Daily Grain / Hogs Marketing Outlook Written By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hong Kong Observatory, 134A Nathan Road, Kowloon, Hong Kong

78 BAVI AUG : ,- HAISHEN JANGMI SEP AUG 6 KUJIRA MAYSAK SEP SEP HAGUPIT AUG DOLPHIN SEP /1 CHAN-HOM OCT TD.. MEKKHALA AUG TD.. AUG AUG ATSANI Hong Kong HIGOS NOV AUG DOLPHIN() 2012 SEP : 78 HAISHEN() 2010 NURI ,- /1 BAVI() 2008 SEP JUN JANGMI CHAN-HOM() 2014 NANGKA HIGOS(2007) VONGFONG AUG ()2005 OCT OCT AUG MAY HAGUPIT() 2004 + AUG SINLAKU AUG AUG TD.. JUL MEKKHALA VAMCO ()2006 6 NOV MAYSAK() 2009 AUG * + NANGKA() 2016 AUG TD.. KUJIRA() 2013 SAUDEL SINLAKU() 2003 OCT JUL 45 SEP NOUL OCT JUL GONI() 2019 SEP NURI(2002) ;< OCT JUN MOLAVE * OCT LINFA SAUDEL(2017) OCT 45 LINFA() 2015 OCT GONI OCT ;< NOV MOLAVE(2018) ETAU OCT NOV NOUL(2011) ETAU() 2021 SEP NOV VAMCO() 2022 ATSANI() 2020 NOV OCT KROVANH(2023) DEC KROVANH DEC VONGFONG(2001) MAY 二零二零年 熱帶氣旋 TROPICAL CYCLONES IN 2020 2 二零二一年七月出版 Published July 2021 香港天文台編製 香港九龍彌敦道134A Prepared by: Hong Kong Observatory, 134A Nathan Road, Kowloon, Hong Kong © 版權所有。未經香港天文台台長同意,不得翻印本刊物任何部分內容。 © Copyright reserved. No part of this publication may be reproduced without the permission of the Director of the Hong Kong Observatory. 知識產權公告 Intellectual Property Rights Notice All contents contained in this publication, 本刊物的所有內容,包括但不限於所有 including but not limited to all data, maps, 資料、地圖、文本、圖像、圖畫、圖片、 text, graphics, drawings, diagrams, 照片、影像,以及數據或其他資料的匯編 photographs, videos and compilation of data or other materials (the “Materials”) are (下稱「資料」),均受知識產權保護。資 subject to the intellectual property rights 料的知識產權由香港特別行政區政府 which are either owned by the Government of (下稱「政府」)擁有,或經資料的知識產 the Hong Kong Special Administrative Region (the “Government”) or have been licensed to 權擁有人授予政府,為本刊物預期的所 the Government by the intellectual property 有目的而處理該等資料。任何人如欲使 rights’ owner(s) of the Materials to deal with 用資料用作非商業用途,均須遵守《香港 such Materials for all the purposes contemplated in this publication. -

NASA Analyzes Typhoon Haishen's Water Vapor Concentration 2 September 2020, by Rob Gutro

NASA analyzes typhoon Haishen's water vapor concentration 2 September 2020, by Rob Gutro develop. Water vapor releases latent heat as it condenses into liquid. That liquid becomes clouds and thunderstorms that make up a tropical cyclone. Temperature is important when trying to understand how strong storms can be. The higher the cloud tops, the colder and the stronger the storms. NASA's Terra satellite passed over Haishen on Sept. 2 at 9:35 a.m. EDT (1335 UTC), and the Moderate Resolution Imaging Spectroradiometer or MODIS instrument gathered water vapor content and temperature information. The MODIS image showed highest concentrations of water vapor and coldest cloud top temperatures were around the center of circulation and in a large band of thunderstorms in the northeastern quadrant of the storm. MODIS data also showed coldest cloud top temperatures were as cold as or colder than minus 70 degrees Fahrenheit (minus 56.6 degrees On Sept. 2 at 9:35 a.m. EDT (1335 UTC), NASA’s Terra Celsius) in those storms. Storms with cloud top satellite passed over Typhoon Haishen in the temperatures that cold have the capability to Northwestern Pacific Ocean. Terra found highest produce heavy rainfall. concentrations of water vapor (brown) and coldest cloud top temperatures were around the center and northeastern quadrant. Credits: NASA/NRL On Sept. 2 at 11 a.m. EDT (1500 UTC), Typhoon Haishen had maximum sustained winds near 70 knots (80 mph/130 kph) and it was strengthening. It was centered near latitude 19.5 degrees north and When NASA's Terra satellite passed over the longitude 140.4 degrees east, about 812 nautical Northwestern Pacific Ocean, it gathered water miles east-southeast of Kadena Air Base, Okinawa, vapor data on recently developed Typhoon Japan. -

NASA Eyes Typhoon Haishen's 10 Mile-Wide Eye 3 September 2020, by Rob Gutro

NASA eyes typhoon Haishen's 10 mile-wide eye 3 September 2020, by Rob Gutro Satellite imagery was created using NASA's Worldview product at NASA's Goddard Space Flight Center in Greenbelt, Md. Haishen on Sept. 1 At 5 a.m. EDT (0900 UTC) on Sept. 3, the Joint Typhoon Warning Center (JTWC) in Honolulu, Hawaii noted that Typhoon Haishen was located about 646 nautical miles east-southeast of Kadena Air Base, Okinawa Island, Japan. It was centered near latitude 20.7 degrees north and longitude 137.7 degrees east. Haishen was moving to the northwest with maximum sustained winds of 95 knots (109 mph/176 kph). Haishen is forecast to turn northwest while NASA’s Terra satellite captured a visible image of intensifying to 130 knots (150 mph/241 kph) within Tropical Storm Haishen on Sept. 3 at 0145 UTC (Sept. 2 at 9:45 p.m. EDT). Satellite imagery shows deep the next two days. The storm will pass west of convection and spiral banding of thunderstorms Kyushu, Japan to make landfall in South Korea wrapping tightly around the eye and into a low-level after 4 days. circulation center. Credit: NASA Worldview, Earth Observing System Data and Information System (EOSDIS). Provided by NASA's Goddard Space Flight Center NASA's Terra satellite's visible image of Typhoon Haishen revealed a small "pinhole" eye surrounded by several hundred miles of thunderstorms spiraling around it as it continued moving north though the Northwestern Pacific Ocean. NASA satellite view: Haishen's organization The Moderate Resolution Imaging Spectroradiometer or MODIS instrument that flies aboard NASA's Terra satellite captured a visible image of Typhoon Haishen on Sept. -

ASIA and the PACIFIC Weekly Regional Humanitarian Snapshot 1 - 7 September 2020

ASIA AND THE PACIFIC Weekly Regional Humanitarian Snapshot 1 - 7 September 2020 MYANMAR PAKISTAN Inactive MONGOLIA Watch As monsoon rains continue to batter On 31 August, a locally transmitted Watch COVID-19 case was confirmed in Alert different parts of Pakistan, casualties have risen to over 230 people and 170 the Taung Paw IDP relocation site in DPR KOREA Alert Pyongyang people being injured. Sindh is the most impacted Rakhine state. As part of COVID-19 control El Niño JAPAN province with some 2.27 million people being measures, the Government limited RO KOREA affected. According to the Government, over Kabul La Niña humanitarian assistance to camps and CHINA Kobe AFGHANISTAN 214,000 houses are partially or fully damaged, displacement sites to “essential activities” Islamabad NEPAL BHUTAN LA NIÑA/EL NIÑO LEVEL and around 1 million acres of crops are destroyed. only, such as food assistance, COVID-19 Source: Commonwealth of Australia Bureau of Meteorology Over 23,600 people have been displaced and are response, and provision of water, sanitation T y hosted across nearly 200 relief camps. A rapid T p and hygiene and basic non-food items. C h MYANMAR o needs assessment is under way on the request of M o Movement restrictions and the requirement PAKISTAN a n the Government of Sindh. WHO donated supplies INDIA y H s ai a s for humanitarian actors to undergo testing he worth of around US$126,000 to NDMA for k n 6 6 continue to impact the delivery of assistance BANGLADESH VIET NAM PACIFIC accelerating relief efforts in the flood affected LAO PDR and people’s access to critical services. -

A Season of Unrest Summer Protests Expose Demand for Change, Obstacles

MILITARY/MIDEAST NFL FACES Duterte pardons US If new QBs, coaches Debicki rises to the Marine in killing of plan to limit playbooks, leading lady challenge transgender woman they aren’t telling in Nolan’s latest, ‘Tenet’ Page 4 Back page Page 14 Typhoon pummels South Korea with flooding, damaging winds » Page 12 stripes.com Volume 79, No. 102 ©SS 2020 TUESDAY, SEPTEMBER 8, 2020 50¢/Free to Deployed Areas A season of unrest Summer protests expose demand for change, obstacles BY COLLEEN LONG, KAT STAFFORD AND R.J. RICO Associated Press WASHINGTON — Memorial Day brought the death of George Floyd at the hands of Minneapo- lis police, prompting hundreds of thousands of Americans to take to the streets in protest. Presi- dent Donald Trump called Floyd’s death a “disgrace“ and momen- tum built around policing reform. But by Labor Day, the prospects for federal legislation have evapo- rated. And Trump is seeking to leverage the violence that has erupted around some of the pro- tests to scare white, suburban vot- ers and encourage them to back his reelection campaign. The three-month stretch be- tween the symbolic kickoff and close of America’s summer has both galvanized broad public sup- port for the racial justice move- ment and exposed the obstacles to turning that support into concrete Demonstrators gather to protest political and policy changes. It has the death of George Floyd near the also clarified the choice for voters White House in Washington in June. in the presidential race between ALEX BRANDON / AP SEE PROTESTS ON PAGE 8 Veterans divided about reports Trump disparaged military BY JEFFREY COLLINS AND DAVID CRARY what he heard. -

MEMBER REPORT Japan

MEMBER REPORT Japan ESCAP/WMO Typhoon Committee 15th Integrated Workshop Video Conference – Vietnam 1 – 2 December 2020 CONTENTS I. Overview of Tropical Cyclones which have Affected/impactedMember’s Area since the Last Committee Session 1. Meteorological Assessment (highlighting forecasting issues/impacts) 2. Hydrological Assessment (highlighting water-related issues/impacts) 3. Socio-economic Assessment (highlighting socio-economic and DRR issues/impacts) 4. Regional Cooperation Assessment (highlighting regional cooperation success and challenges) II. Summary of Progress in Priorities supporting Key Result Areas 1. Commencement of five-day forecasts for TDs expected to have TS intensity within 24 hours 2. Upgrade of products on the RSMC Tokyo-Typhoon Center’s Numerical Typhoon Prediction website 3. Updates on JMA's numerical weather prediction system 4. Upgrade of temporal resolution for High-resolution Cloud Analysis Information (HCAI) 5. TCC products and publications related to tropical cyclones 6. Direction of River Basin Disaster Resilience and Sustainability by All 7. Organization of the 9th TC WGH Meeting (online), 22 October 2020 8. Asian Conference on Disaster Reduction (ACDR) 2020 9. Visiting Researchers from ADRC Member Countries I. Overview of tropical cyclones which have affected/impacted Member’s area since the last Committee Session 1. Meteorological Assessment (highlighting forecasting issues/impacts) In 2020, seven tropical cyclones (TCs) of tropical storm (TS) intensity or higher had come within 300 km of the Japanese archipelago as of 7 November*. The country was affected even by those that did not make landfall. The TCs are described below, with their tracks shown in Figure 1. * The track/intensity commentary provided here is subject to change once best-track data are finalized. -

Special Report DPRK Flooding

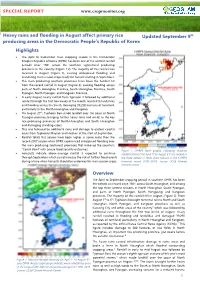

SPECIALSPECIAL REPORT REPORT www.cropmonitor.orgwww.cropmonitor.org Heavy rains and flooding in August affect primary rice Updated September 9th producing areas in the Democratic People’s Republic of Korea Highlights • The April to September main cropping season in the Democratic People’s Republic of Korea (DPRK) has been one of the wettest rainfall periods since 1981 across the southern agricultural producing provinces in the country (Figure 1,2). The majority of this rainfall was received in August (Figure 3), causing widespread flooding and inundating main season crops ready for harvest starting in September. • The main producing southern provinces have been the hardest hit from the record rainfall in August (Figure 3), causing flooding across parts of North Hwanghae Province, South Hwanghae Province, South Pyongan, North Pyongan, and Kangwon Province. • In early August, heavy rainfall from Typhoon 4 followed by additional rainfall through the first two weeks of the month resulted in landslides and flooding across the South, damaging 39,296 hectares of farmland, particularly in the North Hwanghae and Kangwon. • On August 27th, Typhoon Bavi made landfall over the coast of North Pyongan province, bringing further heavy rains and winds to the key rice-producing provinces of North Hwanghae and South Hwanghae and damaging standing crops. • This was followed by additional rains and damage to eastern coastal areas from Typhoons Maysak and Haishen at the start of September. • Rainfall totals this season have been higher in some areas than the record 2007 season when DPRK experienced widespread flooding over the main producing southwest provinces that make up the country’s “Cereal Bowl” with severe food security outcomes. -

TIDES and STORM SURGES in the COAST of TAIWAN a Forecast System Based on Opencoasts

TIDES AND STORM SURGES IN THE COAST OF TAIWAN A forecast system based on OPENCoastS REPORT 42/2021 – DHA/NEC . TIDES AND STORM SURGES IN THE COAST OF TAIWAN A forecast system based on OPENCoastS An EOSC-hub report Lisbon • February 2021 R&D HYDRAULICS AND ENVIRONMENT REPORT 42/2021 – DHA/NEC Title TIDES AND STORM SURGES IN THE COAST OF TAIWAN A forecast system based on OPENCoastS Authors HYDRAULICS AND ENVIRONMENT DEPARTMENT André B. Fortunato Senior Researcher with Habilitation, Estuaries and Coastal Zones Unit Anabela Oliveira Senior Researcher, Information Technology in Water and Environment Research Group Alberto Azevedo Assistant Researcher, Estuaries and Coastal Zones Unit Copyright © LABORATÓRIO NACIONAL DE ENGENHARIA CIVIL, I. P. Av do BrAsil 101 • 1700-066 lisBoA e-mail: [email protected] www.lnec.pt Report 42/2021 File no. 0604/1101/2103901, 0602/1101/21039 TIDES AND STORM SURGES IN THE COAST OF TAIWAN A forecast system based on OPENCoastS TIDES AND STORM SURGES IN THE COAST OF TAIWAN A forecast system based on OPENCoasts Abstract This report describes the implementation and validation of a forecast system to predict sea water levels in the coast of Taiwan. The forecast system was generated using the OPENCoastS platform, in the scope of the EOSC-hub Early Adopters Program. Keywords: Forecasts / OPENCoastS / SCHISM MARÉS E SOBRELEVAÇÕES NA COSTA DE TAIWAN Um sistema de previsão baseado no OPENCoastS Resumo O presente relatório descreve a implementação e a validação de um sistema de previsão oceanográfico, para marés e sobrelevações, para a costa de Taiwan. O sistema de previsão foi desenvolvido com a plataforma OPENCoastS, no âmbito do EOSC-hub Early Adopters Program. -

The Enhanced Phase of the MJO Remains Over the Indian Ocean

The enhanced phase of the MJO remains over the Indian Ocean, with an envelope of anomalous upper- level divergence continuing to extend from the eastern Atlantic into the western Indian Ocean. The suppressed phase remains predominantly over the Pacific, with the strongest upper-level convergence anomalies now centered over the eastern Pacific. The amplitude of the MJO is expected to gradually weaken over the next several days, with increased uncertainty of the state of the MJO heading into mid- September. Models favor continued easterly wave activity and support an active Atlantic basin during the outlook periods. Following the formation of TC's Omar and Nana in the Atlantic earlier this week, no new tropical cyclones (TC) have formed across the basin since earlier this week TS Omar peaked at Tropical Storm intensity to the northwest of Bermuda and since weakened and become post-tropical as it continues to track east in the open waters of the Atlantic. In the Caribbean, Hurricane Nana strengthened to a category 1 Hurricane prior to making landfall over southern Belize, triggering heavy rainfall and localized flooding over northern Honduras. As the remnant low is expected to continue to track west over Guatemala and into the Pacific, there is an increased chance that the low will reform over the next five days according to the National Hurricane Center (NHC), and a moderate confidence area is added to the outlook. With the peak of the Atlantic Hurricane season upon us, all eyes remain focused in the Main Development Region (MDR) with multiple tropical waves continuing to propagate off West Africa. -

NASA Satellites Catch Typhoon Haishen Before and After Landfall 8 September 2020, by Rob Gutro

NASA satellites catch Typhoon Haishen before and after landfall 8 September 2020, by Rob Gutro located within a tropical cyclone. Tropical cyclones do not always have uniform strength, and some sides have stronger sides than others. The stronger the storms, the higher they extend into the troposphere, and they have the colder cloud temperatures. NASA provides that data to forecasters so they can incorporate in their forecasts. On Sept. 3 at 11:53 p.m. EDT (Sept. 4 at 0353), NASA's Aqua satellite analyzed the storm using the Atmospheric Infrared Sounder or AIRS instrument. At the time, Haishen was a Super Typhoon with maximum sustained winds near 135 knots (155 mph/250 kph) and strengthened to a Category 5 hurricane/typhoon later that day. On Sept. 3 at 11:53 p.m. EDT (Sept. 4 at 0353) NASA’s AIRS found coldest cloud top temperatures as cold Aqua satellite analyzed Typhoon Haishen using the as or colder than minus 80 degrees Fahrenheit AIRS found coldest cloud top temperatures as cold as or (minus 62.2 degrees Celsius) around a very clear colder than minus 80 degrees Fahrenheit (minus 62.2 and open eye. NASA research has shown that degrees Celsius) around a very clear and open eye. cloud top temperatures that cold indicate strong Credit: NASA JPL/Heidar Thrastarson storms that have the capability to create heavy rain. Formerly a typhoon, Tropical Storm Haishen made landfall in South Korea on Monday, Sept. 2 and continued moving north toward China. NASA's Aqua satellite provided an infrared view of Haishen as a typhoon before landfall and a visible image after landfall as an extra-tropical storm. -

'MGTO Role Remains Unchanged' Despite Move to Economy Secretariat

FOUNDER & PUBLISHER Kowie Geldenhuys EDITOR-IN-CHIEF Paulo Coutinho www.macaudailytimes.com.mo TUESDAY T. 26º/ 31º Air Quality Good MOP 8.00 3614 “ THE TIMES THEY ARE A-CHANGIN’ ” N.º 08 Sep 2020 HKD 10.00 AFTER A LENGTHY PUBLIC DEBATE, TRAVEL BUBBLE: HEALTH CODE CHINA LAUNCHED A NEW OPTICAL CHILDREN UNDER THE AGE OF TO RESUME ONCE HK BRINGS REMOTE-SENSING SATELLITE THREE WILL BE ALLOWED BACK TO FROM THE TAIYUAN LAUNCH PRESCHOOL AS EARLY AS SEP 21 COVID-19 UNDER CONTROL CENTER IN SHANXI PROVINCE P5 P5 P6 India’s coronavirus cases surged to 4.2 million, the second-highest total in the world as urban metro trains partially resume service in the capital New Delhi and other states. The 90,802 cases added in the past 24 hours pushed India’s total to 4,204,614, passing Brazil, which has more than XU 4.1 million, according to a tally by Johns Hopkins University. More than 6.2 million people in the United States have been infected. India’s Health Ministry also reported 1,016 deaths YINGZHEN from COVID-19 in the past 24 hours, taking fatalities to 71,642, the third-highest national death toll. LEAVES AP PHOTO FORUM China Organizers reported strong turnout at an event in Beijing billed as the first hybrid online and in-person trade show during the coronavirus pandemic. A total of 95,000 visitors MACAO attended the 2020 China International Fair for Trade in Services on Saturday, the first full day of the exhibition. The fair is being P12 held as China’s economy TOP POST has largely restarted, despite the devastating blow to many industries from a months-long shutdown and the loss of domestic demand and foreign orders. -

2021 DEFENSE of JAPAN Defense White Paper DIGEST

2021 DEFENSE OF Pamphlet JAPAN On the Publication of Defense of Japan 2021 Minister of Defense KISHI Nobuo In the year 2020, not only did the entire world face unprecedented difficulties due to COVID-19, but various security challenges and destabilizing factors became more tangible and acute, and the international order based on universal values, which has underpinned the peace and prosperity of the international community, has been greatly tested. Looking at the situation around Japan, China has continued its unilateral attempts to change the status quo in the East and South China Seas. China Coast Guard (CCG) vessels are sighted almost daily in the contiguous zone surrounding the Senkaku Islands, an inherent part of the territory of Japan, and repeatedly intrude into Japan’s territorial waters. Furthermore, there have also been incidents of CCG vessels approaching Japanese fishing boats while intruding into Japanese territorial waters, further making the situation serious. Against this backdrop, China entered into force the China Coast Guard Law in February 2021. The CCG Law includes problematic provisions in terms of their inconsistency with international law. Sources of inconsistency include, among others, ambiguity as to geographical areas the CCG Law applies and how the rules governing the use of weapons are implemented. The CCG Law must not be allowed to infringe on the legitimate interests of the relevant countries including Japan. Furthermore, the raising of tensions in the East China Sea and other sea areas is completely unacceptable. In addition, North Korea is proceeding with ballistic missile development at an extremely rapid pace. It launched ballistic missiles of a new type in 2021, and such military trends, including nuclear and missile development, pose grave and imminent threats to Japan’s security.