China's Overseas Investments in Oil and Gas Production

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2015 Annual Report Mission

2015 annual report Mission Our mission is to facilitate innovation, collaborative research and technology development, demonstration and deployment for a responsible Canadian hydrocarbon energy industry. 2 Vision Our vision is to help Canada become a global hydrocarbon energy technology leader. PTAC Technology Areas Manage Environmental Impacts • Air Quality • Alternative Energy Improve Oil and Gas Recovery • Ecological • CO2 Enhanced Hydrocarbon Recovery • Emission Reduction / Eco-Efficiency • Coalbed Methane, Shale Gas, Tight Gas, Gas Hydrates, • Energy Efficiency and other Unconventional Gas • Resource Access • Conventional Heavy Oil, Cold Heavy Oil Production with • Soil and Groundwater Sands • Water • Conventional Oil and Gas Recovery • Wellsite Abandonment • Development of Arctic Resources • Development of Remote Resources Additional PTAC Technical Areas • Enhanced Heavy Oil Recovery • e-Business • Enhanced Oil and Gas Recovery • Genomics • Enhanced Oil Sands Recovery • Geomatics • Emerging Technologies to Recover Oil Sands from Deposits • Geosciences with Existing Zero Recovery • Health and Safety • Tight Oil, Shale Oil, and other Unconventional Oil • Instrumentation/Measurement • Nano Technology Reduce Capital, Operating, and G&A Costs • Operations • Automation • Photonics • Capital Cost Optimization • Production Engineering • Cost Reduction Using Emerging Drilling and Completion • Remote Sensing Technologies • Reservoir Engineering • Cost Reduction Using Surface Facilities • Security • Eco-Efficiency and Energy Efficiencyechnologies -

Case M.9837 — BP/Sinopec Fuel Oil Sales/BP Sinopec Marine Fuels) Candidate Case for Simplified Procedure

C 6/16 EN Offi cial Jour nal of the European Union 8.1.2021 Prior notification of a concentration (Case M.9837 — BP/Sinopec Fuel Oil Sales/BP Sinopec Marine Fuels) Candidate case for simplified procedure (Text with EEA relevance) (2021/C 6/13) 1. On 22 December 2020, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (1). This notification concerns the following undertakings: — BP Plc. (United Kingdom), — Sinopec Fuel Oil Sales Co. Ltd (People’s Republic of China), controlled by China Petrochemical Corporation (People’s Republic of China), — BP Sinopec Marine Fuels Pte. Ltd. BP Plc. and Sinopec Fuel Oil Sales Co. Ltd acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of BP Sinopec Marine Fuels Pte. Ltd. The concentration is accomplished by way of contract. 2. The business activities of the undertakings concerned are: — for BP Plc.: exploration, production and marketing of crude oil and natural gas; refining, marketing, supply and transportation of petroleum products; production and supply of petrochemicals and related products; and supply of alternative energy, — for Sinopec Fuel Oil Sales Co. Ltd: providing oil products and service to domestic and international trading vessels, — BP Sinopec Marine Fuels Pte. Ltd: wholesale and retail supply of bunker fuels in Europe, Asia and the Middle East. 3. On preliminary examination, the Commission finds that the notified transaction could fall within the scope of the Merger Regulation. However, the final decision on this point is reserved. Pursuant to the Commission Notice on a simplified procedure for treatment of certain concentrations under the Council Regulation (EC) No 139/2004 (2) it should be noted that this case is a candidate for treatment under the procedure set out in the Notice. -

Q3 2020 Husky-MDA

MANAGEMENT’S DISCUSSION AND ANALYSIS October 29, 2020 Table of Contents 1.0 Summary of Quarterly Results 2.0 Business Overview 3.0 Business Environment 4.0 Results of Operations 5.0 Risk Management and Financial Risks 6.0 Liquidity and Capital Resources 7.0 Critical Accounting Estimates and Key Judgments 8.0 Recent Accounting Standards and Changes in Accounting Policies 9.0 Outstanding Share Data 10.0 Reader Advisories 1.0 Summary of Quarterly Results Three months ended Quarterly Summary Sep. 30 Jun. 30 Mar. 31 Dec. 31 Sept. 30 Jun. 30 Mar. 31 Dec. 31 ($ millions, except where indicated) 2020 2020 2020 2019 2019 2019 2019 2018(1) Production (mboe/day) 258.4 246.5 298.9 311.3 294.8 268.4 285.2 304.3 Throughput (mbbls/day) 300.1 281.3 307.8 203.4 356.4 340.3 333.6 286.9 Gross revenues and Marketing and other(1) 3,379 2,408 4,113 4,921 5,373 5,321 4,610 5,042 Net earnings (loss) (7,081) (304) (1,705) (2,341) 273 370 328 216 Per share – Basic (7.05) (0.31) (1.71) (2.34) 0.26 0.36 0.32 0.21 Per share – Diluted (7.06) (0.31) (1.71) (2.34) 0.25 0.36 0.31 0.16 Cash flow – operating activities 79 (10) 355 866 800 760 545 1,313 Funds from operations(2) 148 18 25 469 1,021 802 959 583 Per share – Basic 0.15 0.02 0.02 0.47 1.02 0.80 0.95 0.58 Per share – Diluted 0.15 0.02 0.02 0.47 1.02 0.80 0.95 0.58 (1) Gross revenues and Marketing and other results reported for 2019 have been recast to reflect a change in reclassification of intersegment sales eliminations and a change in presentation of the Integrated Corridor and Offshore business units. -

Suncor Q3 2020 Investor Relations Supplemental Information Package

SUNCOR ENERGY Investor Information SUPPLEMENTAL Published October 28, 2020 SUNCOR ENERGY Table of Contents 1. Energy Sources 2. Processing, Infrastructure & Logistics 3. Consumer Channels 4. Sustainability 5. Technology Development 6. Integrated Model Calculation 7. Glossary SUNCOR ENERGY 2 SUNCOR ENERGY EnergyAppendix Sources 3 202003- 038 Oil Sands Energy Sources *All values net to Suncor In Situ Mining Firebag Base Plant 215,000 bpd capacity 350,000 bpd capacity Suncor WI 100% Suncor WI 100% 2,603 mmbbls 2P reserves1 1,350 mmbbls 2P reserves1 Note: Millennium and North Steepank Mines do not supply full 350,000 bpd of capacity as significant in-situ volumes are sent through Base Plant MacKay River Syncrude 38,000 bpd capacity Syncrude operated Suncor WI 100% 205,600 bpd net coking capacity 501 mmbbls 2P reserves1 Suncor WI 58.74% 1,217 mmbbls 2P reserves1 Future opportunities Fort Hills ES-SAGD Firebag Expansion Suncor operated Lewis (SU WI 100%) 105,000 bpd net capacity Meadow Creek (SU WI 75%) Suncor WI 54.11% 1,365 mmbbls 2P reserves1 First oil achieved in January 2018 SUNCOR ENERGY 1 See Slide Notes and Advisories. 4 1 Regional synergy opportunities for existing assets Crude logistics Upgrader feedstock optionality from multiple oil sands assets Crude feedstock optionality for Edmonton refinery Supply chain Sparing, warehousing & supply chain management Consolidation of regional contracts (lodging, busing, flights, etc.) Operational optimizations Unplanned outage impact mitigations In Situ Turnaround planning optimization Process -

Patronage of Vladimir Putin

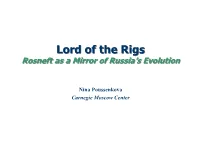

LLorord of the d of the RiRigsgs RosRosnenefftt a as s a a MMiirrrror oor off Rus Russisia’sa’s Ev Evololututiionon Nina Poussenkova Carnegie Moscow Center PortPortrraiaitt of of RosneRosneft ft E&P Refining Marketing Projects Yuganskneftegas Komsomolsk Purneftegas Altainefteproduct Sakhalin 3, 4, 5 Sakhalinmorneftegas Tuapse Kurgannefteproduct Vankor block of fields Severnaya Neft Yamalnefteproduct West Kamchatka shelf Polar Lights Nakhodkanefteproduct Black and Azov Seas Sakhalin1 Vostoknefteproduct Kazakhstan Vankorneft Arkhangelsknefteproduct Algiers Krasnodarneftegas Murmansknefteproduct CPC Stavropolneftegas Smolensknefteproduct VostochnoSugdinsk block Grozneft Artag Verkhnechonsk KabardinoBalkar Fuel Co Neftegas Karachayevo Udmurtneft Cherkessknefteproduct Kubannefteproduct Tuapsenefteproduct Stavropoliye ExYuganskneftegas: 2004 oil production (21 mt) – 4.7% of Russia’s total CEO – S.Bogdanchikov BoD Chairman – I.Sechin Proved oil reserves – 4.8% of Russia’s total With Yuganskneftegas: > 75% owned by the state Rosneftegas 2006 oil production (75 mt) – 15% of Russia’s total 9.44% YUKOS >14% sold during IPO Proved oil reserves – 20% of Russia’s total RoRosnesneftft’s’s Saga Saga 1985 1990 1992 1995 2000 2005 2015 KomiTEK Sibneft LUKOIL The next ONACO target ??? Surgut TNK Udmurtneft The USSR Slavneft Ministry of Rosneftegas the Oil Rosneft Rosneft Rosneft Rosneft Rosneft Industry 12 mt 240 mt 20 mt 460 mt 75 mt 595 mt VNK 135 mt Milestones: SIDANCO 1992 – start of privatization Severnaya Neft 1998 – appointment of S.Bogdanchikov -

Sinopec Oilfield Service Corporation

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this announcement, makes no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Sinopec Oilfield Service Corporation (a joint stock limited company established in the People’s Republic of China) (Stock code: 1033) Proposed Election of the Directors of the 10th Session of the Board and the Non-employee Representative Supervisors of the 10th Session of the Supervisory Committee The tenure of office of the ninth session of the board of directors and the supervisory committee of Sinopec Oilfield Service Corporation (the “Company”) will soon expire. The board of directors (the “Board”) of the Company announces that: 1. The following candidates are proposed to be elected as the directors (not include independent non-executive directors) of the 10th Session of the Board: Mr. Chen Xikun Mr. Yuan Jianqiang Mr. Lu Baoping Mr. Fan Zhonghai Mr. Wei Ran Mr. Zhou Meiyun 2. The following candidates are proposed to be elected as the independent non-executive directors of the 10th Session of the Board: Mr. Chen Weidong Mr. Dong Xiucheng Mr. Zheng Weijun 1 3. The following candidates are proposed to be elected as the non-employees representative supervisors of the 10th Session of the Supervisory Committee of the Company (the "Supervisory Committee"): Mr. Ma Xiang Mr. Du Jiangbo Ms. Zhang Qin Mr. Zhang Jianbo The information of each of the above proposed candidates for directors of the Company (the "Director") and the non-employee representative supervisors of the Company (the " Non-employee Representative Supervisor") is set out below: Information of the Proposed Directors (1) Mr. -

Process Technologies and Projects for Biolpg

energies Review Process Technologies and Projects for BioLPG Eric Johnson Atlantic Consulting, 8136 Gattikon, Switzerland; [email protected]; Tel.: +41-44-772-1079 Received: 8 December 2018; Accepted: 9 January 2019; Published: 15 January 2019 Abstract: Liquified petroleum gas (LPG)—currently consumed at some 300 million tonnes per year—consists of propane, butane, or a mixture of the two. Most of the world’s LPG is fossil, but recently, BioLPG has been commercialized as well. This paper reviews all possible synthesis routes to BioLPG: conventional chemical processes, biological processes, advanced chemical processes, and other. Processes are described, and projects are documented as of early 2018. The paper was compiled through an extensive literature review and a series of interviews with participants and stakeholders. Only one process is already commercial: hydrotreatment of bio-oils. Another, fermentation of sugars, has reached demonstration scale. The process with the largest potential for volume is gaseous conversion and synthesis of two feedstocks, cellulosics or organic wastes. In most cases, BioLPG is produced as a byproduct, i.e., a minor output of a multi-product process. BioLPG’s proportion of output varies according to detailed process design: for example, the advanced chemical processes can produce BioLPG at anywhere from 0–10% of output. All these processes and projects will be of interest to researchers, developers and LPG producers/marketers. Keywords: Liquified petroleum gas (LPG); BioLPG; biofuels; process technologies; alternative fuels 1. Introduction Liquified petroleum gas (LPG) is a major fuel for heating and transport, with a current global market of around 300 million tonnes per year. -

Journal of Current Chinese Affairs

3/2006 Data Supplement PR China Hong Kong SAR Macau SAR Taiwan CHINA aktuell Journal of Current Chinese Affairs Data Supplement People’s Republic of China, Hong Kong SAR, Macau SAR, Taiwan ISSN 0943-7533 All information given here is derived from generally accessible sources. Publisher/Distributor: Institute of Asian Affairs Rothenbaumchaussee 32 20148 Hamburg Germany Phone: (0 40) 42 88 74-0 Fax:(040)4107945 Contributors: Uwe Kotzel Dr. Liu Jen-Kai Christine Reinking Dr. Günter Schucher Dr. Margot Schüller Contents The Main National Leadership of the PRC LIU JEN-KAI 3 The Main Provincial Leadership of the PRC LIU JEN-KAI 22 Data on Changes in PRC Main Leadership LIU JEN-KAI 27 PRC Agreements with Foreign Countries LIU JEN-KAI 30 PRC Laws and Regulations LIU JEN-KAI 34 Hong Kong SAR Political Data LIU JEN-KAI 36 Macau SAR Political Data LIU JEN-KAI 39 Taiwan Political Data LIU JEN-KAI 41 Bibliography of Articles on the PRC, Hong Kong SAR, Macau SAR, and on Taiwan UWE KOTZEL / LIU JEN-KAI / CHRISTINE REINKING / GÜNTER SCHUCHER 43 CHINA aktuell Data Supplement - 3 - 3/2006 Dep.Dir.: CHINESE COMMUNIST Li Jianhua 03/07 PARTY Li Zhiyong 05/07 The Main National Ouyang Song 05/08 Shen Yueyue (f) CCa 03/01 Leadership of the Sun Xiaoqun 00/08 Wang Dongming 02/10 CCP CC General Secretary Zhang Bolin (exec.) 98/03 PRC Hu Jintao 02/11 Zhao Hongzhu (exec.) 00/10 Zhao Zongnai 00/10 Liu Jen-Kai POLITBURO Sec.-Gen.: Li Zhiyong 01/03 Standing Committee Members Propaganda (Publicity) Department Hu Jintao 92/10 Dir.: Liu Yunshan PBm CCSm 02/10 Huang Ju 02/11 -

Analiza Efikasnosti Naftnih Kompanija U Srbiji Efficency Analysis of Oil Companies in Serbia

________________________________________________________________________ 79 Analiza efikasnosti naftnih kompanija u Srbiji Efficency Analysis of Oil Companies in Serbia prof. dr. sc. Radojko Lukić Ekonomski fakultet u Beogradu [email protected] Ključne reči: ekspolatacija sirove nafte i gasa, Abstract tržišno učešće, efikasnost poslovanja, financijske Lately, significant attention has been paid to the performanse, održivo izveštavanje evolution of the performance of oil companies around Key words: exploration of crude oil and gas, market the world, by individual regions and countries. Bearing share, business efficiency, financial performance, susta- this in mind, relying on the existing theoretical and inable reporting methodological and empirical results, this paper analyzes the efficiency of operations, financial perfor- mance and sustainable reporting of oil companies in Sažetak Serbia, with special emphasis on the Petroleum Industry of Serbia (NIS). The results of the survey show signifi- U poslednje vreme značajna se pažnja poklanja cant role of mining, i.e. oil companies in creating addi- evoluaciji performansi naftnih kompanija u svetu, tional value of the entire economy of Serbia. Concer- po pojedinim regionima i zemljama. Imajući to u ning the Petroleum Industry of Serbia, it has a signi- vidu, oslanjajući se na postojeće teorijsko-metodo- ficant place in the production and trade of petroleum loške i empirijske rezultate, u ovom radu se analizi- products in Serbia. For these reasons, the efficiency of raju efikasnosti poslovanja, finansijske performanse operations, financial performance and maintenance of i održivo izveštavanje naftnih kompanija u Srbiji, s the Petroleum Industry of Serbia has been complexly posebnim osvrtom na Naftnu industriju Srbije (NIS). analyzed. In this respect, according to many indicators, Rezultati istraživanja pokazuju značajnu ulogu rudar- it is at a satisfactory level in relation to the average of the stva, odnosno naftnih kompanija u kreiranju dodatne world’s leading oil companies. -

Pride Drillships Awarded Contracts by BP, Petrobras

D EPARTMENTS DRILLING & COMPLETION N EWS BP makes 15th discovery in ultra-deepwater Angola block Rowan jackup moving SONANGOL AND BP have announced west of Luanda, and reached 5,678 m TVD to Middle East to drill the Portia oil discovery in ultra-deepwater below sea level. This is the fourth discovery offshore Saudi Arabia Block 31, offshore Angola. Portia is the 15th in Block 31 where the exploration well has discovery that BP has drilled in Block 31. been drilled through salt to access the oil- ROWAN COMPANIES ’ Bob The well is approximately 7 km north of the bearing sandstone reservoir beneath. W ell Keller jackup has been awarded a Titania discovery . Portia was drilled in a test results confirmed the capacity of the three-year drilling contract, which water depth of 2,012 m, some 386 km north- reservoir to flow in excess of 5,000 bbl/day . includes an option for a fourth year, for work offshore Saudi Arabia. The Bob Keller recently concluded work Pride drillships in the Gulf of Mexico and is en route to the Middle East. It is expected awarded contracts to commence drilling operations during Q2 2008. Rowan re-entered by BP, Petrobras the Middle East market two years ago after a 25-year absence. This PRIDE INTERNATIONAL HAS contract expands its presence in the announced two multi-year contracts for area to nine jackups. two ultra-deepwater drillships. First, a five-year contract with a BP subsidiary Rowan also has announced a multi- will allow Pride to expand its deepwater well contract with McMoRan Oil & drilling operations and geographic reach Gas Corp that includes re-entering in deepwater drilling basins to the US the Blackbeard Prospect. -

Madagascar's Extractive Industries Poised for Big Leap Forward

Madagascar’s extractive industries poised for big leap forward Report produced by The Energy Exchange www.theenergyexchange.co.uk 2 Contents page 3 Foreword 4 Executive summary 5 Madagascar Country profile 6 The political and economic environment 7 Madagascar’s mining potential 8 Madagascar’s hydrocarbon potential 9 Exploration is everywhere 10 Strengths, weaknesses, opportunities and threats 11 Conclusion 12 About The Energy Exchange 13 From the people who brought you... www.theenergyexchange.co.uk 3 Foreword The last frontier of the last frontier Following presidential and parliamentary elections held in late 2013, the situation in Madagascar is returning to normal after five years of internal socio-political crisis following the coup. The government is now keen to exploit the abundant and diversified natural resources and use them to carry out major structural changes in the economy. We have created a report to enable you to understand the potential of the extractive industries in the last frontier of Africa. This report includes: • An analysis of the current economic and political environment in the country • An overview of the mineral and hydrocarbon potential • A SWOT analysis of Madagascar as an investment destination The Energy Exchange is committed to creating high quality, strategic and technical conferences across the globe. We also recognise your need for pioneering industry content throughout the year. Enjoy the report, and please do get in touch with any feedback or questions. Best regards, Hannah Wharrier Managing Director, The Energy Exchange Telephone: +44 (0)20 7384 8030 Email: [email protected] www.theenergyexchange.co.uk 4 Executive summary The inauguration of Madagascar’s President Hery Rajaonarimampianina International support for the country is growing and foreign direct investment on 25 January 2014, and his pledge to open up his country to foreign (FDI) inflow this year is put at $837.5 million. -

Husky Energy Ltd

CLEAN ENERGY FINAL REPORT PACKAGE Project proponents are required to submit a Final Report Package, consisting of a Final Public Report and a Final Financial Report. These reports are to be provided under separate cover at the conclusion of projects for review and approval by Alberta Innovates (AI) Clean Energy Division. Proponents will use the two templates that follow to report key results and outcomes achieved during the project and financial details. The information requested in the templates should be considered the minimum necessary to meet AI reporting requirements; proponents are highly encouraged to include other information that may provide additional value, including more detailed appendices. Proponents must work with the AI Project Advisor during preparation of the Final Report Package to ensure submissions are of the highest possible quality and thus reduce the time and effort necessary to address issues that may emerge through the review and approval process. Final Public Report The Final Public Report shall outline what the project achieved and provide conclusions and recommendations for further research inquiry or technology development, together with an overview of the performance of the project in terms of process, output, outcomes and impact measures. The report must delineate all project knowledge and/or technology developed and must be in sufficient detail to permit readers to use or adapt the results for research and analysis purposes and to understand how conclusions were arrived at. It is incumbent upon the proponent to ensure that the Final Public Report is free of any confidential information or intellectual property requiring protection. The Final Public Report will be released by Alberta Innovates after the confidentiality period has expired as described in the Investment Agreement.