An Introduction to NTT's NGN and New Services in Japan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?

IRLE IRLE WORKING PAPER #188-09 September 2009 Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? James R. Lincoln, Masahiro Shimotani Cite as: James R. Lincoln, Masahiro Shimotani. (2009). “Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?” IRLE Working Paper No. 188-09. http://irle.berkeley.edu/workingpapers/188-09.pdf irle.berkeley.edu/workingpapers Institute for Research on Labor and Employment Institute for Research on Labor and Employment Working Paper Series (University of California, Berkeley) Year Paper iirwps-- Whither the Keiretsu, Japan’s Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? James R. Lincoln Masahiro Shimotani University of California, Berkeley Fukui Prefectural University This paper is posted at the eScholarship Repository, University of California. http://repositories.cdlib.org/iir/iirwps/iirwps-188-09 Copyright c 2009 by the authors. WHITHER THE KEIRETSU, JAPAN’S BUSINESS NETWORKS? How were they structured? What did they do? Why are they gone? James R. Lincoln Walter A. Haas School of Business University of California, Berkeley Berkeley, CA 94720 USA ([email protected]) Masahiro Shimotani Faculty of Economics Fukui Prefectural University Fukui City, Japan ([email protected]) 1 INTRODUCTION The title of this volume and the papers that fill it concern business “groups,” a term suggesting an identifiable collection of actors (here, firms) within a clear-cut boundary. The Japanese keiretsu have been described in similar terms, yet compared to business groups in other countries the postwar keiretsu warrant the “group” label least. -

CIAJ Profile 2019-2020

CIAJ PROFILE Communications and Information Network Association of Japan 2019-2020 ADDRESS: 6th Fl., Kabutocho Uni-square, 21-7 Kabutocho, Nihonbashi, Chuo-ku, Tokyo 103-0026 PHONE: +81 3 5962-3454 COMMU N ICATIONS FAX: +81 3 5962-3455 E-mail: [email protected] URL: https://www.ciaj.or.jp/en/ AND INFORM ATION NETW ORK ASSOCIATION O F JA P A N Who we are CIAJ Management Team (As of September, 2019) Board of Directors Senior Steering Committee Members The Communications and Information Network Association of Japan promotes the further use and advancement of info-communication technologies (ICT), aiming for the robust growth of all industries that provides and/or uses info-communication networks by bringing together diverse industries and Chairman Director Director Nobuhiro Endo Tatsuya Tanaka sharing insights. Through such initiatives, CIAJ has Nobuhiro Endo Koichi Hamada Ryota Kitamura Chairman, Chairman, Chairman, President, Telecommunications NEC Corporation Fujitsu Limited NEC Corporation Anritsu Corporation Carriers the mission of contributing to solving social issues Association (NTT) and realizing an enriching society in Japan as well as a sustainable global community. CIAJ was established in 1948 as a voluntary industry association composed mainly of telecom terminal Director Director Director manufacturers and network infrastructure vendors. In Hideichi Kawasaki Toshiaki Higashihara Kaichiro Sakuma Shuji Nakamura Kunihiko Satoh Chairman, President, October 2009, CIAJ embarked on a new page in its President, Executive Officer, Corporate Adviser, OKI Electric Industry Hitachi, Ltd. Hitachi Kokusai Mitsubishi Research Ricoh Co., Ltd. Co., Ltd. history by becoming a general incorporated Electric Inc. Institute, Inc. association. CIAJ’s diverse regular members include communication network and equipment vendors, telecommunication carriers, service providers and user companies. -

Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?

UC Berkeley Working Paper Series Title Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? Permalink https://escholarship.org/uc/item/00m7d34g Authors Lincoln, James R. Shimotani, Masahiro Publication Date 2009-09-24 eScholarship.org Powered by the California Digital Library University of California WHITHER THE KEIRETSU, JAPAN’S BUSINESS NETWORKS? How were they structured? What did they do? Why are they gone? James R. Lincoln Walter A. Haas School of Business University of California, Berkeley Berkeley, CA 94720 USA ([email protected]) Masahiro Shimotani Faculty of Economics Fukui Prefectural University Fukui City, Japan ([email protected]) 1 INTRODUCTION The title of this volume and the papers that fill it concern business “groups,” a term suggesting an identifiable collection of actors (here, firms) within a clear-cut boundary. The Japanese keiretsu have been described in similar terms, yet compared to business groups in other countries the postwar keiretsu warrant the “group” label least. The prewar progenitor of the keiretsu, the zaibatsu, however, could fairly be described as groups, and, in their relatively sharp boundaries, hierarchical structure, family control, and close ties to the state were structurally similar to business groups elsewhere in the world. With the break-up by the U. S. Occupation of the largest member firms, the purging of their executives, and the outlawing of the holding company structure that held them together, the zaibatsu were transformed into quite different business entities, what we and other literature call “network forms” of organization (Podolny and Page, 1998; Miyajima, 1994). -

Annual Report

VCCI Council VCCI VCCI Council April2018March 2018 - 2019 ANNUAL REPORT English This publication is printed on an environment-friendly ink. VCCI Council The purpose of this corporate body is to promote, in cooperation with related industries, the Greetings voluntary control of radio disturbances emitted from multimedia equipment (MME) on the one Thank you for your continuing support for the activities of VCCI. hand, and improvement of robustness of MME against radio disturbances on the other hand, so This is a report on our activities in FY 2018. that the interests of Japanese consumers are protected with respect to anxiety-free use of MME. At the world's largest CPS and IoT general exhibition, "CEATEC JAPAN 2018", held in October last year, Japan's growth strategy to achieve "Society 5.0" and its vision for the future were announced to the world based on the theme "Connecting Society, Co-Creating the Future". 5G Description mobile communications system services are planned to finally begin operation in Japan next year, and steady initiatives are underway to make "Society 5.0", a.k.a. a "super-smart society", a reality. Formulate…basic…policies… on… voluntary… control… of… electromagnetic… Hold …measurement…skills…courses…to…prepare…members’…engineers… 1 disturbances…emitted…by…multimedia…equipment 6 for…adequate…conformity…assessment We have high hopes for further developments in the IT and electronics industry, which holds deep ties to VCCI, as a key player in providing a platform for achieving "Society 5.0". By VCCI Council leveraging its growing technological prowess in an increasingly competitive world, the IT and Coordinate… the…interest… of…member… organizations… and…liaise… with… Study…trends…in…overseas…EMC…regulations…and…seek…opportunities… President: 2 the…government…and…related…agencies 7 for…mutual…recognition…agreement electronics industry will help solve a variety of social problems through collaborative creation. -

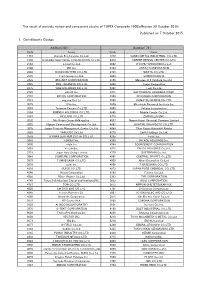

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Respondents(Eng)

2005 JCGR JCGIndex Survey Responding Companies http://www.jcgr.org/ TSE Code Company Indutry T1334 Maruha Group Inc. Fishery, Agriculture & Forestry T1801 Taisei Corp. Construction T1802 Obayashi Corp. Construction T1814 Daisue Construction Co., Ltd. Construction T1816 Ando Corp. Construction T1822 Daiho Corp. Construction T1824 Maeda Corp. Construction T1834 Odakyu Construction Co., Ltd. Construction T1835 Totetsu Kogyo Co., Ltd. Construction T1861 Kumagai Gumi Co., Ltd. Construction T1881 NIPPO Corp. Construction T1925 Daiwa House Industry Co., Ltd. Construction T1928 Sekisui House, Ltd. Construction T1950 Nippon Densetsu Kogyo Co., Ltd. Construction T1954 Nippon Koei Co., Ltd. Services T1967 Yamato Corp. Construction T1980 Dai-Dan Co., Ltd. Construction T2051 Nosan Corp. Foods T2052 Kyodo Shiryo Co., Ltd. Foods T2107 Toyo Sugar Refining Co., Ltd. Foods T2201 Morinaga & Co., Ltd. Foods T2202 Meiji Seika Kaisha, Ltd. Foods T2206 Ezaki Glico Co., Ltd. Foods T2267 Yakult Honsha Co., Ltd. Foods T2282 Nippon Meat Packers, Inc. Foods T2284 Itoham Foods Inc. Foods T2290 Yonekyu Corp. Foods T2322 NEC Fielding, Ltd. Services T2501 Sapporo Holdings Ltd. Foods T2502 Asahi Breweries, Ltd. Foods T2533 Oenon Holdings, Inc. Foods T2536 Mercian Corp. Foods T2579 Coca-Cola West Japan Co., Ltd. Foods T2590 Dydo Drinco, Inc. Foods T2591 Calpis Co., Ltd. Foods T2597 Unicafe Inc. Foods T2599 Japan Foods Co., Ltd. Foods T2602 The Nisshin Oillio Group, Ltd. Foods T2671 F.D.C. Products Inc. Retail Trade T2698 Can Do Co., Ltd. Retail Trade T2734 Sala Corp. Retail -

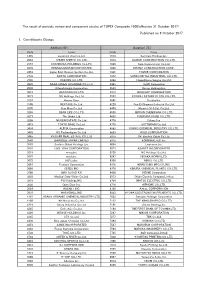

Published on 6 October 2017 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2017) Published on 6 October 2017 1. Constituents Change Addition( 92 ) Deletion( 73 ) Code Issue Code Issue 1435 investors cloud co.,ltd. 1514 Sumiseki Holdings,Inc. 2053 CHUBU SHIRYO CO.,LTD. 1814 DAISUE CONSTRUCTION CO.,LTD. 2157 KOSHIDAKA HOLDINGS Co.,LTD. 1826 Sata Construction Co.,Ltd. 2378 RENAISSANCE,INCORPORATED 1866 KITANO CONSTRUCTION CORP., 2453 Japan Best Rescue System Co.,Ltd. 1921 TOMOE CORPORATION 2733 ARATA CORPORATION 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2742 HALOWS CO.,LTD. 2286 Hayashikane Sangyo Co.,Ltd. 2899 NAGATANIEN HOLDINGS CO.,LTD. 2485 TEAR Corporation 2930 Kitanotatsujin Corporation 2533 Oenon Holdings,Inc. 3031 RACCOON CO.,LTD. 3313 BOOKOFF CORPORATION 3073 DD Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 3134 Hamee Corp. 3681 V-cube,Inc. 3186 NEXTAGE Co.,Ltd. 4229 Gun Ei Chemical Industry Co.,Ltd. 3230 Star Mica Co.,Ltd. 4404 Miyoshi Oil & Fat Co.,Ltd. 3245 DEAR LIFE CO.,LTD. 4539 NIPPON CHEMIPHAR CO.,LTD. 3271 The Global Ltd. 4620 FUJIKURA KASEI CO.,LTD. 3299 MUGEN ESTATE Co.,Ltd. 4776 Cybozu,Inc. 3415 TOKYO BASE Co.,Ltd. 4779 SOFTBRAIN Co.,Ltd. 3434 ALPHA Corporation 4992 HOKKO CHEMICAL INDUSTRY CO.,LTD. 3445 RS Technologies Co.,Ltd. 5603 KOGI CORPORATION 3465 KI-STAR REAL ESTATE CO.,LTD 5815 Oki Electric Cable Co.,Ltd. 3548 BAROQUE JAPAN LIMITED 5915 KOMAIHALTEC Inc. 3563 Sushiro Global Holdings Ltd. 6054 Livesense Inc. 3564 LIXIL VIVA CORPORATION 6073 ASANTE INCORPORATED 3661 m-up,Inc. 6236 NC Holdings Co.,Ltd. 3667 enish,inc. 6247 HISAKA WORKS,LTD. -

2004 C&C Prize Recipients Are Honored

News 2004 C&C Prize Recipients are Honored The Foundation for C&C Promotion (President: of California, Berkeley for “Contributions to the ad- Hajime Sasaki, Chairman of the Board, NEC Corpo- vancement of computer science, engineering, and in- ration) was established as a nonprofit organization dustry through inspiring textbooks, research, and funded by the NEC Corporation in March of 1985. It professional services for computer architecture.” was established to promote pioneering research and They have contributed to the advancement of com- development efforts related to C&C, the integration of puter architecture. After the invention of RISC archi- computers and communications technologies, with tecture by John Cocke (the recipient of the 1994 C&C the aim of advancing the sciences, advancing commu- Prize) they further developed RISC architecture and nication between people, and contributing to a culture built RISC based VLSI processors. MIPS and SPARC in which each person can reach their maximum po- RISC chips are the result of their effort and are used tential. by many servers and workstations and are also used In order to advance these objectives, the founda- as embedded processors for game machines, termi- tion has three main activities: 1) awards (C&C nals, and communication equipment. Co-authored Prizes), 2) grants (for researchers attending interna- textbooks on computer architecture have been widely tional conferences, for non-Japanese researchers, and read worldwide. for receivers of doctorates), and 3) surveys and re- Their contribution to R&D, transfer of technology search. to industry, and the cultivation of human resources The year 2004 marks the 20th year of awards are highly appreciated. -

ITU-AJ Members List URL: April22, 2019 /104 Members

ITU-AJ Members List URL:http://www.ituaj.jp/?p=1353 April22, 2019 /104 Members All Nippon Airways Co., Ltd. NTT COMWARE CORPORATION ALPHA SYSTEMS INC. NTT DATA CORPORATION Alpine Electronics, Inc. NTT DOCOMO, INC. Anritsu Corporation NTT WORLD ENGINEERING MARINE CORPORATION Association of Radio Industries and Businesses Oi Electric Co.,Ltd. ASTRODESIGN,Inc. Oki Electric Industry Co., Ltd. Basic Human Needs Association Orange Japan Co., Ltd Broadcasting Satellite System Corporation Panasonic Corporation Central Japan Industries Association PTC Japan Committee Central Research Institute of Electric Power Industry Radio Engineering & Electronics COMMUNICATION LINE PRODUCTS ASSOCIATION OF JAPAN RIKUJYOU MUSEN KYOUKAI COMMUNICATIONS AND INFORMATION NETWORK ASSOCIATION OF JAPAN SEIKOU Corporation Dempa Publications, Inc Sharp Corporation Denki Kogyo Company, Limited SKY Perfect JSAT Corporation Electric Power Development Co.,Ltd. SoftBank Corp. Fuji Television Network, Inc. Sony Corporation FUJI XEROX Co., Ltd. SUMITOMO ELECTRIC Fujikura Ltd. Support Center for Advanced Telecommunications Technology Research FUJITSU LIMITED Telecommunications Carriers Association Furukawa Electric Co., Ltd. Telecommunications Services Association FURUNO ELECTRIC CO.,LTD The Foundation for MultiMedia Communications GITS WASEDA University The Japan Amateur Radio League Hitachi,Ltd. THE JAPAN COMMERCIAL BROADCASTERS ASSOCIATION IBM Japan, Ltd The Japan Society of Information and Communication Research InfoCom Research, Inc. THE TELECOMMUNICATION TECHNOLOGY COMMITTEE -

CIAJ Profile 2017-2018

CIAJ PROFIP FILEILE Communications and Information Network Association of Japan 2017-2018 ADDRESS: 3rd Fl., JEI Hamamatsucho Bldg., 2-2-12 Hamamatsucho, Minato-ku, Tokyo 105-0013 PHONE: +81 3 5403-9363 FAX: +81 3 5403-9360 COMMUNICATIONS URL: http://www.ciaj.or.jp/en/ E-mail: [email protected] AND INFORMATION NETW ORK ASSOCIATION OF JA P AN Who we are CIAJ Management Team (As of July, 2017) Board of Directors Senior Steeringg Committee Members CIAJ contributes to the advancement of ICT as an industry association Working hand-in-hand with our member companies, the Communications and Information Network Association of Japan (CIAJ) is committed to the healthy development Chairman DirectorDirectoor HideichiHid i hi Kawasaki K ki ToshiakiToshiaki HigashiharaHigashihara KenichiroKenichiro YamanishiYamanishi of info-communication network industries through the Hideichi Kawasaki Naoki Tamura Chairman, President,President, Chairman, Chairman, President, OKI Electric Industry Hitachi, Ltd. Mitsubishi Electric promotion of ICT. CIAJ also strives for the realization of OKI Electric Industry Tamura Corporation Co., Ltd. Corporation Co., Ltd. a socially, economically and culturally enriching society in Japan as well as in the global community, by supporting advanced and widely available uses of information. CIAJ was established in 1948 as a voluntary industry Director DirectorDirector Satoshi Tsunakawa NobuhiroNobuhiro EEndondo MasamiMaasami YamamotoYamamoto association composed mainly of telecom terminal Mikio Matsuzawa Yasuyoshi Katayama President, President, Chairman,Chaia rman President, President, Toshiba Corporation NEC Corporation Fujitsu Limited manufacturers and network infrastructure vendors. In Denki Kogyo Co., Ltd. CIAJ October 2009, CIAJ embarked on a new page in its history by becoming a general incorporated association. -

Best Platform for Smart Energy Industry Leaders Industry Best Platformforsmartenergy Organised by Dates: February 27 February Dates: Organised By: Organised By: Ltd

Best Platform for Smart Energy Industry Leaders Who is Exhibiting Information SE13_BRC_英_表1_4 (yamamoto) Reed Exhibitions Japan Ltd. ? Reed Exhibitions Japan Ltd. is the Japan branch of world’s leading trade fair organiser –Reed Exhibitions. Reed Exhibitions Japan Ltd. organises 75 exhibitions and conferences in 36 industries in Japan annually which all of them are in great success. Below are excerpt of some shows that Reed Exhibitions Japan Ltd. organises. ELECTRONICS Asia’s Largest Electronics Manufacturing Show INTERNEPCON JAPAN CAR-ELE JAPAN EV JAPAN IC PACKAGING TECHNOLOGY EXPO Dates: February 27 [Wed] – March 1 [Fri], 2013 1,217* Exhibitors 59,963* Trade Visitors Venue : Tokyo Big Sight, Japan Organised by: Reed Exhibitions Japan Ltd. IT Japan’s Largest IT Solution Show WIRELESS M2M EXPO CLOUD COMPUTING EXPO JAPAN DATA CENTER EXPO 1,241* Exhibitors 113,299* Trade Visitors Reed Exhibitions Japan Ltd. is the professional exhibition organiser with rich experiences in establishing an international business platform for non-Japanese companies to interact and expand business. With continuous growth in both exhibitors and visitors number, Reed Exhibitions Japan Ltd. holds strong database that fully covers various markets in depth. Be confident and count on us. We look forward to your active participation in World Smart Energy Week. *Figures of previous event including all concurrent shows World Smart Energy Week Show Management Attn: Yasu MUROTA / Nina XIANG / Machiko AIKAWA / Mitsuru TAKAZAWA / Yoona CHANG / Aya ARAI Reed Exhibitions Japan -

Sy-320A/321A

Instruction Manual Chamber Scanner System SY-320A/321A Ⓒ 2010 IWATSU ELECTRIC CO., LTD. All rights reserved. Preface ◇ Thank you for purchasing the Chamber Scanner System SY-320A/321A and please regularly use lastingly in future. ◇ Please read this manual before using this instrument, then keep the manual handy for future reference. ◇ This instruction manual describes operating precautions, operating procedures, and specifications of this instrument (chamber scanner system: SY-320A/321A). For B-H analyzer itself, the remote control software: SY-810, and the chamber, refer to the instruction manual for each. ◇ In this manual, the constant temperature chamber is written "chamber". Important Safety Precautions To ensure safe operation of this instrument and to prevent injury to the user or damage to property, read and carefully observe the WARNING and CAUTION in the following sections. Definition of WARNING and CAUTION used in this manual Incorrect operation or failure to observe the WARNING may WARNING result in death or serious injury. Incorrect operation or failure to observe the CAUTION may CAUTION result in injury or damage to instrument. Notices ◇ Parts of the contents of this manual may be modified without notice for improvements in specifications and functions. ◇ Reproduction or reprinting of the contents of this manual without prior permission from IWATSU is prohibited. ◇ If any question about this instrument arises, contact Iwatsu at the address listed at the end of this manual or our sales distributors. ◇ For inquiry about options described in this manual, contact IWATSU listed at the end of this manual or our sales distributors. Revision History ◇ Oct 2014: 1st edition ◇ Jul 2015: 2nd edition ◇ Aug 2016: 3rd edition ◇ Aug 2018: 4th edition KML094841 I Read the following safety information.