NOIC-2020-Transcripts Final.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hamilton at the Paramount Seattle

SPECIAL EDITION • FEBRUARY 2018 ENCORE ARTS PROGRAMS • SPECIAL EDITION HAMILTON FEBRUARY 2018 FEBRUARY PROGRAMS • SPECIAL EDITION HAMILTON ARTS ENCORE HAMILTON February 6 – March 18, 2018 Cyan Magenta Yellow Black Inks Used: 1/10/18 12:56 PM 1/11/18 11:27 AM Changes Prev AS-IS Changes See OK OK with Needs INITIALS None Carole Guizetti — Joi Catlett Joi None Kristine/Ethan June Ashley Nelu Wijesinghe Nelu Vivian Che Barbara Longo Barbara Proofreader: Regulatory: CBM Lead: Prepress: Print Buyer: Copywriter: CBM: · · · · Visual Pres: Producer: Creative Mgr Promo: Designer: Creative Mgr Lobby: None None 100% A N N U A L UPC: Dieline: RD Print Scale: 1-9-2018 12:44 PM 12:44 1-9-2018 D e si gn Galle r PD y F Date: None © 2018 Starbucks Co ee Company. All rights reserved. All rights reserved. ee Company. SBX18-332343 © 2018 Starbucks Co x 11.125" 8.625" Tickets at stgpresents.org SKU #: Bleed: SBUX FTP Email 12/15/2017 STARBUCKS 23 None 100% OF TICKET SALES GOOF TOTHE THE PARTICIPATING MUSIC PROGRAMS HIGH SCHOOL BANDS — FRIDAY, MARCH 30 AT 7PM SBX18-332343 HJCJ Encore Ad Encore HJCJ blongo014900 SBX18-332343 HotJavaCoolJazz EncoreAd.indd HotJavaCoolJazz SBX18-332343 None RELEASED 1-9-2018 Hot Java Cool Jazz None None None x 10.875" 8.375" D i sk SCI File Cabinet O t h e r LIVE AT THE PARAMOUNT IMPORTANT NOTES: IMPORTANT Vendor: Part #: Trim: Job Number: Layout: Job Name: Promo: File Name: Proj Spec: Printed by: Project: RELEASE BEFORE: BALLARD | GARFIELD | MOUNTLAKE TERRACE | MOUNT SI | ROOSEVELT COMPANY Seattle, 98134 WA 2401 Utah Avenue South2401 -

Movie-Going on the Margins: the Mascioli Film Circuit of Northeastern Ontario

Movie-Going on the Margins: The Mascioli Film Circuit of Northeastern Ontario A DISSERTATION SUBMITTED TO THE FACULTY OF GRADUATE STUDIES IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY JESSICA LEONORA WHITEHEAD GRADUATE PROGRAM IN COMMUNICATION AND CULTURE YORK UNIVERSITY TORONTO, ONTARIO February 2018 © Jessica Leonora Whitehead 2018 ii Abstract Northeastern Ontario film exhibitor Leo Mascioli was described as a picture pioneer, a business visionary, “the boss of the Italians,” a strikebreaker and even an “enemy alien” by the federal government of Canada. Despite these various descriptors, his lasting legacy is as the person who brought entertainment to the region’s gold camps and built a movie theatre chain throughout the mining and resource communities of the area. The Porcupine Gold Rush—the longest sustained gold rush in North America—started in 1909, and one year later Mascioli began showing films in the back of his general store. Mascioli first came to the Porcupine Gold Camp as an agent for the mining companies in recruiting Italian labourers. He diversified his business interests by building hotels to house the workers, a general store to feed them, and finally theatres to entertain them. The Mascioli theatre chain, Northern Empire, was headquartered in Timmins and grew to include theatres from Kapuskasing to North Bay. His Italian connections, however, left him exposed to changes in world politics; he was arrested in 1940 and sent to an internment camp for enemy aliens during World War II. This dissertation examines cinema history from a local perspective. The cultural significance of the Northern Empire chain emerges from tracing its business history, from make-shift theatres to movie palaces, and the chain’s integration into the Hollywood-linked Famous Players Canadian national circuit. -

Fairbanks Field Hearing Chairman Lisa Murkowski March 28, 2016

Opening Statement: Fairbanks Field Hearing Chairman Lisa Murkowski March 28, 2016 Good afternoon, everyone, and Happy Seward’s Day. I am delighted to call this Field Hearing to order in our Golden Heart city of Fairbanks. I want to start by thanking the Pipeline Training Center for hosting us. And I want to welcome our witnesses and all who have joined us for this important discussion about resource development in Alaska. As many of you likely know, it was gold mining that ultimately determined the location of Fairbanks. Captain Barnette’s riverboat ran out of draft on the Chena, and fate determined where his mining supply business was to be located. And while Barnette was too late and too far away to profit from the Klondike gold rush, he helped create the Fairbanks gold rush. Today, Fort Knox and Pogo, world-class gold mines north and south of the city, continue the proud tradition that give meaning to Fairbanks’ motto. This region – like so much of our state – is blessed with vast natural resources that we can use to gain prosperity and fulfill the promises of our statehood. Today is Seward’s Day, we can laugh about Seward’s Ice Box or Seward’s Folly, but not even Seward could conceive of the resource wealth the U.S. purchased from Russia. Alaska has what virtually no one else has: tens of billions of barrels of oil, hundreds of trillions of cubic feet of natural gas, a massive supply of coal, and countless deposits of hardrock minerals. Of course renewable resources beyond imagination. -

World Affairs Summer 2020 (April – June) Vol 24 No 2 1 2 World Affairs Summer 2020 (April – June) Vol 24 No 2 World Affairs International Advisory Board

W ORLD AFFAIRS VOLUME TWENTY FOUR • NUMBER TWO SUMMER 2020 (APRIL-JUNE) The Journal of International Issues of International The Journal DECLINE, CRISIS AND RESET THE ONGOING TRANSITION SUDHANSHU TRIPATHI RAVI PRATAP SINGH SHAHZADA RAHIM ANDREY VOLODIN PAOLO RAIMONDI EVOLVING SOCIAL AND REGIONAL SYMPTOMS APRIL-JUNE 2020 VOL 24 NO 2 VOL APRIL-JUNE 2020 TAYE DEMISSIE BESHI AND RANVINDERJIT KAUR KANIKA SANSANWAL AND RAHUL KAMATH SANCHITA BHATTACHARYA SUYASH CHANDAK “The world is the great gymnasium where we come to make ourselves strong.” – Swami Vivekananda Quintessence Fragrances Limited, headquartered in UK with manufacturing in UK, India, Hong Kong & China. Creation centres in Newhaven and Mumbai, creating innovative sensory experiences. Specialists in fine fragrances, soaps, toiletries and air care. Clients in 25 countries. Quintessence Fragrances Ltd Unit 2A, Hawthorn Industrial Estate, Avis Way, Newhaven East Sussex BN9 0DJ, United Kingdom Tel.: +44 (0) 1273 519000, Mobile: +44 (0) 7711 007318 Website: www.quintessencefragrances.com Quintessence Fragrances Pvt. Ltd A-31, Phase 1, MEPZ-SEZ, Special Economic Zone, Tambaram, Chennai - 600045 Tel.: 091 44 22622325, Fax: +91 44 22622327 Quintessence Fragrances Ltd 1/17, Prabhadevi Industrial Estate, 402 Veer Savarkar Marg, Prabhadevi, Mumbai 400025 Tel: 91 22 66225959/24314806, Fax 91 22 24367031 URL: www.goldfieldfragrances.com, Email: [email protected] WORLD AFFAIRS The Journal of International Issues SUMMER (APRIL-JUNE) 2020 PUBLISHER CHANDA SINGH EDITOR CHANDA SINGH CONSULTING -

NOAA Parcel G Relinquishment Environmental Assessment (EA) DOI-BLM-AK-F020-2017-0016 Serial Number F-025943

United States Department of the Interior Bureau of Land Management Eastern Interior Field Office 222 University Avenue Fairbanks, AK 99709 Phone: 907-474-2200 NOAA Parcel G Relinquishment Environmental Assessment (EA) DOI-BLM-AK-F020-2017-0016 Serial Number F-025943 July 26, 2017 This Page is Intentionally Left Blank Table of Contents 1.0 INTRODUCTION AND BACKGROUND ..................................................................5 1.1 PURPOSE AND NEED FOR THE PROPOSED ACTION...................................... 6 1.2 DECISION TO BE MADE ........................................................................................ 6 1.3 CONFORMANCE WITH BLM MANAGEMENT PLAN(S).................................. 6 1.4 CONSISTENCY WITH LAWS, REGULATIONS, AND POLICIES ..................... 7 1.5 SCOPING AND IDENTIFICATION OF ISSUES ................................................... 8 2.0 PROPOSED ACTION AND ALTERNATIVES ........................................................11 2.1 Alternative A: Proposed Action ............................................................................... 11 2.2 Alternative B: No Action Alternative ...................................................................... 11 2.3 Alternatives Considered but Eliminated From Detailed Analysis ........................... 12 3.0 AFFECTED ENVIRONMENT and ENVIRONMENTAL CONSEQUENCES ........12 3.1 Realty and Land Status ............................................................................................ 13 3.2 Vegetation ............................................................................................................... -

Worldpeaceoneaçom

A D V E R T I S E M E N T ito EXPERIENCE THE BUZZ FEB 9 _ - ----.. wor .. ' hRD:llwww.worWpeaceorle.coml--. yrniMall. 1A.4 . taunt NaaN1eM m ._ .. .. .. fall yew -Magness on_.. .Mar Vector ... eeay yahoo, V/orld ® old boo... Newr Apple Apppe. 1Sa1- Peace ^ q - . .. PIRChif... AAmazor, - - - -- q GVer S.- 1G Cuogle ... O S1T1( ' Direcur.._ fashM (a leanvau cena WORLD PEACE ® Worla. A ONE - TEN TEN YEAR GLOBAL PEACE INITIATIVE rF;f!L 10 ANNUAL CLOUM. CONC,F.Ftr OROAOCASTS 10 ANNUAL WORLD PEACE SYMPOSIA 10 OLOLAE AMUASSAOOR GENERALS Portugal issues CLAES NOBEL First WPI Joins World Peace One cad more Stamp and Race Artivist DOUG 1VANOV{CN Eiletime Award WP1's Founder and Executive see vedee. Producer tens us why humanity must barn, an end to war, before war brings an end b humanity. , CHINA GOVERNMENT COMMITS tc TO WORLD PEACE ONE CONCERT ligillillrrllr.s``.111 NAM UNVEILS- 1 - YEAR PORTUGAL JOINS .GLBALINITtATIVE WORLD PEACE ONE CONCERT PEACE TALKS Pateec Swayze Cheftrna Applegate Brian McKnight Taylor Dane ONE UiarY P00111 O.elbìYSa bald IMPS IfaaRei Pews Award Welcome co WPt 000P0«'O www.billboard.com www.billboard.biz US $6.99 CAN $8.99 UK £5.50 WorldPeaceOneaçom k I3XNCTCC SCH 3 -DIGIT 907 913L24080439 MAR08 REG A04 000 /004 $6.99US $8 99CAN 06> I IIlu liii ilIIIIIIiiiIiiiIiiIIiiIIIIIIIllliIilllllll MONTY GREENLY 0028 3740 ELM AVE t A LONG BEACH CA 90807 -3402 001164 i i o 89 47205 9 World Peace One invites you to launch a World Movement whose intent is nothing less than to secure the future of the entire Human Race. -

Symbol Company Market Maker Market Maker Type Effective Date ACB AURORA CANNABIS INC. Canaccord Genuity Corp. (#033) Full 12/13/2016 ASO AVESORO RESOURCES INC

Symbol Company Market Maker Market Maker Type Effective Date ACB AURORA CANNABIS INC. Canaccord Genuity Corp. (#033) Full 12/13/2016 ASO AVESORO RESOURCES INC. J Canaccord Genuity Corp. (#033) Full 12/13/2016 CNL CONTINENTAL GOLD INC. J Canaccord Genuity Corp. (#033) Full 12/13/2016 ECN ECN CAPITAL CORP. Canaccord Genuity Corp. (#033) Full 12/13/2016 FF FIRST MINING FINANCE CORP. Canaccord Genuity Corp. (#033) Full 12/13/2016 GCM GRAN COLOMBIA GOLD CORP. J Canaccord Genuity Corp. (#033) Full 12/13/2016 LAC LITHIUM AMERICAS CORP. J Canaccord Genuity Corp. (#033) Full 12/13/2016 LUC LUCARA DIAMOND CORP. J Canaccord Genuity Corp. (#033) Full 12/13/2016 NYX NYX GAMING GROUP LIMITED Canaccord Genuity Corp. (#033) Full 12/13/2016 SWY STORNOWAY DIAMOND CORPORATION J Canaccord Genuity Corp. (#033) Full 12/13/2016 USA AMERICAS SILVER CORPORATION J Canaccord Genuity Corp. (#033) Full 12/13/2016 WEED CANOPY GROWTH CORPORATION J Canaccord Genuity Corp. (#033) Full 12/13/2016 XRE ISHARES S&P/TSX CAPPED REIT INDEX ETF UN Canaccord Genuity Corp. (#033) Full 12/13/2016 CCX CANADIAN CRUDE OIL INDEX ETF CL 'A' UN CIBC World Markets Inc. (#079) Full 6/13/2017 CGL ISHARES GOLD BULLION ETF HEDGED UNITS CIBC World Markets Inc. (#079) Full 6/13/2017 CIC FIRST ASSET CANBANC INCOME CLASS ETF CIBC World Markets Inc. (#079) Full 6/13/2017 CMR ISHARES PREMIUM MONEY MARKET ETF UNITS CIBC World Markets Inc. (#079) Full 6/13/2017 DXM 1ST ASST MORNSTAR CDA DIV TARGET 30IDX ETF UN CIBC World Markets Inc. -

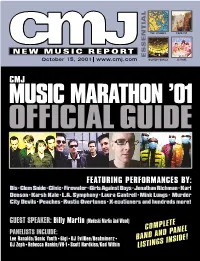

Complete Band and Panel Listings Inside!

THE STROKES FOUR TET NEW MUSIC REPORT ESSENTIAL October 15, 2001 www.cmj.com DILATED PEOPLES LE TIGRE CMJ MUSIC MARATHON ’01 OFFICIALGUIDE FEATURING PERFORMANCES BY: Bis•Clem Snide•Clinic•Firewater•Girls Against Boys•Jonathan Richman•Karl Denson•Karsh Kale•L.A. Symphony•Laura Cantrell•Mink Lungs• Murder City Devils•Peaches•Rustic Overtones•X-ecutioners and hundreds more! GUEST SPEAKER: Billy Martin (Medeski Martin And Wood) COMPLETE D PANEL PANELISTS INCLUDE: BAND AN Lee Ranaldo/Sonic Youth•Gigi•DJ EvilDee/Beatminerz• GS INSIDE! DJ Zeph•Rebecca Rankin/VH-1•Scott Hardkiss/God Within LISTIN ININ STORESSTORES TUESDAY,TUESDAY, SEPTEMBERSEPTEMBER 4.4. SYSTEM OF A DOWN AND SLIPKNOT CO-HEADLINING “THE PLEDGE OF ALLEGIANCE TOUR” BEGINNING SEPTEMBER 14, 2001 SEE WEBSITE FOR DETAILS CONTACT: STEVE THEO COLUMBIA RECORDS 212-833-7329 [email protected] PRODUCED BY RICK RUBIN AND DARON MALAKIAN CO-PRODUCED BY SERJ TANKIAN MANAGEMENT: VELVET HAMMER MANAGEMENT, DAVID BENVENISTE "COLUMBIA" AND W REG. U.S. PAT. & TM. OFF. MARCA REGISTRADA./Ꭿ 2001 SONY MUSIC ENTERTAINMENT INC./ Ꭿ 2001 THE AMERICAN RECORDING COMPANY, LLC. WWW.SYSTEMOFADOWN.COM 10/15/2001 Issue 735 • Vol 69 • No 5 CMJ MUSIC MARATHON 2001 39 Festival Guide Thousands of music professionals, artists and fans converge on New York City every year for CMJ Music Marathon to celebrate today's music and chart its future. In addition to keynote speaker Billy Martin and an exhibition area with a live performance stage, the event features dozens of panels covering topics affecting all corners of the music industry. Here’s our complete guide to all the convention’s featured events, including College Day, listings of panels by 24 topic, day and nighttime performances, guest speakers, exhibitors, Filmfest screenings, hotel and subway maps, venue listings, band descriptions — everything you need to make the most of your time in the Big Apple. -

Promise Beheld and the Limits of Place

Promise Beheld and the Limits of Place A Historic Resource Study of Carlsbad Caverns and Guadalupe Mountains National Parks and the Surrounding Areas By Hal K. Rothman Daniel Holder, Research Associate National Park Service, Southwest Regional Office Series Number Acknowledgments This book would not be possible without the full cooperation of the men and women working for the National Park Service, starting with the superintendents of the two parks, Frank Deckert at Carlsbad Caverns National Park and Larry Henderson at Guadalupe Mountains National Park. One of the true joys of writing about the park system is meeting the professionals who interpret, protect and preserve the nation’s treasures. Just as important are the librarians, archivists and researchers who assisted us at libraries in several states. There are too many to mention individuals, so all we can say is thank you to all those people who guided us through the catalogs, pulled books and documents for us, and filed them back away after we left. One individual who deserves special mention is Jed Howard of Carlsbad, who provided local insight into the area’s national parks. Through his position with the Southeastern New Mexico Historical Society, he supplied many of the photographs in this book. We sincerely appreciate all of his help. And finally, this book is the product of many sacrifices on the part of our families. This book is dedicated to LauraLee and Lucille, who gave us the time to write it, and Talia, Brent, and Megan, who provide the reasons for writing. Hal Rothman Dan Holder September 1998 i Executive Summary Located on the great Permian Uplift, the Guadalupe Mountains and Carlsbad Caverns national parks area is rich in prehistory and history. -

4Th Quarter, 2008•Pages 60–84

www.AlaskaPhilatelic.org Volume 44, No. 4 • Whole No. 228 4th Quarter, 2008 • Pages 60–84 AK 50th Anniversary Cancels ..................................................................................page 61 Want Ads ................................................................................................................page 62 President’s Message ..................................................................................................page 63 Secretary/Treasurer’s Report .....................................................................................page 63 Sustaining Member Cover .......................................................................................page 64 Unreported Cancels ......................................................................................... pages 65, 68 The Journal of the Alaska Collectors Club • American Philatelic Society Affiliate No. 218 Affiliate No. American Philatelic Society Alaska Collectors Club • of the The Journal King Salmon AFB ...................................................................................................page 66 Member Request .....................................................................................................page 67 50th Anniversary Stamp Artwork Revealed .............................................................page 68 Klondike EKU or Something More Mysterious? .....................................................page 69 Gold Nuggets ................................................................................................. -

OSC Bulletin

The Ontario Securities Commission OSC Bulletin September 15, 2016 Volume 39, Issue 37 (2016), 39 OSCB The Ontario Securities Commission administers the Securities Act of Ontario (R.S.O. 1990, c. S.5) and the Commodity Futures Act of Ontario (R.S.O. 1990, c. C.20) The Ontario Securities Commission Published under the authority of the Commission by: Cadillac Fairview Tower Thomson Reuters 22nd Floor, Box 55 One Corporate Plaza 20 Queen Street West 2075 Kennedy Road Toronto, Ontario Toronto, Ontario M5H 3S8 M1T 3V4 416-593-8314 or Toll Free 1-877-785-1555 416-609-3800 or 1-800-387-5164 Contact Centre – Inquiries, Complaints: Fax: 416-593-8122 TTY: 1-866-827-1295 Office of the Secretary: Fax: 416-593-2318 The OSC Bulletin is published weekly by Thomson Reuters Canada, under the authority of the Ontario Securities Commission. Subscriptions to the print Bulletin are available from Thomson Reuters Canada at the price of $868 per year. The eTable of Contents is available from $148 to $155. The CD-ROM is available from $1392 to $1489 and $314 to $336 for additional disks. Subscription prices include first class postage to Canadian addresses. Outside Canada, the following shipping costs apply on a current subscription: 440 grams US – $5.41 Foreign – $18.50 860 grams US – $6.61 Foreign – $10.60 1140 grams US – $7.64 Foreign – $14.70 Single issues of the printed Bulletin are available at $20 per copy as long as supplies are available. Thomson Reuters Canada also offers every issue of the Bulletin, from 1994 onwards, fully searchable on SecuritiesSource™, Canada’s pre-eminent web-based securities resource. -

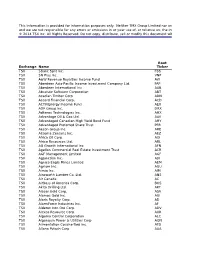

This Information Is Provided for Information Purposes Only. Neither

This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies represents, warrants or guarantees the accuracy or completeness of the information contained in this document and we are not responsible for any errors or omissions in or your use of, or reliance on, the information provided. © 2014 TSX Inc. All Rights Reserved. Do not copy, distribute, sell or modify this document without TSX Inc.'s prior written consent. Root Exchange Name Ticker TSX 5Banc Split Inc. FBS TSX 5N Plus Inc. VNP TSX A&W Revenue Royalties Income Fund AW TSX Aberdeen Asia-Pacific Income Investment Company Ltd. FAP TSX Aberdeen International Inc. AAB TSX Absolute Software Corporation ABT TSX Acadian Timber Corp ADN TSX Accord Financial Corp. ACD TSX ACTIVEnergy Income Fund AEU TSX ADF Group Inc. DRX TSX Adherex Technologies Inc. AHX TSX Advantage Oil & Gas Ltd. AAV TSX Advantaged Canadian High Yield Bond Fund AHY TSX Advantaged Preferred Share Trust PFR TSX Aecon Group Inc. ARE TSX AEterna Zentaris Inc. AEZ TSX Africa Oil Corp. AOI TSX Africo Resources Ltd. ARL TSX AG Growth International Inc AFN TSX Agellan Commercial Real Estate Investment Trust ACR TSX AGF Management Limited AGF TSX AgJunction Inc. AJX TSX Agnico Eagle Mines Limited AEM TSX Agrium Inc. AGU TSX Aimia Inc. AIM TSX Ainsworth Lumber Co. Ltd. ANS TSX Air Canada AC TSX AirBoss of America Corp. BOS TSX Akita Drilling Ltd. AKT TSX Alacer Gold Corp. ASR TSX Alamos Gold Inc. AGI TSX Alaris Royalty Corp. AD TSX AlarmForce Industries Inc. AF TSX Alderon Iron Ore Corp.