, but not frequently. We frequently consider our social and environmental impact, but it isn't a high priority in decision-making. We consistently incorporate social and environmental impact into decision-making because we consider it important to the success and profitability of our business. We treat our social and environmental impact as a primary measure of success for our business and prioritize it even in cases where it may not drive profitability. Points Available: 0.00 Mission Statement Characteristics Does your company's formal, written corporate mission statement include any of the following? A formal written corporate mission statement is one that is either publicly facing or formally shared with the employees of the company. -

Guardian Media Group PLC's

CONFIDENTIAL GMG RESPONSE TO CMA STATEMENT OF SCOPE - DIGITAL ADVERTISING MARKET STUDY CONFIDENTIAL VERSION About Guardian Media Group PLC (GMG) GMG is one of the UK’s leading commercial media organisations and a British-owned, independent, news media business. GMG owns Guardian News & Media (GNM), the publisher of theguardian.com website and the Guardian and Observer newspapers. It is known for its globally acclaimed investigations, including investigating the Paradise Papers and Panama Papers and Cambridge Analytica. As well as being the UK’s largest quality news brand, the Guardian and Observer have pioneered a highly distinctive, open approach to publishing on the web and their website has achieved significant global audience growth over the past 20 years. Our endowment fund and portfolio of other holdings exist to support the Guardian’s journalism by providing financial returns. As the CMA may be aware, The Guardian’s unique structure and trust model means that our owner - the Scott Trust - takes no dividend from the business. This means that any revenue generated by GNM is reinvested back into funding more high-quality public interest Guardian journalism. Introduction GMG welcomes the opportunity to respond to the CMA statement of scope and wider work to examine competition in digital markets. The digital economy underpins and impacts almost every sector of the UK and global economy in some way. Ensuring that there is fair and effective competition in the supply of key products such as digital advertising, and digital payment services