Autonomous Vehicles and the Future of Work in Canada

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lyft, Inc. (Exact Name of Registrant As Specified in Its Charter)

S-1 1 d633517ds1.htm S-1 Table of Contents As filed with the Securities and Exchange Commission on March 1, 2019. Registration No. 333- UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM S-1 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 Lyft, Inc. (Exact name of registrant as specified in its charter) Delaware 7389 20-8809830 (State or other jurisdiction of (Primary Standard Industrial (I.R.S. Employer incorporation or organization) Classification Code Number) Identification Number) Lyft, Inc. 185 Berry Street, Suite 5000 San Francisco, California 94107 (844) 250-2773 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) Logan Green Co-Founder and Chief Executive Officer John Zimmer Co-Founder, President and Vice Chairman Lyft, Inc. 185 Berry Street, Suite 5000 San Francisco, California 94107 (844) 250-2773 (Name, address, including zip code, and telephone number, including area code, of agent for service) Copies to: Katharine A. Martin Kristin N. Sverchek Richard A. Kline Rezwan D. Pavri David V. Le Anthony J. McCusker Lisa L. Stimmell Kevin C. Chen An-Yen E. Hu Andrew T. Hill Christopher M. Reilly Goodwin Procter LLP Wilson Sonsini Goodrich & Rosati, P.C. Lyft, Inc. 601 Marshall Street 650 Page Mill Road 185 Berry Street, Suite 5000 Redwood City, California 94063 Palo Alto, California 94304 San Francisco, California 94107 (650) 752-3100 (650) 493-9300 (844) 250-2773 Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective. If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. -

Exploration of the Current State and Directions of Dynamic Ridesharing Joseph J

Montclair State University Montclair State University Digital Commons Theses, Dissertations and Culminating Projects 8-2015 Exploration of the Current State and Directions of Dynamic Ridesharing Joseph J. Di Gianni Montclair State University Follow this and additional works at: https://digitalcommons.montclair.edu/etd Part of the Environmental Sciences Commons Recommended Citation Di Gianni, Joseph J., "Exploration of the Current State and Directions of Dynamic Ridesharing" (2015). Theses, Dissertations and Culminating Projects. 187. https://digitalcommons.montclair.edu/etd/187 This Dissertation is brought to you for free and open access by Montclair State University Digital Commons. It has been accepted for inclusion in Theses, Dissertations and Culminating Projects by an authorized administrator of Montclair State University Digital Commons. For more information, please contact [email protected]. EXPLORATION OF THE CURRENT STATE AND DIRECTIONS OF DYNAMIC RIDESHARING A DISSERTATION Submitted to the Faculty of Montclair State University in partial fulfillment of the requirements for the degree of Doctor of Philosophy by JOSEPH J. DI GIANNI Montclair State University Montclair, NJ 2015 Dissertation Chair: Dr. Rolf Sternberg Copyright © 2015 by Joseph J. Di Gianni. All rights reserved. MONTCLAIR STATE UNIVERSITY THE GRADUATE SCHOOL DISSERTATION APPROVAL We hereby approve the Dissertation EXPLORATION OF THE CURRENT STATE AND DIRECTIONS OF DYNAMIC RIDESHARING of Joseph J. Di Gianni Candidate for the Degree: Doctor ofPhilosophy Dissertation Committee: Department ofEarth and Environmental Studies Dr. RolfSter^eT^ Certified by: Dissertation.Chair Dr. Joan C. Ficke Dr. Gregory Pope Dean ofThe Graduate School Date Dr. Harbans^nsh . Joseph Mirabella ABSTRACT EXPLORATION OF THE CURRENT STATE AND DIRECTIONS OF DYNAMIC RIDSHAREING by Joseph J. -

Mission Is Critical

Stanford eCorner Mission is Critical Navin Chaddha, Mayfield 06-03-2019 URL: https://ecorner.stanford.edu/?post_type=snippet&p=63105 Navin Chaddha, managing director of Mayfield, attributes Lyft’s rapid growth not just to technology, but to the mission that founders John Zimmer and Logan Green set for the company from day one: to make people’s lives better through transportation. He describes how services like providing free rides to polling places exemplify the values that give Lyft its structural integrity. Transcript - So, when we met John and Logan in 2011, their business was called Zimride, as Lyft didn't even exist.. What was the idea? The idea was a social site, a variant of Craigslist where people were posting requests and offers for shared rides.. It was primarily being used by students, primarily at Stanford, and commuters for the Bay Area traffic.. But it wasn't a direct consumer to consumer application.. It was distributed through universities and corporations.. It was a good idea, but not a massive market that a VC would invest in.. Then comes the smartphone revolution.. And the smartphone step.. Like any other smart entrepreneur, John and Logan pivoted the company to creating the first, now this is debatable, I'm an investor in them, so please take it with a grain of salt.. The first peer-to-peer ridesharing service not focused on the black car market and have grown in seven years or so to providing more than 50 million rides a month.. What led to their success was their authentic mission of making people's lives better by providing the best transportation. -

First Zipcar, Now Uber: Legal and Policy Issues Facing the Expanding “Shared Mobility” Sector in U.S

FIRST ZIPCAR, NOW UBER: LEGAL AND POLICY ISSUES FACING THE EXPANDING “SHARED MOBILITY” SECTOR IN U.S. CITIES JOSEPH P. SCHWIETERMAN, PH.D.* & MOLLIE PELON** INTRODUCTION ......................................................................................... 109 I. TYPES OF SHARED-MOBILITY SERVICES .............................................. 111 A. Carsharing .............................................................................. 112 1. Evolution and Expansion. ................................................. 113 2. Notable Research .............................................................. 116 3. Policy Issues and Outlook. ............................................... 118 B. Transportation Network Companies ...................................... 120 1. Evolution and Expansion. ................................................. 121 2. Notable Research. ............................................................. 124 3. Policy Issues and Outlook ................................................ 127 C. Microtransit Service ............................................................... 128 1. Evolution and Expansion. ................................................. 129 2. Notable Research .............................................................. 131 3. Policy Issues and Outlook ................................................ 132 D. Crowdsourced Intercity Bus Operators .................................. 132 1. Evolution and Expansion .................................................. 132 2. Notable Research. ............................................................ -

Glossary of Key Sharing Economy Terms

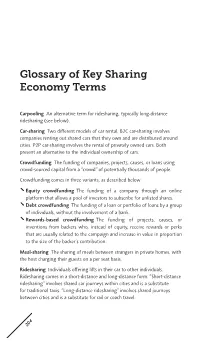

Glossary of Key Sharing Economy Terms Carpooling An alternative term for ridesharing, typically long-distance ridesharing (see below). Car-sharing Two different models of car rental. B2C car-sharing involves companies renting out shared cars that they own and are distributed around cities. P2P car-sharing involves the rental of privately owned cars. Both present an alternative to the individual ownership of cars. Crowdfunding The funding of companies, projects, causes, or loans using crowd-sourced capital from a “crowd” of potentially thousands of people. Crowdfunding comes in three variants, as described below. Equity crowdfunding The funding of a company through an online platform that allows a pool of investors to subscribe for unlisted shares. Debt crowdfunding The funding of a loan or portfolio of loans by a group of individuals, without the involvement of a bank. Rewards-based crowdfunding The funding of projects, causes, or inventions from backers who, instead of equity, receive rewards or perks that are usually related to the campaign and increase in value in proportion to the size of the backer’s contribution. Meal-sharing The sharing of meals between strangers in private homes, with the host charging their guests on a per seat basis. Ridesharing Individuals offering lifts in their car to other individuals. Ridesharing comes in a short-distance and long-distance form. “Short-distance ridesharing” involves shared car journeys within cities and is a substitute for traditional taxis. “Long-distance ridesharing” involves shared journeys between cities and is a substitute for rail or coach travel. 204 Glossary of Key Sharing Economy Terms 205 Sharing economy (condensed version) The value in taking underutilized assets and making them accessible online to a community, leading to a reduced need for ownership of those assets. -

First Zipcar, Now Uber: Legal and Policy Issues Facing the Expanding “Shared Mobility” Sector in U.S

Belmont Law Review Volume 4 Symposium 2016: The Modern Metropolis – Article 5 Contemporary Legal Issues in Urban Communities 2017 First Zipcar, Now Uber: Legal and Policy Issues Facing the Expanding “Shared Mobility” Sector in U.S. Cities Joseph P. Schwieterman DePaul University Mollie Pelon DePaul University Follow this and additional works at: https://repository.belmont.edu/lawreview Part of the Legal Writing and Research Commons Recommended Citation Schwieterman, Joseph P. and Pelon, Mollie (2017) "First Zipcar, Now Uber: Legal and Policy Issues Facing the Expanding “Shared Mobility” Sector in U.S. Cities," Belmont Law Review: Vol. 4 , Article 5. Available at: https://repository.belmont.edu/lawreview/vol4/iss1/5 This Article is brought to you for free and open access by the College of Law at Belmont Digital Repository. It has been accepted for inclusion in Belmont Law Review by an authorized editor of Belmont Digital Repository. For more information, please contact [email protected]. FIRST ZIPCAR, NOW UBER: LEGAL AND POLICY ISSUES FACING THE EXPANDING “SHARED MOBILITY” SECTOR IN U.S. CITIES JOSEPH P. SCHWIETERMAN, PH.D.* & MOLLIE PELON** INTRODUCTION ......................................................................................... 109 I. TYPES OF SHARED-MOBILITY SERVICES .............................................. 111 A. Carsharing .............................................................................. 112 1. Evolution and Expansion. ................................................. 113 2. Notable Research ............................................................. -

For Hire Transportation Services Report

For Hire Transportation services report A Study by The Institute for Municipal & Regional Policy (IMRP) CENTRAL CONNECTICUT STATE UNIVERSITY The Institute for Municipal and Regional Policy 1 Authors: Dr. James Thorson, Ph.D. Professor of Economics and Finance School of Business Southern Connecticut State University Veronica L. Gill, JD Assistant Professor of Management/MIS School of Business Southern Connecticut State University IMRP Staff Contributors: Andrew Clark, Director James Fazzalaro, Research Specialist Ken Barone, Research and Policy Specialist Teodor Radu, University Assistant The Institute for Municipal and Regional Policy 2 TABLE OF CONTENTS Introduction................................................................................................................................4 Executive Summary...................................................................................................................5 PART I: Background ................................................................................................................10 PART II: History.........................................................................................................................11 PART III: Literature Review......................................................................................................14 PART IV: Other Jurisdictions Regulations ................................................................................19 PART V: Outstanding Issues in Connecticut ............................................................................28 -

Impacts of Ridesourcing on VMT, Parking Demand, Transportation Equity, and Travel Behavior

MPC 19-379 | A. Henao, W. Marshall, and B. Janson Impacts of Ridesourcing on VMT, Parking Demand, Transportation Equity, and Travel Behavior A University Transportation Center sponsored by the U.S. Department of Transportation serving the Mountain-Plains Region. Consortium members: Colorado State University University of Colorado Denver Utah State University North Dakota State University University of Denver University of Wyoming South Dakota State University University of Utah Technical Report Documentation Page 1. Report No. 2. Government Accession No. 3. Recipient's Catalog No. MPC-514 4. Title and Subtitle 5. Report Date Impacts of Ridesourcing on VMT, Parking Demand, Transportation Equity, and March, 2019 Travel Behavior 6. Performing Organization Code 7. Author(s) 8. Performing Organization Report No. Alejandro Henao, PhD Wesley E. Marshall, PhD, PE MPC 19-379 Bruce Janson, PhD, PE 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) University of Colorado Denver 1200 Larimer Street 11. Contract or Grant No. Denver, CO 80217 12. Sponsoring Agency Name and Address 13. Type of Report and Period Covered Mountain-Plains Consortium Final Report North Dakota State University 09/30/2013 – 9/30/2018 PO Box 6050, Fargo, ND 58108 14. Sponsoring Agency Code 15. Supplementary Notes Supported by a grant from the US DOT, University Transportation Centers Program 16. Abstract Ride-haling such as Uber and Lyft are changing the ways people travel and is critical to forecasting mode choice demands and providing adequate infrastructure. Despite widespread claims that these services help reduce driving and the need for parking, there is little research on these topics. -

Planning for Autonomous Mobility (PAS Report 592)

PAS REPORT 5 9 2 PLANNING FOR AUTONOMOUS MOBILITY Jeremy Crute, William Riggs, AICP, Timothy S. Chapin, and Lindsay Stevens, AICP ABOUT THE AUTHORS APA RESEARCH MISSION Jeremy Crute has been the senior planner in Florida State University’s Depart- ment of Urban and Regional Planning for the last four years. There he has man- APA conducts applied, policy-relevant research that aged a wide range of applied and scholarly research projects on community advances the state of the art in planning practice. redevelopment, transportation, and land-use issues. He has prior professional APA’s National Centers for Planning—the Green community development experience in Chattanooga, Tennessee, and Atlanta, Communities Center, the Hazards Planning Center, Georgia. He holds a master of science degree in urban and regional planning and the Planning and Community Health Center— from Florida State University, and bachelors degrees in economics and com- guide and advance a research directive that address- munity development from Covenant College. es important societal issues. APA’s research, educa- William (Billy) Riggs, aicp, phd, leed ap, is a global expert and thought leader tion, and advocacy programs help planners create in the areas of future mobility and smart transportation, housing, economics, communities of lasting value by developing and dis- and urban development. He is a professor at the University of San Francisco seminating information, tools, and applications for School of Management, and an advisor to multiple companies and start-ups on built and natural environments. technology, smart mobility, and urban development. This follows two decades of work as a planner, economist, and engineer. -

Exploration of the Current State and Directions in the Emerging Field of Dynamic Ridesharing Platforms

Middle States Geographer, 2014, 47: 68-78 EXPLORATION OF THE CURRENT STATE AND DIRECTIONS IN THE EMERGING FIELD OF DYNAMIC RIDESHARING PLATFORMS Joseph J. Di Gianni Department of Earth and Environmental Studies Montclair State University Montclair, NJ 07043 ABSTRACT: Automobility has advanced since the postwar decline of public transportation and its near universal replacement by single-occupant vehicles (SOVs) throughout much of the developed economies. Even so- called “transit friendly” economies of the Global South have seen shifts in their modes of transportation to systems that are predominantly SOV-based (Cervero, 2013). Intensive infrastructure expansion within emerging economies indicates that the SOV is being adopted at a rate similar to the developed economies of one hundred years ago. In Henry Ford's quote “With mobility comes freedom and progress” mobility becomes universally interpreted as “automobility”. Grave concern is linked to the continuation of the SOV model and its consequences for an environment taxed by an ever-expanding transportation sector. A paradigm shift, however, in the SOV-driven model, has been detected coming not from transportation but the different domains of information and communication technologies (ICT). This review examined the current state and direction of dynamic ridesharing (DRS), an emerging technology driven by recent innovations in ICT over the last two decades (Siddiqi & Buliung, 2013). DRS matches drivers and riders in real-time using Internet and mobile technology, and are single- occurrence events organized on short notice (Amey, Attanucci, & Mishalani, 2011). We conclude with a case study of DRS from its roots in San Francisco, CA. The city provides a present-day template for emerging themes when DRS is introduced into the present-day urban transportation system. -

Matias Malig, As Trustee for the Malig Family Trust, Et Al. V. Lyft, Inc. Et Al

Case 4:19-cv-02690-HSG Document 1 Filed 05/17/19 Page 1 of 27 1 Jeffrey C. Block, pro hac vice to be filed Jacob A. Walker (SBN 271217) 2 BLOCK & LEVITON LLP 260 Franklin Street, Suite 1860 3 Boston, MA 02110 (617) 398-5600 phone 4 [email protected] 5 Attorneys for Plaintiff Matias Malig, as Trustee for the Malig Family Trust 6 UNITED STATES DISTRICT COURT 7 NORTHERN DISTRICT OF CALIFORNIA 8 MATIAS MALIG, AS TRUSTEE FOR THE Case No._________________________ 9 MALIG FAMILY TRUST, Individually and on Behalf of All Others Similarly Situated, 10 Plaintiff, CLASS ACTION 11 vs. COMPLAINT FOR VIOLATIONS 12 OF FEDERAL SECURITIES LAWS LYFT INC.; LOGAN GREEN; JOHN ZIMMER; 13 BRIAN ROBERTS; PRASHANT (SEAN) AGGARWAL; BEN HOROWITZ; VALERIE 14 JARRETT; DAVID LAWEE; HIROSHI MIKITANI; ANN MIURA-KO; MARY AGNES 15 (MAGGIE) WILDEROTTER; J.P. MORGAN SECURITIES LLC; CREDIT SUISSE 16 SECURITIES (USA) LLC; JEFFERIES LLC; DEMAND FOR JURY TRIAL UBS SECURITIES LLC; STIFEL, NICOLAUS 17 & COMPANY, INCORPORATED; RBC CAPITAL MARKETS, LLC; KEYBANC 18 CAPITAL MARKETS INC.; COWEN AND COMPANY, LLC; RAYMOND JAMES & 19 ASSOCIATES, INC.; CANACCORD GENUITY LLC; EVERCORE GROUP L.L.C.; 20 PIPER JAFFRAY & CO.; JMP SECURITIES LLC; WELLS FARGO SECURITIES, LLC; 21 KKR CAPITAL MARKETS LLC; ACADEMY SECURITIES, INC.; BLAYLOCK VAN, LLC; 22 PENSERRA SECURITIES LLC; SIEBERT CISNEROS SHANK & CO., L.L.C.; THE 23 WILLIAMS CAPITAL GROUP, L.P.·; CASTLEOAK SECURITIES, L.P.; C.L. KING 24 & ASSOCIATES, INC.; DREXEL HAMILTON, LLC; GREAT PACIFIC SECURITIES; LOOP 25 CAPITAL MARKETS LLC; MISCHLER FINANCIAL GROUP, INC.; SAMUEL A 26 RAMIREZ & COMPANY, INC.; R. -

Lyft's Rapid Surge in the Rideshare Sector

VC20033 Lyft’s Rapid Surge in the Rideshare Sector Joseph Conde University of the Incarnate Word Ryan Lunsford, Ph.D. University of the Incarnate Word VC20033 Abstract Lyft is a rideshare company that has successfully provided convenient and cost-effective transportation services for 22.9 million people across the United States (Iqbal, 2020). The company was established in the Summer of 2012 and by 2019, Lyft increased both the total number of customers and the crucial rides per customer metric leading to a valuation of nearly $24 billion (Madrigal, 2019). The rise began in 2017 when Lyft began increasing its earnings rapidly after pitfalls from its primary competitor, Uber, which had several ethical and legal scandals that received intense media coverage (Carson, 2017). In the subsequent months, Lyft realized a 130% rise in the number of rides from the previous year and launched service in 160 new cities, increasing Lyft’s percentage of market share to 48% (Kerr, 2018). Lyft’s competitive advantage relative to its rivals includes maintaining a transparent, trustworthy reputation, resolving customer and employee concerns quickly and equitably, and providing a safe ride experience that enables riders to conveniently and affordably enjoy their transportation service (Srivastava, 2016). Lyft prioritizes both the relationships that it has with its employees and the industry-leading rates that it charges per ride (Oswald & Revilla, 2020). The company has emphasized improvements to Lyft services by concentrating on customer data analytics, implementing rideshare capabilities to minimize fees, and providing customers a monthly membership subscription that is expected to generate eight times as much revenue in the next 12 years (Forbes, 2018).