Building a Solid Foundation for a Sustainable Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MEDIA RELEASE Citibank Appoints New Director of Retail

MEDIA RELEASE Citibank appoints new Director of Retail Bank Sydney, 30 June 2006: Citibank has appointed Nicholas Cowell as the Director of the Retail Bank, reporting to Les Matheson, CEO Citibank Australia. Nicholas takes over the role from Mark Jones, who is now the CEO for Citibank Philippines. The Retail Bank area consists of Mortgages, CitiGold (Citibank’s wealth management arm) and Citibanking (encompassing transactional and deposit products and banking channels). “The appointment of Nicholas to this key role places Citibank in a unique position to proactively build our Retail Bank franchise in Australia,” said Mr Matheson. Since joining the company in May 2004, Nicholas has been the Head of Citibank Business Development. Nicholas brings to his new role, a depth of banking and management experience. Prior to Citibank, Nicholas held a variety of senior positions at the ANZ bank during his 15 years with the organisation. These included responsibility in the areas of general management, marketing and research, as well as most recently in strategy and mergers and acquisitions including substantial time in Asia. In addition, Nicholas helped establish and manage the ANZ Private Bank from 1997-1999. He has recently completed a Masters degree in Applied Finance from Macquarie University. He holds a First Class Honours degree in Arts and a degree in Computer Science from the University of Melbourne. -ends- Media enquiries: Anita Fu: T: 02) 8225 1631 M: 0401 862 986 [email protected] Leila Dean: T: 02) 8225 1658 M: 0404 509 894 [email protected] Citigroup (NYSE:C), the leading global financial services company has some 200 million customer accounts and does business in more than 100 countries, providing consumers, corporations, governments and institutions with a broad range of financial products and services, including consumer banking and credit, corporate and investment banking, securities brokerage, and wealth management. -

NATIONAL CAPITAL REGION Child & Youth Welfare (Residential) ACCREDITED a HOME for the ANGELS CHILD Mrs

Directory of Social Welfare and Development Agencies (SWDAs) with VALID REGISTRATION, LICENSED TO OPERATE AND ACCREDITATION per AO 16 s. 2012 as of March, 2015 Name of Agency/ Contact Registration # License # Accred. # Programs and Services Service Clientele Area(s) of Address /Tel-Fax Nos. Person Delivery Operation Mode NATIONAL CAPITAL REGION Child & Youth Welfare (Residential) ACCREDITED A HOME FOR THE ANGELS CHILD Mrs. Ma. DSWD-NCR-RL-000086- DSWD-SB-A- adoption and foster care, homelife, Residentia 0-6 months old NCR CARING FOUNDATION, INC. Evelina I. 2011 000784-2012 social and health services l Care surrendered, 2306 Coral cor. Augusto Francisco Sts., Atienza November 21, 2011 to October 3, 2012 abandoned and San Andres Bukid, Manila Executive November 20, 2014 to October 2, foundling children Tel. #: 562-8085 Director 2015 Fax#: 562-8089 e-mail add:[email protected] ASILO DE SAN VICENTE DE PAUL Sr. Enriqueta DSWD-NCR RL-000032- DSWD-SB-A- temporary shelter, homelife Residentia residential care -5- NCR No. 1148 UN Avenue, Manila L. Legaste, 2010 0001035-2014 services, social services, l care and 10 years old (upon Tel. #: 523-3829/523-5264/522- DC December 25, 2013 to June 30, 2014 to psychological services, primary community-admission) 6898/522-1643 Administrator December 24, 2016 June 29, 2018 health care services, educational based neglected, Fax # 522-8696 (Residential services, supplemental feeding, surrendered, e-mail add: [email protected] Care) vocational technology program abandoned, (Level 2) (commercial cooking, food and physically abused, beverage, transient home) streetchildren DSWD-SB-A- emergency relief - vocational 000410-2010 technology progrm September 20, - youth 18 years 2010 to old above September 19, - transient home- 2013 financially hard up, (Community no relative in based) Manila BAHAY TULUYAN, INC. -

Robinsons Land Corporation RLC

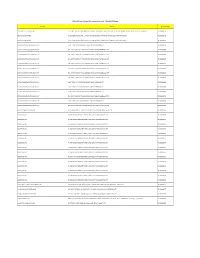

The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. Robinsons Land Corporation RLC PSE Disclosure Form 17-11 - List of Stockholders Reference: Section 17.11 of the Revised Disclosure Rules Type of Securities Common Preferred - Others - Record Date of Apr 24, 2019 Stockholders' Meeting Date of Stockholders' May 29, 2019 Meeting Type of Stockholders' Meeting Annual (Annual or Special) Other Relevant Information Please find attached the list of stockholders of Robinsons Land Corporation (RLC) as of April 24, 2019, the record date set by the Board of Directors of RLC to determine the stockholders entitled to notice and to vote at the annual meeting of the stockholders of RLC to be held on May 29, 2019. Filed on behalf by: Name Rosalinda Rivera Designation Corporate Secretary Robinsons Land Corporation April 24, 2019 SH # SH NAME SH ADDRESS NATIONALITY TOTAL NO. OF SHARES PERCENTAGE 0000230766 A & A SECURITIES, INC. 1906 PACIFIC BANK BLDG. AYALA AVENUE, MAKATI CITY FILIPINO 4,000.00 0.00007701 0000230768 A. ANGEL S. TANJANGCO 542 ARQUIZA ST.,ERMITA, MANILA FILIPINO 38,500.00 0.00074126 0000230770 ABOITIZ JEBS EN BULK TRANSPORT CORPORATION CEBU CITY, PHILIPPINES FILIPINO 400.00 0.00000770 0000230771 ABRAHAM T. CO C/O PBU, RCBC 333 SEN GIL PUYAT AVE 1200 MAKATI, METRO MANILA FILIPINO 1,000.00 0.00001925 0000230772 ACRIS CORPORATION 5/F BENPRES BUILDING,MERALCO AVENUE, PASIG CITY FILIPINO 8,900.00 0.00017136 0000230774 ADELINA A. -

Kod-4000 Sort by Title Tagalog Song Num Title Artist Num

KOD-4000 SORT BY TITLE TAGALOG SONG NUM TITLE ARTIST NUM TITLE ARTIST 650761 214 Luke Mejares 650801 A Tear Fell Victor Wood 650762 ( Anong Meron Ang Taong ) Happy Itchyworms 650802 A Wish On Christmas Night Jose Mari Chan 650000 (Ang) Kailangan Ko'y Ikaw Regine Velasquez 650803 A Wit Na Kanta Yoyoy Villame 650763 (He's Somehow Been) A Part Of Me Roselle Nava 650804 Aalis Ka Ba?(Crying Time) Rocky Lazatin 650764 (He's Somehow Been)A Part Of Me Roselle Nava 650805 Aangkin Sa Puso Ko Vina Morales 650765 (Nothing's Gonna Make Me) Change Roselle Nava 650806 Aawitin Ko Na Lang Ariel Rivera 650766 (Nothing's Gonna)Make Me Change Roselle Nava 650807 Abalayan Bingbing Bonoan 650187 (This Song) Dedicated To You Lilet 650808 Abalayan (Ilocano) Bingbing Bonoan 650767 ‘Cha Cha Cha’ Unknown 650809 Abc Tumble Down D Children 650768 100 Years Five For Fighthing 650188 Abot Kamay Orange&Lemons 650769 16 Candles The Crest 650810 Abot Kamay (Mtv) Orange&Lemons 650770 214 (Mtv) Luke Mejares 650189 Abot-Kamay Orange And Lemons 650771 214 (My Favorite Song) Rivermaya 650811 About Kaman Orange&Lemons 650772 2Nd Floor Nina 650812 Adda Pammaneknek Nollie Bareng 650773 2Nd Floor (Mtv) Nina 650813 Adios Mariquita Linda Adapt. L. Celerio 650774 6_8_12 (Mtv) Ogie Alcasid 650814 Adlaw Gai-I Nanog Rivera 650775 9 & Cooky Chua Bakit (Mtv) Gloc 650815 Adore You Eddie Peregrina 650776 A Ba Ka Da Children 650816 Adtoyakon R. Lopez 650777 A Beautiful Sky (Mtv) Lynn Sherman 650817 Aegis Rachel Alejandro 650778 A Better Man Ogie Alcasid 650190 Aegis Medley Aegis 650779 A -

Graduate Student Handbook

STUDENT HANDBOOK STUDENT HANDBOOK 2015 - 2018 2015-2018 The Student Handbook Revision Committee AY 2015-2018 Name: Name: Chairperson Ms. Fritzie Ian Paz-De Vera Dean of Student Affairs Address: Address: Members Dr. Rosemary Seva Telephone: I.D Number: Dean, Gokongwei College of Engineering Email Address: Email Address: Dr. Rochelle Irene Lucas Vice Dean, Br. Andrew Gonzalez FSC College of Education Course: Course: Ms. Elsie Velasco Faculty, Accountancy Department Mr. Oscar Unas Faculty, Manufacturing Engineering and Management Department Carlo Iñigo Inocencio President, University Student Government FOREWORD Wilbur Omar Chua Chairperson, Council of Student Organizations Jose Mari Carpena The regulations that appear on this Student Handbook apply to all undergraduate Graduate Student Council Convenor and graduate students who are enrolled in the different colleges of the University. GSC President, CLA Upon admission, they agree to abide by these regulations so as to maintain Consultant Atty. Christopher Cruz discipline, uphold the good order of the school, preserve the fair name of the University Legal Counsel University, and actualize its Mission-Vision Statement. Secretariat Ms. Maria Cecilia Renee Moreno Aside from norms contained in this Student Handbook, bulletin board and website postings, special manuals for specific purposes, and published announcements Resource Persons Joy Fajardo are the ordinary channels by which the University administration informs the student President, DLSU Parents of University Students Organization body of official business. The students should consult these channels regularly. Dr. Voltaire Mistades University Registrar The administrative authority of the University is vested on the President of the institution. The continued attendance of any student at De La Salle University Ms. -

The College of Medicine in 2002

INSTITUTIONAL PROFILE 1.1 MISSION-VISION STATEMENT OF THE LASALLIAN FAMILY IN THE PHILIPPINES Preamble Deeply moved, as St. John Baptiste de la Salle was, by the plight of the poor and youth at risk, we, the members of the Lasallian schools in the Philippines, commit ourselves to the La Sallian Mission of providing a human and Christian education to the young, especially in schools, with the service of the poor as priority, in order to evangelize and catechize, to promote peace and justice, accomplishing these together as shared mission. We draw strength from the many Lasallians committed to incarnating our charism in our country today to serve the needs of the Filipino youth, especially those at risk. Declaration Inflamed by the Holy Spirit, God’s own fire, we declare our commitment to the following: We shall work together as a national network of Lasalllian schools in the Philippines for the efficient and effective implementation of the Lasallian Mission, following the directives of the De La Salle Brothers and the Philippine Lasallian Family as set by the General Chapter, the District Chapter and the Philippine Lasallian Family Convocation; We shall ensure the integrity of the Lasallian Mission by setting directions and standards applicable to the Philippine Lasallian schools and by monitoring their implementation; We shall promote the Lasallian Mission by fostering synergy, collaboration and sharing among the Lasallian schools; and We shall uphold the Lasallian values of faith, zeal in service and communion in mission. Prayer In all these, we, together and by association, dedicate our life and work to God, who alone guarantees the fulfillment of our Lasallian dream. -

1623400766-2020-Sec17a.Pdf

COVER SHEET 2 0 5 7 3 SEC Registration Number M E T R O P O L I T A N B A N K & T R U S T C O M P A N Y (Company’s Full Name) M e t r o b a n k P l a z a , S e n . G i l P u y a t A v e n u e , U r d a n e t a V i l l a g e , M a k a t i C i t y , M e t r o M a n i l a (Business Address: No. Street City/Town/Province) RENATO K. DE BORJA, JR. 8898-8805 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A 0 4 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) NONE (Secondary License Type, If Applicable) Corporation Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 2,999 as of 12-31-2020 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. 2 SEC Number 20573 File Number______ METROPOLITAN BANK & TRUST COMPANY (Company’s Full Name) Metrobank Plaza, Sen. Gil Puyat Avenue, Urdaneta Village, Makati City, Metro Manila (Company’s Address) 8898-8805 (Telephone Number) December 31 (Fiscal year ending) FORM 17-A (ANNUAL REPORT) (Form Type) (Amendment Designation, if applicable) December 31, 2020 (Period Ended Date) None (Secondary License Type and File Number) 3 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. -

Expressions of Tagalog Imaginary the Tagalog Sarswela and Kundiman in Early Films in the Philippines (1939–1959)

ISSN: 0041-7149 ISSN: 2619-7987 VOL. 89 • NO. 2 • NOVEMBER 2016 UNITASSemi-annual Peer-reviewed international online Journal of advanced reSearch in literature, culture, and Society Expressions of Tagalog Imaginary The Tagalog Sarswela and Kundiman in Early Films in the Philippines (1939–1959) Antonio p. AfricA . UNITAS Expressions of Tagalog Imaginary The Tagalog Sarswela and Kundiman in Early Films in the Philippines (1939–1959) . VOL. 89 • NO. 2 • NOVEMBER 2016 UNITASSemi-annual Peer-reviewed international online Journal of advanced reSearch in literature, culture, and Society Expressions of Tagalog Imaginary The Tagalog Sarswela and Kundiman in Early Films in the Philippines (1939–1959) Antonio P. AfricA since 1922 Indexed in the International Bibliography of the Modern Language Association of America Expressions of Tagalog Imgaginary: The Tagalog Sarswela and Kundiman in Early Films in the Philippines (1939–1959) Copyright @ 2016 Antonio P. Africa & the University of Santo Tomas Photos used in this study were reprinted by permission of Mr. Simon Santos. About the book cover: Cover photo shows the character, Mercedes, played by Rebecca Gonzalez in the 1950 LVN Pictures Production, Mutya ng Pasig, directed by Richard Abelardo. The title of the film was from the title of the famous kundiman composed by the director’s brother, Nicanor Abelardo. Acknowledgement to Simon Santos and Mike de Leon for granting the author permission to use the cover photo; to Simon Santos for permission to use photos inside pages of this study. UNITAS is an international online peer-reviewed open-access journal of advanced research in literature, culture, and society published bi-annually (May and November). -

PCIEERD Annual Report 2010 MESSAGE from the SECRETARY

PROFILE The Philippine Council for Industry, Energy and Emerging Technology Research and Development (PCIEERD) is one of the sectoral planning councils of the Department of Science and Technology (DOST). It is mandated to serve as the central agency in the development of policies, plans and programs as well as in the implementation of strategies in the industry, energy and emerging technology sectors through the following S&T programs: • Human Resource Development • Institution Development • Research and Development • Technology Transfer and Commercialization • Information Dissemination and Promotion VISION A recognized leader in fostering new and emerging technologies and innovations in building Science and Technology collaborations for vibrant industry and energy sectors. SECTORAL COVERAGE Industry • Electronics • Food Processing • Process • Mining/Minerals • Metals and Engineering Energy • Alternative Energy • Energy Efficiency • Transportation Emerging Technologies • Materials Science/Nanotechnology • Genomics • Biotechnology • Information and Communications Technology • Space Technology Applications b PCIEERD Annual Report 2010 MESSAGE FROM THE SECRETARY congratulate the Philippine Council for Industry, Energy and Emerging Technology Research and Development (PCIEERD) for its accomplishments in its first year of existence. I am very pleased that the Iw ork that you have done is very much aligned with the rallying call of the Department of Science and Technology (DOST) toward a more sustainable economic growth that would benefit our people. DOST’s priority programs are directed to using S&T in solving pressing national problems, developing appropriate technologies to boost growth in the countryside, and improving industry competitiveness for our country’s socio-economic development. Likewise, the Department is prioritizing the use of S&T towards enhancing government and social services, and the development of emerging technologies to underpin our industry’s global competitiveness. -

In the Footsteps of De La Salle

1st International Conference on Advanced Research (ICAR- 2017), Manama, Bahrain ISBN:978-0-995398-016 www.apiar.org.au IN THE FOOTSTEPS OF DE LA SALLE: ON BECOMING A LASALLIAN EVALUATION OF THE CONDUCT OF THE INTRO TO LA SALLE AND CONTEXTUALIZATION AND LIVING OUT THE LASALLIAN GUIDING PRINCIPLES SESSIONS FOR ALL INCOMING FIRST YEAR AND SECOND YEAR STUDENTS OF DELA SALLE HEALTH SCIENCES INSTITUTE, SY 2016-2017 Juanito O. Cabanias, PhD De La Salle Health Sciences Institute, Cavite, Philippines Email: [email protected] Abstract In De La Salle Health Sciences Institute, the beginning of SY 2016-2017 became a significant year with regards to the implementation of and living out the Lasallian Guiding Principles. The Institute programmed a 5-day Lasallian Formation activity focusing on the life of St. John Baptist De La Salle and Lasallian Guiding Principles facilitated by different resource persons. This program endeavored to integrate the Life of St. John Baptist De La Salle in the De La Salle Health Sciences Institute curriculum and contextualize and live out the Lasallian Guiding Principles. Specifically, it aimed to: (1.) Orient the incoming freshman and sophomore students about the life of Life of St. John Baptist De La Salle and the existence of the LGP; (2.) Involve all incoming freshman and sophomore students in the discussion of the Lasallian Guiding Principles through the different programs, team building activities and individual/group presentations and sessions; (3.) Contextualize and live out all lessons learned from the discussion on the life of Life of St. John Baptist De La Salle and conduct Lasallian Guiding Principles; and (4.) Assess/evaluate the implementation of the Intro to La Salle and Lasallian Guiding Principles sessions. -

Directory of Participants 11Th CBMS National Conference

Directory of Participants 11th CBMS National Conference "Transforming Communities through More Responsive National and Local Budgets" 2-4 February 2015 Crowne Plaza Manila Galleria Academe Dr. Tereso Tullao, Jr. Director-DLSU-AKI Dr. Marideth Bravo De La Salle University-AKI Associate Professor University of the Philippines-SURP Tel No: (632) 920-6854 Fax: (632) 920-1637 Ms. Nelca Leila Villarin E-Mail: [email protected] Social Action Minister for Adult Formation and Advocacy De La Salle Zobel School Mr. Gladstone Cuarteros Tel No: (02) 771-3579 LJPC National Coordinator E-Mail: [email protected] De La Salle Philippines Tel No: 7212000 local 608 Fax: 7248411 E-Mail: [email protected] Batangas Ms. Reanrose Dragon Mr. Warren Joseph Dollente CIO National Programs Coordinator De La Salle- Lipa De La Salle Philippines Tel No: 756-5555 loc 317 Fax: 757-3083 Tel No: 7212000 loc. 611 Fax: 7260946 E-Mail: [email protected] E-Mail: [email protected] Camarines Sur Brother Jose Mari Jimenez President and Sector Leader Mr. Albino Morino De La Salle Philippines DEPED DISTRICT SUPERVISOR DEPED-Caramoan, Camarines Sur E-Mail: [email protected] Dr. Dina Magnaye Assistant Professor University of the Philippines-SURP Cavite Tel No: (632) 920-6854 Fax: (632) 920-1637 E-Mail: [email protected] Page 1 of 78 Directory of Participants 11th CBMS National Conference "Transforming Communities through More Responsive National and Local Budgets" 2-4 February 2015 Crowne Plaza Manila Galleria Ms. Rosario Pareja Mr. Edward Balinario Faculty De La Salle University-Dasmarinas Tel No: 046-481-1900 Fax: 046-481-1939 E-Mail: [email protected] Mr. -

DOLE-NCR for Release AEP Transactions As of 7-16-2020 12.05Pm

DOLE-NCR For Release AEP Transactions as of 7-16-2020 12.05pm Company Address Transaction No. 3M SERVICE CENTER APAC, INC. 17TH, 18TH, 19TH FLOORS, BONIFACIO STOPOVER CORPORATE CENTER, 31ST STREET COR., 2ND AVENUE, BONIFACIO GLOBAL CITY, TAGUIG CITY TNCR20000756 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000178 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000283 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000536 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000554 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000569 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000607 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000617 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000632 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000633 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000638 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000680 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY