C:\Documents and Settings\H0540c8\Local Settings\Temp\FI Interim Report.Wpd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Policy Report Texas Fact Book 2010

Texas Fact Book 2010 Legislative Budget Board LEGISLATIVE BUDGET BOARD EIGHTY-FIRST TEXAS LEGISLATURE 2009 – 2010 DAVID DEWHURST, JOINT CHAIR Lieutenant Governor JOE STRAUS, JOINT CHAIR Representative District 121, San Antonio Speaker of the House of Representatives STEVE OGDEN Senatorial District 5, Bryan Chair, Senate Committee on Finance ROBERT DUNCAN Senatorial District 28, Lubbock JOHN WHITMIRE Senatorial District 15, Houston JUDITH ZAFFIRINI Senatorial District 21, Laredo JIM PITTS Representative District 10, Waxahachie Chair, House Committee on Appropriations RENE OLIVEIRA Representative District 37, Brownsville Chair, House Committee on Ways and Means DAN BRANCH Representative District 108, Dallas SYLVESTER TURNER Representative District 139, Houston JOHN O’Brien, Director COVER PHOTO COURTESY OF HOUSE PHOTOGRAPHY CONTENTS STATE GOVERNMENT STATEWIDE ELECTED OFFICIALS . 1 MEMBERS OF THE EIGHTY-FIRST TEXAS LEGISLATURE . 3 The Senate . 3 The House of Representatives . 4 SENATE STANDING COMMITTEES . 8 HOUSE OF REPRESENTATIVES STANDING COMMITTEES . 10 BASIC STEPS IN THE TEXAS LEGISLATIVE PROCESS . 14 TEXAS AT A GLANCE GOVERNORS OF TEXAS . 15 HOW TEXAS RANKS Agriculture . 17 Crime and Law Enforcement . 17 Defense . 18 Economy . 18 Education . 18 Employment and Labor . 19 Environment and Energy . 19 Federal Government Finance . 20 Geography . 20 Health . 20 Housing . 21 Population . 21 Science and Technology . 22 Social Welfare . 22 State and Local Government Finance . 22 Transportation . 23 Border Facts . 24 STATE HOLIDAYS, 2010 . 25 STATE SYMBOLS . 25 POPULATION Texas Population Compared with the U .s . 26 Texas and the U .s . Annual Population Growth Rates . 27 Resident Population, 15 Most Populous States . 28 Percentage Change in Population, 15 Most Populous States . 28 Texas Resident Population, by Age Group . -

82Nd Leg Members

Representative Party District Phone Number Jose Aliseda R HD35 512-463-0645 Alma Allen D HD131 512-463-0744 Roberto Alonzo D HD104 512-463-0408 Carol Alvarado D HD145 512-463-0732 Rafael Anchia D HD103 512-463-0746 Charles (Doc) Anderson R HD56 512-463-0135 Rodney Anderson R HD106 512-463-0694 Jimmie Don Aycock R HD54 512-463-0684 Marva Beck R HD57 512-463-0508 Leo Berman R HD6 512-463-0584 Dwayne Bohac R HD138 512-463-0727 Dennis Bonnen R HD25 512-463-0564 Dan Branch R HD108 512-463-0367 Fred Brown R HD14 512-463-0698 Cindy Burkett R HD101 512-463-0464 Lon Burnam D HD90 512-463-0740 Angie Chen Button R HD112 512-463-0486 Erwin Cain R HD3 512-463-0650 Bill Callegari R HD132 512-463-0528 Stefani Carter R HD102 512-463-0454 Joaquin Castro D HD125 512-463-0669 Warren Chisum R HD88 512-463-0736 Wayne Christian R HD9 512-463-0556 Garnet Coleman D HD147 512-463-0524 Byron Cook R HD8 512-463-0730 Tom Craddick R HD82 512-463-0500 Brandon Creighton R HD16 512-463-0726 Myra Crownover R HD64 512-463-0582 Drew Darby R HD72 512-463-0331 John Davis R HD129 512-463-0734 Sarah Davis R HD134 512-463-0389 Yvonne Davis D HD111 512-463-0598 Joe Deshotel D HD22 512-463-0662 Joe Driver R HD113 512-463-0574 Dawnna Dukes D HD46 512-463-0506 Harold Dutton D HD142 512-463-0510 Craig Eiland D HD23 512-463-0502 Rob Eissler R HD15 512-463-0797 Gary Elkins R HD135 512-463-0722 Joe Farias D HD118 512-463-0714 Jessica Farrar D HD148 512-463-0620 Allen Fletcher R HD130 512-463-0661 Sergio Munoz, Jr. -

Masarrat Ali Roland Gutierrez Ruth Jones Mcclendon

Roland Gutierrez products sold in local outlets. Masarrat Ali State Representative, District 119 While the successes of this past State Representative, District 122 session are many, we still have more work I entered elective public ahead. Our fight will continue for better Masarrat Ali was born in the service first as a San Antonio City Coun- public schools, affordable public health historic town of Jhansi, India. He was the cilman and currently serve as the State care, effective public safety, and policies to oldest of 9 children all living in a small Representative of District 119 because I help strengthen the economic security of one-room home. His parents saw early wanted to make a difference. I feel that our citizens, reduce homeowners insurance signs of a great future for him and decided if we work together on the issues facing premiums, increase funding of CHIP – to send him to the Aligarh University, one us, we will enjoy a better community. Children’s Health Insurance Program, and of the oldest and most prestigious universi- In the last Legislative Session, Demo- efforts to incentivize a greener moreties of India. crats and Republicans passed a $182 environmentally sound Texas. After earning various degrees in Billion budget, maintaining a $9 Billion Rainy Day A native of San Antonio, Gutierrez is a 1989 the sciences, he earned his Ph.D. in 1981 at the Central Drug Research Fund, increased public school funding, increased graduate of Central Catholic High School. He earned Institute in India due to his research in cancer genes. After spending pay for teachers, increased Texas Grants, as well as his BA in political science from the University of time as an assistant professor in Paris and in furthering his education provided tax relief to small businesses. -

Select Committee on Judicial Interpretation Of

TEXAS HOUSE OF REPRESENTATIVES SELECT COMMITTEE ON JUDICIAL INTERPRETATIONS OF LAW INTERIM REPORT TO THE 77TH TEXAS LEGISLATURE FRED M. BOSSE Chairman Committee Clerk CRAIG P. CHICK Committee On Select Committee on Judicial Interpretations of Law December 5, 2000 Fred M. Bosse P.O. Box 2910 Chairman Austin, Texas 78768-2910 The Honorable James E. "Pete" Laney Speaker, Texas House of Representatives Members of the Texas House of Representatives Texas State Capitol, Rm. 2W.13 Austin, Texas 78701 Dear Mr. Speaker and Fellow Members: The Select Committee on Judicial Interpretations of Law of the Seventy-Sixth Legislature hereby submits its interim report including recommendations for consideration by the Seventy-Seventh Legislature. Respectfully submitted, Fred M. Bosse, Chairman Jim Dunnam Toby Goodman Patricia Gray Peggy Hamric Juan Hinojosa Todd Smith Members: Jim Dunnam; Toby Goodman; Patricia Gray; Peggy Hamric; Juan Hinojosa; Todd Smith; and Burt Solomons Burt Solomons TABLE OF CONTENTS Introduction ...................................................................ii Review of Identified Appellate Court Decisions .........................................2 I. Decisions Clearly Failing to Properly Implement Legislative Purposed ..........3 II. Decisions Finding Two or More Statutes to be in Conflict ..................5 III. Decisions Holding a Statute Unconstitutional ..........................15 IV. Decisions Expressly Finding a Statute to be Ambiguous ..................19 V. Decisions Expressly Suggesting Legislative Action .......................34 -

IDEOLOGY and PARTISANSHIP in the 87Th (2021) REGULAR SESSION of the TEXAS LEGISLATURE

IDEOLOGY AND PARTISANSHIP IN THE 87th (2021) REGULAR SESSION OF THE TEXAS LEGISLATURE Mark P. Jones, Ph.D. Fellow in Political Science, Rice University’s Baker Institute for Public Policy July 2021 © 2021 Rice University’s Baker Institute for Public Policy This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and the Baker Institute for Public Policy. Wherever feasible, papers are reviewed by outside experts before they are released. However, the research and views expressed in this paper are those of the individual researcher(s) and do not necessarily represent the views of the Baker Institute. Mark P. Jones, Ph.D. “Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature” https://doi.org/10.25613/HP57-BF70 Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature Executive Summary This report utilizes roll call vote data to improve our understanding of the ideological and partisan dynamics of the Texas Legislature’s 87th regular session. The first section examines the location of the members of the Texas Senate and of the Texas House on the liberal-conservative dimension along which legislative politics takes place in Austin. In both chambers, every Republican is more conservative than every Democrat and every Democrat is more liberal than every Republican. There does, however, exist substantial ideological diversity within the respective Democratic and Republican delegations in each chamber. The second section explores the extent to which each senator and each representative was on the winning side of the non-lopsided final passage votes (FPVs) on which they voted. -

Interim Report to the 82Nd Texas Legislature

InterIm report to the 82nd texas LegisLature House Committee on State affairS December 2010 ______________________________________________________________________________ HOUSE COMMITTEE ON STATE AFFAIRS TEXAS HOUSE OF REPRESENTATIVES INTERIM REPORT 2010 BURT R. SOLOMONS CHAIRMAN LESLEY FRENCH COMMITTEE CLERK/GENERAL COUNSEL ROBERT ORR DEPUTY COMMITTEE CLERK/POLICY ANALYST ALFRED BINGHAM LEGAL INTERN ______________________________________________________________________________ ______________________________________________________________________________ COMMITTEE ON STATE AFFAIRS TEXAS HOUSE OF REPRESENTATIVES P.O. BOX 2910 • AUSTIN, TEXAS 78768-2910 CAPITOL EXTENSION E2.108 • (512) 463-0814 September 27th, 2010 The Honorable Joe Straus Speaker, Texas House of Representatives Texas State Capitol, Rm. 2W.13 Austin, Texas 78701 Dear Mr. Speaker and Fellow Members: The Committee on State Affairs of the Eighty-First Legislature hereby submits its interim report for consideration by the Eighty-Second Legislature. Respectfully submitted, _______________________ Burt Solomons, Chair _______________________ _______________________ Rep. José Menéndez, Vice-Chair Rep. Byron Cook _______________________ _______________________ Rep. Tom Craddick Rep. David Farabee _______________________ _______________________ Rep. Pete Gallego Rep. Charlie Geren ______________________ _______________________ Rep. Patricia Harless Rep. Harvey Hilderbran ______________________ _______________________ Rep. Delwin Jones Rep. Eddie Lucio III _______________________ -

State Representative Jim Pitts

State Representative Jim Pitts District 10 Chairman, House Appropriations Jim Pitts, of Waxahachie, Texas, was born in Dallas, Texas. He attended Southern Methodist University where he received a bachelor of Business Administration with a major in Accounting, Masters of Business Administration, and a Juris Doctorate. Jim and his late wife, Evelyn Eastham Pitts, have three children, two daughters: Duffy Pitts Bloemendal and Ashley Eastham Pitts, and one son: James Ryan Pitts. He is the proud grandfather of three grandsons. Jim is the son of the late Roy and Agnes Pitts. Jim has a twin brother, John, who lives in Houston, Texas, and a sister, Rosemary Burns, who lives in Henderson County. A fourteen-year member of the Board of Trustees for the Waxahachie Independent School District, Jim was serving as President of the Board when he was elected to the Texas House of Representatives. Other offices include director of Citizens National Bank in Waxahachie, director of Sims Library, a past-president of the Waxahachie Chamber of Commerce and immediate past-president and treasurer of the Board of Trustees of Presbyterian Children's Services. He also currently serves on the Community Advisory Council for the Scottish Rite Learning Center. The people of District 10, which consists of Hill and Ellis Counties, elected Jim as their state representative on November 3, 1992. It was a new district resulting from the 1991 redistricting of the state. During the 1993 session of the Texas Legislature, Jim served on the House Committees on Economic Development and Transportation. The 74th session found him serving on the Criminal Jurisprudence Committee and the Corrections Committee. -

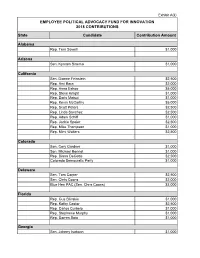

2018 BMS PAC Contributions

Exhibit A(ii) EMPLOYEE POLITICAL ADVOCACY FUND FOR INNOVATION 2018 CONTRIBUTIONS State Candidate Contribution Amount Alabama Rep. Terri Sewell $1,000 Arizona Sen. Kyrsten Sinema $1,000 California Sen. Dianne Feinstein $2,500 Rep. Ami Bera $2,000 Rep. Anna Eshoo $5,000 Rep. Steve Knight $1,000 Rep. Doris Matsui $1,000 Rep. Kevin McCarthy $5,000 Rep. Scott Peters $2,500 Rep. Linda Sanchez $2,500 Rep. Adam Schiff $1,000 Rep. Jackie Speier $2,500 Rep. Mike Thompson $1,000 Rep. Mimi Walters $2,500 Colorado Sen. Cory Gardner $1,000 Sen. Michael Bennet $1,000 Rep. Diana DeGette $2,500 Colorado Democratic Party $1,000 Delaware Sen. Tom Carper $2,500 Sen. Chris Coons $2,000 Blue Hen PAC (Sen. Chris Coons) $3,000 Florida Rep. Gus Bilirakis $1,000 Rep. Kathy Castor $2,500 Rep. Carlos Curbelo $1,000 Rep. Stephanie Murphy $1,000 Rep. Darren Soto $1,000 Georgia Sen. Johnny Isakson $1,000 Sen. David Perdue $2,000 Rep. Buddy Carter $2,500 Iowa Gov. Kim Reynolds $2,000 Sen. Chuck Grassley $2,500 State Sen. Charles Schneider $2,000 State Sen. Tom Shipley $500 Idaho Sen. Mike Crapo $5,000 Illinois Rep. Cheri Bustos $1,000 Rep. Bill Foster $1,000 Rep. Robin Kelly $1,000 Rep. Darin LaHood $1,000 Rep. Pete Roskam $1,000 Rep. Brad Schneider $1,000 Rep. John Shimkus $2,500 Indiana Sen. Mike Braun $1,000 Sen. Joe Donnelly $2,500 Rep. Larry Bucshon $2,500 Rep. Susan Brooks $2,000 Rep. Andre Carson $1,000 Rep. -

Legislative Update

January 29, 2021| Regular Session, Issue 3 | 87th Regular Session Every Friday, this newsletter will keep you up to speed on some of the legislation important to Texas Farm Bureau members that Austin staff are following. Please do not hesitate to contact the appropriate staff with any questions. Legislative Update Water SB 152 and companion HB 668: Relating to the regulation of groundwater conservation districts. Perry, Charles (R) and Harris, Cody (R) Summary: SB 152 and HB 668 empower landowners to protect their constitutional rights from illegal groundwater regulations. Current law does not require enough transparency or provide landowners with reasonable options to change or challenge bad regulations. If property owners are faced with an illegal regulation, they only have one option— to challenge the district’s action in court and take on the risk having to pay the district’s attorney fees. The language in SB 152 and HB 668 is currently being negotiated. The following description of the bills is based upon the current state of negotiations: 1. Requiring notice of a permit or permit amendment that will prevent a neighboring landowner from being able to drill a well on their property or drill at a particular location on their property. The local district will determine how that notice will be provided. This notice will give landowners who will be DIRECTLY affected by the district’s actions an opportunity to decide if they should participate in the permitting process to protect their right to drill a well. In some districts, spacing rules allow a neighbor to drill a well 50 feet from a property line. -

Policy Report Texas Fact Book 2008

Texas Fact Book 2 0 0 8 L e g i s l a t i v e B u d g e t B o a r d LEGISLATIVE BUDGET BOARD EIGHTIETH TEXAS LEGISLATURE 2007 – 2008 DAVID DEWHURST, JOINT CHAIR Lieutenant Governor TOM CRADDICK, JOINT CHAIR Representative District 82, Midland Speaker of the House of Representatives STEVE OGDEN Senatorial District 5, Bryan Chair, Senate Committee on Finance ROBERT DUNCAN Senatorial District 28, Lubbock JOHN WHITMIRE Senatorial District 15, Houston JUDITH ZAFFIRINI Senatorial District 21, Laredo WARREN CHISUM Representative District 88, Pampa Chair, House Committee on Appropriations JAMES KEFFER Representative District 60, Eastland Chair, House Committee on Ways and Means FRED HILL Representative District 112, Richardson SYLVESTER TURNER Representative District 139, Houston JOHN O’Brien, Director COVER PHOTO COURTESY OF SENATE MEDIA CONTENTS STATE GOVERNMENT STATEWIDE ELECTED OFFICIALS . 1 MEMBERS OF THE EIGHTIETH TEXAS LEGISLATURE . 3 The Senate . 3 The House of Representatives . 4 SENATE STANDING COMMITTEES . 8 HOUSE OF REPRESENTATIVES STANDING COMMITTEES . 10 BASIC STEPS IN THE TEXAS LEGISLATIVE PROCESS . 14 TEXAS AT A GLANCE GOVERNORS OF TEXAS . 15 HOW TEXAS RANKS Agriculture . 17 Crime and Law Enforcement . 17 Defense . 18 Economy . 18 Education . 18 Employment and Labor . 19 Environment and Energy . 19 Federal Government Finance . 20 Geography . 20 Health . 20 Housing . 21 Population . 21 Social Welfare . 22 State and Local Government Finance . 22 Technology . 23 Transportation . 23 Border Facts . 24 STATE HOLIDAYS, 2008 . 25 STATE SYMBOLS . 25 POPULATION Texas Population Compared with the U .s . 26 Texas and the U .s . Annual Population Growth Rates . 27 Resident Population, 15 Most Populous States . -

Appendix a – List of Recipients

Preliminary Engineering / Environmental Impact Statement Northwest Corridor LRT Line to Irving and DFW Airport Appendix A – List of Recipients FEDERAL AGENCIES Michael A. McMullen, Stakeholder Manager, Transportation Security Administration Ralston Cox, Administration Director, Advisory Council on Historic Preservation Donald R. Sutherland, NEPA Coordinator, Bureau of Indian Affairs Ann B. Aldrich, Group Manager, Planning, Assessment, and Community Support, Bureau of Land Management Dirk Kempthorne, Secretary of Interior, Department of the Interior Willie Taylor, Director, Office of Environmental Policy and Compliance, Department of the Interior William E. Peterson, Regional Director, Federal Emergency Management Agency Region 6 Sal Deocampo, District Engineer, Federal Highway Administration, Texas Division David Visney, Regional Manager, Federal Railroad Administration Leighton W. Waters, Acting Regional Administrator, General Service Administration, Region 7 Don Babers, U.S. Department of Housing and Urban Development, Dallas Office Colonel John R. Minahan, Commander, U.S. Army Corps of Engineers, Fort Worth District Wayne Lea, Chief, Regulatory Branch, U.S. Army Corps of Engineers, Fort Worth District Rear Admiral Robert Duncan, District Commander, U.S. Coast Guard, 8th District Richard Greene, Administrator, U.S. Environmental Protection Agency, Region 6 Carl Edlund, Division Director, Multimedia Planning and Permitting Division, U.S. Environmental Protection Agency, Region 6 Michael Jansky, EIS Review Coordinator, Compliance Assurance -

Memo (7-31-13) Hazlewood Legacy Act Reimbustments Corrections

TEXAS HIGHER EDUCATION COORDINATING BOARD P.O. Box 12788 Austin, Texas 78711 Fred W. Heldenfels IV CHAIR July 31, 2013 Harold W. Hahn VICE CHAIR Dennis D. Golden, O.D. TO: Ursula Parks, Director SECRETARY OF THE BOARD Legislative Budget Board Alice Schneider STUDENT REPRESENTATIVE Durga D. Agrawal, Ph.D. FROM: Raymund A. Paredes Christopher M. Huckabee Robert W. Jenkins, Jr. Munir Abdul Lalani SUBJECT: Formula for Distributing Hazlewood Legacy Act Reimbursements Janelle Shepard David D. Teuscher, M.D. Raymund A. Paredes COMMISSIONER House Bill 1025, passed by the 83rd Legislature, Regular Session, appropriates $30 OF HIGHER EDUCATION million to reimburse public institutions of higher education for costs associated with 512/ 427-6101 the Hazlewood Legacy Program (TEC 54.341(k)). The Legislation directs the Fax 512/ 427-6127 Coordinating Board to develop a plan to allocate the appropriations according to the Web site: http://www.thecb.state.tx.us proportion of each institution's respective share of the aggregate cost of the exemption for students under the Legacy Program, subject to input by institutions for their respective share, and present the plan to the Legislative Budget Board no later than August 1, 2013. On June 7, all institutions were advised via memo that the allocation of the HB 1025 funding would be based on their FY2012 data regarding Legacy students as they reported in the Hazlewood Exemption Database Report, and that they had until July 15 to review, revise and correct any misreported data. A June 28 notice was sent to Hazlewood contacts to remind them of the deadline.