General Stationery Template

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

INET to Join NASDAQ's Supermontage New York, NY— Instinet ECN And

INET to join NASDAQ's SuperMontage New York, NY— Instinet ECN and Island ECN, soon to be combined into one electronic marketplace branded INET, today announced plans to participate in NASDAQ's SuperMontage. INET will begin displaying orders on SuperMontage in January following the consolidation of the Island ECN and Instinet ECN. "We are committed to exposing our customers' orders to as much liquidity as possible and improving the marketplace for all investors," said Alex Goor, executive vice president, head of Alternative Trading Systems, Instinet Corporation. "As a result of NASDAQ's recent proposed rule changes, we expect that participation in SuperMontage will benefit our subscribers." "With Instinet's participation, SuperMontage offers a deeper pool of liquidity for NASDAQ market participants and ultimately, enhanced opportunity for best execution," said Chris Concannon, executive vice president of The NASDAQ Stock Market. "SuperMontage was designed to provide a highly transparent, highly liquid venue where multiple parties -- and competing market models -- can come together to yield the best outcome for investors." Separately, NASDAQ announced that it intends to use Instinet SmartRouter technology to provide its members with access to enhanced routing services. Instinet SmartRouter integrates liquidity pools including all major ECNs through its order routing algorithm. "NASDAQ is pleased to announce that it intends to partner with INET to make available Instinet's enhanced order-routing technology to NASDAQ's SuperMontage participants," Concannon added. Instinet ECN and Island ECN, soon to be combined into one electronic marketplace branded INET, will comprise one of the largest liquidity pools in U.S. over-the-counter securities. -

Filing for SEC Rule

Rule 606 Quarterly Report Instinet, LLC 309 West 49th Street New York, NY 10019 Disclosure of Order Routing Information – SEC Rule 606 for Quarter Ending on June 28 2019 In accordance with Securities and Exchange Commission (“SEC”) requirements, Instinet, LLC (“Instinet” or the “Firm”), is publishing statistical information about its routing of certain customers’ orders in NMS Securities and Listed Options. SEC rules require all registered broker- dealers that route orders in certain equity and option securities to make publicly available quarterly reports that present a general overview of a firm’s non-directed order routing practices. Non-directed orders are orders that the customer has not instructed to route to a particular venue for execution. For these non-directed orders, the Firm has selected the execution venue on behalf of its customers. Please note that consistent with the SEC’s requirements, these statistics capture only a portion of Instinet's order flow. This report is intended to provide an overview of Instinet’s order routing practices, and does not create a reliable basis on which to assess whether Instinet or any other trading venue, to which we route orders, has satisfied its duty of best execution. Decisions concerning whether to open an account or direct orders to the Firm should not be established on the information presented in this report alone, but on a broader evaluation of the full range of services and products Instinet provides. This report is divided into four sections: 1. Securities listed on the New York Stock Exchange, LLC and reported as Network A eligible securities; 2. -

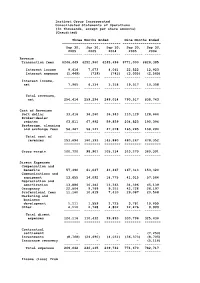

Instinet Group Incorporated Consolidated Statements of Operations (In Thousands, Except Per Share Amounts) (Unaudited)

Instinet Group Incorporated Consolidated Statements of Operations (In thousands, except per share amounts) (Unaudited) Three Months Ended Nine Months Ended ----------------------------- ------------------- Sep 30, Jun 30, Sep 30, Sep 30, Sep 30, 2005 2005 2004 2005 2004 --------- --------- -------- --------- -------- Revenue Transaction fees $246,449 $252,960 $245,696 $771,000 $828,385 Interest income 9,414 7,073 4,061 22,522 12,923 Interest expense (1,449) (739) (743) (3,005) (2,565) -------- -------- -------- -------- -------- Interest income, net 7,965 6,334 3,318 19,517 10,358 -------- -------- -------- -------- -------- Total revenues, net 254,414 259,294 249,014 790,517 838,743 -------- -------- -------- -------- -------- Cost of Revenues Soft dollar 33,416 36,260 36,943 110,129 128,664 Broker-dealer rebates 63,811 67,992 59,859 204,823 190,394 Brokerage, clearing and exchange fees 56,467 56,141 47,078 165,295 159,294 -------- -------- -------- -------- -------- Total cost of revenues 153,694 160,393 143,880 480,247 478,352 -------- -------- -------- -------- -------- Gross margin 100,720 98,901 105,134 310,270 360,391 -------- -------- -------- -------- -------- Direct Expenses Compensation and benefits 57,390 61,047 43,467 167,313 153,320 Communications and equipment 13,655 14,092 18,775 41,015 57,564 Depreciation and amortization 13,886 10,382 13,363 34,396 45,139 Occupancy 22,804 9,769 9,351 42,728 28,197 Professional fees 11,160 10,815 7,410 29,087 20,568 Marketing and business development 1,111 1,559 2,725 3,781 10,655 Other -

Instinet Group Incorporated Second Quarter 2005 Earnings ______Conference Call Transcript July 22, 2005

Instinet Group Incorporated Second Quarter 2005 Earnings _____________________________________________________ Conference Call Transcript July 22, 2005 CORPORATE PARTICIPANTS Lisa Kampf Instinet Group - Investor Relations Ed Nicoll Instinet Group - CEO John F. Fay Instinet Group – Co-President and CFO CONFERENCE CALL PARTICIPANTS Alex Kremm Lehman Brothers - Analyst Daniel Goldberg Bear Stearns – Analyst Charlotte Chamberlain Jeffries & Company – Analyst ___________________________________________________________________________________________________________ Instinet Group Incorporated. 2Q05 Earnings Call 1 Operator: Good morning ladies and gentlemen. This is the operator. Today’s conference is scheduled to begin momentarily. Until that time, your lines will again be placed on music hold. Thank you for your patience. Good morning. My name is Cynthia and I will be your conference facilitator. At this time I would like to welcome everyone to the Instinet Group, Incorporated Second Quarter 2005 Earnings conference call. All lines have been placed on mute to prevent any background noise. After the speaker’s remarks there will be a question and answer period. If you would like to ask a question during this time, simply press star then the number 1 on your telephone keypad. If you would like to withdraw your question, press star then the number 2. I would now like to turn the conference over to Lisa Kampf, Investor Relations Officer. Ma’am, you may begin your conference. Lisa Kampf: Good morning and welcome to the Instinet Group conference call to discuss results for the second quarter of 2005. During this conference call we may make statements that are forward looking in nature. Our actual results may be materially different from the results anticipated in those statements. -

Wall Street's New Alchemist Buyout Specialist Glenn Hutchins Is Behind Discount Brokerage and Electronic Exchange Deals That Could Reshape Stock Trading

Close Window AUGUST 8, 2005 FINANCE Wall Street's New Alchemist Buyout specialist Glenn Hutchins is behind discount brokerage and electronic exchange deals that could reshape stock trading Directors of Sungard Data Systems Inc. sat around a conference table on Mar. 22 at a midtown Manhattan law firm and listened to some bad news. A consortium of seven private-equity firms had been pursuing a buyout of SunGard, which processes transactions for Wall Street firms, for four months. Now five of them were balking at the price. The lead firm, Silver Lake Partners, had agreed to the amount but needed more time to convince co-investors. But James L. Mann, SunGard's 70-year-old chairman and a former bomber pilot, is not one to haggle. Mann and the board delivered an ultimatum: accept the price within 48 hours, or the deal is off. The same day, Silver Lake co-founder and managing director Glenn H. Hutchins began working the phone. Compared with the other consortium members, which included Kohlberg Kravis Roberts & Co. and the Blackstone Group, the $5.8 billion Silver Lake was small fry. Still, Hutchins could draw on 20 years of relationships in private equity. By the deadline, only two original consortium members, Thomas H. Lee Co. and the Carlyle Group, had dropped out and Silver Lake had helped persuade Goldman Sachs Group Inc. (GS ) and Providence Equity Partners Inc. to replace them. "It's a tribute to the credibility that Glenn has in the sector that people wanted to be partners with him," says Jane Wheeler, senior managing director at New York investment bank Evercore Partners Inc. -

Instinet's Trading Floor Features Yahoo! Financevision Live

Instinet's Trading Floor Features Yahoo! FinanceVision Live Instinet Research Analysts to Provide Live Pre- and Post-Market Analysis Twice Daily on Yahoo! FinanceVision NEW YORK, February 1, 2001 -- Instinet Corporation, a wholly-owned subsidiary of Reuters Group PLC (Nasdaq: RTRSY) and the eFinancial Marketplace offering equities trading, research, fixed income trading, and clearing and settlement services, today extended its relationship with Yahoo! Inc. (Nasdaq: YHOO), a global Internet communications, commerce and media company. Instinet Research analysts will provide live market analysis, twice daily, from the Instinet trading floor to Yahoo!® FinanceVision (http://financevision.yahoo.com). Yahoo! FinanceVision will broadcast from Instinet's trading floor at regularly scheduled time slots, once before 9:30 a.m. (EST) and once after 4:00 p.m. (EST). Instinet Research analysts will provide Yahoo! viewers with pre- and post- market analysis. To date, this information has not been widely available to the public from Instinet or any other broker. Presently, on the Instinet trading floor, CNBC and CNN hold daily broadcasts, with their respective reporters commenting on market conditions and movements pre-, post- and during market hours. In September 2000, Instinet signed an agreement with Yahoo! to provide Instinet top of book and last sale trade data on Yahoo! Finance, the Web's No. 1 finance site. Commenting on today's deal, John Oddie, CEO, Global Equities, Instinet Corporation said, "Instinet's expanded relationship with Yahoo! demonstrates our continued efforts to provide investors with unique and valuable market data that was previously available to institutional investors only, via various distribution points. Our skilled analysts have access to information that enables them to highlight specific stock trends and analyze market direction. -

Destinations of Choice Mapping the New Equity Trading Landscape Opening up the Market

Market Commentary & Insights Destinations of Choice Mapping the New Equity Trading Landscape Opening Up the Market MiFID II is transforming the European equity For a buy-side firm, the trading options are trading landscape, resulting in unprecedented not limited to traditional multilateral venues choice for participants. To remain competitive, such as dark pools operating within central buy-side firms looking to optimise order limit order books (“CLOBs”). Indeed, bilateral performance and meet more stringent best protocols such as SIs and requests-for-quote execution requirements need to be aware (“RFQs”), as well as the increasing use of of the growing range of options now at their conditional trading via Indications of Interest disposal. (“IOIs”), are at the forefront of this new, more open marketplace. The choices start with selecting the optimal type of venue: should your order be routed to Broker dealers also have a choice to make, a Regulated Market (“RM”) or a multilateral as they cannot run an MTF and an SI within trading facility (“MTF”)—regulated the same legal entity. trading venues required to provide non- discriminatory access—or, directly to a AROUND THE BLOCK Systematic Internaliser (“SI”)? RMs and MTFs are able to cross buyers and sellers and may The diversification in trading choices responds benefit from pre-trade transparency waivers. to a clear (though not necessarily loud) SIs, on the other hand, must trade on risk investor need. Buy-side firms, especially the but benefit from being able to price improve larger ones, have an ongoing requirement to relative to their published quotes as well as efficiently and quietly manage trillions of euros keep their quotes private when they deal above in assets. -

THE NASDAQ STOCK MARKET LLC NOTICE of ACCEPTANCE of AWC Certified, Return Receipt Requested TO: Instinet, LLC Mr. Faron Webb

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF AWC Certified, Return Receipt Requested TO: Instinet, LLC Mr. Faron Webb General Counsel Worldwide Plaza 309 West 49th Street New York, NY 10019 FROM: The NASDAQ Stock Market LLC ("Nasdaq") do Financial Industry Regulatory Authority ("FINRA") Department of Enforcement 9509 Key West Avenue Rockville, MD 20850 DATE: April 11, 2018 RE: Notice of Acceptance of Letter of Acceptance, Waiver and Consent No. 20130368360-01 Please be advised that your above-referenced Letter of Acceptance, Waiver and Consent ("AWC") has been accepted on April 11, 2018 by the Nasdaq Review Council's Review Subcommittee, or by the Office of Disciplinary Affairs on behalf of the Nasdaq Review Council, pursuant to Nasdaq Rule 9216. A copy of the AWC is enclosed herewith. You are again reminded of your obligation, if currently registered, immediately to update your Uniform Application for Broker-Dealer Registration ("Form BD") to reflect the conclusion of this disciplinary action. Additionally, you must also notify FINRA (or NASDAQ if you are not a member of FINRA) in writing of any change of address or other changes required to be made to your Form BD. You are reminded that Section I of the attached Letter of Acceptance, Waiver, and Consent includes an undertaking. In accordance with the terms of the AWC, a registered principal of the firm is required to notify the Compliance Assistant, Department of Enforcement, 9509 Key West Avenue, Rockville, MD 20850, of completion of the undertaking. You will be notified by the Registration and Disclosure Department regarding sanctions if a suspension has been imposed and by NASDAQ's Finance Department regarding the payment of any fine if a fine has been imposed. -

Bank of America Merrill Lynch ITG Nicholas Demaria Sean Klinkowize Peter Wilson Qbeats KCG Beth Hamburger David Lavalle State Street Global Advisors

2016 Events 80th Annual Conference and Dinner Three Sixty° | 10 Desbrosses Street | New York, NY Thursday April 7, 2016 2016 Golf Classic & John Harrington Cup Tournament Canoe Brook Country Club | Summit, NJ Monday July 25, 2016 26th Annual International Reception 80The Bryant Park Grill | New York, NY Thursday November 10, 2016 Kimberly Unger Chief Executive Officer [email protected] 212.344.0410 www.stany.org - 1 - Security Traders Association of New York Table of Contents 4 STANY BOARD OF DIRECTORS 6 STANY PRESIDENT’S WELCOME LETTER 8 STA PRESIDENT’S WELCOME LETTER 10 2015 SPONSORS THANK YOU 12 2016 SPONSORS 14 2016 CONFERENCE SCHEDULE COMpany PROFILES 16 Diamond Sponsor 16 Platinum Sponsors 18 Gold Sponsors 20 Silver Sponsors 22 Bronze Sponsors 30 Additional Sponsors 3RD AnnuaL HONORS 32 Lifetime Achievement and Dedication to STANY Award 34 Outstanding Contribution to Industry Award 36 EVENT PHOTOS 70 2016 STANY ATTENDEES 80 2016 STANY MEMBERSHIP DIRECTOry 88 2016 RETIRED AND HONOrary MEMBERS 89 ADVertisiMENT INDEX - 3 - Security Traders Association of New York Board of Directors 2016 OFFICERS President CHUCK LUGAY Citadel Securities First Vice President MICHAEL MODESKI OTC Markets Group Second Vice President BARRY HICKMAN Pershing Secretary PATRICIA KOETZNER Siebert, Brandford, Shank & Co. Treasurer RON HOOEY BNY Mellon Capital Markets Past President LISA M. UTASI ClearBridge Investments CEO/Executive Director KIMBERLY UNGER, Esq. STANY DIRECTORS Peter Cocuzza James Hyde Daniel Strack Global Liquidity Partners NYSE/ISE Goldman Sachs Jeffrey Cooper Adam Inzirillo Dan Weingarten FIS Global Bank of America Merrill Lynch ITG Nicholas DeMaria Sean Klinkowize Peter Wilson qbeats KCG Beth Hamburger David LaValle State Street Global Advisors CONSULTANTS Tom Jordan Bill Karsh Kevin Sweeney Jordan & Jordan National Stock Exchange Societe Generale Stephen Kay Stephen Nelson, Esq. -

Press Release Nasdaq to Acquire Chi-X Canada

Press Release Nasdaq to Acquire Chi-X Canada Expands Equity Trading Beyond U.S. and Nordics NEW YORK, December 8, 2015 – Nasdaq (Nasdaq: NDAQ) today announced that it will acquire Chi-X Canada, an Alternative Trading System for Toronto Stock Exchange (TSX) and TSX Venture Securities, from Chi-X Global. The acquisition will provide Nasdaq with direct access to the Canadian equities market. The deal is expected to close in the first quarter of 2016, and be accretive to the company's earnings at closing, excluding transaction-related costs. “This acquisition is an important part of our North American strategy as Chi-X handles about 22% of the order flow of S&P/TSX Composite securities in Canada,” said Hans-Ole Jochumsen, President, Nasdaq. “The addition of these thriving marketplaces will create a powerful combination for investors.” The deal will expand Nasdaq’s North American equities trading business beyond the U.S., where Nasdaq currently operates multiple trading venues in cash equities, options, commodities, fixed income and other financial instruments. The acquisition will ultimately enhance the trading experience for customers by promoting greater uniformity in technology and functionality across U.S. and Canadian trading venues. “Nasdaq and Chi-X Canada have both demonstrated their commitment to market innovation and efficiency,” said Tal Cohen, CEO of Chi-X Global. “We believe Nasdaq is well positioned to enhance Chi-X Canada’s current capabilities and to capitalize on new product and asset class opportunities, while maintaining Chi-X Canada’s core values of cost-effective and client-driven solutions.” Chi-X Canada’s two platforms, Chi-X Canada and CX2, are the only equity trading venues in Canada to offer fully-customizable smart order routing to all market centers, and offer two trading models: post- trade attribution and advanced order types. -

Reuters Subsidiary Instinet Files for IPO

Reuters Subsidiary Instinet Files for IPO February 8, 2001 London – Reuters, the global information, news and technology group, announced today that Instinet, its wholly owned electronic brokerage subsidiary, has filed a Registration Statement with the US Securities and Exchange Commission for a proposed initial public offering (IPO). Instinet intends to apply for quotation of its common stock on the Nasdaq National Market. It is expected that the IPO will be completed by the middle of 2001. This will be a primary offering of common stock all of which will be issued by Instinet. Following the IPO, Reuters will continue to own a substantial majority of Instinet's common stock. Instinet is the world's largest electronic agency securities broker, trading in 40 securities markets, with membership of 20 exchanges throughout North America, Europe, and Asia. It is headquartered in New York and has eight other global offices. Founded in 1969, Instinet was acquired by Reuters in 1987 and has grown substantially under Reuters ownership in both US and international securities markets. Reuters announced in February last year that an IPO was a strategic option under consideration for Instinet. In October the Group confirmed that it would proceed with plans for an IPO. Peter Job, Reuters Chief Executive, said: "A public listing is a natural evolution for Instinet. Reuters believes that backing an independent Instinet whilst remaining a substantial shareholder is the best way forward for Reuters shareholders." A registration statement relating to these securities has been filed with the Securities and Exchange Commission but has not yet become effective. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. -

Instinet, LLC and INET ATS, Inc.; Release No. 34-52623

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES EXCHANGE ACT OF 1934 Release No. 52623 / October 18, 2005 ADMINISTRATIVE PROCEEDING File No. 3-12088 ORDER INSTITUTING ADMINISTRATIVE In the Matter of AND CEASE-AND-DESIST PROCEEDINGS, MAKING FINDINGS, AND IMPOSING Instinet, LLC and INET ATS, REMEDIAL SANCTIONS AND A Inc. CEASE-AND-DESIST ORDER PURSUANT TO SECTIONS 15(b) AND 21C OF THE Respondents. SECURITIES EXCHANGE ACT OF 1934 I. The Securities and Exchange Commission (“Commission” or “SEC”) deems it appropriate and in the public interest that administrative and cease-and-desist proceedings be, and hereby are, instituted pursuant to Sections 15(b) and 21C of the Securities Exchange Act of 1934 (“Exchange Act”), against Instinet, LLC (“INCA”) and INET ATS, Inc. (“INET”), f/k/a the Island ECN, Inc. (“ISLD”). II. In anticipation of the institution of these proceedings, Respondents have submitted Offers of Settlements (the “Offers”) which the Commission has determined to accept. Solely for the purpose of these proceedings and any other proceedings brought by or on behalf of the Commission, or in which the Commission is a party, and without admitting or denying the findings contained herein, except as to the Commission’s jurisdiction over Respondents and the subject matter of these proceedings, which are admitted, Respondents consent to the entry of this Order Instituting Administrative and Cease-and-Desist Proceedings, Making Findings, and Imposing Remedial Sanctions and a Cease-and-Desist Order Pursuant to Sections 15(b) and 21C of the Securities Exchange Act of 1934 (“Order”), as set forth below. III.