Government Assistance to the Financial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SC13-2384 Exhibit D (Lavalle)

EXHIBIT D REPORT ON NYE LAVALLE’S INVESTIGATIONS, RESEARCH BACKGROUND, BONA FIDES, EXPERTISE, & EXPERIENCE IN PREDATORY MORTGAGE SECURITIZATION, SERVICING, FORECLOSURE & ROBO-SIGNING PRACTICES INTRODUCTION 1. My name is Aneurin Adlai Lavalle. I am most commonly referred to as Nye Lavalle. I am a resident of the State of Florida. 2. I provide this report based upon facts and information personally known by me and to me and gathered from my research and investigation over a period of more than twenty-years. 3. I have a research background and as a consumer and shareholder advocate, I have developed a series of skills, procedures, and protocols over 20-years that has led me to be an expert in predatory mortgage securitization, servicing, and foreclosure fraud issues with a specialty in robo-signing.1 4. I have been accepted by Courts as an expert in matters relating to predatory mortgage securitization, servicing, and foreclosure fraud issues. 5. My findings, analyses, opinions, and many of my protocols, opinions, and conclusions have been reviewed, corroborated, and adopted by state and Federal regulatory agencies such as the Federal Reserve, Office of Comptroller of the Currency; Federal Deposit Insurance Corporation, Federal Housing Financing Agency, U.S. Attorney General and Attorneys General from all 50 states, FILED, 02/04/2015 12:11 am, JOHN A. TOMASINO, CLERK, SUPREME COURT including Florida, but especially by those in New York, Delaware, Nevada, and California. 1 http://en.wikipedia.org/wiki/Nye_Lavalle 1 6. In addition, numerous state and federal courts, including the Supreme and highest courts of the states of Massachusetts,2 Maryland,3 and Kansas4 have agreed with some of my opinions, findings, conclusions, and analyses I have developed over the last twenty-years. -

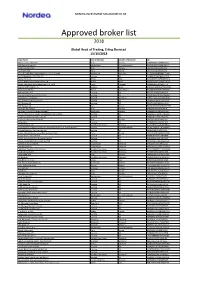

External Borkers List

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2018 Global Head of Trading, Erling Skorstad 15/10/2018 Legal Name City of Domicile Country of Domicile LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABN Amro Group NV Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BCS Prime Brokerage Limited London UK 213800UU8AHE2B6QUI26 BGC Brokers LP London UK ZWNFQ48RUL8VJZ2AIC12 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Carnegie AS Norway Oslo Norway 5967007LIEEXZX57BC18 Carnegie Investment Bank AB (publ) Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities AS Oslo Norway 5967007LIEEXZXA40G44 CLSA (UK) London UK 213800VZMAGVIU2IJA72 Commerzbank AG Frankfurt -

Housing and the Financial Crisis

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Housing and the Financial Crisis Volume Author/Editor: Edward L. Glaeser and Todd Sinai, editors Volume Publisher: University of Chicago Press Volume ISBN: 978-0-226-03058-6 Volume URL: http://www.nber.org/books/glae11-1 Conference Date: November 17-18, 2011 Publication Date: August 2013 Chapter Title: The Future of the Government-Sponsored Enterprises: The Role for Government in the U.S. Mortgage Market Chapter Author(s): Dwight Jaffee, John M. Quigley Chapter URL: http://www.nber.org/chapters/c12625 Chapter pages in book: (p. 361 - 417) 8 The Future of the Government- Sponsored Enterprises The Role for Government in the US Mortgage Market Dwight Jaffee and John M. Quigley 8.1 Introduction The two large government- sponsored housing enterprises (GSEs),1 the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”), evolved over three- quarters of a century from a single small government agency, to a large and powerful duopoly, and ultimately to insolvent institutions protected from bankruptcy only by the full faith and credit of the US government. From the beginning of 2008 to the end of 2011, the two GSEs lost capital of $266 billion, requiring draws of $188 billion under the Treasured Preferred Stock Purchase Agreements to remain in operation; see Federal Housing Finance Agency (2011). This downfall of the two GSEs was primarily a question of “when,” not “if,” given that their structure as a public/private Dwight Jaffee is the Willis Booth Professor of Banking, Finance, and Real Estate at the University of California, Berkeley. -

Primers Federal Home Loan Banks Feb. 8, 2021

The NAIC’s Capital Markets Bureau monitors developments in the capital markets globally and analyzes their potential impact on the investment portfolios of U.S. insurance companies. Please see the Capital Markets Bureau website at INDEX. Federal Home Loan Banks Analyst: Jennifer Johnson Executive Summary • The Federal Home Loan Bank (FHLB) system was established in 1932 for the purpose of providing liquidity and transparency to the capital markets. • It is comprised of 11 regional banks that are government-sponsored entities (GSEs) and support the market for homes. These FHLB regional banks provide low-cost financing to member financial institutions, which in turn make loans to individuals. • Each FHLB regional bank is structured as a cooperative of mortgage lenders, or members, which sets its credit standards and lending policies. To become a member, a financial institution must purchase shares of the regional bank. • FHLB regional bank members may apply for a loan or “advance” based on required credit limits and borrowing capacity. Each loan or advance is secured by eligible collateral, and lending capacity is based on applicable discount rates on the eligible collateral. The more liquid and easily valued the collateral, the lower the discount rate. • Eligible collateral may include U.S. government or government agency securities; residential mortgage loans; residential mortgage-backed securities (RMBS); multifamily mortgage loans; cash; deposits in an FHLB regional bank; and other real estate-related assets such as commercial What is thereal FHLB estate? loans. • U.S. insurers interact with the FHLB system via borrowing, investing in FHLB debt and owning stock in FHLB regional banks. -

Switzerland in the Second World War

To Our American Friends: Switzerland in the Second World War By Dr. Hans J. Halbheer, CBE Honorary Secretary of the American Swiss Foundation Advisory Council in Switzerland and a Visiting Scholar at the Hoover Institution, Stanford University, California Dr. Halbheer wrote the following essay in 1999 to offer a Swiss perspective on some issues of the recent controversy to American friends of Switzerland. In addressing the arguments raised by U.S. critics of the role of Switzerland during the Second World War, I am motivated both by my feelings of friendship towards America and by my Swiss patriotism. For both of these reasons, I feel deeply hurt by both the charges against my country and the vehemence with which they have been expressed. During a recent period of residency at the Hoover Institution at Stanford University, one of the leading U.S. think tanks, I sought to present my personal standpoint regarding the lack of understanding about Switzerland’s role during the Second World War in many discussions with Americans both young and old. On these occasions, I emphasized my awareness of the fact that the criticisms of Switzerland came only from a small number of Americans. Despite the settlement reached in August 1998 between the two major Swiss banks (Credit Suisse Group and UBS) and two Jewish organizations (the World Jewish Congress and the World Jewish Restitution Organization), the matter has still not run its course, although it has widely disappeared from the American media. Unfortunately, I must maintain that as a result of the generally negative portrayal of Switzerland over the past few years, the image of Switzerland has suffered. -

Fiscal Conservatism and Autonomy Without Much Coordination

Nils Soguel The Swiss cantons: Fiscal conservatism and autonomy without much coordination Working paper de l’IDHEAP 13/2014 Unité de recherche en finances publiques Nils Soguel The Swiss cantons: Fiscal conservatism and autonomy without much coordination Working paper de l’IDHEAP 13/2014 Unité de recherche en finances publiques The Swiss cantons: Fiscal conservatism and autonomy without much coordination Nils Soguel* Institut de hautes études en administration publique-IDHEAP, University of Lausanne, Switzerland May, 2014 Abstract This paper presents the way the Swiss cantons were impacted by the 2008 financial crisis and its aftermaths, and the way they reacted. The Federal Constitution of the Swiss Confederation provides that “the Confederation [central government], the Cantons [sub-central governments] and the Communes [local governments] shall take account of the economic situation in their revenue and expenditure policies (Art.100, al.4)”. Simultaneously, it stipulates that “Cantons are sovereign except to the extent that “their sovereignty is limited by the Federal Constitution” (Art.3). Thus the cantons benefit from far-reaching political, financial and fiscal autonomy. In the past and despite the provision of Art.100, most of them have made use of this autonomy to engage in pro- cyclical fiscal policies. The pro-cyclical behaviour stems from a culture of rather conservative fiscal policy. This culture has indeed been transposed by individual cantons into their own legislation governing their public finance. Most have chosen to legally cap the deficit or even ban that possibility—often referred to as budget constraints—regardless the macroeconomic conditions. This particular institutional setting points towards the difficulty to conduct a consistent macroeconomic policy not only between the different tiers of government, but also between the fiscal and the monetary policies. -

Folder 29 Switzerland

TREASURY DEPARTMENT INTER OFFICE COMMUNICATION DATE TO Miss Hodel March 14, 1944 FROM R. B. Parke ~ubject: Recipien~s in Switz/rland of fu~ds remitted by relief organizations for reliif and evacuation operations in enemw and enemw-occupied territory. / In accordance with your request there are listed below the names and addresses of individuals to whom remittances are made by,relief organizations in this country for relief and evacuation operations in enero.y and enemw-occupied territory: . Address Organization Represented Dr. A. Freudenberg, 41 Avenue de Champel,Geneva, American Committee for Switzerland. · Christian Refugees, Inc. Rene Berthelet, 14 Waserstrasse, Zurich, ~ternational Rescue and Switzerland. Relief Committee. Noel Field, '- ,_ 12 Rue du Vieux College, Unitarian Service Committee. ····Geneva, Switzerland, Saly :Mayer, St. Gallen, Switzerland. J.D.C. Dr. Riegner, , Geneva, Switzerland•. · Vlorld Jewish Congress. Isaac Sternbuch, St. Gallen, Switzerland. Union of Orthodox Rabbis. Dr. B. Tchlenov International Red Cross, Gmeva Jewish Labof Coin.'irl.ttee and/or Dr. L •. Hersh, Professor at the Universi;ty ···- · · ·.· of Geneva. · - - In addition to the foregoing, the Intern~tional.Red Cross, Geneva, Switz~land, was the recipient of the sum of $100,000 from the JDC for the purchase of food and other suppli~ for distribution in Rumania, Croatia, Hungary and· Czechoslovalda. The Greek Legation, Bern, Switzerland;, \Vas ayo the recipient .. of a relat:i._vely small runount, 20,000 t1\v:i,_ss fr_51nc:3Jor the re:LJ._e_!'__E_f ~Cl_rE3ek~pationals >~ held as hostages in Northern Italy. The International Red Cross, Geneva, Switzer land, vms also the pa;yee designc>.ted in a license issti~d to the International Rescue and Relief Conunittee per1nitting it to remit $7,500 monthly for a period of six months for the relief of Spanish refugees_in camps .inSouth Frli.hceo · · r~_-·o_-./-_ ~- R. -

5–7 8–11 12–17 Leading Through Chairman’S Message Group CEO’S Message

B 5–7 8–11 12–17 Leading Through Chairman’s Message Group CEO’s Message 18–21 22–23 26–29 Group CFO’s Message Financial Highlights Economic Overview 32–37 40–47 50–55 Board Roundtable Strategy Management’s Discussion & Analysis 58–69 72–79 80–81 Business Review Sustainability Awards & Recognition 84–89 90–93 94–109 Board of Directors Profiles Executive Management Corporate Governance Profiles Report 110–116 117–192 Risk Management Consolidated Financial Statements His Highness Sheikh Khalifa bin Zayed Al Nahyan President of the United Arab Emirates and Ruler of Abu Dhabi Supreme Commander of the UAE Armed Forces 2 His Highness Sheikh Mohammed bin Zayed Al Nahyan Crown Prince of Abu Dhabi Deputy Supreme Commander of the UAE Armed Forces Chairman of the Abu Dhabi Executive Council 3 Ambition and discipline propel us forward, as a leader, as we work to create the most valuable bank in the UAE. ADCB’s success is built on sheet, and now, even as the delivering extraordinary service to regional and global economy has our customers and communities. become more challenging, growth Offering a better way to bank, we continues. have carved out a leading role in The qualities that give rise to the banking sector and this region enduring success become all through a clear, focused strategy the more apparent when times and its disciplined execution. This get tough. And they continue to led to a series of record-breaking differentiate ADCB as the bank you years and a very strong balance can count on, going forward. -

Financial Crises and Policy Responses

Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE © 2016 by the American Enterprise Institute. All rights reserved. The American Enterprise Institute (AEI) is a nonpartisan, nonprofit, 501(c)(3) educational organization and does not take institutional posi- tions on any issues. The views expressed here are those of the author(s). Table of Contents Preface ................................................................................................................................................................................... v I. Financial Crises and Challenges: The Origins of the Shadow Financial Regulatory Committee ..... 1 II. A Brief 30-Year History of Finance ..................................................................................................................... 5 III. The S&L Crises of the 1980s ................................................................................................................................. 7 IV. The Banking Crises of the 1980s and Policy Responses .............................................................................. 11 V. Deposit Insurance and Safety-Net Reform .................................................................................................... 17 VI. Banking Regulation -

PO Box: 120728, Al Kifaf Commercial Building, Opposite to Burjuman Center, Bur Dubai, UAE

PO Box: 120728, Al Kifaf Commercial Building, Opposite to Burjuman Center, Bur Dubai, UAE. Dear Member As you are aware that Outbreak of COVID19 (Novel Coronavirus) is underway which is gravest challenge faced by us into this new millennia. This is testing time for all of us & UAE government is trying hard to contain this deadly disease. The drive of UAE government of sterilization program is especially commendable with mass disinfection taking place around each corner. This has pushed ourselves into a situation where all are confined into our Homes or has access for limited mobility. Although the measures by UAE authorities are strict but we should all welcome such measures in one voice as they shall keep all of us safe from this virus infection. Inayah TPA a fully owned subsidiary of National Life & General Insurance Company SAOG being serious player in partnering healthcare sector has understood its responsibility and we are fully functional 24 X 7 for providing services to our members into these dire times. We understand that at this time any step outside can lead to an increased risk of infection for our esteemed members and thus we have partnered with our Network providers to start an innovative service of TELECONSULTATION. Above service shall provide our members an online Audio/Video consultation with doctor/physician into our Network providers while sitting at home. There will be no requirement of visiting the premises of the healthcare care provider (Hospital/Clinic/Pharmacy) to take this consultation service. This service is extended in the lines of recommendation of Health Authorities which has allowed this new service in UAE healthcare sector while maintaining standards of healthcare delivery. -

Elizabeth a Duke: a Framework for Analyzing Bank Lending

Elizabeth A Duke: A framework for analyzing bank lending Speech by Ms Elizabeth A Duke, Member of the Board of Governors of the US Federal Reserve System, at the 13th Annual University of North Carolina Banking Institute, Charlotte, North Carolina, 30 March 2009. The original speech, which contains figures and various links to the documents mentioned, can be found on the US Federal Reserve System’s website. * * * In August 2008 I joined the Board of Governors of the Federal Reserve System, leaving behind a 30-year career as a commercial banker to become a central banker. My time as a commercial banker spanned numerous business cycles. It also encompassed at least one severe financial system crisis, in the late 1980s through the early 1990s, albeit one that was not as severe as the current one. From my time as a commercial banker, I already understood the factors considered by bankers in the initial lending decision as well as those in loss mitigation when collecting those same loans. As a central banker, I have come to appreciate even more fully the role of credit in our economic well-being. So I thought it would be appropriate for me to provide my perspective on credit conditions in our economy and the current crisis. Today, I would like to discuss a three-dimensional view of the flow of credit to households and businesses and describe the evolving role of banks in the U.S. economy. I will begin by taking a look at recent trends in aggregate borrowing by households and by the nonfinancial business sector. -

Danmarks Nationalbank 2 Thedanmarks Response of Householdnationalbank Customers to Negative Deposit Rates Analyses

ANALYSIS DANMARKS NATIONALBANK 27 APRIL 2021 — NO. 9 The response of house- hold customers to negative deposit rates Negative deposit Reduction in Announcement rates more deposits following increases demand widespread announcements for investments Negative deposit rates There are indications Household customers for household custom that household cus appear to increase their ers are now being tomers reduce their de demand for investment applied by most banks posits when their bank fund shares and switch in Denmark. Further announces negative their deposits to pool more, the banks have interest rates. However, schemes when faced gradually reduced the household customers’ with prospects of nega thresholds for when total deposits have tive deposit rates. negative interest rates increased during the are imposed. period of negative deposit rates. Read more Read more Read more ANALYSIS — DANMARKS NATIONALBANK 2 THEDANMARKS RESPONSE OF HOUSEHOLDNATIONALBANK CUSTOMERS TO NEGATIVE DEPOSIT RATES ANALYSES Low for long Denmark was the first country to introduce negative ABOUT THIS ANALYSIS monetary policy rates in 2012. Since then, Switzer- land, Sweden, Japan and the euro area have followed Most banks in Denmark have now in suit. troduced negative deposit rates for household customers. Furthermore, Very low and in some cases negative interest rates the banks have gradually reduced the thresholds for when negative have characterised the past decade across the ad- interest rates are payable. vanced economies. There are several reasons why interest rates have fallen to the current low levels. Low There are indications that household interest rates reflect the fact that inflation has been customers reduce their deposits subdued in many countries, but structural changes when their bank announces negative in household and corporate savings and investment interest rates.