2015 Annual Report and Accounts Our History

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

2017-2018 Annual Investment Report Retirement System Investment Commission Table of Contents Chair Report

South Carolina Retirement System Investment Commission 2017-2018 Annual Investment Report South Carolina Retirement System Investment Commission Annual Investment Report Fiscal Year Ended June 30, 2018 Capitol Center 1201 Main Street, Suite 1510 Columbia, SC 29201 Rebecca Gunnlaugsson, Ph.D. Chair for the period July 1, 2016 - June 30, 2018 Ronald Wilder, Ph.D. Chair for the period July 1, 2018 - Present 2017-2018 ANNUAL INVESTMENT REPORT RETIREMENT SYSTEM INVESTMENT COMMISSION TABLE OF CONTENTS CHAIR REPORT Chair Report ............................................................................................................................... 1 Consultant Letter ........................................................................................................................ 3 Overview ................................................................................................................................... 7 Commission ............................................................................................................................... 9 Policy Allocation ........................................................................................................................13 Manager Returns (Net of Fees) ..................................................................................................14 Securities Lending .....................................................................................................................18 Expenses ...................................................................................................................................19 -

Property Investor Profiles

ACC Property Investor Profiles Accrue Capital Ltd Addington Capital 11 Hill Street, London W1J 5LG 6 Heddon Street, London W1B 4BT Tel: 020 7318 4700 Fax: 020 7409 0052 Tel: 020 7042 9250 Email: [email protected] Email: [email protected] Web: www.accruecap.com Web: www.addingtoncapital.com Contacts Contacts Stephen Webster (Chairman) Martin Roberts (Managing Director) Brian Quinn (Structured Finance) Matthew Allen (Director) Comment Alex Wagstaff (Retail Asset Management) 10/14 - Accrue Capital acquired a retail portfolio for £22.2m, at a Comment yield of 8.71%. The acquired portfolio comprises 10 fully-let assets, Martin Roberts, formerly of CIT, formed Addington in April 2010. the majority of which are retail properties — including a retail park, a neighbourhood shopping centre, a hotel, high street retail and 10/12 - Addington Capital purchased a 563 asset residential offices. portfolio from Lloyds Banking Group and Grainger for £39.1m. The The unexpired lease term is over eight years, with more than 72% properties are mainly converted houses that are privately let to of the income secured on leases in excess of five years. students across UK cities such as Edinburgh, Newcastle, Bristol, Assets include: part of Hough Retail Park, Stafford; Kingsway Manchester and Nottingham. Retail Park, Lancaster; the Fylde Road site in Southport; and Pelham Street, Nottingham. 07/14 - Addington Capital was appointed asset management partner by Tristan Capital Partners for the Tree Portfolio. The Ace Liberty & Stone Plc Portfolio was acquired -

Newriver REIT Plc Annual Report and Accounts 2018

& Annual Report 2018 Accounts and NewRiver REIT plc Annual Report and Accounts 2018 NewRiver REIT plc (‘NewRiver’) is a Premium Listed REIT on the Main Market of the London Stock Exchange and a constituent of the FTSE 250 and EPRA indices. Founded in 2009, we specialise in buying, managing, developing and recycling convenience-led, community-focused retail and leisure assets. Our high-quality and conveniently located portfolio provides value for money on essential goods and services to consumers across the UK, and our affordable rents and high footfall locations create desirable and profitable trading opportunities for our occupiers. It is our fundamental belief that affordability for occupiers, and not lease length, means sustainability for our business. With an experienced management team and proven business model, we have a track record of delivering growing and sustainable cash returns to our shareholders and creating thriving communities across the UK. CONTENTS Strategic Report Financial Highlights IFC Our Business at a Glance 04 Chairman’s Review 08 Our Business Model 10 Our Marketplace 12 Leveraging our Key Relationships 16 CEO Review 18 OUR FINANCIAL HIGHLIGHTS Our Strategy 24 Our KPIs 26 Property Review 32 Gross income Funds From Operations Financial Review 56 (proportionally consolidated) Our People 68 ESG Report 69 Risk Management Report 74 £107.0m £60.3m Governance FY17: £106.7m FY17: £58.2m Board of Directors 78 Corporate Governance Report 80 Audit Committee Report 85 FFO per share Ordinary dividend per share Nomination Committee -

Industrial & Logistics Viewpoint

INDUSTRIAL & LOGISTICS VIEWPOINT 2020 UK CONTENTS FOREWORD 4 NATIONAL MARKET 6 LONDON & THE SOUTH EAST 8 WEST LONDON 10 SOUTH WEST 12 MIDLANDS 14 NORTH WEST 16 YORKSHIRE & THE NORTH EAST 18 SCOTLAND 20 NORTHERN IRELAND 22 CAPITAL MARKETS 24 2 3 We are pleased to launch our new Industrial and Logistics Viewpoint 2020, which is designed to give you an overview of national and regional activity. Despite the political and economic uncertainty that many businesses in the UK faced in 2019, the Industrial and Logistics sector has remained resilient. Some of the key findings of this Viewpoint include: • Demand for industrial and logistics space in 2019 remained strong with take-up reaching in excess of 30m sq ft for the year, exceeding the 10-year annual average by 17%, but 14% below the record breaking 2018 • The industrial sector out-performed all other property asset classes in 2019, partly driven by very strong rental growth in London and key South East locations • Rental growth is expected to moderate in 2020, although logistics units located in heavily populated areas will reach above average returns • At the beginning of the year we were expecting 2020 to be a record year in terms of demand. However, material downside risks associated with the Covid-19 virus may limit the occupational upside. Should the virus run its course in the first half of 2020, we may expect to see a busy second half as occupiers regroup and press ahead with urgent projects For an informal chat, please do not hesitate to get in touch with either myself or one of the team. -

Londonmetric Property Plc Notice of Annual General Meeting Transfer Of

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take, you should seek your own personal financial advice from your stockbroker, bank manager, solicitor, accountant, or other financial advisor authorised under the Financial Services and Markets Act 2000. If you have sold or otherwise transferred all your ordinary shares, please send this document, together with the accompanying documents, as soon as possible to the purchaser or transferee, or to the stockbroker, bank or other agent through whom the sale or transfer was effected, for delivery to the purchaser or transferee. The distribution of this document in jurisdictions other than the United Kingdom may be restricted by the laws of those jurisdictions and therefore persons into whose possession this document comes should inform themselves about and observe any such restrictions. Failure to comply with any such restrictions may constitute a violation of the securities law of any such jurisdiction. LondonMetric Property Plc (incorporated and registered in England and Wales under company registration number 7124797) Notice of Annual General Meeting Transfer of Listing Category Your attention is drawn to the letter from the Chairman of LondonMetric Property Plc which contains the unanimous recommendation of the Directors that you vote in favour of the resolutions proposed at this Annual General Meeting. Notice of the Annual General Meeting of LondonMetric Property Plc to be held at 10.00 a.m. on 17 July 2014 at The Connaught, Carlos Place, Mayfair, London W1K 2AL is set out at the end of this document. -

Mount Allison University Endowment Fund Holdings As of December 31, 2017

Mount Allison University Endowment Fund Holdings As of December 31, 2017 Security Name Market Value ($Can) EQUITY HOLDINGS Canadian Holdings 5N PLUS INC $ 155 ABSOLUTE SOFTWARE CORP $ 851 ACADIAN TIMBER CORP $ 302 ADVANTAGE OIL & GAS LTD $ 283,788 AECON GROUP INC $ 1,728 AFRICA OIL CORP $ 684 AG GROWTH INTERNATIONAL INC $ 1,163 AGELLAN COMMERCIAL REAL ESTATE $ 349 AGF MANAGEMENT LTD $ 990 AGNICO-EAGLE MINES LTD $ 427,207 AGT FOOD AND INGREDIENTS INC $ 653 AIMIA INC $ 832 AIR CANADA INC $ 325,411 AIRBOSS OF AMERICA CORP $ 315 ALACER GOLD CORP $ 1,289 ALAMOS GOLD INC $ 2,216 ALAMOS GOLD INC NEW COM CLASS A $ 4,877 ALARIS ROYALTY CORP $ 1,107 ALGOMA CENTRAL CORP $ 330 ALIMENTATION COUCHE-TARD INC $ 98,854 ALIO GOLD INC $ 472 ALLIED PROPERTIES REAL ESTATE INVESTMENT TRUST $ 2,575 ALTIUS MINERALS CORP $ 1,233 ALTUS GROUP LTD/CANADA $ 1,916 ANDREW PELLER LTD $ 1,448 ARGONAUT GOLD INC $ 656 ARTIS REAL ESTATE INVESTMENT TRUST $ 1,539 ASANKO GOLD INC $ 209 ATCO LTD $ 119,947 ATHABASCA OIL COP $ 703 ATS AUTOMATION TOOLING SYSTEMS INC $ 1,769 AURICO METALS INC $ 311 AUTOCANADA INC $ 1,128 AVIGILON CORP $ 1,258 B2GOLD CORP $ 29,898 BADGER DAYLIGHTING LTD $ 1,525 BANK OF MONTREAL $ 725,449 BANK OF NOVA SCOTIA $ 2,019,757 BARRICK GOLD CORP $ 459,749 BAYTEX ENERGY CORP $ 1,213 BCE INC $ 791,441 BELLATRIX EXPLORATION LTD $ 94 BIRCHCLIFF ENERGY LTD $ 1,479 BIRD CONSTRUCTION INC $ 731 1 Mount Allison University Endowment Fund Holdings As of December 31, 2017 Security Name Market Value ($Can) BLACK DIAMOND GROUP LTD $ 95 BLACKBERRY LIMITED $ 151,777 BLACKPEARL RESOURCES INC $ 672 BOARDWALK REAL ESTATE INVESTMENT TRUST $ 1,610 BONAVISTA ENERGY CORP $ 686 BONTERRA ENERGY CORP $ 806 BORALEX INC $ 2,276 BROOKFIELD ASSET MANAGEMENT INCORPORATED $ 672,870 BROOKFIELD INFRASTRUCTURE PARTNERS L.P. -

2020 Real Estate Review

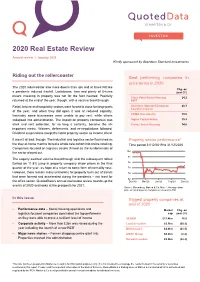

2020 Real Estate Review Annual review | January 2021 Kindly sponsored by Aberdeen Standard Investments Riding out the rollercoaster Best performing companies in price terms in 2020 The 2020 rollercoaster saw more downs than ups and at times felt like Chg. on a pandemic induced freefall. Lockdowns, tiers and plenty of U-turns year (%) meant investing in property was not for the faint hearted. Positivity Triple Point Social Housing 24.2 returned at the end of the year, though, with a vaccine breakthrough. REIT Retail, leisure and hospitality sectors were forced to close for large parts Aberdeen Standard European 20.3 Logistics Income of the year, and when they did open it was at reduced capacity. Inevitably some businesses were unable to pay rent, while others CEIBA Investments 19.0 collapsed into administration. The impact on property companies was Sigma Capital Group 15.9 stark and rent collection, for so long a certainty, became the all- Civitas Social Housing 14.8 important metric. Waivers, deferments, and re-negotiations followed. Dividend suspensions swept the listed property sector as income dived. It wasn’t all bad, though. The industrial and logistics sector flourished as Property sector performance* the stay-at-home mantra forced a whole new cohort into online retailing. Time period 31/12/2019 to 31/12/2020 Companies focused on logistics assets thrived as the fundamentals of the sector played out. 102 94 The eagerly awaited vaccine breakthrough and the subsequent rollout fuelled an 11.8% jump in property company share prices in the final 86 quarter of the year, as hope of a return to some form of normality rose. -

Men and Women Working Together for Real Change

Men and women working together for real change February 2018 30% Club . The 30% Club is a global campaign that signs up Chairs and CEOs to take action to create a better balance of men and women at all levels of their organisations as a business imperative rather than a ‘women’s issue’. The Club launched in the UK in 2010 with a target of a minimum of 30% women on FTSE-100 boards by 2015. There are 259 members of the UK Club and the proportion of female FTSE-100 directors has risen from 12.5% to 28.4%*. As of 2016 the scope of the above target was extended to a minimum of 30% women on FTSE-350 boards by end 2020 (currently at 24.8%*) . In tandem with the above – and in order to ensure that this 30% remains sustainable – we have also established a pipeline target of a minimum of 30% women at senior management level of FTSE-100 companies by 2020 (currently 25.2% at Executive Committee + direct report levels**). The 30% Club is becoming an international community. It complements and amplifies individual company efforts and existing initiatives through collaboration, sharing of best practice, measurable goals and joined-up actions. The 30% Club does not believe in mandatory quotas. Instead, the 30% Club is aiming for meaningful, sustainable, business- led change, as recommended by the Davies and Hampton-Alexander Reviews. Scarce representation of women at senior levels is a global phenomenon. Local 30% Clubs have been launched in the US, Hong Kong, Ireland, Southern Africa, Australia, Malaysia, Canada, Italy, the GCC and Turkey. -

TR Property Investment Trust Plc – Report & Accounts for the Year Ended 31 March 2009 Report Investment Trusttr Property Plc –

TR Property Investment Trust plc –TR Property Investment Trust Report March 2009 & Accounts for the year ended 31 TR Property Investment Trust plc Report & Accounts for the year ended 31 March 2009 TR Property Investment Trust plc is managed by This document is printed on Revive Silk of which 75% of the furnish is made from 100% de-inked post consumer waste. The remaining 25% being mill broke and virgin fibres. This paper is bleached using a combination of Totally Chlorine Free (TCF) and Elemental Chlorine Free (ECF). The manufacturing mill is accredited with the ISO 14001 standard for environmental management. TR Property Investment Trust plc Directors’ Review Accounts 1 Overview 63 Independent Auditors’ Report 2 Statement of Investment Objective and Policy 64 Group Income Statement 4 Financial Highlights and Performance 65 Group and Company Statement of Changes in Equity 5 Historical Performance 66 Group and Company Balance Sheets 6 Chairman’s Statement 67 Group and Company Cash Flow Statements 11 Managers’ Report – Market Background and Outlook 68 Notes to the Financial Statements 16 Ordinary Shares – Financial Highlights and Performance Shareholder Information 17 Ordinary Shares – Manager’s Report 86 Notice of Annual General Meeting 22 Ordinary Shares – Portfolio Details 89 Explanation of Notice of Annual General Meeting 28 Ordinary Shares – Income Statement 90 Glossary of Terms 29 Ordinary Shares – Balance Sheet 91 Directors and Other Information 30 Sigma Shares – Financial Highlights and Performance 92 General Shareholder Information -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 30 January 2020 Big Yellow Group BYG Real Estate Investment Trusts — GBP 11.75 at close 30 January 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 30-Jan-2020 30-Jan-2020 30-Jan-2020 12 120 120 1D WTD MTD YTD Absolute 0.6 -0.4 -2.1 -2.1 11.5 115 Rel.Sector 1.0 1.0 0.0 0.0 115 Rel.Market 1.9 2.2 0.1 0.1 11 110 110 VALUATION 10.5 105 Trailing RelativePrice RelativePrice 105 10 100 PE 15.8 Absolute(localPrice currency) EV/EBITDA 34.7 100 9.5 95 PB 1.8 PCF 27.6 9 95 90 Div Yield 1.7 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Price/Sales +ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.3 100 90 90 Div Payout 43.4 90 80 80 ROE 12.0 80 70 70 Share Index) Share Share Sector) Share - 70 - 60 DESCRIPTION 60 60 50 50 The principal activity of the Company and its 50 40 RSI RSI (Absolute) subsidiaries is the provision of self storage and 40 related services. 40 30 30 20 30 RSI (Relative to FTSE UKFTSE All to RSI (Relative RSI (Relative to FTSE UKFTSE All to RSI (Relative 20 10 20 Jan-2019 Mar-2019 May-2019 Jul-2019 Sep-2019 Nov-2019 Jan-2019 Mar-2019 May-2019 Jul-2019 Sep-2019 Nov-2019 Jan-2019 Mar-2019 May-2019 Jul-2019 Sep-2019 Nov-2019 See final page and http://www.londonstockexchange.com/prices-and-markets/stocks/services-stock/ftse-note.htm for further details. -

Interim Results Presentation 6 Months Ended 31 December 2015

Half Year Results Presentation 6 months ended 31 December 2015 Agenda • Introduction - Edward Ziff, Chairman and CEO • Strategy overview • Active first half • Good financial performance • Financial Performance & Portfolio Overview - Duncan Syers, FD • Portfolio Activity • Leeds – Merrion House, Merrion Hotel & Whitehall Riverside Scheme • Capital Recycling Programme • CitiPark • Investment Case & Outlook • Questions 2 Strategy Overview • Intensive asset management based on local knowledge • Conservative funding • Regional focus - Leeds, Manchester, suburban London • Ongoing capital recycling • Investment in car parking Focus on shareholder returns, proven by 55 years of unbroken dividends 3 Active first half Active asset management in a low growth market • Portfolio re-positioning and capital recycling • Acquisition in suburban London for £6m • Two disposals for £13.1m – Glasgow, Leeds • Creating investments on development sites • Merrion House, Merrion Hotel and Premier Inn on Whitehall Road • Adding £7.5m to assets and £2m to income in FY17 and FY18 • Ongoing asset management of existing portfolio • 104 transactions in 6 months and like for like passing rent up by £0.8m (4.6%) • Car parking • Profits increased due to strong portfolio of acquisitions • Value of freehold assets increased 4 Delivering Total Shareholder Returns 6m to Dec 15 12m to Dec 15 Big Yellow Group PLC 28.4 Safestore Holdings plc 58.8 Safestore Holdings plc 27.8 Big Yellow Group PLC 36.9 Capital & Regional plc 15.6 Capital & Regional plc 27.9 Tritax Big Box REIT Plc