Estate Analyst®

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OFFICIAL RECORD of PROCEEDINGS Wednesday, 16 December 2020 the Council Met at Eleven O'clock

LEGISLATIVE COUNCIL ― 16 December 2020 2375 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 16 December 2020 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE ANDREW LEUNG KWAN-YUEN, G.B.M., G.B.S., J.P. THE HONOURABLE ABRAHAM SHEK LAI-HIM, G.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, G.B.S., J.P. THE HONOURABLE JEFFREY LAM KIN-FUNG, G.B.S., J.P. THE HONOURABLE WONG TING-KWONG, G.B.S., J.P. THE HONOURABLE STARRY LEE WAI-KING, S.B.S., J.P. THE HONOURABLE CHAN HAK-KAN, B.B.S., J.P. THE HONOURABLE CHAN KIN-POR, G.B.S., J.P. DR THE HONOURABLE PRISCILLA LEUNG MEI-FUN, S.B.S., J.P. THE HONOURABLE WONG KWOK-KIN, S.B.S., J.P. THE HONOURABLE MRS REGINA IP LAU SUK-YEE, G.B.S., J.P. THE HONOURABLE PAUL TSE WAI-CHUN, J.P. THE HONOURABLE MICHAEL TIEN PUK-SUN, B.B.S., J.P. THE HONOURABLE STEVEN HO CHUN-YIN, B.B.S. 2376 LEGISLATIVE COUNCIL ― 16 December 2020 THE HONOURABLE FRANKIE YICK CHI-MING, S.B.S., J.P. THE HONOURABLE YIU SI-WING, B.B.S. THE HONOURABLE MA FUNG-KWOK, G.B.S., J.P. THE HONOURABLE CHAN HAN-PAN, B.B.S., J.P. THE HONOURABLE LEUNG CHE-CHEUNG, S.B.S., M.H., J.P. THE HONOURABLE ALICE MAK MEI-KUEN, B.B.S., J.P. THE HONOURABLE KWOK WAI-KEUNG, J.P. THE HONOURABLE CHRISTOPHER CHEUNG WAH-FUNG, S.B.S., J.P. -

Complete Press

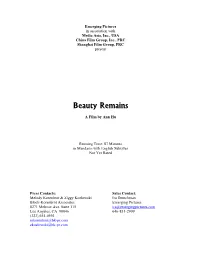

Emerging Pictures in association with Media Asia, Inc., USA China Film Group, Inc., PRC Shanghai Film Group, PRC present Beauty Remains A Film by Ann Hu Running Time: 87 Minutes in Mandarin with English Subtitles Not Yet Rated Press Contacts: Sales Contact: Melody Korenbrot & Ziggy Kozlowski Ira Deutchman Block-Korenbrot Associates Emerging Pictures 8271 Melrose Ave. Suite 115 [email protected] Los Angeles, CA 90046 646-831-2909 (323) 655-0593 [email protected] [email protected] Beauty Remains The Cast Fei .....................................................................................................................ZHOU XUN Ying..................................................................................................................VIVIAN WU Huang...................................................................................................... WANG ZHI WEN The Woman Gambler............................................................................................. LISA LU Bai........................................................................................................... ZHU MAN FANG Xiao Tian .....................................................................................................SHEN CHANG Li Zhu...................................................................................................... WANG JIAN JUN Niu Niu................................................................................................................... XU JING Lawyer ..................................................................................................... -

In 1994, Anna Nicole Smith and the Billionaire J

Is there a guarantee that my Will cannot be challenged? Nina Wang, Asia's richest woman, died on 3rd April 2007. It was said that her estate was worth $4.2 billion. Days after her death, newspapers around the world reported that Wang named one individual as the sole beneficiary in her will. It was further reported or alleged that this individual was not a member of her own family nor that of her late husband’s. As the widow of Hong Kong business tycoon, Teddy Wang, Nina was at the center of one of the most well publicised disputes in history over the succession of a business. This dispute pitted Nina Wang against her father-in-law, Wang Din-shin. Chinachem Group, the subject matter of the dispute, was established by Teddy Wang as a pharmaceutical company but eventually became one of Hong Kong's largest and most prominent companies. Teddy and Nina have no children. As the story goes, in 1990 Teddy Wang was kidnapped and later thrown into the sea by his abductors. After his disappearance, Nina took the helm of Chinachem. In 1999, nine years after his disappearance, Teddy Wang was declared dead, although his body was never found. The fight over the late Teddy's estate which began sometime in 2000 was not because he did not leave behind a will. There were two wills and the court had the difficult task of determining which was the last valid will. Din-Shin, Teddy’s father presented a 1968 will, in which Teddy left him the entire estate after he discovered that his wife was cheating on him. -

Final Report on a Discreet Due Diligence Investigation Into Ng Lap

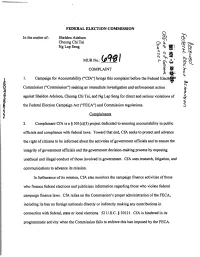

FEDERAL ELECTION COMMISSION CN ^ In the matter of: Sheldon Adelson & Cheung Chi Tai O . S- NgLap Seng § ^ :;i ^ c ^ X MURNo.: I w' ^ R Oi COMPLAINT ^ § k 1. Campaign for Accountability ("CfA") brings this complaint before the Federal Electii!®'' Commission ("Cortimission") seeking an immediate investigation and enforcement action against Sheldon Adelson, Cheung Chi Tai, and Ng Lap Seng for direct and serious violations of ^ the Federal Election Campaign Act ("FECA") and Commission regulations. i Complainants 2. Complainant CfA is a § 501(c)(3) project dedicated to ensuring accountability in public officials and compliance with federal laws. Toward that end, CfA seeks to protect and advance the right of citizens to be informed about the activities of government officials and to ensure the integrity of government officials and the government decision-making process by exposing unethical and illegal conduct of those involved in government. CfA uses research, litigation, and communications to advance its mission. In furtherance of its mission, CfA also monitors the campaign finance activities of those who finance federal elections and publicizes information regarding those who violate federal campaign finance laws. CfA relies on the Commission's proper administration of the FECA, including its ban on foreign nationals directly or indirectly making any contributions in connection with federal, state or local elections. 52 U.S.C. § 30121. CfA is hindered in its programmatic activity when the Commission fails to enforce this ban imposed by the FECA. 3. Anne L. Weismann is the executive director of CfA, a citizen of the United States, and a registered voter and resident of the State of Maryland. -

Guardians of Fortune Accountants Take Centre Stage As Nina Wang’S Estate Administrators

+24 Estate administration Guardians of fortune Accountants take centre stage as Nina Wang’s estate administrators [ 24 ] A Plus + January 2008 By Heda Bayron erek Lai is in a hurry. He has The Nina Wang case is only one just wrapped up a meeting in a list of high profile international in Kowloon. Upon returning cases showing the role of estate Dto Deloitte’s offices in Admiralty, he administrators in disputes over a still has to dash off for a conference deceased person’s assets. When the call. It has been a long day. In fact, legendary New York philanthropist it’s his first day on a new job: Lai has Brooke Astor died in August 2007, been appointed as administrator of the a court appointed temporary late tycoon Nina Wang’s estimated administrators over her US$132 million HK$100 billion estate. estate until a court rules on which of Being an administrator is no easy Astor’s two wills is valid. feat, says Lai, the chief of Deloitte’s When a dispute arises over China reorganization team and a entitlement to an estate and the veteran of estate administration cases, appointment of administrators is being but he declines to comment on details considered, each party may propose to of this high profile case. the court its own possible appointee The legal battle over the estate as administrator, which often includes of Asia’s former richest woman, who accountants, lawyers or sometimes died in April last year, promises to be specialist bankers. The court will then epic. It pits feng shui enthusiast and make its decision in the best interests businessman Tony Chan, who claims of the estate, after considering the to be the sole heir under a 2006 will, nominees’ experience and expertise, against the Chinachem Charitable likely costs, and the views of the Foundation run by Wang’s siblings, parties involved. -

The Administration of the Estate of the Late Mrs Nina WANG

LC Paper No. CB(4)1313/14-15(01) For discussion on 20 July 2015 Legislative Council Panel on Administration of Justice and Legal Services The administration of the Estate of the late Mrs Nina WANG PURPOSE This paper is to brief Members of the Panel on the administration of the Estate of the late Mrs Nina Wang (“the Estate”). ROLE OF SECRETARY FOR JUSTICE (“SJ”) 2. SJ, in his capacity as protector of charities, may intervene in relevant legal proceedings for the purpose of protecting the interests of charity and may render assistance to the Court in the administration of charitable trusts. The role of SJ, which arises under common law, is recognized in the Trustee Ordinance (Cap. 29) and under Order 120 of the Rules of High Court (Cap. 4A). 3. As the protector of charities, SJ is necessarily a party to charity proceedings and represents the beneficial interest or objects of the charity. As there are charitable interests under the will made by the late Mrs Wang on 28 July 2002 (“2002 Will”), and given the exceptional size of the Estate, SJ has been a party to the probate, construction and administration proceedings, and has been keeping a close monitor of the case developments at all times. BACKGROUND Construction proceedings 4. Following the conclusion of the contentious probate proceedings in which the Court upheld the validity of the 2002 Will, SJ commenced proceedings in May 2012 in his capacity as the protector of charities to seek guidance from the Court on the proper construction of the 2002 Will 1 in order to determine the proper administration and eventual distribution of the Estate. -

The Administration of the Estate of the Late Mrs Nina WANG

For discussion on 20 July 2015 Legislative Council Panel on Administration of Justice and Legal Services The administration of the Estate of the late Mrs Nina WANG PURPOSE This paper is to brief Members of the Panel on the administration of the Estate of the late Mrs Nina Wang (“the Estate”). ROLE OF SECRETARY FOR JUSTICE (“SJ”) 2. SJ, in his capacity as protector of charities, may intervene in relevant legal proceedings for the purpose of protecting the interests of charity and may render assistance to the Court in the administration of charitable trusts. The role of SJ, which arises under common law, is recognized in the Trustee Ordinance (Cap. 29) and under Order 120 of the Rules of High Court (Cap. 4A). 3. As the protector of charities, SJ is necessarily a party to charity proceedings and represents the beneficial interest or objects of the charity. As there are charitable interests under the will made by the late Mrs Wang on 28 July 2002 (“2002 Will”), and given the exceptional size of the Estate, SJ has been a party to the probate, construction and administration proceedings, and has been keeping a close monitor of the case developments at all times. BACKGROUND Construction proceedings 4. Following the conclusion of the contentious probate proceedings in which the Court upheld the validity of the 2002 Will, SJ commenced proceedings in May 2012 in his capacity as the protector of charities to seek guidance from the Court on the proper construction of the 2002 Will 1 in order to determine the proper administration and eventual distribution of the Estate. -

TAX Quarterly Newsletter

TAX QUARTERLY NEWSLEttER A reVIEW OF PRC AND HONG KONG TAx dEVELOPMENTS www.dlapiper.com | SEPTEMBER 2012 EDitoRS’ CoLUMN In THIS ISSUE… Welcome to our September edition of the Tax Quarterly Newsletter. The summer quarter is always a slower one but still a few things have caught our attention. CHINA We start our China review1 with Wrong Wei, considering the recent decisions by two Beijing courts to reject Ai Weiwei’s appeal of a RMB 15.22M tax evasion fine. In Now or Never, we consider the advantages freeze planning may provide 04 WRONG WEI Chinese-US taxpayers looking to deal with wealth generated from initial public 06 now OR NEVER offerings. The Future Commences Now announces the launch of RMB currency futures in Hong Kong. In 601 + 30 = Some Clarity, we discuss Circular 30 and 09 tHE FUTURE consider how it will affect the application of Circular 601. COMMENCES now For our Hong Kong review, An Intellectual DIPN is a discussion of how DIPN No. 49 aims to clarify the intellectual property right legislation introduced 10 601 + 30 = soME last year. Alternate Reality examines the decision of the Court of Appeal in CLARITY Canray International where the court upheld the decision of the Court of First 12 TIDBit: Instance allowing the Commissioner of Inland Revenue to issue alternate INEVitaBLY assessments against multiple taxpayers on the same profits. In Cheers!, we look at the Nice Cheer Investment case where the Court of Appeal ruled in favour 12 TIDBit: of the taxpayer in its decision that unrealized gains from the revaluation of INEVitaBLY too trading securities are not subject to profits tax. -

Journal of Current Chinese Affairs

1/2006 Data Supplement PR China Hong Kong SAR Macau SAR Taiwan CHINA aktuell Journal of Current Chinese Affairs Data Supplement People’s Republic of China, Hong Kong SAR, Macau SAR, Taiwan ISSN 0943-7533 All information given here is derived from generally accessible sources. Publisher/Distributor: Institute of Asian Affairs Rothenbaumchaussee 32 20148 Hamburg Germany Phone: (0 40) 42 88 74-0 Fax:(040)4107945 Contributors: Uwe Kotzel Dr. Liu Jen-Kai Christine Reinking Dr. Günter Schucher Dr. Margot Schüller Contents The Main National Leadership of the PRC LIU JEN-KAI 3 The Main Provincial Leadership of the PRC LIU JEN-KAI 22 Data on Changes in PRC Main Leadership LIU JEN-KAI 27 PRC Agreements with Foreign Countries LIU JEN-KAI 45 PRC Laws and Regulations LIU JEN-KAI 50 Hong Kong SAR Political Data LIU JEN-KAI 54 Macau SAR Political Data LIU JEN-KAI 57 Taiwan Political LIU JEN-KAI 59 Bibliography of Articles on the PRC, Hong Kong SAR, Macau SAR, and on Taiwan UWE KOTZEL / LIU JEN-KAI / CHRISTINE REINKING / GÜNTER SCHUCHER 61 CHINA aktuell Data Supplement - 3 - 1/2006 The Leading Group for Fourmulating a National Strategy on Intellectual Prop- CHINESE COMMUNIST erty Rights was established in January 2005. The Main National (ChiDir, p.159) PARTY The National Disaster-Reduction Commit- tee was established on 2 April 2005. (ChiDir, Leadership of the p.152) CCP CC General Secretary China National Machinery and Equip- Hu Jintao 02/11 PRC ment (Group) Corporation changed its name into China National Machinery In- dustry Corporation (SINOMACH), begin- POLITBURO Liu Jen-Kai ning 8 September 2005. -

LC Paper No. CB(4)13/14-15(02)

LC Paper No. CB(4)13/14-15(02) Bills Committee on Administration of Justice (Miscellaneous Provisions) Bill 2014 Provision of Information requested at the Meeting on 3 June 2014 PURPOSE This paper provides the information relating to appeals in civil causes or matters to the Court of Final Appeal (“CFA”) as requested by Members at the first meeting on 3 June 2014. STATISTICS 2. At the meeting, Members requested the Judiciary Administration to provide the following updated statistics – (a) successful and unsuccessful rates of as of right appeals disposed of in the CFA filed since July 1997; (b) the number of substantive appeals (including as of right appeals) disposed of in the CFA since July 1997; and (c) leave applications disposed of in the CFA since July 1997. 3. The present as of right appeal system in civil matters is objectionable as a matter of principle. The Judiciary has proposed its removal because of the principles involved rather than the caseload as such. 4. The Judiciary would like to reiterate that as a matter of policy, the Judiciary does not normally maintain statistics on the results of appeal cases. The success of the appeals can be attributed to a large variety of reasons, depending very much on individual merits and circumstances of each appeal case. In some of these successful appeal cases, the CFA may take a different view from the lower courts’ judgment usually on law, but sometimes on the facts of the case. Sometimes, points not argued in the lower courts are argued in the CFA. Care must be taken in the use of such statistics, if they are useful in the first place. -

HKSAR V. CHAN CHUN CHUEN (30/10/2015, CACC233/2013)

HKSAR v. CHAN CHUN CHUEN (30/10/2015, CACC233/2013) Home | Go to Word | Print | CACC233/2013 IN THE HIGH COURT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION COURT OF APPEAL CRIMINAL APPEAL NO. 233 OF 2013 (ON APPEAL FROM HCCC NO. 182 OF 2012) ____________ BETWEEN HKSAR Respondent and CHAN CHUN CHUEN (陳振聰) Applicant ____________ Before : Hon Lunn VP, Poon and Pang JJA in Court Date of Hearing : 17, 18, 21-24 September 2015 Date of Judgment : 30 October 2015 ________________________ J U D G M E N T ________________________ Hon Lunn VP (giving the Judgment of the Court) : 1. The applicant seeks leave to appeal against his conviction on 4 July 2013 after trial by Macrae J, as Macrae JA was then, and a jury of a count of forgery of the will of Nina Kung (Count 1), and a count of using that will (Count 2), contrary to sections 71 and 73 respectively of the Crimes Ordinance, Cap. 200 (the ‘Ordinance’). In addition, the applicant seeks leave to appeal against the sentence of 12 years’ imprisonment imposed on him by the judge in respect of each of the two counts, which sentences were ordered to be served concurrently. The indictment http://legalref.judiciary.gov.hk/lrs/common/ju/ju_frame.jsp?DIS=101120&currpage=T[30-Oct-2015 15:55:29] HKSAR v. CHAN CHUN CHUEN (30/10/2015, CACC233/2013) Count 1 2. The Particulars of Offence of Count 1 alleged that between 15 October 2006 and 8 April 2007 the applicant made a will of Nina Kung, to whom reference will be made by her married name Mrs Nina Wang, bearing the date of 16 October 2006: “ …. -

Legislative Council

立法會 Legislative Council LC Paper No. CB(3) 627/18-19 Paper for the House Committee meeting of 24 May 2019 Questions scheduled for the Legislative Council meeting of 29 May 2019 Questions by: (1) Hon SHIU Ka-chun (Oral reply) (2) Hon Wilson OR (Oral reply) (Replacing his previous question) (3) Hon CHU Hoi-dick (Oral reply) (4) Hon AU Nok-hin (Oral reply) (5) Hon Holden CHOW (Oral reply) (6) Dr Hon Fernando CHEUNG (Oral reply) (7) Hon CHAN Kin-por (Written reply) (8) Hon Mrs Regina IP (Written reply) (9) Hon Dennis KWOK (Written reply) (10) Hon Tony TSE (Written reply) (11) Hon WU Chi-wai (Written reply) (12) Dr Hon Elizabeth QUAT (Written reply) (13) Hon Kenneth LEUNG (Written reply) (14) Hon Andrew WAN (Written reply) (Replacing his previous question) (15) Hon Charles Peter MOK (Written reply) (16) Hon Paul TSE (Written reply) (Replacing his previous question) (17) Hon Jimmy NG (Written reply) (18) Hon CHAN Hak-kan (Written reply) (19) Hon LUK Chung-hung (Written reply) (20) Hon SHIU Ka-fai (Written reply) (Replacing his previous question) (21) Hon Holden CHOW (Written reply) (Hon HUI Chi-fung has given up the question slot) (22) Hon Wilson OR (Written reply) Question 2 (For oral reply) (Translation) Regulation of the sale of residential units by way of tender Hon Wilson OR to ask: It has been reported that recently, some units of a residential development were offered for sale by way of tender. According to the tender results, a certain unit was sold unexpectedly at a price of $470,000 higher than that of another unit with the same orientation and size but 12 storeys higher, which was sold on the same day, and five other units with the same size and orientation but on different floors were sold surprisingly at the same price.