Coin Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Coinage of Akragas C

ACTA UNIVERSITATIS UPSALIENSIS Studia Numismatica Upsaliensia 6:1 STUDIA NUMISMATICA UPSALIENSIA 6:1 The Coinage of Akragas c. 510–406 BC Text and Plates ULLA WESTERMARK I STUDIA NUMISMATICA UPSALIENSIA Editors: Harald Nilsson, Hendrik Mäkeler and Ragnar Hedlund 1. Uppsala University Coin Cabinet. Anglo-Saxon and later British Coins. By Elsa Lindberger. 2006. 2. Münzkabinett der Universität Uppsala. Deutsche Münzen der Wikingerzeit sowie des hohen und späten Mittelalters. By Peter Berghaus and Hendrik Mäkeler. 2006. 3. Uppsala universitets myntkabinett. Svenska vikingatida och medeltida mynt präglade på fastlandet. By Jonas Rundberg and Kjell Holmberg. 2008. 4. Opus mixtum. Uppsatser kring Uppsala universitets myntkabinett. 2009. 5. ”…achieved nothing worthy of memory”. Coinage and authority in the Roman empire c. AD 260–295. By Ragnar Hedlund. 2008. 6:1–2. The Coinage of Akragas c. 510–406 BC. By Ulla Westermark. 2018 7. Musik på medaljer, mynt och jetonger i Nils Uno Fornanders samling. By Eva Wiséhn. 2015. 8. Erik Wallers samling av medicinhistoriska medaljer. By Harald Nilsson. 2013. © Ulla Westermark, 2018 Database right Uppsala University ISSN 1652-7232 ISBN 978-91-513-0269-0 urn:nbn:se:uu:diva-345876 (http://urn.kb.se/resolve?urn=urn:nbn:se:uu:diva-345876) Typeset in Times New Roman by Elin Klingstedt and Magnus Wijk, Uppsala Printed in Sweden on acid-free paper by DanagårdLiTHO AB, Ödeshög 2018 Distributor: Uppsala University Library, Box 510, SE-751 20 Uppsala www.uu.se, [email protected] The publication of this volume has been assisted by generous grants from Uppsala University, Uppsala Sven Svenssons stiftelse för numismatik, Stockholm Gunnar Ekströms stiftelse för numismatisk forskning, Stockholm Faith and Fred Sandstrom, Haverford, PA, USA CONTENTS FOREWORDS ......................................................................................... -

Compte Rendu 62/2015 Publié Par Le Secrétariat Du Conseil

C O N S E J O I N T E R N A C I O N A L D E N U M I S M Á T I C A I N T E R N A T I O N A L N U M I S M A T I C C O U N C I L C O N S E I L I N T E R N A T I O N A L D E N U M I S M A T I Q U E I N T E R N A T I O N A L E R N U M I S M A T I S C H E R R A T C O N S I G L I O I N T E R N A Z I O N A L E D I N U M I S M A T I C A compte rendu 62/2015 Publié par le Secrétariat du Conseil Layout and proofreading EN /FR : Jan MOENS (KBGN - SRNB ) INTERNATIINTERNATIOOOONALNAL NUMISNUMISMMMMATICATIC COUNCIL CCCOCOOONSEILNSEIL INTERNATIINTERNATIOOOONALNAL DDDEDE NUMISNUMISMMMMATIQUEATIQUE TABLE OF CONTENTS – SOMMAIRE COMPOSITION OF THE COMMITTEE 1 STATUTS|CONSTITUTION 3 LAW AND PRACTICE REGARDING COIN FINDS Das Eigentum an (Münz -)Schatzfunden in der Bundesrepublik Deutschland, by Ralf Fischer zu Cramburg 15 GREAT NUMISMATISTS Jean Svoronos (1863 -1922), by Carmen Arnold-Biucchi 25 Christian Jürgensen Thomsen (1788 -1865), by Jorge Steen Jensen 31 NUMISMATIC COLLECTIONS Australian Numismatic Collections, by Kenneth Sheedy 41 The Netherlands – Vicissitudes of a Collection. -

Annual Report 2018 1

ANNUAL REPORT 2018 _______________________________________________________________________________ - Annual report 2018 1 CONTENTS CORPORATE BODIES 4 REPORT ON OPERATIONS 5 CONSOLIDATED NON-FINANCIAL STATEMENT (LEGISLATIVE DECREE 254/2016) 38 INDIPENDENT AUDITORS’ REPORT 112 CONSOLIDATED FINANCIAL STATEMENTS AT 31 JANUARY 2019 115 NOTES TO THE CONSOLIDATED STATEMENT OF FINANCIAL POSITION 159 NOTES TO THE CONSOLIDATED INCOME STATEMENT 183 RELATIONS WITH RELATED PARTIES 192 APPENDICES TO THE CONSOLIDATED FINANCIAL STATEMENTS 199 INDIPENDENT AUDITORS’ REPORT 205 SEPARATE FINANCIAL STATEMENTS OF OVS SPA AT 31 JANUARY 2019 211 _______________________________________________________________________________ - Annual report 2018 2 COMPANY INFORMATION Registered office of the Parent Company OVS S.p.A. Via Terraglio 17, 30174 - Venice - Mestre Legal details of the Parent Company Authorised share capital €227,000,000.00 Subscribed and paid-up share capital €227,000,000.00 Venice Companies Register no. 04240010274 Tax and VAT code 04240010274 Corporate website: www.ovscorporate.it _______________________________________________________________________________ - Annual report 2018 3 CORPORATE OFFICERS Board of Directors Nicholas Stathopoulos Chairman Stefano Beraldo Chief Executive Officer and General Manager Gabriele Del Torchio (1) (2) Director Elena Garavaglia * (1) (2) Director Alessandra Gritti ** Director Heinz Jürgen Krogner-Kornalik (2) Director Massimiliano Magrini ** Director Chiara Mio (1) Director Giovanni Tamburi ** (2) Director * Elena -

COMPANY 2016 12 6 ENG.Pdf

COMPANYPROFILE / IN _ about us p. 02 _ mission p. 03 _ network p. 04 _ direct stores network p. 05 _ multi-concept stores p. 06 _ beauty and cosmetics p. 07 DEX _ coincasa home decoration p. 08 _ coin excelsior p. 09 _ coin excelsior brand portfolio p. 10 _ communication network p. 11 _ videwall Milano 5 Giornate p. 12 _ crm & relationship management p. 13 _ new digital media p. 14 _ store window display p. 15 _ tv, radio & digital totems p. 16 _ corporate social responsability p. 17 _ events p. 18 _ new designers at coin excelsior p. 19 _ in-store events p. 20 _ press reviews p. 23 / 01. ABOUT US Established in 1926, Coin is the first Italian department Store: * € 362.2 MILLION NET SALES IN 2015; * 38 DIRECTLY OWNED STORES IN ITALY, IN THE MOST IMPORTANT ITALIAN CITIES AND DOWNTOWN SHOPPING AREAS; * PORTFOLIO OF MORE THAN 1000 BRANDS; * 34.7 MILLION VISITORS EVERY YEAR; * 9.7 MILLION RECEIPTS AND 21.6 MILLION ITEMS OF CLOTHING SOLD. / 02. MISSION We inspire and enable people to create their own style. We are committed to selecting the best Brands in apparel, cosmetics, accessories and home decoration. We strive to create a vibrant, contemporary setting, enriched by the professional expertise of our sales assistants. / 03. NETWORK High value locations: *38 CENTRALLY LOCATED STORES; *A TOTAL SALE SURFACE AREA OF NEARLY 114,600 SQM; *AVERAGE SELLING SURFACE: 2,865 SQM; *OVER 3.5 MILLION CUSTOMERS PURCHASE AT LEAST ONCE A YEAR. / 04. Bari Casamassima DIRECT Napoli Bergamo Padova Bologna Rizzoli Parma Brescia STORES Piacenza Cagliari Rimini Campi Bisenzio NETWORK Roma Bufalotta Carugate Roma Cinecitta Catania Coin Excelsior Roma Cola Di Rienzo Como Roma S.Giovanni Ferrara Roma Termini Firenze Sanremo Genova Sassari Lecce Torino Le Gru Livorno Treviso Messina Trieste Mestre Varese Milano 5 Giornate Coin Excelsior Venezia Milano Cantore Verona Milano Vercelli Vicenza / 05. -

The Denarius – in the Middle Ages the Basis for Everyday Money As Well

The Denarius – in the Middle Ages the Basis for Everyday Money as well In France the coin was known as "denier," in Italy as "denaro," in German speaking regions as "Pfennig," in England as "penny," – but in his essence, it always was the denarius, the traditional silver coin of ancient Rome. In his coinage reform of the 780s AD, Charlemagne had revalued and reintroduced the distinguished denarius as standard coin of the Carolingian Empire. Indeed for the following 700 years, the denarius remained the major European trade coin. Then, in the 13th century, the Carolingian denarius developed into the "grossus denarius," a thick silver coin of six denarii that was later called "gros," "grosso," "groschen" or "groat." The denarius has lasted until this day – for instance in the dime, the North American 10 cent-coin. But see for yourself. 1 von 15 www.sunflower.ch Frankish Empire, Charlemagne (768-814), Denarius (Pfennig), after 794, Milan Denomination: Denarius (Pfennig) Mint Authority: Emperor Charlemagne Mint: Milan Year of Issue: 793 Weight (g): 1.72 Diameter (mm): 20.0 Material: Silver Owner: Sunflower Foundation The pfennig was the successor to the Roman denarius. The German word "pfennig" and the English term "penny" correspond to the Latin term "denarius" – the d on the old English copper pennies derived precisely from this connection. The French coin name "denier" stemmed from the Latin term as well. This pfennig is a coin of Charlemagne, who in 793/794 conducted a comprehensive reform of the Carolingian coinage. Charlemagne's "novi denarii," as they were called in the Synod of Frankfurt in 794, bore the royal monogram that was also used to authenticate official documents. -

The Case of Veneto and Verona

Dario Calomino Processing coin finds data in Northern Italy: the case of Veneto and Verona ICOMON e-Proceedings (Utrecht, 2008) 3(2009), 55 - 62 Downloaded from: www.icomon.org 55 Processing coin finds data in Northern Italy: the case of Veneto and Verona Dario Calomino Università degli Studi di Verona [email protected] The aim of this paper is to present the numismatic research of the Centro Regionale di Catalogazione dei Beni Numismatici del Veneto, a programme of cataloguing and processing coin finds and numismatic collections data in the region of Veneto, supervised by Prof. Giovanni Gorini of the University of Padua. The project takes place with the cooperation of both municipal and state museums, gathering together all the coins found in the region or belonging to historical collections. The coin finds are published in the multi-volume series of the Ritrovamenti monetali di età romana in Veneto, and the entire numismatic heritage of the museums of Veneto is catalogued in a numismatic computer database that will be available on the regional website. This paper offers some examples of the filing scheme for both the volumes and the database, illustrating research tools that can be used to find a specimen or to process data for further studies. Some results of these projects are also shown in the paper. The publication plan for coin finds and numismatic research in the town of Verona is also illustrated, in particular the forthcoming volume covering the coins found in the historical centre. Since 1986 the Centro Regionale di Catalogazione dei Beni Numismatici del Veneto (Regional Centre for Cataloguing the Numismatic Heritage in Veneto) has promoted a wide programme of cataloguing and processing data concerning coin finds in the region of Veneto, supervised by Prof. -

World Numismatics Newsletter U.S

May / June 2016 WORLD NUMISMATICS NEWSLETTER U.S. MEXICAN NUMISMATIC ASSOCIATION WORLD NUMISMATICS WILL BE 2016 CONVENTION AND EDUCATIONAL FORUM IN LONG BEACH - JUNE 9-11, 2016 AT LONG BEACH CONVENTION CENTER Stop by at the convention at Booth 922 and meet Benjamin Bell, Kent Ponterio, Cory Frampton and Max Keech. We will be showing our newest inventory from recent trips to Europe along with our regular Mexican and Latin inventories. VALIDATION STAMPS OF THE WAR FOR INDEPENDENCE, PART 2 By Max A. Keech In Part 1 of this article, in the last issue of the journal, I The fifth annual convention will be held Thursday through suggested three “rules” that this series follows which can guide Saturday, October 6-8, 2016 at the Hilton Scottsdale Resort, us to a better understanding of the mint casting stamps and 6333 N Scottsdale Road, Scottsdale, Arizona. The schedule of counterstamps of the period. A quick summary of the rules events is as follows: are: (1) stamps are either casting stamps originating from the casting process or counterstamps used to validate provisional/ Thursday necessity coins already in circulation, (2) they were applied only between 1811 and 1814 and (3) only provisional/ Dealer Setup 12:00-5:00pm necessity coinage was counterstamped (a detailed review of Early Entry 2:00-5:00pm ($10 Donation) these rules can be found on pages 14-16 of Part 1 in the Welcome Party 5:00-7:00pm December 2014 issue). Part 1 also surveyed the most often Silent Auction encountered Royalist issues. To conclude, we will review a Awards Ceremony cross-section of the Insurgent validation stamps. -

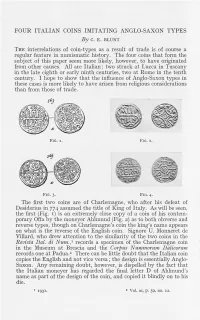

FOUR ITALIAN COINS IMITATING ANGLO-SAXON TYPES the Interrelations of Coin-Types As a Result of Trade Is of Course a Regular Feat

FOUR ITALIAN COINS IMITATING ANGLO-SAXON TYPES By C. E. BLUNT THE interrelations of coin-types as a result of trade is of course a regular feature in numismatic history. The four coins that form the subject of this paper seem more likely, however, to have originated from other causes. All are Italian; two struck at Lucca in Tuscany in the late eighth or early ninth centuries, two at Rome in the tenth century. I hope to show that the influence of Anglo-Saxon types in these cases is more likely to have arisen from religious considerations than from those of trade. FIG. I. FIG. 2. Hfit 1-- FIG. 3. FIG. 4. The first two coins are of Charlemagne, who after his defeat of Desiderius in 774 assumed the title of King of Italy. As will be seen, the first (Fig. 1) is an extremely close copy of a coin of his contem- porary Off a by the moneyer Ahlmund (Fig. 2) as to both obverse and reverse types, though on Charlemagne's coin the king's name appears on what is the reverse of the English coin. Signore U. Monneret de Villard, who drew attention to the similarity of the two coins in the Revista Ital. di Num.,1 records a specimen of the Charlemagne coin in the Museum at Brescia and the Corpus Nummorum Italicorum records one at Padua.2 There can be little doubt that the Italian coin copies the English and not vice versa; the design is essentially Anglo- Saxon. Any remaining doubt, however, is dispelled by the fact that the Italian moneyer has regarded the final letter D of Ahlmund's name as part of the design of the coin, and copied it blindly on to his die. -

The Coins of Venice by Peter E

The Coins of Venice by Peter E. Lewis View of Venice. (Wikimedia Commons) HE coins of Venice are a fascinating Tarea of study, especially if you have a strong Christian faith, because they nearly always have designs relating to Christi - anity. The people of northern Italy had been converted to Christianity by 400 AD, and when the barbarian invasions occurred in the 5 th and 6 th centuries, the people living near the coast fled to islands in the large lagoon at the north-west tip of the Adriatic Sea. Eventually the islands in the centre of the lagoon became the city of Venice. (Figure 1) At first Venice continued to be under Byzantine control, but as Constantinople, the capital of the Byzantine Empire, was far to the east, Venice came more under the influence of the Francs, whose empire was founded by Charlemagne (768-814 AD) and included most of Italy. By about 840 AD, however, the city had established a largely independent position between the great empires in the east and the west, and this greatly favoured its development as a centre of trade for the whole of Europe. Figure 1 – Painting of Venice by Canaletto, c. 1730, on a coin of the Cook Islands issued in 2011. Figure 2 – Denier (Italian: denaro) of Louis the Diameter 55 mms. The painting is entitled, ‘The Bucintoro returning to the Molo on Ascen sion Pious (814-840 AD). Diameter 21 mms. Obverse: Day’. The Bucintoro was the doge’s ceremonial barge on which he attended a ritual called + H LVDOVVICVS IMP. -

Padova Summer Handbook

PADUA ITALY Summer 2012 Handbook BU in Padua 1 Getting Ready to Go A Sense of Purpose Helpful Websites 2 Academics Courses Textbooks Academic Policies and Procedures Libraries 2 What to Bring Handbooks Passport and Student Visa Student Identification Calling Card/Phones Clothing Prescription/Drug Store Items Appliances Computers/E-mail Miscellaneous 4 Money Matters Program Fees Cash Banking 5 Arrival Travel Arrangements Orientation 6 Housing Housing Assignments Italian Households Family Housing Guidelines 8 Life in Padua Food and Dining Shopping Entertainment Transportation: Getting Around Padua Communication/Mail Media Padua-area Hotels and Hostels Outside of Padua 11 Names and Numbers 2 Boston University International Programs Padua Getting Ready to Go “...Per Il grande desiderio che avevo Divedere la bella Padua, culla delle arti Padua (known to Italians as Padova) claims to be the oldest Sono arrivato... city in northern Italy. Ancient Padua, inhabited by Veneti, Ed a Padua sono venuto, come chi lascia thrived thanks to its excellent breed of horses and the wool of its sheep. Its men fought for the Romans at Cannae, and Uno stagno per tuffarsi nel mare.” the city (a Roman municipium since 45 BC) became so powerful that it reportedly was able to raise two hundred –Shakespeare thousand fighting men. The historian Livy was born in La Bisbetica Domata, Atto 1, Scena 1 Padua, and Padua was the first home to one of the most famous architects of the Renaissance, Andrea Palladio. Padua is also the setting for most of the action in “…For the great desire I had Shakespeare's “The Taming of the Shrew.” To see fair Padua, Nursery of Arts. -

Lr100 — Rinascente · Stories of Innovation

Milano, 2 maggio 2017 LR100 — RINASCENTE · STORIES OF INNOVATION Il Comune di Milano | Cultura, Palazzo Reale e la Rinascente celebrano i 100 anni del nome della grande azienda milanese, con una mostra che racconta un secolo di storia del costume e della cultura di Milano e dell’Italia. A Palazzo Reale dal 24 maggio al 24 settembre. Quest’anno la Rinascente festeggia i 100 anni del suo nome, ideato da Gabriele D’Annunzio su commissione di Senatore Borletti, che acquistò i grandi magazzini Bocconi nel 1917, promuovendone la rinascita. Cominciava così una storia fatta di passione, talento e capacità di visione tale da suscitare, a partire dai primi del Novecento, un impatto innovativo sui modelli di consumo e sull’evoluzione che portò Milano ad affermarsi come motore economico dell’Italia postunitaria. Per celebrare l’evento il Comune di Milano | Cultura, Palazzo Reale e la Rinascente, hanno deciso di raccontare questa storia, con una mostra nelle sale dell’Appartamento del Principe al piano nobile, dal 24 maggio al 24 settembre 2017. Attraverso un’eccezionale varietà e quantità di opere d’arte, grafica, oggetti di design, immagini storiche e contributi inediti, il pubblico potrà scoprire come la Rinascente abbia scritto capitoli importanti nella storia del costume, della comunicazione e della grande distribuzione. Sin dalle sue origini, infatti si caratterizzò come laboratorio dove sperimentare le novità che provenivano dal resto d’Europa. Il modello di vendita innovativo, derivato dalle iniziali esperienze francesi, con la merce esposta negli scaffali a prezzo fisso, non solo fu la chiave di volta di un’economia moderna, ma produsse decisivi cambiamenti nella vita quotidiana della nascente società dei consumi, creando nuovi miti e archetipi nel gusto, rivoluzionando l’immagine femminile e maschile e stimolando la nascita dei sistemi produttivi legati alla moda e al design, pilastri fondanti del Made in Italy. -

Inside View on the International Beauty Industry January 21 - February 3, 2016 #124

www.bwconfidential.com The inside view on the international beauty industry January 21 - February 3, 2016 #124 CONFIDENTIAL CONFIDENTIAL CONFIDENTIAL Comment Inside The buzz 2 The millennial maze News roundup eauty companies have made the millennial consumer Netwatch 7 Ba key target. Many brands are going out of their way to attract 18 to 34 year olds on social media—with Social media monitor varying degrees of success—and are looking at how to better design, market and even price their products to Interview 8 appeal to these consumers. La Prairie Group vice president of However, analysts say that while brands are making travel retail Laurent Marteau efforts when it comes to millennials, there is a disconnect at the point of sale. They maintain that traditional Insight 10 beauty stores are not attractive enough to bring in these Prestige retailing in Italy consumers, and that millennials do not feel at ease shopping in a perfumery or a department store. Young consumers are either buying elsewhere (for example, Store visit 13 online or in branded standalone stores) or are simply not buying beauty at all. Grupo Boticário’s The Beauty Box This criticism has seen some retailers look to open more youth-friendly stores flagship, São Paulo, Brazil complete with interactive elements and digital features. The problem however, is that these special features are usually only to be seen in key flagship doors, while many of the local perfumeries do not get the same treatment and continue to have a tough time attracting the young consumer. Oonagh Phillips Editor in Chief [email protected] Meet the BW Confidential team at: l PCD, Paris, Feb 3-4 l Cosmopack, Bologna, March 17-20 l Cosmoprof Worldwide, Bologna, March 18-21 News headlines daily on www.bwconfidential.com @BWCbeautynews News roundup At a glance..