FTSE Factsheet

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Aberdeen Standard OEIC ASI UK Real Estate Share (Class a Acc [GBP])](https://docslib.b-cdn.net/cover/3695/aberdeen-standard-oeic-asi-uk-real-estate-share-class-a-acc-gbp-13695.webp)

Aberdeen Standard OEIC ASI UK Real Estate Share (Class a Acc [GBP])

Aberdeen Standard OEIC ASI UK Real Estate Share (Class A Acc [GBP]) Benchmark Aims Benchmark FTSE 350 Real Estate To generate income and some growth over the long term (5 years or more) by investing in UK property-related equities (company shares) including listed closed ended real estate investment trusts (“REITs”). Performance IA sector Property Target: To achieve the return of the FTSE 350 Real Estate Index plus 3% per annum (before charges) over rolling three year periods. The Performance Target is the level of performance that the management team hopes to Identification Codes achieve for the fund. There is however no certainty or promise that they will achieve the Performance Target. The ACD believes this is an appropriate target for the fund based on the investment policy of the fund and the Sedol code B0XWNM5 constituents of the index. Mex code AFPRSA ISIN code GB00B0XWNM59 Performance Fund Overview Price Bid 178.69p Offer 178.69p (24/09/2021) Historic yield 1.11% Fund size £468.6m Number of holdings 32 Concentration Coefficient* 23 Charges Discounted initial charge 0.000% Net discounted AMC 0.750% Initial charge 4.25% Annual Management Charge 1.50% Exit charge None Performance fees No Cumulative Performance (%) 3m 6m 1Yr 3Yr 5Yr Fund Background Fund 7.72% 19.32% 35.73% 44.71% 70.86% Valuation point Daily 12:00 Sector 2.76% 13.07% 22.94% 20.79% 31.89% Fund type OEIC Rank 3/26 4/26 2/24 1/20 1/20 Launch date 29/10/1990 Quartile 1 1 1 1 1 Launch price £0.50 Discrete Performance (%) - to last month end Fund currency Pound Sterling -

REAL ESTATE July 2020

LISTED MARKETS – REAL ESTATE July 2020 Leo Zielinski Partner Tel. +44 (0)7980 809031 [email protected] John Rodgers Partner Tel. +44 (0)7810 307422 [email protected] Will Strachan Partner Tel. +44 (0)7929 885859 [email protected] Lloyd Davies We track the share price movement and regulatory announcements Partner of 57 real estate owning listed entities (“Gerald Eve tracked index”). Tel. +44 (0)7767 311254 A summary of the Gerald Eve tracked index in terms of GAV, NAV, [email protected] LTV, Dividend, Share Price, Market Cap, Discount/Premium to NAV and their respective weekly movement is attached. Lorenzo Solazzo Data Analyst We provide a comparison to share price data from 3 February 2020 Tel. +44 (0)783 309 5582 [email protected] (pre-Covid-19 level) to present day to demonstrate the impact across certain entities as a direct result of Covid-19. James Brown Surveyor As at 30 of June, the Gerald Eve tracked index is currently down 30% to pre- Tel. +44 (0)7464 656563 Covid-19 level, under-performing the FTSE350 which is slowly recovering and is [email protected] now down 16%. The tracked listed REITs share price decreased on average 3% since 1 June 2020 (March: -25%, April: +6%, May: -3%). To provide context around the share price movement, the average discount to NAV is currently 31% against 3% pre-Covid-19. It is unsurprising to note that specialist sector entities across Industrial, Healthcare and Supermarkets have out-performed the REIT universe relative to other strategies within the Gerald Eve tracked index. -

COVID-19 Proxy Governance Update

COVID-19 Proxy Governance Update 2020 AGM mid-season review FROM EQUINITI 01 Looking back and planning ahead It is incredible to note that it has been over 12 weeks since the official announcement on 23 March of the UK Government’s Stay at Home Measures, and nearly seven months since the severity of the pandemic became apparent in China. Over the said period, PLC boards, company secretaries and investor relations officers have kept their corporate calendars going thanks to rapid adoption of modified regulatory guidelines and inventive modes of engagement with investors. With annual general meetings being an obvious highlight in the corporate calendar, we take stock of the progress made so far over the 2020 AGM season, as well as using what we learned to plan ahead. Now that we are over the first ‘hump’ with the busy period of May AGMs out of the way, we are readying for the second ‘peak’ of June and July AGMs, and then an ‘easing’ until the second ‘mini’ season in the early autumn. As such, in this update, we look at: • 2020 AGM season statistics…so far • Proxy adviser engagement and ISS recommendations review • High-level assumptions for Q3 and Q4 • Relevant updates from the regulators, industry bodies and proxy advisers • Communications in the COVID-19 world – special commentary by leading financial PR firm,Camarco • How has COVID-19 impacted activism – special commentary by international law firm,White & Case 02 2020 AGM Season Statistics…so far Scope of data To assess progress and forecast what is to come, we look at the key statistics for the UK AGM season 2020 thus far. -

Disclaimer Strictly Not to Be Forwarded to Any

DISCLAIMER STRICTLY NOT TO BE FORWARDED TO ANY OTHER PERSONS IMPORTANT: You must read the following disclaimer before reading, accessing or making any other use of the attached document relating to SEGRO plc (the “Company”) dated 10 March 2017. In accessing the attached document, you agree to be bound by the following terms and conditions, including any modifications to them from time to time, each time you receive any information from us as a result of such access. You acknowledge that this electronic transmission and the delivery of the attached document is confidential and intended for you only and you agree you will not forward, reproduce, copy, download or publish this electronic transmission or the attached document (electronically or otherwise) to any other person. The attached document has been prepared solely in connection with the proposed rights issue and offering of nil paid rights, fully paid rights and new ordinary shares (the “Securities”) of the Company (the “Transaction”). The Prospectus has been published in connection with the admission of the Securities to the Official List of the UK Financial Conduct Authority (the ‘‘Financial Conduct Authority’’) and to trading on the London Stock Exchange plc’s main market for listed securities (together, ‘‘Admission’’). The Prospectus has been approved by the Financial Conduct Authority as a prospectus prepared in accordance with the Prospectus Rules made under section 73A of the Financial Services and Markets Act 2000, as amended. NOTHING IN THIS ELECTRONIC TRANSMISSION AND THE ATTACHED DOCUMENT CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. -

Exciting New Retail and Leisure Opportunity in the Centre of Milton Keynes

MILTON KEYNES EXCITING NEW RETAIL AND LEISURE OPPORTUNITY IN THE CENTRE OF MILTON KEYNES 809-811 Silbury Boulevard , Milton Keynes HOME INTRODUCTION LOCATION MILTON KEYNES RETAIL AND SITE PLAN AVAILABILITY LEISURE THE DEVELOPER OPPORTUNITY 02 CONTACT Retail and leisure units to let Two new commercial units with flexible planning consent for A1-A5 / D1 & B1 uses Unit sizes 1,959 sq ft (182 sq m) and 1,808 sq ft (168 sq m) Units can be combined to create one large unit of 3,767 sq ft (349 sq m) Directly opposite John Lewis entrance and Centre:MK Located directly beneath 132 new homes built for rent by Grainger Plc. For further information go to www.solstice-apartments.co.uk HOME INTRODUCTION LOCATION MILTON KEYNES SITE PLAN AVAILABILITY LOCATION THE DEVELOPER AERIAL 03 CONTACT SNOZONE / 12TH INTU SHOPPING CENTRE: JOHN XSCAPE STREET CENTRE MK LEWIS MILTON KEYNES MILTON KEYNES THEATRE ROSE HOME INTRODUCTION LOCATION MILTON KEYNES SITE PLAN AVAILABILITY LOCATION THE DEVELOPER NEIGHBOURS 04 CONTACT EAT/DRINK/RETAIL es) 1 Las Iguanas 18 Oliver Bonas M1 (2 mil 2 Byron Burger 19 White Stuff 3 Brasserie Blanc 20 Halifax 4 Carluccios 21 Pizza Hut 10 15 John Lewis 5 Lloyds Bank 22 McDonald’s Lloyds Court 5 8 1 6 Mothercare 23 Monsoon MK 6 Gallery 7 Ask Italian 24 Paperchase 7 16 9 Theatre 8 Next 25 Apple 2 13 24 9 Lakeland 26 Gap 14 4 11 10 John Lewis 27 H&M 17 Centre:MK 23 Secklow 11 Debenhams 28 Hollister 18 22 ard 19 7 12 Marks & Spencer 29 Michael Kors 12 21 Boulev 20 Gate 13 Primark 30 Sports Direct y 26 27 Snozone/Xscape A509 25 28 3 14 TK Maxx 31 T.M. -

Unlocking Potential What’S in This Report

Great Portland Estates plc Annual Report 2013 Unlocking potential What’s in this report 1. Overview 3. Financials 1 Who we are 68 Group income statement 2 What we do 68 Group statement of comprehensive income 4 How we deliver shareholder value 69 Group balance sheet 70 Group statement of cash flows 71 Group statement of changes in equity 72 Notes forming part of the Group financial statements 93 Independent auditor’s report 95 Wigmore Street, W1 94 Company balance sheet – UK GAAP See more on pages 16 and 17 95 Notes forming part of the Company financial statements 97 Company independent auditor’s report 2. Annual review 24 Chairman’s statement 4. Governance 25 Our market 100 Corporate governance 28 Valuation 113 Directors’ remuneration report 30 Investment management 128 Report of the directors 32 Development management 132 Directors’ responsibilities statement 34 Asset management 133 Analysis of ordinary shareholdings 36 Financial management 134 Notice of meeting 38 Joint ventures 39 Our financial results 5. Other information 42 Portfolio statistics 43 Our properties 136 Glossary 46 Board of Directors 137 Five year record 48 Our people 138 Financial calendar 52 Risk management 139 Shareholders’ information 56 Our approach to sustainability “Our focused business model and the disciplined execution of our strategic priorities has again delivered property and shareholder returns well ahead of our benchmarks. Martin Scicluna Chairman ” www.gpe.co.uk Great Portland Estates Annual Report 2013 Section 1 Overview Who we are Great Portland Estates is a central London property investment and development company owning over £2.3 billion of real estate. -

LXI REIT Plc Prospectus.Pdf

168594 Project Olympus - Prospectus Intro_168594 Project Olympus - Prospectus Intro 06/02/2017 10:43 Page 1 168594 Proof 3 Monday, February 6, 2017 10:43 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt about the action you should take, you are recommended to seek your own financial advice immediately from an independent financial adviser who is authorised under the Financial Services and Markets Act 2000 (as amended) (“FSMA”) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. A copy of this document, which comprises a prospectus relating to LXI REIT plc (the “Company”) prepared in accordance with the Prospectus Rules of the UK Listing Authority made pursuant to section 73A of the FSMA, has been filed with the Financial Conduct Authority in accordance with Rule 3.2 of the Prospectus Rules. Applications will be made to the UK Listing Authority and the London Stock Exchange for the Ordinary Shares to be issued in connection with the Issue and each Subsequent Placing under the Placing Programme to be admitted to listing on the premium listing segment of the Official List and to trading on the premium segment of the main market for listed securities of the London Stock Exchange respectively. It is expected that First Admission will become effective and that dealings for normal settlement in the Ordinary Shares will commence on 27 February 2017. It is expected that any Subsequent Admission pursuant to Subsequent Placings under the Placing Programme will become effective and dealings will commence between 28 February 2017 and 5 February 2018. -

Description Iresscode Exchange Current Margin New Margin 3I

Description IRESSCode Exchange Current Margin New Margin 3I INFRASTRUCTURE PLC 3IN LSE 20 20 888 HOLDINGS PLC 888 LSE 20 20 ASSOCIATED BRITISH ABF LSE 10 10 ADMIRAL GROUP PLC ADM LSE 10 10 AGGREKO PLC AGK LSE 20 20 ASHTEAD GROUP PLC AHT LSE 10 10 ANTOFAGASTA PLC ANTO LSE 15 10 ASOS PLC ASC LSE 20 20 ASHMORE GROUP PLC ASHM LSE 20 20 ABERFORTH SMALLER COM ASL LSE 20 20 AVEVA GROUP PLC AVV LSE 20 20 AVIVA PLC AV LSE 10 10 ASTRAZENECA PLC AZN LSE 10 10 BABCOCK INTERNATIONAL BAB LSE 20 20 BARR PLC BAG LSE 25 20 BARCLAYS PLC BARC LSE 10 10 BRITISH AMERICAN TOBA BATS LSE 10 10 BAE SYSTEMS PLC BA LSE 10 10 BALFOUR BEATTY PLC BBY LSE 20 20 BARRATT DEVELOPMENTS BDEV LSE 10 10 BARING EMERGING EUROP BEE LSE 50 100 BEAZLEY PLC BEZ LSE 20 20 BH GLOBAL LIMITED BHGG LSE 30 100 BOWLEVEN PLC BLVN LSE 60 50 BANKERS INVESTMENT BNKR LSE 20 20 BUNZL PLC BNZL LSE 10 10 BODYCOTE PLC BOY LSE 20 20 BP PLC BP LSE 10 10 BURBERRY GROUP PLC BRBY LSE 10 10 BLACKROCK WORLD MININ BRWM LSE 20 65 BT GROUP PLC BT-A LSE 10 10 BRITVIC PLC BVIC LSE 20 20 BOVIS HOMES GROUP PLC BVS LSE 20 20 BROWN GROUP PLC BWNG LSE 25 20 BELLWAY PLC BWY LSE 20 20 BIG YELLOW GROUP PLC BYG LSE 20 20 CENTRAL ASIA METALS PLC CAML LSE 40 30 CLOSE BROTHERS GROUP CBG LSE 20 20 CARNIVAL PLC CCL LSE 10 10 CENTAMIN PLC CEY LSE 20 20 CHARIOT OIL & GAS LTD CHAR LSE 100 100 CHEMRING GROUP PLC CHG LSE 25 20 CONYGAR INVESTMENT CIC LSE 50 40 CALEDONIA INVESTMENTS CLDN LSE 25 20 CARILLION PLC CLLN LSE 100 100 COMMUNISIS PLC CMS LSE 50 100 CENTRICA PLC CNA LSE 10 10 CAIRN ENERGY PLC CNE LSE 30 30 COBHAM PLC -

XINT F UK Real Estate P GBP Index

As of December 30, 2020 XINT F UK Real Estate P GBP Index DE000A13PXZ5 GBP The XINT F UK Real Estate P GBP Index is a free-float adjusted index, designed to track the performance of real estate companies and REITS listed on the London Stock Exchange. INDEX PERFORMANCE - PRICE RETURN 120 115 110 105 100 95 90 85 80 75 70 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Returns (p.a) Standard Deviation (p.a) Maximum Drawdown 3M 69.43% 3M 23.80% From 14.02.2020 6M 21.90% 6M 21.90% To 19.03.2020 1Y -17.08% 1Y -17.08% Return -38.63% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com Top 10 Constituents FFMV (GBPm) Weight % Industry Sector Segro PLC 11,298 19.84 Real Estate Land Securities Group PLC 4,910 8.62 Real Estate British Land Company PLC 4,630 8.13 Real Estate Unite Group PLC 3,341 5.87 Real Estate Derwent London PLC 3,136 5.51 Real Estate Tritax Big Box REIT Plc 2,866 5.03 Real Estate LondonMetric Property PLC 2,059 3.61 Real Estate Assura PLC 2,021 3.55 Real Estate Primary Health Properties PLC 1,989 3.49 Real Estate Grainger PLC 1,900 3.34 Real Estate Total 38,151 66.99 This information has been prepared by Index Intelligence GmbH (“IIG”). All information is provided "as is" and IIG makes no express or implied warranties, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included herein. -

Recommended Cash and Share Offer for A&J Mucklow Group

172591 Proof 2 Thursday, May 23, 2019 03:22 NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OR REGULATIONS OF SUCH JURISDICTION. THIS ANNOUNCEMENT IS DEEMED BY LONDONMETRIC AND MUCKLOW TO CONTAIN INSIDE INFORMATION AS STIPULATED UNDER THE MARKET ABUSE REGULATION NO 596/2014. UPON THE PUBLICATION OF THIS ANNOUNCEMENT VIA A REGULATORY INFORMATION SERVICE, THIS INSIDE INFORMATION IS NOW CONSIDERED TO BE IN THE PUBLIC DOMAIN. THIS ANNOUNCEMENT IS AN ADVERTISEMENT AND NOT A PROSPECTUS OR PROSPECTUS EQUIVALENT DOCUMENT AND INVESTORS SHOULD NOT MAKE ANY INVESTMENT DECISION IN RELATION TO THE NEW LONDONMETRIC SHARES EXCEPT ON THE BASIS OF INFORMATION IN THE SCHEME DOCUMENT AND THE COMBINED CIRCULAR AND PROSPECTUS WHICH ARE PROPOSED TO BE PUBLISHED IN DUE COURSE. 23 May 2019 FOR IMMEDIATE RELEASE RECOMMENDED CASH AND SHARE OFFER FOR A&J MUCKLOW GROUP PLC (“MUCKLOW”) BY LONDONMETRIC PROPERTY PLC (“LONDONMETRIC”) to be effected by means of a Scheme of Arrangement under Part 26 of the Companies Act 2006 Summary The boards of directors of LondonMetric and Mucklow are pleased to announce that they have reached agreement on the terms of a recommended offer pursuant to which LondonMetric will acquire the entire issued and to be issued ordinary share capital of Mucklow (the “Combination” forming the “Combined Group”). The Combination is to be effected by means of a scheme of arrangement under Part 26 of the Companies Act. Under the terms of the Combination, for each Mucklow Ordinary Share, Mucklow Shareholders will be entitled to receive: 2.19 New LondonMetric Shares and 204.5 pence in cash On the basis of the Closing Price per LondonMetric Ordinary Share of 205.8 pence on 22 May 2019, the Combination values each Mucklow Ordinary Share at 655.2 pence and the entire issued and to be issued ordinary share capital of Mucklow at approximately £414.7 million. -

The Intu Difference Intu Properties Plc Annual Report 2016 Welcome to Our Annual Report 2016

The intu difference intu properties plc Annual report 2016 Welcome to our annual report 2016 Our purpose is to create compelling, joyful experiences that surprise and delight our customers and make them smile. We are a people business and everything we do is guided by our culture and our values. We’re passionate about providing people with their perfect shopping experience so that our retailers flourish. And it’s this that powers our business, creating opportunity for our retailers and value for our investors; benefiting our communities and driving our long-term success. Contents Overview Governance Highlights of 2016 2 Chairman’s introduction 58 Our top properties 4 Board of Directors 60 Executive Committee 62 Strategic report The Board 63 Chairman’s statement 6 Viability statement 68 Chief Executive’s review 8 Audit Committee 69 Our growth story 10 Nomination and Review Committee 74 Investment case 12 Directors’ remuneration report 76 Directors’ report 94 The intu difference Statement of Directors’ responsibilities 96 Making the difference 14 Understanding our markets 16 Financial statements Optimising asset performance 18 Independent auditors’ report 98 Delivering UK developments 20 Consolidated income statement 106 Making the brand count 22 Consolidated statement of Seizing the growth opportunity in Spain 24 comprehensive income 107 At the heart of communities 26 Balance sheets 108 Our business model 28 Statements of changes in equity 109 Relationships 30 Statements of cash flows 112 Strategy overview 32 Notes to the financial statements -

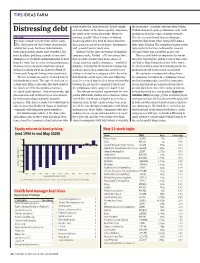

Distressing Debt Seek out Shares in the Lowest Quality Companies; Verdad Compared Equity Performance with Credit the Worst-Of-The-Worst, If You Like

TIPS IDEAS FARM want to play the ‘dash for trash’ should simply the issue price. A similar story was found when Distressing debt seek out shares in the lowest quality companies; Verdad compared equity performance with credit the worst-of-the-worst, if you like. However, quality based on the scores of rating agencies. ALGY HALL ignoring ‘quality’ when it comes to buying Here the research found share performance t’s been a tough time for short sellers lately. beaten-up stocks (the kind of shares found on started to deteriorate when ratings fell below a IThe ‘dash for trash’ that I wrote about in this these pages in our tables of shorts, downgrades high single B rating. The annualised equity return column last week, has been indiscriminate. and 52-week lows) is rarely wise. from stocks in the least creditworthy category Even real no-hoper shares have benefited. The Intrigued by the price movement of bankrupt- (CC and below) was a negative 34 per cent. most headline-grabbing example of investors’ company stocks, Verdad – a US investment firm This research holds an important lesson for willingness to overlook all fundamentals in their that specialises in investing in the shares of investors targeting the grubbier end of this recov- hunt for ‘trash’ has been the strong performance cheap, indebted, smaller companies – trawled its ery. Rather than buying the worst-of-the-worst, of shares in US companies that have already database. It looked for the long-term relationship it’s the best-of-the-worst that should provide the declared bankruptcy or are about to (Hertz, JC between share price performance and the level optimal trade-off between risk and reward.