The New Global Competition for Corporate Profits September 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ohio Major Employers

Policy Research and Strategic Planning Office A State Affiliate of the U.S. Census Bureau Ohio Major Employers September 2011 John R. Kasich, Governor of Ohio Christiane Schmenk, Director of Development TABLE OF CONTENTS Section One: Employers Ranked by Ohio Employment: Summary Findings Table 01. Ohio's Top Employers Table 02. Ohio's Leading Manufacturing Employers Table 03. Ohio's Leading Financial Employers Table 04. Ohio's Leading University Employers Section Two: Ohio-Based Companies Ranked by Sales: Map 01. Location of Ohio based Fortune 1000 Table 05. Fortune 1000 Companies Based in Ohio Table 06. Ohio-Based Forbes 500 Companies Table 07. Standard & Poor’s 500 / Ohio Based Corporations Table 08. Forbes 200 Largest Private Companies / Ohio Based Table 09. INC. 500 Private Companies / Ohio Based Section Three: Ohio Top Employers – Historic Section Top Employers in Ohio: 1995-2010 Fortune 1000 Companies Headquartered in Ohio Applied Industrial Technologies Medical Mutual of Ohio TravelCenters of America American Greetings Cliffs Natural Resources Sherwin-Williams Eaton KeyCorp Toledo Ferro !( Owens Corning ! !( !( !( !( Lubrizol Andersons !(!( Cleveland Lincoln Electric Dana Holding !( !(!( !( !(!( PolyOne !(!( Progressive Owens-Illinois !( !(! !( NACCO Industries !( Parker Hannifin Invacare Aleris International RPM International !( !( Jo-Ann Stores FirstEnergy !(!( Youngstown! !( Cooper Tire ! Goodyear Tire & Rubber Akron & Rubber Diebold !( !( J. M. Canton Smucker !!( Timken Thor Industries !( Scotts Greif Miracle-Gro !( !( !( Mettler-Toledo -

177 Mental Toughness Secrets of the World Class

177 MENTAL TOUGHNESS SECRETS OF THE WORLD CLASS 177 MENTAL TOUGHNESS SECRETS OF THE WORLD CLASS The Thought Processes, Habits And Philosophies Of The Great Ones Steve Siebold 177 MENTAL TOUGHNESS SECRETS OF THE WORLD CLASS 177 MENTAL TOUGHNESS SECRETS OF THE WORLD CLASS The Thought Processes, Habits And Philosophies Of The Great Ones Steve Siebold Published by London House www.londonhousepress.com © 2005 by Steve Siebold All Rights Reserved. Printed in Hong Kong. No part of this book may be reproduced, stored in or introduced into a retrieval system, or transmitted, in any form or by any means (electronic, mechanical, photocopying, recording or otherwise) without the prior written permission of the copyright owner. Ordering Information To order additional copies please visit www.mentaltoughnesssecrets.com or visit the Gove Siebold Group, Inc. at www.govesiebold.com. ISBN: 0-9755003-0-9 Credits Editor: Gina Carroll www.inkwithimpact.com Jacket and Book design by Sheila Laughlin 177 MENTAL TOUGHNESS SECRETS OF THE WORLD CLASS DEDICATION This book is dedicated to the three most important people in my life, for their never-ending love, support and encouragement in the realization of my goals and dreams. Dawn Andrews Siebold, my beautiful, loving wife of almost 20 years. You are my soul mate and best friend. I feel best about me when I’m with you. We’ve come a long way since sub-man. I love you. Walter and Dolores Siebold, my parents, for being the most loving and supporting parents any kid could ask for. Thanks for everything you’ve done for me. -

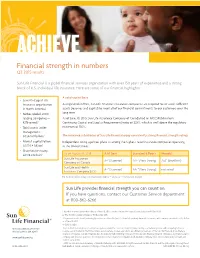

Financial Strength in Numbers Q2 2015 Results

ACHIEVE Financial strength in numbers Q2 2015 results Sun Life Financial is a global financial services organization with over 150 years of experience and a strong block of U.S. individual life insurance. Here are some of our financial highlights: A solid capital base • Seventh-largest life insurance organization As regulated entities, Sun Life Financial’s insurance companies are required to set aside sufficient in North America1 assets (reserves and capital) to meet all of our financial commitments to our customers over the • Forbes Global 2000 long term. leading companies— As of June 30, 2015, Sun Life Assurance Company of Canada had an MCCSR (Minimum #276 overall2 Continuing Capital and Surplus Requirements) ratio of 223%, which is well above the regulatory • Total assets under minimum of 150%. management: US$646.9 billion3 The insurance subsidiaries of Sun Life Financial enjoy consistently strong financial strength ratings. • Market capitalization: Independent rating agencies place us among the highest-rated insurance companies operating US$20.4 billion1 in the United States. • Shareholder equity: US$14.2 billion3 As of August 10, 2015 A.M. Best Standard & Poor’s Moody’s Sun Life Assurance A+4 (Superior) AA-4 (Very Strong) Aa34 (Excellent) Company of Canada Sun Life and Health A+4 (Superior) AA-4 (Very Strong) not rated Insurance Company (U.S.) For the most current ratings, visit www.sunlife.com/us --> About us --> Our financial strength. Sun Life provides financial strength you can count on. If you have questions, contact our Customer Service department at 800-862-6266. 1. Based on market capitalization data as of June 30, 2015, compiled by Sun Life Financial using data provided by IPREO. -

Wal-Mart's Data Warehouse

Wal-Mart’s Data Warehouse SCODAWA 2006 Patrick Ohlinger¨ Vienna University of Technology June 19, 2006 Abstract Wal-Mart is an exceptional company. As professor Strassmann [Stra06] says,”Mal-Mart really is a an information system integrator. Not a merchandising company. They are just selling goods as a byprod- uct. Fundamentally when you look at the value added by Wal-Mart, it is knowledge assets and how they are able to establish a global infor- mation network.” Wal-Mart’s data warehouse, the biggest in the world, enabled it to become a very successful company. Contents 1 About Wal-Mart 2 1.1 Where did Wal-Mart’s success come from? . 2 1.2 The Key to Always Low Prices. Always. ............ 3 2 Wal-Mart’s data warehouse provides Business Value 5 3 Focus on the Business 6 4 Build a Team 6 5 Apply Technology 8 5.1 Retail Link . 8 5.2 RFID . 8 1 1 About Wal-Mart Just getting read about in Austria, Wal-Mart is omnipresent in the U.S. It is the biggest retailer in the world and in many aspects just as well the biggest company in the world. Wal-Mart has 1,700,000 employes and their 5500 stores cannot be ignored. Wal-Mart is the second biggest private company in the world. With sales of $312 billion, this retailer is just behind ExxonMobil. While ExxonMobil is holding this position because of record oil prices, Wal-Mart is here to stay. As the worlds biggest company 1. Figure 1: Companies ranked by Sales [Forbes2000] Wal-Mart not only is big, with $11 billion in profit, it is also very suc- cessful. -

Pharmaceutical and Life Science Industry Services

PwC Russia’s Pharmaceutical and Life Science industry consulting practice has been operating Pharmaceutical for over 15 years. Thus far, we have assisted over 100 clients, including the largest companies and Life Science in the industry, to meet their business challenges. Industry Services Our knowledge and practical experience in executing projects for clients in the pharmaceutical and life science industry help us to deliver tax and legal services based on PwC best practices and advanced methods. Our services Entry to the Russian market Price regulation Limitation of advertising and communication with medical professionals • Consulting on price regulations for vital • Reviewing and elaborating advertising and essential medicines, including the Operating via representative materials, advising on compliance with registration of maximum selling prices, statutory limitations on advertising and offices and Russian legal application of maximum trade mark-ups, entities promotion of medicines, medical products and provision of discounts and rewards and services, representing clients in contact with the Russian Federal Anti-Trust Service • Providing advice on complying with statutory Localising Russian production Drug registration and limitations on communications with medical circulation and pharmaceutical professionals • Consulting on preferences and restrictions • Providing advice on licensing drug production and pharmaceutical activities in drug procurement for state needs, Compliance assessing specific benefits of localisation • Consulting -

Revolutionary Leadership Playing to Win the Power of Persuasion Happiness Matters Minimizing Gender Biases in the Workplace

EXECUTIVE BRIEFINGS DVDS AND VIDEO STREAMING NEW SPEAKERS AND BEST SELLERS ISISSSUEUE XXXIIXXXI Revolutionary Playing to Win The Power of Happiness Minimizing A.G. Lafley Leadership Former Chairman Persuasion Matters Gender Biases Gary Hamel and CEO Robert Cialdini Tony Hsieh in the Visiting Professor Procter & Gamble Professor CEO London Business Arizona State Zappos.com, Inc. Workplace School University Roger Martin Shelley Correll Dean Professor Rotman School Stanford of Management University Now You Can Stream Dear Friends, Executive Briefings Each month, we sponsor a business presentation here on the Stanford campus. Business Programs! leaders, academic experts, and renowned consultants provide creative solutions and practical advice for the challenges businesses face today. These engaging, thought-provoking 1-5 users: talks are available to you on DVD or online, giving you quick and easy access. Online Access price $95/program Get both: We’re proud to present new programs of particular interest: Online Access + DVD $139/program • Revolutionary Leadership by Gary Hamel, Visiting Professor, London Business School 6 or more users: (page 3) Online Access price $5.50/user and • Playing to Win: How Strategy Really Works by A.G. Laey, former Chairman and $65 setup fee/program CEO of Procter & Gamble, and Roger L. Martin, Dean, Rotman School of Get both: Online Access Management, University of Toronto (page 9) Online Access + DVD price plus $44/DVD • Minimizing Gender Biases in the Workplace by Stanford Professor Shelley Correll Generate quick quotes for Online (page 15) Access volume discounts at http://info.ExecutiveBriefings.com We also offer you the opportunity to order 10-program Special Collections by discipline, or the entire library of Stanford Executive Briengs on page 7—all at substantial discounts. -

MULGRAVE IPOD SHUFFLE NIGHT SONG LIST When You Purchase a Song It Acts As a Raffle Ticket

MULGRAVE IPOD SHUFFLE NIGHT SONG LIST When you purchase a song it acts as a raffle ticket. If your song is playing at 7:30pm, 8:00pm, 8:30pm etc. to 11:00pm (major prize) you will win a prize. The more songs you buy the better chance you have of winning. $5 per song. This is in conjunction with the 5k draw night on 11th of August. View the list and contact Brad Andrews to reserve your song(s) either via Facebook or by text 0403 193 085 SONG ARTIST PURCHASED BY PAID Mamma Mia Abba Gary Hewitt paid Rolling In The Deep Adele Bon Andrews paid destination calibria Alex guadino Alex Pagliaro Empire State Of Mind, Part. II Alicia Keys Damien Sheean paid Bound for Glory Angry Anderson Paul Bartlett paid Parlez Vous Francais Art Vs Science The Boys Of Summer The Ataris Aaron Kerr The Boys Light Up Australian Crawl Kade Wilsmore I Want I That Way Backstreet boys Now you're gone Basshunter Kokomo The Beach Boys Chris Anderton paid Belinda Carlisle ‐ Leave A Light On For Me Belinda carlisle Bon Andrews paid Girls (Who Run The World) Beyonce Uptown Girl Billy Joel Tim Knowles Only the Good Die Young Billy Joel Bon Andrews paid Pump It Black Eyed Peas The Time (The Dirty Bit) Black Eyed Peas I Gotta Feeling Black Eyed Peas Catherine Gladman paid The Sea is Rising Bliss N Eso Bad Touch Bloodhound Gang Aaron Kerr The Roof Is On Fire Bloodhound Gang Ron Gladman paid WARP 1.9 The Bloody Beetroots Matt Young Broken Leg Bluejuice Ryan James Freestyler Bomfunk MC's Bjorn Reed livin on a prayer Bon Jovi Gerry Beiniak paid you give love a bad name Bon Jovi Ash Beiniak paid in these arms tonight Bon Jovi Luke Parker The Lazy Song Bruno Mars Just The Way You Are Bruno Mars Taylor Buckley paid Let's Go (feat. -

Cognizant—Corporate Overview

Corporate Overview Engineering modern businesses DOOR 1 | Corporate Overview Cognizant (Nasdaq-100: CTSH) is one of the world’s leading professional services companies, transforming clients’ business, operating and technology models for the digital era. Our unique industry-based, consultative approach helps many of the best-known organizations in every industry and geography envision, build and run more innovative and efficient businesses. Founded in 1994 as a technology development arm of The Dun & Bradstreet Corporation, we were spun off as an independent company in 1996, and have worked closely with large organizations to help them build stronger businesses ever since. Today, Cognizant engineers modern businesses to improve everyday life, helping some of the world’s most established companies remain the most loved brands. In today’s fast-changing technology landscape, we work with our clients to advance every aspect of how they serve their customers: digitizing their products, services and customer experiences; automating their business processes; and modernizing their technology infrastructures. Put simply, we help clients harness digital to address their daily needs and keep their businesses relevant. As the partner they turn to execute on their digital priorities, we focus on IoT, AI, software engineering and cloud — the technologies that are changing the nature of business. Today, creating value by leveraging technology is very industry-specific, so we continue to deepen our expertise in 20 different industries, including banking and financial services, healthcare, manufacturing and retail. And to help speed clients’ journeys toward becoming digital, we bring our digital capabilities and industry expertise together into horizontal offerings and industry solutions that accelerate the most essential leaps that today’s technology makes possible, and complement those solutions with consulting and services built for the speed of business today. -

Forbes Top 500

Advances Newsletter, May, 2015 Vol. 5, #4, May 2015, No. 48 Forbes Top 500 The group has entered Forbes’ list of the world’s top 500 public companies 1 Advanceswww.midea.com Newsletter, May, 2015 ADVANCES Newsletter Contents NEWSLINE US$800 million to Be Spent on Language Group Enters the Forbes 500 Automation in 5 Years PAGE 8 PAGE 3 To Use or Not to Use a Dic- Magazine Publishes in-Depth tionary? PAGE 13-14 Report about Xiaomi Deal Midea App Available on PAGE 9 Big Picture Apple Watch PAGE 4 CAC Global Technical Concepcion Midea to Training Held in Shunde PAGE The Fast Food Wars PAGE 15 Double Sales Year-On-Year 10 PAGE 4 Innovative Cooking Solutions Idea Tasting the Home of the Fu- for Homes and Businesses Idea of the Month: Social ture PAGE 5 PAGE 11-12 Skills PAGE 16 Belarus JV to Diversify Prod- uct Range PAGE 6 People DDB Shanghai Wins RAC The Brains Behind the Brazil Contract PAGE 6 Brand PAGE 17-19 Official Sponsor of Indian Premier League Cricket Team PAGE 7 RAC Dominates Central Chinese City PAGE 7 Midea Advances Newsletter is published monthly Managing Editor: by the International Strategy Department of Midea Group. We welcome all comments, Kevin McGeary suggestions and contribution of articles, as well as Regular Correspondents: requests for subscription to our newsletter. You can reach us by email at: [email protected] Javier Romano John Baker Kelvin Wu Address: Lemon Lin ADVANCES, International Strategy Department Shirley Liu Midea HQ No. 6 Midea Road Beijiao, Shunde, Foshan, Guangdong P.R.C. -

In Focus 11Mar 2014

www.capsindia.org IN FOCUS 11MAR 2014 THE BIG QUESTION: IS CHINA FACING A FINANCIAL CRISIS, OR NOT? Prerna Gandhi Research Associate, CAPS In a first for Chinese Banks, four of them made history recently. The Industrial and Commercial Bank of China (ICBC) unseated Exxon Mobil last year to take the top spot on the Forbes Global 2000i as the world’s largest company. China Construction Bank moved up 11 spots to number 2 on the list. Agricultural Bank of China stood at number 8 and Bank of China with its double digit growth in sales and profits, improved its ranking by 10 places to number 11ii. However what is more interesting is that ICBC, world’s largest and most profitable bank was itself on the verge of defaulting until it was bailed out in January this year. A 3 billion Yuan (around US$500 million) product issued by China Credit Trust Co., a shadow bank and marketed through ICBC was underpinned by a loan to a mining operation of Shanxi Zhenfu Energy Group that later collapsed as the price of coal fell. Investors who had been promised a hefty 10% annual return over three years were told in January not to expect payment. Upset investors, some of whom had reportedly put as much as $500,000 each into the fund, sought reimbursement from the ICBC, who in turn, argued that it had never guaranteed the product, and had no legal responsibility to pay investors. However, the situation was retrieved by a bailout by an unnamed third party that ensured investors that they would recover their initial investment, though interest will not be paidiii. -

13 Malaysian Companies Listed on Forbes Global 2000

Headline 13 Malaysian companies listed on Forbes Global 2000 MediaTitle The Malaysian Reserve Date 08 Jun 2018 Language English Circulation 12,000 Readership 36,000 Section Money Page No 9 ArticleSize 666 cm² Journalist FARA AISYAH PR Value RM 18,485 13 Malaysian companies listed on Forbes Global 2000 Maybank takes the lead China Construction Bank Corp remains in the second spot. The although falls 4 spots to other two of China's "Big Four" 394th place with TNB banks — Agricultural Bank of at 503, CIMB (620) and China Ltd and Bank of China (BoC) — remain in the top ten, which Public Bank (646) is evenly split between China and the US. by FARA AISYAH JPMorgan Chase & Co is now the largest company in the US, moving THIRTEEN Malaysian companies « up one spot to number three and asaKii are listed in the Forbes' 16th annual overtaking Berkshire Hathaway Inc Global 2000 list this year, which is (four). based on a combination of sales, Rounding out the top 10 are Agri- profits, assets and market value. cultural Bank of China Ltd (five), " Malayan Banking Bhd (Maybank) Bank of America Corp (six), Wells once again leads local companies in Fargo & Co (seven), Apple Inc (eight), the list with a US$29.6 billion BoC (nine) and Ping An Insurance (RM117.68 billion) market capitalisa- Co of China Ltd (10). tion and US$9.13 billion of sales as at As a group, the Global 2000 June 2018. The bank fell four spots accounts for US$39.1 trillion in sales, from its 390th place last year to 394 in US$3.2 trillion in profit, US$189 tril- this year's list. -

Kevin Smith 2021 Speaker's Packet

Kevin Smith 2021 Speaker’s Packet Part of the Equation for Creating Successful Financial Institutions Contact information: [email protected] 608-217-0556 Biography of Kevin Smith Kevin Smith is Consultant and Publisher with TEAM Resources. He brings extensive experience in training, designing and implementing professional development resources to nourish the growth of leaders within the credit union industry. Kevin facilitates strategic planning processes, teaches Strategic Governance to Boards of Directors, and oversees the TEAM Resources board self- evaluation programs with credit unions nationwide. Kevin is co-author of A Credit Union Guide to Strategic Governance. This essential book helps Governance teams become as effective as possible. He also writes the monthly TEAM Resources blog that is read by thousands nationally. The monthly blog shares guidance on board topics such as governance, strategy and issues related to the supervisory committee. Previously, Kevin spent 10 years at the Credit Union National Association (CUNA), in the Center for Professional Development as Director of Volunteer Education. In that role Kevin developed and oversaw programs for credit union executives, boards, and volunteers. This included conferences and training events, webinars, print programs, and online courses, among others. During his tenure at CUNA, he created and brought several new programs to the credit union movement. One of these is the CUNA Volunteer Certification Program, an intensive, competency-based program for boards and supervisory committees, offered as a five-day onsite event or as a self-study program, both involving rigorous testing for completion. He also created the CUNA Training On Demand series of downloadable training courses, and the CUNA Pressing Economic Issues series featuring the CUNA economists.