Reuse of Primary Packaging Final Report Part I Main Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Packing and Crating Basics C2C Care Webinar to Begin With

Packing and Crating Basics C2C Care Webinar To begin with... ● Determine the needs of your object ○ What is your object made out of? ○ How will your crate be used? ■ Storage? ■ Traveling? ● How many times will the crate travel? ○ Single venue vs. multi-venue Storage vs. Traveling Crates ● There is a difference between crates for storage and crates for transit ● Different materials will be used for storage vs. transit ● Types of foam: ○ Thermal insulating foams for transit ■ U-foam ■ Esterfoam ■ Polystyrene Extruded foam ○ Shock absorbing foams for transit and storage ■ Ethafoam (various densities) ■ Volara Storage Concerns ● Off-gassing inside the storage crate ○ Avoid using Esterfoam, U-foam, and Polystyrene foams. ■ Objects should not be stored in closed crates with these foams for more than 90 days. ○ Be aware of the materials the object will be contact with. ○ Be aware of the composition of the object itself. ● Object should be easy to access and identify Transit Concerns ● Vibration and shock ○ Use an appropriate amount and type of foam ● Changes in temperature and climate ○ Line crates with thermal insulating foam such as U-foam, Esterfoam, or Polystyrene Extruded foam ● Handling ○ Crate should have clear stencils, skids, and handles to encourage safe handling ● Ease of packing/unpacking ○ Clear packing/unpacking instructions/diagrams Flatworks Common packing solutions for flatworks: ● Trays ○ Usually for framed works ○ allows multiple objects to be packed in the same crate ● Travel frames ○ For unframed canvases, or objects that -

WHEATON® Glass Bottles

WHEATON® Glass Bottles WHEATON® Glass Bottles WHEATON offers a comprehensive line of glass laboratory bottles and jars. Glass bottles offer sample reliability and integrity, and is a mainstay of labs worldwide. WHEATON bottles are manufactured from USP Type III soda-lime glass with moderate chemical resistance. Popular bottle styles available include Media Bottles, Boston Rounds, Wide Mouth Packers, Straight Sided Jars and Safety Coated Bottles for enhanced laboratory protection. WHEATON completes the package with the right closure. We provide a variety of caps and seals to ensure a perfect fit for each container. WHEATON offers convenience bulk packs of containers with or without caps attached for high use items or facilities with centralized stockrooms. With safety in mind, Tamper Evident Seal / HAZCOM Labels are provided in each case of bottles with the exception of bulk packs. Product Highlights • Bottles manufactured from clear and amber USP Type III soda-lime glass • Wide mouth bottles are ideal for dry and viscous samples • White polypropylene or black phenolic screw closures can be • Amber colored glass is ideal for light sensitive products purchased separately • Narrow mouth bottles are ideal for liquids • Methods of sterilization: dry heat or EtO (not suitable for autoclave) • Safety coated glass prevents dangerous spills and control sharp fragments WHEATON® Glass Bottles French Square Valumetric™ Graduated Bottle Media Bottle, Lab 45 ■ Clear or Amber, USP Type III soda-lime glass ■ Clear, USP Type III soda-lime glass ■ Manufactured -

Structures and Exterior Envelope

Integration: Structure and Envelope Integrated Building Systems Part I: Integration Principles Part II: Structure and the Exterior Envelope Part III: Integration Case Studies 4.405Building Systems Building Systems: Definitions 1. Foundation/Subgrade (SITE) 2. Superstructure (STRUCTURE) Daly, Genik: Valley Center, CA, 2000. 3. Exterior Envelope (SKIN) 4. Interior Partitions (SPACE PLAN) 5. Mechanical Systems (SERVICES) 6. Furnishings (STUFF) Stuff Space Plan Services Structure Sources: Brand, Howard, Skin How Buildings Learn. Site Also see Turner, Gregory, Construction Economics and Building Design Bensonwood Timber Frame: 1996. Image by MIT OCW. 4.405Building Systems Building Systems: Definitions 1. Foundation/Subgrade (SITE) 2. Superstructure (STRUCTURE) 3. Exterior Envelope (SKIN) 4. Interior Partitions (SPACE PLAN) 5. Mechanical Systems (SERVICES) 6. Furnishings (STUFF) Rush specifies only four systems; • Structure • Envelope • Interior • Mechanical Source: Rush, Richard, The Building Systems Integration Handbook Curtainwall and raised floor construction. Image by MIT OCW. Integration Levels Definitions 1. Remote: systems are Remote physically separated from one another but yet still coordinated functionally Touching 2. Touching: One system rests on another Connected 3. Connected: one system is mechanically fastened and dependent on another Meshed 4. Meshed: systems occupy the same space Unified 5. Unified: systems share the same physical elements Five Levels of Integration Image by MIT OCW. Image by MIT OCW. Performance Mandates Roof Assembly: Performance is, generally, the Roof structure and measurement of achievement structural deck (S) Roofing (E) E against intention. Ceiling (I) Lighting (MI) Roof Assembly S Wall Assembly: 1. Spatial Performance Wall structure (the support plus any lateral bracing, shear panels, I MI 2. Thermal Performance or sheathing) (S) I Exterior wall covering (EI) 3. -

Paper 101 with Courtney Cerruti

Paper 101 with Courtney Cerruti Chapter 1 - Paper 101 Paper 101 (pop drum music) - Paper is one of those medium's that really is so versatile, and can be used for so many projects. I love to make a-million-and-one different things out of paper. Anywhere from book crafts, to paper crafts, things like making cards, doing collages, or even something like making paper flowers. And for all of those projects, I would use a different weight of paper. And it's really helpful to understand a little bit more about paper when you start to work with it. How to find grain and what projects should be used with which types of paper. If you're familiar with the concept that fabric has a grain, paper also has a grain. And that just indicates which way the fibers of the paper, when it's made, are running. If they're predominantly running vertically or horizontally. So, we do this things called the "bounce test," which always you to just fold the paper in one direction, and just gently bounce it to see how much resistance you have, and then you would turn it the opposite direction, and do the same thing. And you can see, that I really press this down. So, that means, that my grain is going parallel to where I'm creating this little fold. So, my grain runs this way. If we go back to that other direction, we can see how hard that is to press it down. And that's against the grain. -

SCHOTT DURAN® Laboratory Glass Bottles and Screw Caps - Rely on the Original! - 50086 E 0105 6.5 Ba/Jo Printed in Germany

04194_Sprache_E_RZ.fh8 24.01.2005 14:31 Uhr Seite 2 LABWARE SCHOTT DURAN® E SCHOTT DURAN® laboratory glass bottles and screw caps - Rely on the original! - 50086 e 0105 6.5 ba/jo Printed in Germany Labware SCHOTT AG Hattenbergstrasse 10 55122 Mainz Germany Phone: +49 (0)6131/664907 Fax: +49 (0)6131/664016 E-mail: [email protected] www.schott.com/duran 04194_Sprache_E_RZ.fh8 24.01.2005 14:31 Uhr Seite 3 SCHOTT DURAN® laboratory glass bottles Fields of application and properties The outstanding properties of DURAN® laboratory glass bottles have been valued for many years. By continuous development and improvement, SCHOTT is able to provide top-quality products and systems based on the original, well proven bottle design. Their consistency, reliability and flexibility in storage, packaging and preparation applications make DURAN® laboratory glass bottles the global standard for the chemical, pharmaceutical and bioscience fields. ■ conformity with ISO standards 3585 and 4796 ■ glass type No. 1, normal glass pursuant to USP 27; EP; DAB 10 ■ high service temperature of up to 500°C ■ excellent thermal shock resistance ■ easy to clean and readily sterilized ■ excellent chemical resistance ■ highly inert ■ standardized GL screw thread and matching screw cap systems ensure a low-leakage closure with excellent pouring capabilities ■ stable design and uniform wall strength make DURAN® laboratory glass bottles robust helpers in daily work even under high mechanical strain and rapid or extreme changes in temperature ■ all DURAN® laboratory glass bottles are now supplied with a printed “Retrace Code” allowing batch and quality certification via the internet NEW 04194_Sprache_E_RZ.fh8 24.01.2005 14:31 Uhr Seite 4 A perfect solution to each and every application The classic version – the DURAN® laboratory glass bottle The original is widely used in labora- tories and factories in numerous applications. -

Food & Distribution

Food & Distribution www.piramalglassusa.com Food & Distribution Quality you can trust, Why Piramal Glass Design you will love Piramal Glass Limited (PGL) provides turnkey solutions for glass packaging in over 54 countries for the Specialty Liquor, Beauty, Pharmaceutical, and Food & Distribution markets. We have glass bottle manufacturing and decorating facilities in India, USA and Sri Lanka & Piramal Glass USA is the leader in glass marketing offices in Mumbai, Paris, Sao Paulo, Colombo and Dayton. packaging solutions for the Specialty Piramal Glass USA (PG USA) is the US subsidiary of PGL and a vertically integrated company. We have a glass manufacturing operation in Park Hills, Missouri and a decoration Liquor, Beauty, Pharmaceutical, and Food facility in Williamstown, New Jersey. Supplementing these operations are our warehouses: on the West Coast in Santa Fe Springs, California; in the heartland of the country in Park & Distribution industries. Our multiple state Hills, Missouri; and on the East Coast in Dayton, NJ (the home of our US corporate and marketing office). of the art molded glass plants produce PG USA offers a wide variety of Industry Standards, Piramal Proprietary Designs and industry standard & unique shelf stock and custom designed molds to customers ranging from emerging start-up companies to large multinationals. We provide high-quality shelf stock bottles that will enhance your product. custom containers for both local and global These in stock containers will facilitate quickness to market and reduce initial launch costs. Should your brand require a custom design whether it be the altering of an existing markets. Additionally we provide a variety stock mold or the building of a new custom mold, we offer digital product and engineering services that take your design from concept to delivery. -

Basic Guide to Bottle Identification Say You're Planting a New Tree in Your

Basic Guide to Bottle Age Identification Say you’re planting a new tree in your backyard, and you dig a hole deeper than you’ve had to dig before. In the hole you find a glass bottle that you didn’t put there. How can you identify the bottle? How can you tell if it is old or just a piece of modern recycling that the previous owner left behind? Below please find a basic guide to help you identify a bottle’s age. Bottle identification is a rabbit hole that I’ve found fun to fall into; one bottle can take hours to research, and sometimes, you can’t find anything on it at all! In addition, manufacturing technological advances were adopted over time, not all at once, so older techniques were used at the same time as newer ones. This makes determining exact age for a bottle that wasn’t machine-made a little tricky. But, by looking at a few basic characteristics, you can learn if you want to toss your find in the recycling bin or place it at the center of your mantle. If you are interested in discovering more, I’ve listed some helpful web sites at the end. If you just want a basic guide, hope this helps! How was the bottle made? The first thing that I do when I handle a bottle is look at the construction – the sides, the top or lip, and the base. Free-Blown - Bottles were blown by hand in antiquity, and free-blown bottles were the main manufacturing technique used before the mid-1800s for utilitarian bottles. -

Festo Didactic, Inc. SKU/Part Number Item Description List Price Discount

FESTO DIDACTIC, INC. Group 38224-Award 23077 Materials and Equipment for Educational Technology and Occupational Training (Statewide) July 2019 Contractor: Festo Didactic, Inc. Contract No: PC67815 SKU/Part Number Item Description List Price Discount Net Price 581539 Cables and Accessories $258.71 5.00% $245.77 581540 Cables and Accessories - Digital Telecommunications $574.89 5.00% $546.15 581541 Cables and Accessories - Digital Communications Add-On $467.09 5.00% $443.74 581542 Power Supply / Dual Audio Amplifier $3,018.17 5.00% $2,867.26 581549 Dual Function Generator $2,903.19 5.00% $2,758.03 581552 Frequency Counter $2,249.25 5.00% $2,136.79 581555 True RMS Voltmeter / Power Meter $2,292.37 5.00% $2,177.75 581558 Spectrum Analyzer $8,407.76 5.00% $7,987.37 581561 RF/Noise Generator $4,024.23 5.00% $3,823.02 581564 Data Acquisition and Management for Telecommunications (LVDAM-COM) $23,642.33 5.00% $22,460.21 581571 TTS Power Supply $1,415.66 5.00% $1,344.88 581574 AM/DSB/SSB Generator $4,804.25 5.00% $4,564.04 581577 AM/DSB Receiver $3,370.14 5.00% $3,201.63 581580 SSB Receiver $3,370.14 5.00% $3,201.63 581583 Direct FM Multiplex Generator $5,162.77 5.00% $4,904.63 581586 Indirect FM/PM Generator $4,517.43 5.00% $4,291.56 581589 FM/PM Receiver $6,740.28 5.00% $6,403.27 581592 Enclosure / Supply Regulator $1,178.53 5.00% $1,119.60 581593 Clock Generator $2,486.40 5.00% $2,362.08 581596 Pseudo-Random Binary Sequence Generator $3,233.76 5.00% $3,072.07 581599 Bit Error Rate Indicator $1,624.06 5.00% $1,542.86 581602 Logic Analyzer $1,997.74 -

KMR Catalogue 2021

The partner of craftsmen Catalogue 2021 New! www.kmr-group.eu Company history Welcome to KMR! 1914 Karl Mathias Reich founded the business with 5 employees and started manufacturing wire and equipment that uses wire. 1925 The first stationary carpentry equipment. 1960s New creations like the first portable pneumatic nailers. 2000 Foundation of the Karl M. Reich GmbH production and distribution company. 2013 The Karl M. Reich Verbindungstechnik brand was taken over by the German BeA group. 2016 The products bear the initials of the founder Karl Mathias Reich: KMR. 2018 Introduction of gas nailers into the product range 2020 Relaunch of the KMR homepage, state-of-the-art technique: modern, quick, user-friendly and all information on tools and fasteners at your disposal any time and anywhere! 2021 Introduction of the new KMR 3-in-1 Multi tool AC/90-942C. The unique nailing tool for 3 different nail collation types. KMR – The partner of craftsmen All information concerning our tools and fasteners can be retrieved as of now on mobile devices at any time. Our product information is at your disposal exactly when you need it - in the office, on the construction site, in the factory or when visiting a client. www.kmr-group.eu gives you quick and easy all information on our product range: Our tools for professionals and fasteners in different materials and dimensions. Furthermore you will find all technical details on our tools, helpful application hints for your projects as well as a huge download area. The download area contains all important documents and declarations of performance (DoPs), CE-label, ETA approvals, as well as manuals - all these documents are available online at any time. -

Vacuum Pump Page 6 IMPORTANT: Read All Instructions Before Using

Festool GmbH Wertstraße 20 D-73240 Wendlingen www.festoolusa.com Instruction manual - Vacuum pump Page 6 IMPORTANT: Read all instructions before using. Guide d’utilisation - Pompe à vide Page 14 IMPORTANT: Lire toutes les instructions avant de démarrer les travaux. Manual de instrucciones - Bomba de vacío Página 23 IMPORTANTE: Lea todas las instrucciones antes de usar. Instruction manual Guide d’utilisation Manual de instrucciones VAC PMP 708410_001 1-1 1-2 1 1-4 1-3 2-5 2-4 2-3 2-2 2-6 2-1 2 Contents Functional description.......................... 8 Symbols................................................ 6 Preparing for use ................................. 9 About this manual................................ 6 Service and maintenance ..................... 11 Safety instructions ............................... 7 Environment ......................................... 11 Intended use ........................................ 8 Troubleshooting.................................... 12 Technical data ...................................... 8 Symbols Symbol Significance Symbol Significance Vvolts Warning of general danger A amperes Risk of electric shock W Watt Hz hertz Read operating instructions and safety rpm rounds per minute notices! ~ a.c. alternating current Do not dispose of as domestic waste. d.c. direct current ft feet Warning: Hot surface! in inch lb pound Tip or advice mbar airpressure in millibar Handling instruction °F temperature in degrees Fahrenheit About this manual Save these instructions It is important for you to read and understand this manual. The information it contains relates to protecting your safety and preventing problems. The symbols below are used to help you recognize this information. DANGER Description of imminent haz- NOTICE Statement including nature of ard and failure to avoid hazard hazard and possible result. will result in death. HINT Indicates information, notes, WARNING Description of hazard and or tips for improving your suc- possible resulting injures or cess using the tool. -

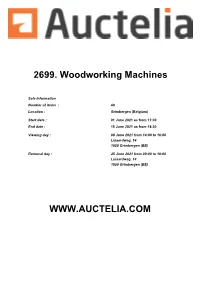

2699. Woodworking Machines

2699. Woodworking Machines Sale Information Number of items : 40 Location : Grimbergen (Belgium) Start date : 01 June 2021 as from 17:00 End date : 15 June 2021 as from 18:30 Viewing day : 08 June 2021 from 14:00 to 16:00 Luiaardweg, 14 1850 Grimbergen (BE) Removal day : 25 June 2021 from 09:00 to 16:00 Luiaardweg, 14 1850 Grimbergen (BE) WWW.AUCTELIA.COM The General Terms and Conditions and the Specific conditions of sale apply to this online Auction SPECIFIC CONDITIONS - 2699. Woodworking Machines START DATE 01 June 2021 as from 17:00 END DATE 15 June 2021 as from 18:30 VIEWING 08 June 2021 from 14:00 to 16:00 Luiaardweg, 14 1850 Grimbergen (BE) REMOVAL 25 June 2021 from 09:00 to 16:00 Luiaardweg, 14 1850 Grimbergen (BE) In order to be able to pick up the Lots, the total amount due has to be paid. The Lots can only be removed if the Buyer shows on the removal day the proforma invoice and signs the delivery note. WARNING: The Buyer is fully responsible for the dismantling, loading and transportation of the bought Lots. WARNING: If Buyers do not collect their goods at the removal date, time and address mentioned above, extra storage and transport costs will be charged. AUCTION FEES Auction Fees (based on Final Selling Price per Piece) - Amounts less than €15,000 17% of the final selling price - Amounts more than €15,000 12% of the final selling price VAT 0.00 % on the highest bid and/or accepted by the Seller and on the Auction fees PAYMENT Within 3 business days of reception by e-mail of the proforma invoice, the Buyer must transfer the total amount due to the bank account below and mention the invoice number: Auctelia ING 363-4520918-79 / IBAN : BE58 3634 5209 1879 / BIC BBRUBEBB BNPPF 035-7704702-33 / IBAN : BE79 0357 7047 0233 / BIC : GEBABEBB ORGANIZER AUCTELIA Rue Emile Francqui 6/3 B-1435 Mont-Saint-Guibert, Belgique, 6 1435 Mont-Saint-Guibert (BE) SUPERVISION EXTENSION OF If there is at least one Bid within the last 5 minutes of a sale, the closing time is extended by 5 minutes until there is no more ONLINE AUCTION Bid. -

Glass Beer Bottle Reuse in Bulgaria

Glass beer bottle reuse in Bulgaria Kameliya Krumova Environmental Management and Sustainability Science Master Thesis June 2016 Introduction This study has been carried out individually in at the 4th semester of the Master Program Environmental Management and Sustainability Science at Aalborg University. The study has been conducted in Bulgaria between February and May 2016. The subject of this research was suggested by Margarita Georgieva, an ecology expert in Ecology department from Stara Zagora Municipality, Bulgaria. I have been on a three month internship at the Ecology department in Stara Zagora Municipality in the 3rd semester of this Master Program. In the last decades increase in the world’s population results in higher need for food and therefore increase in generation of packaging waste like bottles and boxes (Gómez, et al., 2009). The packaging material could have a significant impact on the environment (Meneses, et al., 2012) (Del Borghi, et al., 2014). Moreover the choice of packaging material could lead to impact on the whole beverage value chain (Simon, et al., 2016). Waste management could become a challenge in fast growing cities (Gómez, et al., 2009). Reuse of packaging should be considered before any other waste treatment, placed under ‘reuse’ in the waste hierarchy pyramid (Babader, et al., 2016) (WRAP, 2011). Although reuse is the easiest way to reduce waste, it has not been a common focus in studies (Babader, et al., 2016). One of the packaging, glass, could be easily reused due to its qualities (Brewers Association, 2014) (INFORM, 2012) (FEVE, n.d.) A common way in Western Europe (Denmark, Sweden, Germany) to reuse glass bottle packaging is through deposit system on beverage plastic, cans and glass bottles including water, beer, siders, non-alcoholic drinks (Zero Waste Europe, 2010).