2018 TOD Status Report Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hyatt House Brochure LP.Indd

LOCATION HYATT HOUSE SColfax Avenue & Peoria Street • Aurora, CO 80011 RETAIL SPACE 270 FOR LEASE 25 A I D O 40th/Colorado T Station 70 225,000 vpd 38th/Blake Station 40th Ave Central Park Station Peoria Station 70 101,000 vpd 158,000 vpd COORS FIELD Fitzsimons Station ppd UNIONON d STATION ANSCHUTZ MEDICAL CAMPUS Colfax Station DOWNTOWN 134 Stops Per Day DENVER 33,000 vpd E Colfax Ave 47,999 vpd SITE 1,812,809 Riders Per Year E Colfax Ave 6,000 vpd 13th Avenue Station 17,000 vpd 6 CHERRY 2nd Avenue CREEK 26,995 vpd Abeline Station BUCKLEY Aurora Metro AIR FORCE GLENDALE Center Station BASE Peoria St Peoria Mississippi Ave E 470 Havana St University Blvd Buckley Rd Chambers Rd Hampden Ave 225 Iliff Ave HIGHLIGHTS 85 Iliff Station 25 ACROSS FROM THE NEWLY ANNOUNCED 650,000 235,000 vpd Colorado Blvd Nine Mile Station Sam Zaitz SF, 11 STORY UC HEALTH MEDICAL 285 225 720.529.2888 | [email protected] BUILDING DELIVERING 2022 Dayton Station Jeffery Feldman 8,160 SQUARE FEET OF RETAIL DENVER 720.529.2991 | [email protected] AVAILABLE, ACROSS FROM ANSCHUTZ MEDICAL Belleview Station TECH CENTER CAMPUS DELIVERING Q1 2021 DEMOGRAPHICS TRAFFIC 50,000+ DAYTIME EMPLOYEES AND 100,000+ DAILY VISITORS 1 MILE 3 MILE 5 MILE COLFAX AVENUE 2019 EST. POPULATION 24,218 159,614 394,657 47,999 VEHICLES PER DAY 2024 PROJECTED POPULATION 25,895 169,239 417,293 2019 EST. DAYTIME POPULATION 24,013 80,279 177,838 PEORIA STREET FIRST FLOOR OF THE NEW 140 ROOM HYATT 26,995 VEHICLES PER DAY HOUSE HOTEL OPENING 2020 2019 EST. -

2016-2021 Transportation Improvement Program Project List TIPID Project Name 2016-028 16Th St Mall Reconstruction: Arapahoe St to Lawrence St 2016-018 23Rd Ave

2016-2021 Transportation Improvement Program Project Lookup Lists Project Lookup Lists with TIPID, Project Name and Web file page number for Exhibit 2 -- Project Descriptions Projects by Name Projects by County Projects by Municipality Projects by Project Type This Web version includes all 2016-2021 TIP Amendments through 6/21/2016. Projects selected within pools are not identified individually. Contact Todd Cottrell at [email protected] with questions or comments on pools. Table 1: 2016-2021 Transportation Improvement Program Project List TIPID Project Name 2016-028 16th St Mall Reconstruction: Arapahoe St to Lawrence St 2016-018 23rd Ave. Bike/Ped Path at Fitzsimons Station 2016-035 30th St and Colorado Ave Bike/Ped Underpass 2007-082 56th Avenue: Quebec St to Pena Blvd 2016-067 6th Avenue Parkway Extension 2016-030 71st St Multimodal Pathway Connection: Winchester to Idylwild Trail 2016-002 Air Quality Improvements Pool 2016-012 Anschutz Medical Campus Shuttle 2012-087 Arapahoe Rd and Yosemite St Intersection Operational Improvements 2016-046 Arapahoe Rd: I-25 to Parker Rd Next Steps Operations Study 2016-054 Boulder County Bus-then-Bike Shelters 2016-008 Boulder Slough Multiuse Path: 30th St to 3100 Pearl 2016-026 Broadway Reconstruction: Violet Ave to US-36 2016-014 Broomfield Call-n-Ride 2016-059 C-470 Managed Toll Express Lanes: Wadsworth to I-25 2016-031 C-470 Multi-use Trail: Grade Separation at Yosemite St 2016-019 Colfax 15L Transit Improvements: I-225 to I-25 2012-010 DRCOG Second Commitment to FasTracks Pool 2016-029 East -

RTD I-225 Rail Line Montview Alignment Change

FOR IMMEDIATE RELEASE RTD Board Approves Moving Planned I-225 Rail Station from Montview to Fitzsimons Parkway CU Officials Commit to Shuttle Service from Fitzsimons Station to Anschutz Medical Campus DENVER, June 25, 2013—The Regional Transportation District (RTD) Board of Directors has approved a request from the University of Colorado (CU) Anschutz Medical Campus to relocate the planned Montview Station on the I-225 Rail Line to a new location at Fitzsimons Parkway. CU officials requested the station be moved due to concerns for adequate mitigation of electromagnetic interference (EMI) and vibration near sensitive research equipment at current and future medical buildings. This decision by the Board of Directors will allow the I-225 project team to identify environmental impacts and propose mitigation before moving forward with design and construction. “We will continue to collaborate with our partners to ensure that our project meets the needs of the greater community,” said RTD General Manager Phil Washington. “We will develop a solution that keeps the project moving forward while staying on budget.” During the 2007 - 2009 environmental and early design process, RTD and CU evaluated options for mitigating EMI and vibration from the train, but found that previous measures identified might not be sufficient for future technologies. Additional methods of mitigation were considered but found to be too costly. The project team aims to have a new alignment and station site determined, with design underway, by the end of the year. The I-225 Rail Line is a 10.5-mile light rail extension that will travel through the City of Aurora and make key connections to the Anschutz Medical Campus and the future VA Hospital. -

Broncosride Pickup Schedule for December 22, 2019

BroncosRide and Light Rail Service page 1 of 2 BroncosRide Schedule for: Sunday, December 22, 2019 Route: Park-n-Ride / Stop / Station Times are approximate Post game bus location** BR26: Dry Creek & University 11:35 AM 11:40 AM 11:45 AM every 5-10 minutes until 12:55 PM Row 22 Arapahoe High School BR24: Alameda Havana 12:25 PM 12:40 PM 12:55 PM Row 21 BR10: Boulder High School 11:35 AM 11:55 AM 12:15 PM Row15-16 Arapahoe & 17th BR32: El Rancho 12:00 PM 12:15 PM 12:35 PM Row 4 BR32: Evergreen 11:45 AM 12:00 PM 12:20 PM Row 4 BR38: Federal Shuttle: Lincoln HS (Hazel Ct & Iliff) and bus stops on Federal Blvd 11:35 AM 11:40 AM 11:45 AM every 5 - 10 minutes until 1:50 PM Row 28 between Evans and 8th Ave BR20: Longmont Park-n-Ride 11:30 AM 11:35 AM 11:45 AM 11:50 AM 12:00 PM 12:10 PM 12:20 PM 12:30 PM Rows 17-18 815 South Main Street BR44: Nine Mile (Ga te F) 11:35 AM 11:40 AM 11:45 AM every 5-10 minutes until 1:00 PM Rows 23-24 BR8: Olde Town Arvada Discontinued Discontinued: Ride G-Line to DUS and Transfer to C, E or W-Lines to Broncos Stadium BR48: Parker 11:35 AM 11:45 AM 11:50 AM 12:00 PM 12:15 PM 12:30 PM Row 19 BR48: Pinery 11:35 AM 11:40 AM 11:50 AM 12:05 PM 12:20 PM Row 19 BR56: South High School 11:40 AM 11:50 AM 12:00 PM 12:10 PM 12:20 PM 12:35 PM 12:50 PM Row 26 Louisiana & Gilpin BR4: Thornton (Gate C) 11:40 AM 11:45 AM 11:45 AM every 5-10 minutes until 1:35 PM Rows 9-12 BR10: US 36 & Broomfield Station (Gate 11:35 AM 11:45 AM 11:55 AM 12:05 PM 12:15 PM 12:25 PM 12:45 PM Rows 15-16 K) BR10: US 36 & McCaslin Stn (Gate A) 11:45 -

Final West Corridor Service Plan 2013

Final West Corridor Service Plan 2013 October 2012 Final West Corridor Service Plan 2013 1 Introduction ........................................................................................................ 4 1.1 Background & Focus ....................................................................................... 4 1.2 Relevant Studies ............................................................................................. 4 1.2.1 West Corridor Environmental Impact Study (EIS) – 2004 .............................. 5 1.2.2 2007 West Corridor Transit Plan ............................................................... 5 1.2.3 Lessons Learned from Previous RTD LRT Corridor Implementations ................ 5 2 Current Transit Market Assessment ....................................................................... 6 2.1 Population Density 2005 ................................................................................. 7 2.2 Employment Density 2005 ............................................................................... 7 3 Current Service Evaluation .................................................................................. 10 3.1 Transit Route Network .................................................................................. 10 3.2 Transit Service Levels ................................................................................... 10 3.3 Transit Passenger Facilities ............................................................................ 13 3.4 Ridership .................................................................................................... -

2013 Transit-Oriented Development Status Report RTD and Fastracks Overview

2013 Transit-Oriented Development Status Report RTD and FasTracks Overview RTD oversees a 47-mile rail transit system that services 46 stations on five corridors including: • The 5.3-mile Central Corridor and 1.8-mile Central Platte Valley (CPV) Spur in central Denver • The 8.7-mile Southwest Line to Englewood, Sheridan, and Littleton • The 19.2-mile Southeast Line to Lone Tree and Aurora • The 12.1-mile West Line to Lakewood and Golden The FasTracks program, approved by district voters in a 2004 ballot initiative will: • add 122 miles of rail service • 18 miles of Bus Rapid Transit (BRT) • approximately 60 new stations along six new corridors • extend three existing light rail lines image courtesy Gensler Grand Opening / image courtesy RTD Construction cranes dominated the skyline in RTD and TOD STAMPs Underway STAMPs Kicking Off 2013, as the result of an apartment boom in in 2014 the metro area. Development in 2013 centered Transit-oriented development is typically on the hub of the FasTracks program: Denver higher density and incorporates a mixture C-470/Lucent Station I-25/Broadway Station Area Master Plan Area Master Plan Union Station which is scheduled to open in of different uses that generate transit rider- spring 2014. Significant development has also ship. Multiple TODs contribute to creating 104th Ave. Station TOD Fitzsimons Parkway occurred around other existing and future transit-oriented communities where people Master Planning Study Station Area Master Plan stations as construction of FasTracks corridors can live, work, reduce transportation costs, continues at a rapid pace. and improve overall health through increased 88th Avenue Station Civic Center Station muli-modal activity. -

2019 TOD Status Report Introduction This Report Provides an Update on Transit-Oriented Development (TOD) in the Regional Transportation District (RTD)

2019 TOD Status Report Introduction This report provides an update on transit-oriented development (TOD) in the Regional Transportation District (RTD). Highlights of this report include: • A significant amount of development in the region has occurred within the station influence area (half-mile radius from RTD’s stations) • Development within the station influence area continues at a strong rate Mariposa – 10th Osage • 2019 accounted for the most multifamily TOD deliveries ever • 2019 office TOD deliveries are below 2018 figures, but remain strong Ride at RiNo – 38th•Blake Station 2 Table of Contents 1. What is TOD? 2. RTD TOD data 3. TOD trends over time 4. TOD trends by corridor 5. Highest rent station areas 6. Value creation 7. Denver Union Station 8. Top stations for TOD 9. TOD Database summary 3 What is Transit-Oriented Development? Per RTD’s TOD Strategic Plan (2010): What enables TOD? • More compact and dense development • Real estate market - creates greater demand for development within a 10-minute walk or ½-mile • Zoning - higher densities allow more people to live & work near transit distance around transit facilities compared • Infrastructure/Access - critical for all developments to existing development patterns in the • Jurisdiction Interest/Incentives - local governments can same area incentivize TOD by providing financial incentives, density bonuses, or • A mix of uses — either horizontal or infrastructure vertical — usually including residential, • Lot size and ownership - larger lots & fewer land owners facilitate retail, and office employment TOD • High-quality, pedestrian-oriented urban • Time - station areas may need time to mature design and streetscapes Windsor at Broadway Station – I-25•Broadway Station Depot Square – Boulder Junction Lofts at Lincoln Station – Lincoln Station West Line Flats – Lamar Station 4 RTD TOD Data and Analysis This report analyzes two datasets: the RTD Development Database and the TOD Trend Tool. -

RTD Director Map District M

TENNYSNST Olde Town Arvada EASLEY RD GRANDVIEW AV 56TH AV ZUNI ST Olde Town Station UV391 76 RIDGE RD ¨¦§ 54TH AV ARVADA I 53RD AV INDIANAST TEJONST 52ND AV W 52ND AVE W 52ND AVE 0 0.475 0.95 Arvada Ridge StationCARRST 52ND AV RIDGE RD UV95 Chaffee Park Miles 72 MARSHALL ST 93 UV Regis W REGIS BLVD W 50TH AVE UV 50TH AV ST TABOR KIPLINGST ELDRIDGEST 49TH AV Ward Road Station GARRISON ST 48TH AV 48TH AV W 48TH AVE W 48TH AVE RTD Director MCINTYREST Ward Road UV121 Berkeley W 46TH AVE LAKESIDE NTEJON ST Districts NTENNYSON ST W 44TH AVE 44TH AV NIRVING ST WHEAT RIDGE NLOWELL BLVD Sunnyside UV93 MOUNTAIN VIEW 38TH AV HARLAN ST W 38TH AVE 46 UV YOUNGFIELDST Legend W 35TH AVE W 35TH AVE LightRail Stations West Highland X" NIRVING ST Highland UV93 W 32ND AVE W 32ND AVE NZUNI ST WASHINGTON AV 32ND AV ParkNRides 10TH ST ELDRIDGE ST 29TH AV W 29TH AVE COUNTIES 27TH AV W 26TH AVE Current Director Dist FORD ST 26TH AV ¤£6 Jefferson Park Other Director Dist Sloan Lake W 23RD AVE WATER ST Pepsi Center - Elitch Gardens Station FASTRACKS EDGEWATER 287 70 20TH AV ¤£ 19TH ST ¨¦§ Auraria LightrailLines INVESCO Field at Mile High Station W 17TH AVE ¤£287 BusRoutes 6 25 ¤£ GOLDEN 70 West Colfax 40 ¨¦§ ¤£Auraria West Station¨¦§ 14TH AV Lakewood - Wadsworth Station W 14TH AVE N KNOX CT GOLDEN RD Sheridan Station ULYSSES ST ULYSSES Sun Valley M Oak Station Garrison Station Lamar Station Lincoln Park 10TH AV 10TH AV W 10TH AVE Knox Station 10TH AV Perry Station N ZUNI ST NST PERRY SIMMSST 40 ¤£ VillaNKNOX CT Park W 8TH AVE 8TH AV 121 OAKST UV INDIANA ST INDIANA -

Project Name: Aria Phase II Apartments (Aria II)

Project Name: Aria Phase II Apartments (Aria II) Project Address: 5274 Decatur St., Denver, CO I. Executive Summary: a. Construction Type: Aria II will be a wood framed, 4 story building, on a post tension slab with one central elevator core and two interior stairwells. The exterior will be Hardie Plank siding. IBC Construction category is Type 5A. The architectural style will be contemporary with a low-sloped roof. b. Population Served: Aria II serves families with incomes from 30%- 60% AMI. See Chart below: c. Bedroom Mix Unit Square 30% 40% 50% 60% Total Type Feet AMI AMI AMI AMI Units 1BR/1BA 693 3 21 9 20 53 2BR/1BA 994 1 5 2 4 12 TOTAL 4 26 11 24 65 % 6% 40% 17% 37% 100% d. Location: 5274 Decatur Street. Aria II will be at the corner of 53nd Avenue, and Decatur Street in the Aria Denver redevelopment of former Marycrest Convent Campus in Denver. The location of the Aria II apartments is in the NE corner of the overall Aria Denver site, adjacent to Phase 1 Aria Apartments. The site is within the boundaries of Denver but is surrounded on three sides by Adams County. e. Amenities: Unit Amenities • Energy Efficient Stove, and refrigerator; • Cable and High Speed Internet hookups; • Kitchens with islands or peninsulas; • Private patios for the ground floor units; • Dining areas and eat-at counters • Balconies for all upper floor units • Closets and pantry’s • Washers and dryers in all units. Site and Project Amenities • Mixed-use, mixed-income community; • Open Space with outdoor fitness walks • Multi-generational community, and ADA compliant exercise equipment; • Diversity of housing types; • Pedestrian friendly sidewalks/bike paths • Neighborhood serving retail; • Way-finding signage; • Includes latest, green technologies; • Services of Cultivate health, fresh food. -

2016-2021 Transportation Improvement Program Project List TIPID Project Name 2016-028 16Th St Mall Reconstruction: Arapahoe St to Lawrence St 2016-018 23Rd Ave

2016-2021 Transportation Improvement Program Project Lookup Lists Project Lookup Lists with TIPID, Project Name and Web file page number for Exhibit 2 -- Project Descriptions Projects by Name Projects by County Projects by Municipality Projects by Project Type This Web version includes all 2016-2021 TIP Amendments through 12/18/2015. Projects selected within pools are not identified individually. Contact Todd Cottrell at [email protected] with questions or comments on pools. Table 1: 2016-2021 Transportation Improvement Program Project List TIPID Project Name 2016-028 16th St Mall Reconstruction: Arapahoe St to Lawrence St 2016-018 23rd Ave. Bike/Ped Path at Fitzsimons Station 2016-035 30th St and Colorado Ave Bike/Ped Underpass 2007-082 56th Avenue: Quebec to Pena 2016-030 71st St Multimodal Pathway Connection: Winchester to Idylwild Trail 2016-002 Air Quality Improvements Pool 2016-012 Anschutz Medical Campus Shuttle 2016-046 Arapahoe Rd: I-25 to Parker Rd Next Steps Operations Study 2016-054 Boulder County Bus-then-Bike Shelters 2016-008 Boulder Slough Multiuse Path: 30th St to 3100 Pearl 2016-026 Broadway Reconstruction: Violet Ave to US-36 2016-014 Broomfield Call-n-Ride 2016-031 C-470 Multi-use Trail: Grade Separation at Yosemite St 2016-019 Colfax 15L Transit Improvements: I-225 to I-25 2012-010 DRCOG Second Commitment to FasTracks Pool 2016-029 East Lafayette Multimodal Path Connection: Commerce Ct to Lafayette Park-n-Ride 2012-107 Enhanced Mobility for Elderly and Disabled (FTA 5310) 2016-048 Erie Pkwy Study: SH-287 to I-25 -

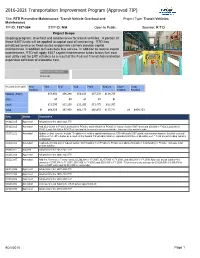

2016-2021 Transportation Improvement Program (Approved TIP)

2016-2021 Transportation Improvement Program (Approved TIP) Title: RTD Preventive Maintenance: Transit Vehicle Overhaul and Project Type: Transit Vehicles Maintenance TIP-ID: 1997-084 STIP-ID: N/A Open to Public: Sponsor: R T D Project Scope Ongoing program: Overhaul and maintenance for transit vehicles. A portion of these 5307 funds will be applied to capital cost of contracting. RTD has privatized service on fixed-routes and private carriers provide capital maintenance in addition to fixed-route bus service. In addition to routine capital maintenance, RTD will apply 5307 capital maintenance funds to bus fuel cost and utility cost for LRT vehicles as a result of the Federal Transit Administration expanded definition of allowable cost. Affected County(ies) Regional Amounts in $1,000s Prior FY16 FY17 FY18 FY19 FY20-21 Future Total Funding Funding Funding Federal (5307) $55,691 $56,248 $56,810 $57,378 $114,756 State $0 $0 $0 $0 $0 Local $11,195 $11,250 $11,365 $11,475 $22,955 Total $0 $66,886 $67,498 $68,175 $68,853 $137,711 $0 $409,123 Date Status Description 04/16/2015 Approved Adopted into the 2016-2021 TIP 05/16/2013 Amended Add $3,140,000 in FY2013, $140,000 in FY2014, and $140,000 in FY2015 of federal Section 5307 funds and $28,000 in FY2013, $28,000 in FY2014, and $28,000 in FY2015 of local match to correct a previous mistake. Increase total project funds. 07/17/2012 Amended Update project scope to include “In addition to routine capital maintenance, RTD will apply 5307 capital maintenance funds to bus fuel cost and utility cost for LRT vehicles as a result of the Federal Transit Administration expanded definition of allowable cost.” Total project funding remains unchanged. -

Broncosride and Light Rail Service Page 1 of 2

BroncosRide and Light Rail Service page 1 of 2 BroncosRide Schedule for: November 3, 2019 Route: Park-n-Ride / Stop / Station Times are approximate Post game bus location** BR26: Dry Creek & University 11:55 AM 12:00 PM 12:05 PM every 5-10 minutes until 1:15 PM Row 22 Arapahoe High School BR24: Alameda Havana 12:45 PM 1:00 PM 1:15 PM Row 21 BR10: Boulder High School 11:55 AM 12:15 PM 12:35 PM Row15-16 Arapahoe & 17th BR32: El Rancho 12:20 PM 12:35 PM 12:55 PM Row 4 BR32: Evergreen 12:05 PM 12:20 PM 12:40 PM Row 4 BR38: Federal Shuttle: Lincoln HS (Hazel Ct & Iliff) and bus stops on Federal Blvd 11:55 AM 12:00 PM 12:05 PM every 5- 10 minutes until 1:15 PM Row 28 between Evans and 8th Ave BR20: Longmont Park-n-Ride 11:50 AM 11:55 AM 12:05 PM 12:10 PM 12:20 PM 12:30 PM 12:40 PM 12:50 PM Rows 17-18 815 South Main Street BR44: Nine Mile (Gate F) 11:55 AM 12:00 PM 12:05 PM every 5-10 minutes until 12:40 PM Rows 23-24 BR8: Olde Town Arvada Discontinued Discontinued: Ride G-Line to DUS and Transfer to C, E or W-Lines to Broncos Stadium BR48: Parker 11:55 AM 12:05 PM 12:10 PM 12:20 PM 12:35 PM 12:50 PM Row 19 BR48: Pinery 11:55 AM 12:00 PM 12:10 PM 12:25 PM 12:40 PM Row 19 BR56: South High School 12:00 PM 12:10 PM 12:20 PM 12:30 PM 12:40 PM 12:55 PM 1:10 PM Row 26 Louisiana & Gilpin BR4: Thornton (Gate C) 12:00 PM 12:05 PM 12:10 PM every 5-10 minutes until 1:35 PM Rows 9-12 BR10: US 36 & Broomfield Station (Gate 11:55 AM 12:05 PM 12:15 PM 12:25 PM 12:35 PM 12:45 PM 12:55 PM 1:05 PM Rows 15-16 K) BR10: US 36 & McCaslin Stn (Gate A) 12:05 PM 12:10