In Focus 11Mar 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ohio Major Employers

Policy Research and Strategic Planning Office A State Affiliate of the U.S. Census Bureau Ohio Major Employers September 2011 John R. Kasich, Governor of Ohio Christiane Schmenk, Director of Development TABLE OF CONTENTS Section One: Employers Ranked by Ohio Employment: Summary Findings Table 01. Ohio's Top Employers Table 02. Ohio's Leading Manufacturing Employers Table 03. Ohio's Leading Financial Employers Table 04. Ohio's Leading University Employers Section Two: Ohio-Based Companies Ranked by Sales: Map 01. Location of Ohio based Fortune 1000 Table 05. Fortune 1000 Companies Based in Ohio Table 06. Ohio-Based Forbes 500 Companies Table 07. Standard & Poor’s 500 / Ohio Based Corporations Table 08. Forbes 200 Largest Private Companies / Ohio Based Table 09. INC. 500 Private Companies / Ohio Based Section Three: Ohio Top Employers – Historic Section Top Employers in Ohio: 1995-2010 Fortune 1000 Companies Headquartered in Ohio Applied Industrial Technologies Medical Mutual of Ohio TravelCenters of America American Greetings Cliffs Natural Resources Sherwin-Williams Eaton KeyCorp Toledo Ferro !( Owens Corning ! !( !( !( !( Lubrizol Andersons !(!( Cleveland Lincoln Electric Dana Holding !( !(!( !( !(!( PolyOne !(!( Progressive Owens-Illinois !( !(! !( NACCO Industries !( Parker Hannifin Invacare Aleris International RPM International !( !( Jo-Ann Stores FirstEnergy !(!( Youngstown! !( Cooper Tire ! Goodyear Tire & Rubber Akron & Rubber Diebold !( !( J. M. Canton Smucker !!( Timken Thor Industries !( Scotts Greif Miracle-Gro !( !( !( Mettler-Toledo -

Financial Strength in Numbers Q2 2015 Results

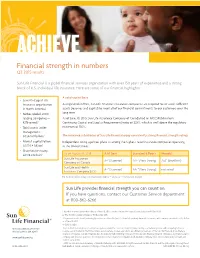

ACHIEVE Financial strength in numbers Q2 2015 results Sun Life Financial is a global financial services organization with over 150 years of experience and a strong block of U.S. individual life insurance. Here are some of our financial highlights: A solid capital base • Seventh-largest life insurance organization As regulated entities, Sun Life Financial’s insurance companies are required to set aside sufficient in North America1 assets (reserves and capital) to meet all of our financial commitments to our customers over the • Forbes Global 2000 long term. leading companies— As of June 30, 2015, Sun Life Assurance Company of Canada had an MCCSR (Minimum #276 overall2 Continuing Capital and Surplus Requirements) ratio of 223%, which is well above the regulatory • Total assets under minimum of 150%. management: US$646.9 billion3 The insurance subsidiaries of Sun Life Financial enjoy consistently strong financial strength ratings. • Market capitalization: Independent rating agencies place us among the highest-rated insurance companies operating US$20.4 billion1 in the United States. • Shareholder equity: US$14.2 billion3 As of August 10, 2015 A.M. Best Standard & Poor’s Moody’s Sun Life Assurance A+4 (Superior) AA-4 (Very Strong) Aa34 (Excellent) Company of Canada Sun Life and Health A+4 (Superior) AA-4 (Very Strong) not rated Insurance Company (U.S.) For the most current ratings, visit www.sunlife.com/us --> About us --> Our financial strength. Sun Life provides financial strength you can count on. If you have questions, contact our Customer Service department at 800-862-6266. 1. Based on market capitalization data as of June 30, 2015, compiled by Sun Life Financial using data provided by IPREO. -

Wal-Mart's Data Warehouse

Wal-Mart’s Data Warehouse SCODAWA 2006 Patrick Ohlinger¨ Vienna University of Technology June 19, 2006 Abstract Wal-Mart is an exceptional company. As professor Strassmann [Stra06] says,”Mal-Mart really is a an information system integrator. Not a merchandising company. They are just selling goods as a byprod- uct. Fundamentally when you look at the value added by Wal-Mart, it is knowledge assets and how they are able to establish a global infor- mation network.” Wal-Mart’s data warehouse, the biggest in the world, enabled it to become a very successful company. Contents 1 About Wal-Mart 2 1.1 Where did Wal-Mart’s success come from? . 2 1.2 The Key to Always Low Prices. Always. ............ 3 2 Wal-Mart’s data warehouse provides Business Value 5 3 Focus on the Business 6 4 Build a Team 6 5 Apply Technology 8 5.1 Retail Link . 8 5.2 RFID . 8 1 1 About Wal-Mart Just getting read about in Austria, Wal-Mart is omnipresent in the U.S. It is the biggest retailer in the world and in many aspects just as well the biggest company in the world. Wal-Mart has 1,700,000 employes and their 5500 stores cannot be ignored. Wal-Mart is the second biggest private company in the world. With sales of $312 billion, this retailer is just behind ExxonMobil. While ExxonMobil is holding this position because of record oil prices, Wal-Mart is here to stay. As the worlds biggest company 1. Figure 1: Companies ranked by Sales [Forbes2000] Wal-Mart not only is big, with $11 billion in profit, it is also very suc- cessful. -

Pharmaceutical and Life Science Industry Services

PwC Russia’s Pharmaceutical and Life Science industry consulting practice has been operating Pharmaceutical for over 15 years. Thus far, we have assisted over 100 clients, including the largest companies and Life Science in the industry, to meet their business challenges. Industry Services Our knowledge and practical experience in executing projects for clients in the pharmaceutical and life science industry help us to deliver tax and legal services based on PwC best practices and advanced methods. Our services Entry to the Russian market Price regulation Limitation of advertising and communication with medical professionals • Consulting on price regulations for vital • Reviewing and elaborating advertising and essential medicines, including the Operating via representative materials, advising on compliance with registration of maximum selling prices, statutory limitations on advertising and offices and Russian legal application of maximum trade mark-ups, entities promotion of medicines, medical products and provision of discounts and rewards and services, representing clients in contact with the Russian Federal Anti-Trust Service • Providing advice on complying with statutory Localising Russian production Drug registration and limitations on communications with medical circulation and pharmaceutical professionals • Consulting on preferences and restrictions • Providing advice on licensing drug production and pharmaceutical activities in drug procurement for state needs, Compliance assessing specific benefits of localisation • Consulting -

Cognizant—Corporate Overview

Corporate Overview Engineering modern businesses DOOR 1 | Corporate Overview Cognizant (Nasdaq-100: CTSH) is one of the world’s leading professional services companies, transforming clients’ business, operating and technology models for the digital era. Our unique industry-based, consultative approach helps many of the best-known organizations in every industry and geography envision, build and run more innovative and efficient businesses. Founded in 1994 as a technology development arm of The Dun & Bradstreet Corporation, we were spun off as an independent company in 1996, and have worked closely with large organizations to help them build stronger businesses ever since. Today, Cognizant engineers modern businesses to improve everyday life, helping some of the world’s most established companies remain the most loved brands. In today’s fast-changing technology landscape, we work with our clients to advance every aspect of how they serve their customers: digitizing their products, services and customer experiences; automating their business processes; and modernizing their technology infrastructures. Put simply, we help clients harness digital to address their daily needs and keep their businesses relevant. As the partner they turn to execute on their digital priorities, we focus on IoT, AI, software engineering and cloud — the technologies that are changing the nature of business. Today, creating value by leveraging technology is very industry-specific, so we continue to deepen our expertise in 20 different industries, including banking and financial services, healthcare, manufacturing and retail. And to help speed clients’ journeys toward becoming digital, we bring our digital capabilities and industry expertise together into horizontal offerings and industry solutions that accelerate the most essential leaps that today’s technology makes possible, and complement those solutions with consulting and services built for the speed of business today. -

Forbes Top 500

Advances Newsletter, May, 2015 Vol. 5, #4, May 2015, No. 48 Forbes Top 500 The group has entered Forbes’ list of the world’s top 500 public companies 1 Advanceswww.midea.com Newsletter, May, 2015 ADVANCES Newsletter Contents NEWSLINE US$800 million to Be Spent on Language Group Enters the Forbes 500 Automation in 5 Years PAGE 8 PAGE 3 To Use or Not to Use a Dic- Magazine Publishes in-Depth tionary? PAGE 13-14 Report about Xiaomi Deal Midea App Available on PAGE 9 Big Picture Apple Watch PAGE 4 CAC Global Technical Concepcion Midea to Training Held in Shunde PAGE The Fast Food Wars PAGE 15 Double Sales Year-On-Year 10 PAGE 4 Innovative Cooking Solutions Idea Tasting the Home of the Fu- for Homes and Businesses Idea of the Month: Social ture PAGE 5 PAGE 11-12 Skills PAGE 16 Belarus JV to Diversify Prod- uct Range PAGE 6 People DDB Shanghai Wins RAC The Brains Behind the Brazil Contract PAGE 6 Brand PAGE 17-19 Official Sponsor of Indian Premier League Cricket Team PAGE 7 RAC Dominates Central Chinese City PAGE 7 Midea Advances Newsletter is published monthly Managing Editor: by the International Strategy Department of Midea Group. We welcome all comments, Kevin McGeary suggestions and contribution of articles, as well as Regular Correspondents: requests for subscription to our newsletter. You can reach us by email at: [email protected] Javier Romano John Baker Kelvin Wu Address: Lemon Lin ADVANCES, International Strategy Department Shirley Liu Midea HQ No. 6 Midea Road Beijiao, Shunde, Foshan, Guangdong P.R.C. -

13 Malaysian Companies Listed on Forbes Global 2000

Headline 13 Malaysian companies listed on Forbes Global 2000 MediaTitle The Malaysian Reserve Date 08 Jun 2018 Language English Circulation 12,000 Readership 36,000 Section Money Page No 9 ArticleSize 666 cm² Journalist FARA AISYAH PR Value RM 18,485 13 Malaysian companies listed on Forbes Global 2000 Maybank takes the lead China Construction Bank Corp remains in the second spot. The although falls 4 spots to other two of China's "Big Four" 394th place with TNB banks — Agricultural Bank of at 503, CIMB (620) and China Ltd and Bank of China (BoC) — remain in the top ten, which Public Bank (646) is evenly split between China and the US. by FARA AISYAH JPMorgan Chase & Co is now the largest company in the US, moving THIRTEEN Malaysian companies « up one spot to number three and asaKii are listed in the Forbes' 16th annual overtaking Berkshire Hathaway Inc Global 2000 list this year, which is (four). based on a combination of sales, Rounding out the top 10 are Agri- profits, assets and market value. cultural Bank of China Ltd (five), " Malayan Banking Bhd (Maybank) Bank of America Corp (six), Wells once again leads local companies in Fargo & Co (seven), Apple Inc (eight), the list with a US$29.6 billion BoC (nine) and Ping An Insurance (RM117.68 billion) market capitalisa- Co of China Ltd (10). tion and US$9.13 billion of sales as at As a group, the Global 2000 June 2018. The bank fell four spots accounts for US$39.1 trillion in sales, from its 390th place last year to 394 in US$3.2 trillion in profit, US$189 tril- this year's list. -

Gpoc 2018 Global Powers of Construction Gpoc Is an Annual Publication Produced by Deloitte Spain and Distributed Free of Charge

GPoC 2018 Global Powers of Construction GPoC is an annual publication produced by Deloitte Spain and distributed free of charge Director Javier Parada, Global Leader Engineering and Construction Coordinated by Margarita Velasco Martín Alurralde Beatriz Rojo Guillem Bofill Published by Communications, Brand and Business Development department Contact Infrastructure Department, Deloitte Madrid Plaza Pablo Ruiz Picasso, S/N Torre Picasso 28020 Madrid, Spain Phone + 34 91 514 50 00 Fax + 34 91 514 51 80 July 2019 GPoC 2018 | Global Powers of Construction 4 Introduction 5 Ranking of listed global construction companies 7 Top 100 GPoC – ranking by sales 10 Top 30 GPoC – ranking by market capitalisation 13 Top 30 GPoC – ranking by international sales 14 Outlook for the construction industry 18 Shaping the future 21 Top 30 GPoC strategies: internationalisation and diversification 24 Financial performance of the GPoC 2018 35 International presence of our GPoC 2018 39 Diversification of the GPoC 2018 48 Study methodology and data sources 49 Deloitte global construction and infrastructure group contacts 50 Appendix - Exchange rates 51 Endnotes 3 GPoC 2018 | Global Powers of Construction Introduction Global Powers of Construction analyses the current economic situation of the construction industry worldwide and examines the strategies and performance of the most representative listed global construction groups in 2018. We are pleased to present Global Powers expected investments in renewables and concessions, engineering, services and real of Construction, a publication that telecommunications are forecast to result estate, and their main financial information identifies and ranks the world's major listed in the construction industry growing above has been compared with that of our GPoC. -

Walmart Pays Workers Poorly and Sinks While Costco Pays Workers Well and Sails-Proof That You Get What You Pay for 9/5/14, 10:00 AM

Walmart Pays Workers Poorly And Sinks While Costco Pays Workers Well And Sails-Proof That You Get What You Pay For 9/5/14, 10:00 AM Safari Power Saver Click to Start Flash Plug-in OPINION (/OPINION) 4/17/2013 @ 10:49AM 273,285 views Walmart Pays Workers Poorly And Sinks While Costco Pays Rick Ungar Workers Well And Sails-Proof That (http://www.forbes.com/sites/rickungar/) Contributor You Get What You Pay For FOLLOW Comment Now Follow Comments I write from the left on politics and policy. Costco’s most recent Safari Power Saver full bio → quarterly earnings report Click to Start Flash Plug-in Opinions expressed by Forbes (http://phx.corporate- Contributors are their own. ir.net/phoenix.zhtml? (http://twitter.com/rickungar)(http://www.facebook.com/richard.ungar)(http://www.forbes.com/sites/rickungar/feed/)(http://www.forbes.com/sites/rickungar/)c=83830&p=irol- A protest in Utah against Wal- Mart (Photo credit: Wikipedia) newsArticle&ID=1794682&highlight=) reveals a fairly healthy eight percent rate of growth in year-on-year 431 sales—including a five percent rise in same store sales. COMMENTS What’s more, with membership fees rising from $459 million in the same quarter last year to $528 million this year, it’s pretty clear that a significant number of 64 CALLED-OUT customers are moving over to the retailer to do their Follow Comments discount shopping. Meanwhile, Costco’s primary competitor, Walmart, saw an anemic 1.2 percent rise in sales, while other competitors such as J.C. Penny and Target (/companies/target/) TGT -0.66% (/companies/target/) experienced even greater disasters in their sales results. -

Forbes India Magazine

Magazine Upfront Features Life Daily Sabbatical Multimedia Blogs News Lists Search forbesindia.com Home | Wednesday, June 10, 2015 | 1:30:33 PM Follow FEATURES/FORBES GLOBAL 2000 | Jun 10, 2015 | 1454 views Visa CEO Charlie Scharf: Moving at the speed of money by Daniel Fisher While overhyped cryptocurrencies like bitcoin grab all the attention, Visa CEO Charlie Scharf has quietly put a $6.8 trillion stranglehold on the world's commercial transactions. The future of payments? Surprise! It's already here Like 91 Tweet 10 Share 6 Tweet Share Advertise with us >> + Comment now + Single Page View Email Print LATEST ISSUE India Inc slowly recovers ground on the Forbes Global 2000 Baby Buffett: Bill Ackman 2.0 David Caldwell and his magic touch Contents » Past Issues » INSTA-SUBSCRIBE to Forbes India Magazine GLOBAL GAME David Caldwell and his magic touch Image: Matt Furman for Forbes The Google for the broken web Visa’s chief executive, Charlie Scharf Bentley on a roll itting inconspicuously among the Pentagon contractors and trade associations in a Meet Andrew Beal, the Warren Buffett of western suburb of Washington, DC, is a low-slung building protected by the banking business S landscaped berms and a fence topped by razor wire. The exterior walls are a MORE » patchwork of whites, greys and greens to confuse passersby trying to judge its size from a distance. A 24-foot-deep moat provides a last line of defence against anybody trying to crash a vehicle through its walls. But while this fortress could easily pass as an outpost of some shadowy three-letter spy agency, it’s actually home to something far more mundane—and far more powerful. -

Business Aviation and the World's Top Performing Companies

BUSINESS AVIATION Part V Fall 2013 And The World’s Top Performing Companies WWW.NEXACAPITAL.COM WWW.NBAA.ORG +1 202 558 7417 +1 202 783 9000 NEXA Advisors thanks the National Business Aviation Association and JETNET LLC for their generous support of this project. This is the fifth in a series of NEXA Advisors studies on business aviation and shareholder value. The prior studies exam- ined various aspects of U.S. business aviation and interrelationships with the key drivers of shareholder value. Business Aviation: the World’s Top Performing Companies raises the issue to the global level, examining business aviation’s contri- bution to the top performing companies in the world. WWW.NEXACAPITAL.COM WWW.NBAA.ORG +1 202 558 7417 +1 202 783 9000 World Leader in Aviation Market Intelligence WWW.JETNET.COM © 2013 NEXA Advisors, LLC. All rights reserved. NEXA Advisors • Business Aviation • 1 Contents Executive Summary 3 Introduction 5 Trade Economics 101 5 Distance and Business Mobility Challenges 5 Business Aviation Growth Tracks GDP Expansion 6 The Time Saving Benefits of Business Aviation 7 NEXA Advisors Business Aviation Value Methodology 8 The UBV Framework 9 What We Found 10 Global Business Aviation Overview 10 Regional Summaries 14 Best of The Best 20 Conclusions 22 NEXA Report Authors and Further Information 23 ABOUT NEXA ADVISORS 24 NEXA Advisors • Business Aviation • 2 Executive Summary There is now ample proof that business aviation creates value in ways unique to American enterprise. Over a broad range of uses, according to prior studies on the matter, business aircraft can materially improve a company’s ability to create shareholder value and subsequently shareholder returns. -

REVISED 2016 Business Awards Booklet

THE HONORABLE MAYOR BELLE ISLE AND THE CITY OF ALPHARETTA COUNCIL PRESENT THE 5TH ANNUAL BUSINESS AWARDS RECOGNITION BREAKFAST LIST OF HONORED BUSINESSES AND CORPORATIONS SPONSORED BY 6 Degrees Group Alpharetta Flower Market Inc 5000 Florist (Runner Up) - Appen's Best of the Best Abbott Laboratories Alpine Bakery Global 2000 - Forbes; America's Best Employers - Bakery (Winner) - Appen's Best of the Best; Dessert Forbes; Fortune 500 - Fortune (Winner) - Appen's Best of the Best Acsential Altria Group Inc 5000 Global 2000 - Forbes; America's Best Employers - Forbes Actimize, Inc. 2016 Best AML Compliance Solution Provider - Amazon Retail, LLC Waters Rankings Innovative Companies - Forbes; Global 2000 - Forbes; World's Most Valuable Brands - Forbes; America's Best Adecco Employers - Forbes; World's Most Admired Companies Global 2000 - Forbes - Fortune; Fortune 500 - Fortune ADP Amdocs America's Best Employers - Forbes; Fortune 500 - Global 2000 - Forbes; America's Best Employers - Fortune; 100 Best Companies for Working Mothers - Forbes; Ground-breaking NFV Initiative - Global Working Mother magazine Telecoms Awards Aetna Antico Global 2000 - Forbes; America's Best Employers - Pizza (Runner Up) - Appen's Best of the Best Forbes AON Alcatel-Lucent Global 2000 - Forbes 2016 Wholesale Service Innovation for Seabras-1 New York to Brazil Subsea Cable Project - Telecoms Appen Media Group, Inc. Innovation & Technology Awards (GTB) 21 Individuals awards for Appen Media Group Staff (David Brown, Suzanne Pacey, A.J. McNaughton, Alpharetta Animal Hospital