Doing Business in Uganda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Gender Equality Seal for Private Entreprises in Uganda

The Gender Equality Seal for Private Entreprises in Uganda. A certification program that enables businesses to increase productivity, profitability and partnerships through: Employee performance schemes that reduce gender-gaps at the work place. Innovations for gender-appropriate product design and customer services. Networking with global companies that support the sustainable development goals. What the Gender Equality Seal is about: The Gender Equality Seal (GES) promotes investment in systems that integrate gender equality into the work environment and business strategies. It is a learning and certification programme, supported by the United Nations Development Programme (UNDP), to help businesses achieve Gender Equality, which is Goal Five of the 17 Sustainable Development Goals. (SDGs). The SDGs (global goals), were signed up by world leaders in September 2015 at the United Nations General Assembly in New York. Private companies that get the Gender Equality Seal certification attain sustainable business growth, which in turn leads to sustainable development. Why getting the Seal is good for private companies: The Gender Equality Seal certification programme provides private companies a mechanism to level the playing field for both women and men at the work place. It also helps companies to make their human resource management systems equitable and more gender sensitive. Working to achieve the Gender Equality Seal helps management of private companies understand how their decisions affect female staff compared to male colleagues; how gender-pay-gaps come about and how to work out a work-life-balance for employees. ...Compliments Certification of Government Institutions. For Government, the Gender Equality Seal complements the Gender and Equity Certificate that is used to assess the gender responsiveness of sector plans and budgets, as provided for by the Public Finance Management Act (PFM 2014). -

THE REPUBLIC of UGANDA in the HIGH COURT of UGANDA(HCT) at KAMPALA COMMERCIAL REGISTRY CAUSELIST for the SITTINGS of : 12-11-2018 to 16-11-2018

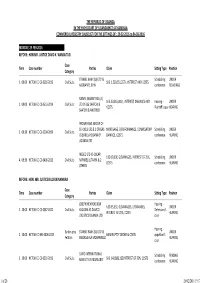

THE REPUBLIC OF UGANDA IN THE HIGH COURT OF UGANDA(HCT) AT KAMPALA COMMERCIAL REGISTRY CAUSELIST FOR THE SITTINGS OF : 12-11-2018 to 16-11-2018 MONDAY, 12-NOV-2018 BEFORE:: HON MR. JUSTICE DAVID K. WANGUTUSI COURT ROOM :: Time Case number Case Category Pares Claim Sing Type Posion UGANDA NATIONAL COTTON Hearing - FARMERS FEDERATION LTD VS UNDER 1. 09:00 HCT-00-CC-CS-0467-2016 Civil Suits SHS 500,400,000, G/DAMAGES & COSTS Plainff's THE COOPER MOTOR HEARING case CORPORATION (U) LTD BEFORE:: HON. LADY JUSTICE ALIVIDZA ELIZABETH JANE COURT ROOM :: Time Case number Case Category Pares Claim Sing Type Posion EDWARD RONALD SEKYEWA T/A Hearing - HUB FOR INVESTGATIVE ME VS SHS. 500,000,000, INJUCTION AGG. DAMAGES, UNDER 1. 09:00 HCT-00-CC-CS-0669-2014 Civil Suits Plainff's ANTI-CORRUPTION COALITION U G/DAMAGES, COSTS HEARING case & OTHERS BRAIN RUGYENDO VS HENRY PENDING 2. 09:00 HCT-00-CC-CS-0209-2017 Civil Suits DECLARATION G/DAMAGES SHS 105,000,000 Menon SSEMUGOOMA KALYAMAGWA HEARING GEOFFREY KARUGIRA VS UAP COMPENSATION, G/DAMAGES, INTEREST, Scheduling UNDER 3. 10:00 HCT-00-CC-CS-0688-2017 Civil Suits OLD MUTUAL INSURANCE COSTS conference PLEADINGS UGANDA LTD NAKASINDE SARAH VS M/S UNDER 4. 10:00 HCT-00-CC-CS-0335-2017 Civil Suits CHENSHIA FINANCIAL SERVICES DECLARATION, G/DAMAGES, COSTS Menon PLEADINGS LTD VERMA JIVRAM & ASSOCIATES Hearing - Miscellaneous PENDING 5. 10:00 HCT-00-CC-MC-0244-2017 VS MERALI JIVRAJ TADIN & ADV /CLIENT BILL OF COSTS Applicant's Cause HEARING ANOTHER case GORDON ARIHO VS RAPID SHS. -

Ibnul Hasan Rizvi

IBNUL HASAN RIZVI 52/2 6th Commercial Street +923018379551 Phase 4, Defense Housing Authority, [email protected] Karachi, Pakistan SENIOR EXECUTIVE SUMMARY I am an objective driven CEO with hands on experience of profitably managing industrial enterprises employing over thousand people. A highly effective communicator and team leader with a proven record of building trust and long term relationships with both internal and external customers leading to long-term customer satisfaction & retention by focusing on QCD (quality, cost and delivery). SKILLS AND QUALIFICATIONS Implemented and executed learning enterprises, focusing on business processes at cross function level. Focusing on Six Sigma fundamentals: variance reduction and waste reduction in processes achieved lesser defects and increased efficiency. Achieved continuous improvement at all levels of the enterprise by lean manufacturing, implementing TQM, JIT, TPM and problem solving through RCA (root cause analysis). All enterprises I led were certified to ISO9000:2000/2008. Voice of the customer was the prime mover of these organizations. Customer need and desire were collected, analyzed to determine CTQ (critical to quality) attributes. Use of Quality Function Deployment (QFD) tool ensured customers desired attributes in all products and services with performance measures embedded in the process to ensure zero defect supply to customer. PROFESSIONAL EXPERIENCE Medicell Institute of Diabetes Endocrinology & Metabolism, 2015 to Present Medicell Institute of Higher Education & Training, Karachi , Pakistan Chief Executive Officer • Engaged in developing fully trained specialists in various disciplines who would serve as consultants and teachers in their respective fields. • Impart training for IELTS (International English Language Training System). Houston Independent School District, Houston, TX, USA 2009 to 2015 Associate Teacher and Science Teacher • Obtained a Post Baccalaureate in Education from the University of Houston in 2011. -

Mapping Uganda's Social Impact Investment Landscape

MAPPING UGANDA’S SOCIAL IMPACT INVESTMENT LANDSCAPE Joseph Kibombo Balikuddembe | Josephine Kaleebi This research is produced as part of the Platform for Uganda Green Growth (PLUG) research series KONRAD ADENAUER STIFTUNG UGANDA ACTADE Plot. 51A Prince Charles Drive, Kololo Plot 2, Agape Close | Ntinda, P.O. Box 647, Kampala/Uganda Kigoowa on Kiwatule Road T: +256-393-262011/2 P.O.BOX, 16452, Kampala Uganda www.kas.de/Uganda T: +256 414 664 616 www. actade.org Mapping SII in Uganda – Study Report November 2019 i DISCLAIMER Copyright ©KAS2020. Process maps, project plans, investigation results, opinions and supporting documentation to this document contain proprietary confidential information some or all of which may be legally privileged and/or subject to the provisions of privacy legislation. It is intended solely for the addressee. If you are not the intended recipient, you must not read, use, disclose, copy, print or disseminate the information contained within this document. Any views expressed are those of the authors. The electronic version of this document has been scanned for viruses and all reasonable precautions have been taken to ensure that no viruses are present. The authors do not accept responsibility for any loss or damage arising from the use of this document. Please notify the authors immediately by email if this document has been wrongly addressed or delivered. In giving these opinions, the authors do not accept or assume responsibility for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by the prior written consent of the author This document has been prepared solely for the KAS and ACTADE. -

East Africa's Family-Owned Business Landscape

EAST AFRICA’S FAMILY-OWNED BUSINESS LANDSCAPE 500 LEADING COMPANIES ACROSS THE REGION PREMIUM SPONSORS: 2 TABLE OF CONTENTS EAST AFRICA’S FAMILY-OWNED BUSINESS CONTENTS LANDSCAPE Co-Founder, CEO 3 Executive Summary Rob Withagen 4 Methodology Co-Founder, COO Greg Cohen 7 1. MARKET LANDSCAPE Project Director 8 Regional Heavyweight: East Africa Leads Aicha Daho Growth Across the Continent Content Director 10 Come Together: Developing Intra- Jennie Forcier Patterson Regional Trade Opens Markets of Data Director Significant Scale Yusra Khadra 11 Interview: Banque du Caire Editorial Manager Lauren Mellows 13 2. FOB THEMES Research & Data Team Alexandria Akena 14 Stronger Together: Private Equity Jerome Amedo Offers Route to Growth for Businesses Laban Bore Prepared to Cede Some Ownership Jessen Chiniven Control Woyneab Habte Mayowa Hambolu 15 Interview: Centum Investment Milkiyas Lekeleh Siyum 16 Interview: Nairobi Securities Exchange Omololu Adeniran 17 A Hire Calling: Merit is Becoming a Medina Mamadou Stronger Factor in FOB Employment Kuringe Masao Melina Matabishi Practices Ivan Matoowa 18 Interview: Anjarwalla & Khanna Sweetness Mathew 21 Interview: CDC Group Plc Paige Arhaus Theodore Angwenyi 22 Interview: Melvin Marsh International Design 23 Planning for the Future: Putting Next- Nuno Caldeira Generation Leaders at the Helm 24 Interview: Britania Allied Industries 25 3. COUNTRY DEEPDIVES 25 Kenya 45 Ethiopia 61 Uganda 77 Tanzania 85 Rwanda 91 4. FOB DIRECTORY EAST AFRICA’S FAMILY-OWNED BUSINESS LANDSCAPE EXECUTIVE SUMMARY 3 EXECUTIVE -

Company Profile

COMPANY PROFILE PLOT 26A, OLD KAMPALA ROAD. PLOT 1-5, MBUYA 1 ROAD. OPP. NAKAWA COURT P.O BOX 9826 KAMPALA – UGANDA TEL: (+256) 75 0 99 22 11 (+256)41 4 236 412 FAX: (+256)41 4 234 999 EMAIL: [email protected] 1 CONTENTS Page 1. INTRODUCTION 1. Brief Overview……………………………………………….……………..3 2. Co. Philosophy …………………………………………….……………….4 3. Core Values ……………………………………………….………………..4 4. Company Vision……………………………………..….…………………..4 5. Values…………………………………………………...….……………….6 6. Mission…………………………………………………...….……………....6 7. Code of Ethics…………………………………………...….……………….6 8. Directors and Addresses………………………………..……..……………..8 9. Company Bankers..…………………………………………..………….…..9 10. Company activities…..……………………………………..………..........10 11. Organization Chart…………………………………………..……………13 2. LEGAL STATUS OF BIDDER · Certificate of Incorporation……………….………………………………...15 · VAT Certificate…………………………………………………………..…16 3. REFERENCE · References…………………………………………………...........................17 4. WORK PERFORMED AS A PRIME/SUB CONTRACTOR · List of Finished Project and Project on Hand…………………………. .…..20 5. CONTRACTOR’S EQUIPMENT( PLANT AND MACHINERY) · Equipments and Asset register……………………………………………....33 6. PERSONNEL · Candidates and C.Vs…………………………………………………....…..39 7. HEALTH AND SAFETY · Health and Safety Policy……………………………………………...….…57 2 1. OVERVIEW Halcons Ltd was incorporated in Uganda in 2011 Halcons has a humble beginning with a steady growth and has managed to attain its goals in a very short span of time. Halcons is the brain child of Two dynamic and determined entrepreneurs, -

Court Case Administration System

THE REPUBLIC OF UGANDA IN THE HIGH COURT OF UGANDA(HCT) AT KAMPALA COMMERCIAL REGISTRY CAUSELIST FOR THE SITTINGS OF : 29‐02‐2016 to 04‐03‐2016 MONDAY, 29‐FEB‐2016 BEFORE:: HON MR. JUSTICE DAVID K. WANGUTUSI Case Time Case number Pares Claim Sing Type Posion Category STANBIC BANK (U) LTD VS Scheduling UNDER 1. 09:00 HCT‐00‐CC‐CS‐0336‐2013 Civil Suits SHS. 1,239,251,357/‐, INTEREST AND COSTS KASIBANTE JOHN conference PLEADINGS SWIVEL MARKETING (U) SHS. 53,515,000/‐, INTEREST, DAMAGES AND Hearing ‐ UNDER 2. 09:00 HCT‐00‐CC‐CS‐0513‐2014 Civil Suits LTD VS QG SAATCHI & COSTS Plainff's case HEARING SAATCHI & ANOTHER PROGRESSIVE GROUP OF SCHOOLS LTD & 2 OTHERS MORTGAGE, S/PERFORMANCE, COMPESATORY Scheduling UNDER 3. 09:30 HCT‐00‐CC‐CS‐0204‐2009 Civil Suits VS BARCLAYS BANK OF DAMAGE, COSTS conference HEARING UGANDA LTD MESCO LTD VS OSCAR USD 10,000, G/DAMAGES, INTEREST OF 25%, Scheduling UNDER 4. 09:30 HCT‐00‐CC‐CS‐0400‐2013 Civil Suits RAPHAEL LUTAAYA & 2 COSTS conference HEARING OTHERS BEFORE:: HON. MR. JUSTICE BILLY KAINAMURA Case Time Case number Pares Claim Sing Type Posion Category JOSEPHINE KYOKUNDA Hearing ‐ USD 53,351, G/DAMAGES, E/DAMAGES, UNDER 1. 10:00 HCT‐00‐CC‐CS‐0587‐2012 Civil Suits KAGGWA VS DAMCO Defendant's INTEREST AT 25%, COSTS HEARING LOGISTICS UGANDA LTD case Hearing ‐ Bankruptcy STANBIC BANK (U) LTD VS UNDER 2. 10:00 HCT‐00‐CC‐BM‐0006‐2015 BANKRUPTCY ORDER & COSTS appellant's Peon SSEBAGGALA MOHAMMED HEARING case CAIRO INTERNATIONAL Scheduling PENDING 3. -

Designation of Tax Withholding Agents) Notice, 2018

LEGAL NOTICES SUPPLEMENT No. 7 29th June, 2018. LEGAL NOTICES SUPPLEMENT to The Uganda Gazette No. 33, Volume CXI, dated 29th June, 2018. Printed by UPPC, Entebbe, by Order of the Government. Legal Notice No.12 of 2018. THE VALUE ADDED TAX ACT, CAP. 349. The Value Added Tax (Designation of Tax Withholding Agents) Notice, 2018. (Under section 5(2) of the Value Added Tax Act, Cap. 349) IN EXERCISE of the powers conferred upon the Minister responsible for finance by section 5(2) of the Value Added Tax Act, this Notice is issued this 29th day of June, 2018. 1. Title. This Notice may be cited as the Value Added Tax (Designation of Tax Withholding Agents) Notice, 2018. 2. Commencement. This Notice shall come into force on the 1st day of July, 2018. 3. Designation of persons as tax withholding agents. The persons specified in the Schedule to this Notice are designated as value added tax withholding agents for purposes of section 5(2) of the Value Added Tax Act. 1 SCHEDULE LIST OF DESIGNATED TAX WITHOLDING AGENTS Paragraph 3 DS/N TIN TAXPAYER NAME 1 1002736889 A CHANCE FOR CHILDREN 2 1001837868 A GLOBAL HEALTH CARE PUBLIC FOUNDATION 3 1000025632 A.K. OILS AND FATS (U) LIMITED 4 1000024648 A.K. PLASTICS (U) LTD. 5 1000029802 AAR HEALTH SERVICES (U) LIMITED 6 1000025839 ABACUS PARENTERAL DRUGS LIMITED 7 1000024265 ABC CAPITAL BANK LIMITED 8 1008665988 ABIA MEMORIAL TECHNICAL INSTITUTE 9 1002804430 ABIM HOSPITAL 10 1000059344 ABUBAKER TECHNICAL SERVICES AND GENERAL SUPP 11 1000527788 ACTION AFRICA HELP UGANDA 12 1000042267 ACTION AID INTERNATIONAL -

Firms Pool Resources to Insure Oil

28 New Vision, Thursday, July 6, 2017 BUSINESS & TENDERS Firms pool resources to insure oil, gas What are your thoughts on the addition to this, we are regulated How prepared is the insurance current economic downturn independently by the Insurance industry and Gold Star that has left businesses Regulatory Authority, who have insurance in particular, for struggling? continuously found us financially bancassurance? The post 2017 national budget sound and solid with adequate As already mentioned, QA speeches and commentaries have reserves and reinsurance capacity Bancassurance is one of our 2017 made interesting reading. It is good both to carry our current risks strategies. We have already sought The Insurance Regulatory Authority of to know that the finance minister, and also the ability to pay claims pre-qualification and presented Uganda released preliminary results of Matia Kasaija, reassured the nation effortlessly without any concern or to some of the commercial banks the insurance industry earlier this month. that the country is not in recession. difficulty. We can also report that we intend to work with. The Paul Kavuma, the deputy managing The economy is likely to blow hot we continue to maintain our current bancassurance modules can be director at Goldstar Insurance Company, and cold. The economic indicators practising licence for the period 2017 varied and a basic consumer spoke to Business Vision about the such as energy or call it electricity, to ensure continuity of service to our approach will certainly be a perfect performance of the insurance industry can be a formidable economic driver existing and prospective clients. fit under the circumstances and and that of Goldstar for industrialisation. -

Generosity in the Time Ofcovid-19

GENEROSITY IN THE TIME OF COVID-19 Stories of giving in the time of the coronavirus pandemic in Uganda. Period Covered March 31st to April 30th, 2020 #OmutimaOmugabi About CivSource Africa CivSource Africa is a philanthropy support and advisory organization committed to nurturing a more sustainable, effective and connected civil society that advances the dignity and voices of all people. We do this through promoting reflective, responsive, and accountable philanthropic practice. CivSource Africa is also passionate about promoting African philanthropy and telling the stories of African giving and generosity. Plot 18, Balikuddembe Road, Naguru Kampala, Uganda P.O Box 4310 Tel: +256 393 224 056 civsourceafrica.com [email protected] https://www.facebook.com/CivSourceAfrica https://twitter.com/CivsourceAfrica WHERE PHILANTHROPY MEETS CIVIL SOCIETY Table of contents Forward 3 Acknowledegments 4 Acronyms 5 Background 6 Chapter 1 8 Giving by Private Sector Chapter 2 19 Individual Giving Chapter 3 28 Gving by Artists Chapter 4 32 Giving in Collectives Chapter 5 36 A Regional Glance Chapter 6 53 Giving Within Refugee Communities Chapter 7 58 Giving: Perspectives Forward t gives us great pleasure to bring you distribute the items received to the right Ithis first of several reports about giving beneficiaries, as well as accountability during COVID-19 lock down in Uganda. for all that was given. In fact, this report Right from the announcement of the first just shares what was given, and we hope lock down on 31st March 2020, we started it can be used as a basis to demand noticing reports of giving and we decided accountability for where and how and by that we needed to capture this momentous whom the resources were used. -

Uganda Section 2020

PRESIDENT OF UGANDA UGANDA UGANDA SECTION 2020 EDITION PRESIDENT OF THE REPUBLIC OF UGANDA H.E. YOWERI KAGUTA MUSEVENI East African Manufacturers & Investors Directory East African Manufacturers & Investors Directory 129 UGANDA PROFILE UGANDA UGANDA Uganda Profile ganda officially the Republic of Uganda, is a landlocked country in East Africa. Uganda is bordered to the east by Kenya, to the north by South Sudan, to the west by the Democratic Republic of the Congo, to the southwest Uby Rwanda, and to the south by Tanzania. Uganda is the world’s second most populous landlocked country after Ethiopia. The southern part of the country includes a substantial portion of Lake Victoria, shared with Kenya and Tanzania. Uganda is in the African Great Lakes region. Uganda also lies within the Nile basin, and has a varied but generally a modified equatorial type of climate. Uganda takes its name from the Buganda kingdom, which encompasses a large portion of the south of the country, including the capital Kampala. The people of Uganda were hunter-gatherers until 1,700 to 2,300 years ago, when Bantu- speaking populations migrated to the southern parts of the country. Environment and conservation The Crested crane is the national bird. Conservation in Uganda Uganda has 60 protected areas, including ten national parks: Bwindi Impenetrable National Park and Rwenzori Mountains National Park (both UNESCO World Heritage Sites[43]), Kibale National Park, Kidepo Valley National Park, Lake Mburo National Park, Mgahinga Gorilla National Park, Mount Elgon National Park, Murchison Falls National Park, Queen Elizabeth National Park, and Semuliki National Park. Economy and infrastructure The Bank of Uganda is the central bank of Uganda and handles monetary policy along with the printing of the Ugandan shilling. -

Uganda Golden Jubilee - Toronto 1 INDEX

2012 Uganda Golden Jubilee - Toronto 1 INDEX PAGE 2 Anthem’s of Canada and Uganda 3 Chairman’s Welcome 4 Editor’s Message 5 Message from the Premier of Ontario 6 Message from His Excellency the High Commissioner of Uganda 7 Message from Honorary Consul of Uganda in Toronto 8 Message from Ontario Minister of Government Services 9 Greetings From Dr. Sudhir Ruparelia 10 Uganda50Toronto Committee 15 Uganda Independence Celebration Committee makes the news 16 Greeting From Mayur Madhvani 17 Kiprotich wins Olympic gold for Uganda 18 A Chronology Of Key Events In Uganda’s History 21 Celebrating Ugandans who have excelled in Canada 37 A Brief Biography Of The Late Hamu Mukasa 38 Professor George Wilberforce Kakoma – The Creator Of Uganda’s Anthem 38 Pioneers 39 The Origin Of The Gomesi / Busuuti 41 Remembering The Expulsion Of Asians In 1972 42 The History Of The Uganda Martyrs Church Of Canada 44 Celebrating Uganda’s Authors 57 Presidential Initiative On Sustainable Tourism (PRESTO) Background 59 Indian Association Uganda 60 Events to Celebrate Uganda’s Golden Jubilee 2 2012 Uganda Golden Jubilee - Toronto NATIONAL ANTHEM OF CANADA NATIONAL ANTHEM OF UGANDA O Canada! Oh Uganda! may God uphold thee, Our home and native land! We lay our future in thy hand. True patriot love in all thy sons command. United, free, With glowing hearts we see thee rise, For liberty The True North strong and free! Together we'll always stand. From far and wide, O Canada, we stand on guard for thee. Oh Uganda! the land of freedom. God keep our land glorious and free! Our love and labour we give, O Canada, we stand on guard for thee.