The World Leader in Art Market Information

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RECENT ACQUISITIONS Dear Friends and Collectors

WALLY FINDLAY GALLERIES RECENT ACQUISITIONS Dear Friends and Collectors, Wally Findlay Galleries is pleased to present our most recent e-catalogue, Recent Acquisitions, featuring the newest additions to our collection. The catalogue features works by Aizpiri, Berthelsen, Brasilier, Cahoon, Calder, Cassignieul, Chagall, D’Espagnat, Jean Dufy, Gen Paul, Hambourg, Hervé, Indiana, Kluge, Leger, Le Pho, Miró, Outin, Sébire, Sipp-Green, Simbari, Simkohvitch, and Vu Cao Dam. For further information in regards to these works and the current collection, please contact the New York gallery. We look forward to hearing from you. WALLY FINDLAY GALLERIES 124 East 57th Street, New York, NY (212) 421 5390 [email protected] Aïzpiri Paul Aïzpiri (b. 1919) was born in Paris on May 14, 1919. Aïzpiri entered l’École Bulle to learn antique restoration, after his father insisted that he first learn a trade as a means of assuring his livelihood. After the course he entered the Beaux-Arts to study painting. Aïzpiri was certainly encouraged as a young painter in his early 20’s, during somber war-torn France, exhibiting amongst the painters of l’École Pont-Aven and the Nabis. He became a member of the Salon d’Automne in 1945, won Third Prize at the Salon de Moins de Trente Ans, of which he was a founding member and later showed at the Salon “Les Peintres Témoin de leur Temps”. In 1948, Aïzpiri won the Prix Corsica which allowed him to go to Marseilles. His stay there so impressed him, that he declared it was a turning point of his art. Not only did he find a whole new world to paint which was far different subjectively from any life he had known in Paris, but also a new world of color. -

Albert Marquet and the Fauve Movement, 1898-1908

Digitized by the Internet Archive in 2010 with funding from Lyrasis IVIembers and Sloan Foundation http://www.archive.org/details/albertmarquetfauOOjudd ALBERT MARQUET AND THE FAirVE MOVEMENT 1898 -1908 by Norrls Judd A thesis submitted to the Faculty of the Department of Art History in partial fulfillment of the requirements for Senior Honors in Art History. ^5ay 1, 1976 /JP 1^1 Iff TABLE OF CONTENTS Page Introduction ...............< 1 I The Fauve Movement Definition of Fauvism, • 3 The Origins of the Fauve Movement 5 The Leaders of the Fauve Group 11 1905: The Crucial Year, Salon Exhibitions and Critical Reactions 26 Fauve Paintings of 1905 34 Critical Reaction to Fauvism.. 41 Denouement 45 II Albert Marquet Bordeaux: Origins 49 Paris: 1890 - 1898 50 Years of Activity with the Fauve Group: 1899-1908 Marquet and Matisse, 1898 - 1905 54 Marquet and Dufy, 1906. 78 Marquet, 1907-1908 83 Marquet: 1903-1910 87 III Summary 89 IV Footnotes 93 V Appendix Marquet Speaks on His Art 116 List of Reproductions 117 Photocopies of Selected Reproductions i 123 VI Bibl iography 142 Note: An asterisk will appear by a plate reference if the reproduction also appears in photocopy in the appendix. il ALBERT MARQUET AND THE FAUVE MOVEMENT 1898 - 1908 INTRODUCTION In 1905, when a group of violently coloured paintings was displayed at the Salon d'Automne, there were varying reactions from the critics. Some were outraged, others merely amused. At that time only a few of the critics were aware of the importance of the event. Even fewer critics realized that the special characteristics of these paintings would have a decisive influence on the future development of Gortain futur e twentieth century art. -

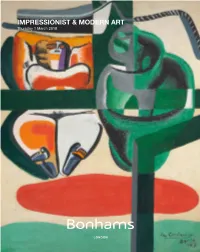

Impressionist & Modern

IMPRESSIONIST & MODERN ART Thursday 1 March 2018 IMPRESSIONIST & MODERN ART Thursday 1 March 2018 at 5pm New Bond Street, London VIEWING ENQUIRIES Brussels Rome Thursday 22 February, 9am to 5pm London Christine de Schaetzen Emma Dalla Libera Friday 23 February, 9am to 5pm India Phillips +32 2736 5076 +39 06 485 900 Saturday 24 February, 11am to 4pm Head of Department [email protected] [email protected] Sunday 25 February, 11am to 4pm +44 (0) 20 7468 8328 Monday 26 February, 9am to 5pm [email protected] Cologne Tokyo Tuesday 27 February, 9am to 3pm Katharina Schmid Ryo Wakabayashi Wednesday 28 February 9am to 5pm Hannah Foster +49 221 2779 9650 +81 3 5532 8636 Thursday 1 March, 9am to 2pm Department Director [email protected] [email protected] +44 (0) 20 7468 5814 SALE NUMBER [email protected] Geneva Zurich 24743 Victoria Rey-de-Rudder Andrea Bodmer Ruth Woodbridge +41 22 300 3160 +41 (0) 44 281 95 35 CATALOGUE Specialist [email protected] [email protected] £22.00 +44 (0) 20 7468 5816 [email protected] Livie Gallone Moeller PHYSICAL CONDITION OF LOTS ILLUSTRATIONS +41 22 300 3160 IN THIS AUCTION Front cover: Lot 16 Aimée Honig [email protected] Inside front covers: Lots 20, Junior Cataloguer PLEASE NOTE THAT THERE IS NO 21, 15, 70, 68, 9 +44 (0) 20 7468 8276 Hong Kong REFERENCE IN THIS CATALOGUE Back cover: Lot 33 [email protected] Dorothy Lin TO THE PHYSICAL CONDITION OF +1 323 436 5430 ANY LOT. -

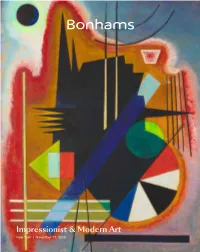

Impressionist & Modern

Impressionist & Modern Art New York | November 17, 2020 Impressionist & Modern Art New York | Tuesday November 17, 2020 at 5pm EST BONHAMS INQUIRIES BIDS COVID-19 SAFETY STANDARDS 580 Madison Avenue New York Register to bid online by visiting Bonhams’ galleries are currently New York, New York 10022 Molly Ott Ambler www.bonhams.com/26154 subject to government restrictions bonhams.com +1 (917) 206 1636 and arrangements may be subject Bonded pursuant to California [email protected] Alternatively, contact our Client to change. Civil Code Sec. 1812.600; Services department at: Bond No. 57BSBGL0808 Preeya Franklin [email protected] Preview: Lots will be made +1 (917) 206 1617 +1 (212) 644 9001 available for in-person viewing by appointment only. Please [email protected] SALE NUMBER: contact the specialist department IMPORTANT NOTICES 26154 Emily Wilson on impressionist.us@bonhams. Please note that all customers, Lots 1 - 48 +1 (917) 683 9699 com +1 917-206-1696 to arrange irrespective of any previous activity an appointment before visiting [email protected] with Bonhams, are required to have AUCTIONEER our galleries. proof of identity when submitting Ralph Taylor - 2063659-DCA Olivia Grabowsky In accordance with Covid-19 bids. Failure to do this may result in +1 (917) 717 2752 guidelines, it is mandatory that Bonhams & Butterfields your bid not being processed. you wear a face mask and Auctioneers Corp. [email protected] For absentee and telephone bids observe social distancing at all 2077070-DCA times. Additional lot information Los Angeles we require a completed Bidder Registration Form in advance of the and photographs are available Kathy Wong CATALOG: $35 sale. -

Émilie Charmy Biographie

EMILIE CHARMY (1878-1974) BIOGRAPHIE Extract from a text by Sandra Martin “Émilie Charmy (1878-1974) : une destinée de peintre, catalogue d’exposition, Villefranche-sur Saône, musée Paul-Dini, musée municipal, 12 octobre 2008-15 février 2009, éd. musée Paul-Dini, 2008 ». 1878 : Le 2 avril, naissance à Saint-Étienne d’Émilie Espérance Barret. Elle prit plus tard le nom de Charmy, comme nom de peintre. 1884 : Fondation de La Société des artistes indépendants présidée par Paul Signac. Émilie est pensionnaire à Saint-Priest en Jarez. 1895 : Première peinture aboutie représentant une usine familiale, à La Bérardière, à Saint- Étienne. Suivront d’autres œuvres, portraits et scènes d’intérieur. Jean l’incite à poursuivre. 1896 : Décès de son père le 24 avril. 1898 : Devant le talent précoce de sa sœur, et le peu d’avenir possible pour eux à Saint- Étienne, Jean, qui est devenu le tuteur de Charmy, vend des concessions minières familiales et quitte Saint-Étienne définitivement avec Émilie. Ils s’installent à Lyon (rue Jarente). Elle rencontre Jacques Martin, chimiste et peintre de Fleurs, qui devient son père spirituel. On lui doit deux portraits d’Emilie Charmy dont un est exposé en 1901 au Salon de Lyon sous le nom de Portrait de Mademoiselle E. B. (n° 373). 1900 : Émilie se rend à Paris. Elle est frappée par les œuvres d’Édouard Manet lors de l’Exposition Universelle. 1901 : 1er décembre, exposition inaugurale de la galerie Berthe Weill, 25, rue Victor- Massé ; le catalogue est préfacé par Gustave Coquiot. 1902 : Charmy occupe un atelier rue Dunoir, sur la rive gauche du Rhône. -

December 2010

Transparency for the Global Art Market Since 2004 www.skatepress.com ! ! 575 Broadway, 5th Floor, New York, NY 10012 USA /phone: +1.212.514.6010 /fax: +1.212.514.6037 Skate’s Art Investment Review Monthly Art Investment Ideas from Skate’s Art Market Research December 2010 In This Issue: 1. IntroducOon 2 2. November Sales Prove Strong Art Market Recovery 2 3. Skate’s Top 5000/Top 1000 StasOcal Overview 3 4. November 2010 AucOon Results 4 5. Major Changes in the Ranking of Skate’s Top ArOsts 5 6. Top 20 New Entrants* to Skate’s Top 5000 6 7. December 2010 Sales: Paris in Decline, A Few OpportuniOes 6 8. Skate’s Top 5000 by Period (ERR performance), as of 1-Dec-2010 7 9. Blue Chip ArOsts With the Highest Growth Rate in Skate’s Top 5000 7 10.Top 5 Art Investment Ideas for December 2010 8 Jean-Michel Basquiat 8 Kees van Dongen 12 Fernand Léger 14 11.Other Artworks to Watch in December 2010 16 ChrisOe’s AucOons 16 Sotheby’s AucOons 17 12.Skate’s Art Stocks 18 Copyright © 2010 Skate’s, LLC—All rights reserved Introduc@on please order Skate’s Artwork Background Report by calling +1.212.514.6010) Welcome to the December issue of Skate’s Art • Favorable price and liquidity trends in the market Investment Review. As always, our coverage is focused today, including a steady demand for the arOst’s on the universe of global arOsts (currently 631 arOsts) works over the last 24 months who are represented in Skate’s Top 5000 database of • A track record of posiOve investment returns the world’s most valuable art according to aucOon based on repeat sales of the arOst’s higher value prices. -

Twentieth Century Masters

TWENTIETH CENTURY MASTERS FINDLAY GALLERIES Gallery Collection on View Balthus (1908 - 2001) Braque (1882 - 1963) Camoin (1879 - 1965) Chagall (1887 - 1985) D'Espagnat (1870 - 1950) Degas (1834 - 1917) Friesz (1879 - 1949) Glackens (1870 - 1938) TWENTIETH Hassam (1859 - 1935) CENTURY Homer (1836 - 1910) Lachaise (1882 - 1935) Laurencin (1883 - 1956) Le Sidaner (1862 - 1939) Lebasque (1865 - 1937) Lebourg (1849 - 1928) Luce (1858 - 1941) Martin- Ferrieres (1893 - 1972) Matisse (1869 - 1954) Metzinger (1883 - 1956) Pissarro- (1830 - 1903) Prendergast (1858 - 1924) Renoir (1841 - 1919) Valtat (1869 - 1952) Van Dongen (1877 - 1968) Vlaminck (1876 - 1958) Vuillard (1868 - 1940) KEES VAN DONGEN (1877 - 1968) Portrait de jeune femme au petit chien, c. 1920 oil on canvas 59 x 59 inches Signed 'van Dongen' (middle right) 137616 3 // FINDLAY TWENTIETH CENTURY MASTERS Findlay Galleries continues its long tradition of presenting highly important paintings to fine art collectors throughout the world. The Masters' Collection offers a cross-section of highlights from our collection including recent acquisitions of Impressionist and Modern Masters. The Galleries' global position in the art market for nearly 148 years has distinguished it as a leader in providing unique opportunities for collectors. Many of the paintings in this exhibition have appeared in museums around the globe and in distinguished collectors' homes. Several of these works have been privately collected and quietly passed down from generation through generation. As always, our art consultants offer unparalleled excellence in assisting our clients as they enhance or begin their collections. As a dealer to individuals, institutions and corporate collectors alike, Findlay Galleries continues to celebrate its traditions of presenting exhibitions featuring collections of diverse, original, and outstanding works. -

Le Fauvisme Été À Collioure, Hors Série Découverte Gallimard, 2005 • S

19/09/13 Bibliographie • S. Fauchereau, Avant-gardes du XXe siècle arts et littérature 1905-1930 Flammarion 2010. • E Lucie-Smith Les arts au XXe siècle Köneman, 1996 • • J. Matamoros et D. Szymusiak, Matisse Derain, 1905, un Le Fauvisme été à Collioure, hors série découverte Gallimard, 2005 • S. Whitfield Le fauvisme, Thames & Hudson, paris, 1997 Ou la couleur libérée • Les fauves ou la couleur libérée, Actualités de arts plastiques, n° 92, Paris, 1995 Catalogue d’exposition: • Le fauvisme ou l’épreuve du feu, Eruption de la modernité en Europe, Ed des Musées de la Ville de 1 Paris, 1999 2 3 Matisse, 1897, 1908 La Desserte, 1897 huile sur toile La Desserte, Harmonie rouge 100 x 131 cm coll. Part. 1908 huile sur toile 181 x 221 cm Musée de l’Hermitage 4 5 6 1 19/09/13 Juillet 1881Liberté de la presse. 1881 Vote des lois Jules Ferry: l'école devient gratuite (1881), l'éducation obligatoire et l'enseignement public laïc (1882). 21 mars 1884 Légalisation des syndicats. 1900:Exposition universelle 1894 - 1906 Affaire Dreyfus : Dreyfus accusé d'espionnage est condamné avant d'être gracié par le La France est un des plus grands président de la République. empires coloniaux 1er juillet 1901 Légalisation des associations. 1905 séparation des Églises et de l'État. [email protected] 7 [email protected] 8 Photographies de Baudelaire, par Nadar et Carjat Exposition universelle de 1889 . Galerie des machines 9 10 « Arrivée du train en gare de la Ciotat, » vue des frères Lumière 11 12 2 19/09/13 14 13 15 16 Dans la salle VII, des œuvres de Henri Matisse, de André Derain, De Maurice de Vlaminck, Charles Camoin, Albert Marquet, Henri Manguin, 17 Salon d’automne, 1905 Matisse, la femme au chapeau Huile sur toile 80.6 x 59.7cm San Francisco Museum of modern art 18 DERAIN 3 19/09/13 19 Le douanier Rousseau: le lion, ayant faim, se jette sur l’antilope 1898-1905 20 M. -

Introduction Picasso De L’Autre Côté Du Rideau De Fer

introduction Picasso de l’autre côté du rideau de fer Jérôme Bazin • colloque Revoir Picasso • 26 mars 2015 1. – L’histoire de Picasso dans les pays communistes d’Europe À l’autre extrémité du monde artistique, chez ceux qui de l’Est est à la fois pauvre et riche. Si l’on part en quête des explorent des formes d’art qui ne sont pas le réalisme œuvres de l’artiste dans cette partie du monde, la recherche socialiste, qui renouent avec les avant-gardes classiques ou est décevante. Peu de tableaux y sont présents ; pour en trou- participent aux néo-avant-gardes, Picasso est également ver, il faut aller dans les salons de quelques collectionneurs ou une référence incontournable, membre du panthéon des dans les réserves de très rares musées où certains administra- libérateurs de l’art. Et comme l’a montré Piotr Piotrowski teurs sont parvenus à faire acheter de modestes images (tels dans son livre In the Shadow of Yalta (2009), les néoavant- les dessins et lithographies que Werner Schmidt fait ache- gardes dans les démocraties populaires ne se construisent ter pour le Cabinet des estampes de Dresde). De même, les pas contre les avant-gardes classiques, mais plutôt en conti- tableaux vont rarement à l’Est, à part, exception notable, lors nuité avec elles, à l’inverse de ce qui se passe dans le monde de la polémique exposition à Moscou et Leningrad en 1956. capitaliste ; elles n’avaient donc aucun mal à intégrer Picasso Mais si l’on cherche à mesurer la diffusion, la connaissance, la dans un récit de la modernité et de la postmodernité, qui ici fréquence des allusions à Picasso, en un mot son inscription ne faisait qu’un. -

Chapter 5 - 1907-1914

Chapter 5 - 1907-1914 And so life in Paris began and as all roads lead to Paris, all of us are now there, and I can begin to tell what happened when I was of it. When I first came to Paris a friend and myself stayed in a little hotel in the boulevard Saint-Michel, then we took a small apartment in the rue Notre-Dame-des-Champs and then my friend went back to California and I joined Gertrude Stein in the rue de Fleurus. I had been at the rue de Fleurus every Saturday evening and I was there a great deal beside. I helped Gertrude Stein with the proofs of Three Lives and then I began to typewrite The Making of Americans. The little badly made French portable was not strong enough to type this big book and so we bought a large and imposing Smith Premier which at first looked very much out of place in the atelier but soon we were all used to it and it remained until I had an American portable, in short until after the war. As I said Fernande was the first wife of a genius I was to sit with. The geniuses came and talked to Gertrude Stein and the wives sat with me. How they unroll, an endless vista through the years. I began with Fernande and then there were Madame Matisse and Marcelle Braque and Josette Gris and Eva Picasso and Bridget Gibb and Marjory Gibb and Hadley Hemingway and Pauline Hemingway and Mrs. Sherwood Anderson and Mrs. -

Blanchet 18102013 Bd.Pdf

2, boulevard Montmartre - 75009 PARIS Tél. : (33)1 53 34 14 44 - Fax : (33)1 53 34 00 50 [email protected] www.blanchet-associes.com Société de ventes volontaires Agrément N°2002-212 BLANCHET ASSOCIÉS & • 18 OCTOBRE 2013 DROUOT-RICHELIEU - Salle 7 9, rue Drouot - 75009 Paris - Tél. : (33)1 48 00 20 20 - Fax : (33)1 48 00 20 33 VENDREDI 18 OCTOBRE 2013 - 14 H 30 Après succession Collection du Dr et Mme Philippe Marette IMPORTANTS TABLEAUX & SCULPTURES XIXe & XXe Première vente EXPOSITIONS PUBLIQUES À DROUOT-RICHELIEU - Salle 7 Jeudi 17 octobre 2013 l 11 h 00 à 18 h 00 Vendredi 18 octobre 2013 l 11 h 00 à 12 h 00 Téléphone pendant l’exposition et la vente : 01 48 00 20 07 Catalogue en ligne : www.blanchet-associes.com - www.gazette-drouot.com PIERRE BLANCHET & PATRICK DAYEN - COMMISSAIRES-PRISEURS ASSOCIÉS FRANCE LENAIN - DIRECTEUR ASSOCIÉ 2, boulevard Montmartre - 75009 PARIS Tél. : (33)1 53 34 14 44 - Fax : (33)1 53 34 00 50 www.blanchet-associes.com [email protected] Société de ventes volontaires Agrément N°2002-212 En couverture lot n° 52 (détail) Le Docteur et Mme Philippe Marette dans leur salon devant les Forain. Le Docteur Philippe Marette, médecin, psychiatre reconnu, frêre de Françoise Dolto, commença sa « carrière de collectionneur » vers 1932. Durant l’occupation, entre deux visites médicales à l’hôpital Bichat, il ouvrit une boutique d’antiquaire. Après 1946, son métier de médecin l’absorbant énormément, il dut quitter avec beaucoup de regrets son activité d’antiquaire, mais sans pour autant perdre son flair de collectionneur. -

Timeline Fauvism Henri Matisse Matisse and Picasso

Henri Matisse a biography Timeline Henri-Emile-Benoît Matisse was born in a small town in northern North Africa to explore ornamental arabesques and flat patterns of color. From roughly 1913 to 1917 he France on December 31, 1869. His mother introduced him to experimented with and reacted against Cubism, the leading avant-garde movement in France at the time. painting at age 21 by bringing art supplies to his bedside while he During his early stay in Nice, France, from about 1917 to 1930, his subjects largely focused on the female 1869 Henri Matisse is born on recovered from appendicitis. He promptly gave up pursuing a law figure and his works were infused with bright colors, southern light, and decorative patterns. 1870 December 31 in Le Cateau, France career and moved to Paris to study traditional nineteenth-century In 1930, Matisse traveled to the United States and received a mural commission from Dr. Albert academic painting. He enrolled at the Académie Julian as a student Barnes, the art-collector who established the Barnes Foundation in Pennsylvania. Destined for the main hall of artist William-Adolphe Bouguereau (1825–1905), but struggled of the Foundation and installed in 1933, Matisse’s masterpiece The Dance II is renowned for its simplicity, under the conservative teacher. Matisse continued his studies with flatness, and use of color. In preparation for the mural, he began using the technique of composing with cut- Gustave Moreau (1826–1898) in 1892, a Symbolist painter at the out pieces of colored paper, which soon became his preferred exploratory method.