Economic Impact Analysis for the Nitric Acid Manufacturing NSPS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NITROGEN by Raymond L

NITROGEN By Raymond L. Cantrell In 1994, nitrogen compound supplies in the second in discharges to surface water, and third per-year ammonia plant based on methane gas United States reached an all time record high in terms of the largest emissions to the air. feedstock derived from lignite. A used because of strong domestic demand for Ammonium nitrate solution, nitric acid, ammonia plant was to be moved from Freeport- agricultural and industrial products; an acetonitrile, and ammonium sulfate solution McMoRan's idle Fort Madison, IA, facility. extremely tight supply situation was were also listed in the top 50 TRI releases, in Total ammonia capacity, including that already experienced. The total value of the U.S. order of importance.6 onsite, should approximate 310,000 tons per nitrogen compound supply, f.o.b. U.S. Gulf, year. The first flue gas desulfurization unit nearly doubled to an impressive $5.0 billion, Production based on ammoniation of sulfur dioxide to compared with $2.7 billion during the previous produce salable ammonium sulfate, was to be year. U.S. ammonia producers operated at more constructed using General Electric A unique combination of strong upward than 100% of design capacity in 1994. Environmental Systems' Inc. technology. The movement in the domestic nitrogen market led Ammonia ranked as the sixth largest volume unit was designed to produce 180,000 tons per to several new all time record highs, including chemical produced in the United States, year of salable ammonium sulfate, to be nitrogen fertilizer consumption1 and agricultural according to information published by Chemical marketed under contract by H. -

2010 Minerals Yearbook

2010 Minerals Yearbook EXPLOSIVES U.S. Department of the Interior October 2012 U.S. Geological Survey EXPLOSIVES By Lori E. Apodaca In 2010, U.S. explosives consumption was 2.68 million metric Vet’s Explosives Inc. tons (Mt), about an 18% increase from that of 2009; sales of Viking Explosives and Supply Inc. explosives were reported in all States except Delaware. Coal W.A. Murphy, Inc. mining, with about 71% of total consumption, continued to be El Dorado Chemical Co. (a subsidiary of LSB Industries Inc.) the dominant use for explosives in the United States. Wyoming, signed a 5-year agreement with Orica International Pte Ltd. West Virginia, and Kentucky, in descending order, led the (Orica) to supply Orica with 230,000 metric tons per year (t/yr) Nation in coal production, accounting for 63% of the total. of industrial-grade ammonium nitrate. The new agreement These States were also the leading explosives-consuming States, replaces the previous agreement to supply 190,000 t/yr of accounting for 46% of total U.S. explosives sales. ammonium nitrate to Orica (Green Markets, 2010b). Apache Nitrogen Products Inc. was investing $5.5 million to Legislation and Government Programs upgrade its Arizona ammonium nitrate prill plant. They were replacing the dry end of the prill ammonium nitrate process Effective February 3, the Occupational Safety and Health in order to reduce moisture problems. Sixty percent of the Administration (OSHA) terminated the rulemaking that had liquid ammonium nitrate produced onsite was used to produce been proposed in 2007 to amend its Explosives and Blasting low-density ammonium nitrate prill for use in the mining Agents Standard (CFR 1910.109). -

2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

Case 4:20-cv-00463-BGM Document 1 Filed 10/28/20 Page 1 of 20 1 Ellen M. Mahan Deputy Section Chief 2 Deborah A. Gitin 3 Senior Counsel Environmental Enforcement Section 4 Environment and Natural Resources Division U.S. Department of Justice 5 450 Golden Gate Avenue, Room 7-6714 6 San Francisco, California 94102 (CA Bar # 284947) 7 Telephone: (415) 744-6488 Facsimile: (415) 744-6476 8 Email: [email protected] 9 Attorneys for the United States of America 10 11 IN THE UNITED STATES DISTRICT COURT 12 FOR THE DISTRICT OF ARIZONA 13 United States of America, 14 15 Plaintiff, 16 v. COMPLAINT 17 Apache Nitrogen Products, Inc., an Arizona 18 corporation, 19 Defendant. 20 21 22 23 24 25 26 27 28 1 COMPLAINT United States of America v. Apache Nitrogen Products, Inc. (D. Ariz.) Case 4:20-cv-00463-BGM Document 1 Filed 10/28/20 Page 2 of 20 1 Plaintiff, the United States of America (“United States”), by the authority of the 2 Attorney General, through its undersigned attorneys, and at the request of the 3 Administrator of the United States Environmental Protection Agency (“EPA”), hereby 4 alleges: 5 I. PRELIMINARY STATEMENT 6 1. This is a civil action for penalties and injunctive relief brought pursuant to 7 Section 113(b)(2) of the Clean Air Act (“CAA”), 42 U.S.C. § 7413(b)(2); Section 325 of 8 the Emergency Planning and Community Right-to-Know Act (“EPCRA”), 42 U.S.C. 9 § 11045; and Section 109(c) of the Comprehensive Environmental Response, 10 Compensation and Liability Act (“CERCLA”), 42 U.S.C. -

Evelyn Muir V. Apache Nitrogen Products and W.H. Burt Explosives V

Brigham Young University Law School BYU Law Digital Commons Utah Court of Appeals Briefs 1994 Evelyn Muir v. Apache Nitrogen Products and W.H. Burt Explosives v. Douglas Bailey : Brief of Respondent Utah Court of Appeals Follow this and additional works at: https://digitalcommons.law.byu.edu/byu_ca1 Part of the Law Commons Original Brief Submitted to the Utah Court of Appeals; digitized by the Howard W. Hunter Law Library, J. Reuben Clark Law School, Brigham Young University, Provo, Utah; machine-generated OCR, may contain errors. Robert H. Copier; attorney for appellant. Shawn E. Draney, Roger P. Christensen, Stacey L. Hayden; Christensen and Jensen; attorneys for appellee. Recommended Citation Brief of Respondent, Muir v. Apache, No. 940553 (Utah Court of Appeals, 1994). https://digitalcommons.law.byu.edu/byu_ca1/6198 This Brief of Respondent is brought to you for free and open access by BYU Law Digital Commons. It has been accepted for inclusion in Utah Court of Appeals Briefs by an authorized administrator of BYU Law Digital Commons. Policies regarding these Utah briefs are available at http://digitalcommons.law.byu.edu/utah_court_briefs/policies.html. Please contact the Repository Manager at [email protected] with questions or feedback. UTAH COURT OP APPEALS BB1EE IN THE UTAH CCBJgjj&jflgftLB KFU EVELYN MUIR, )A10 Plaintiff and Appellant, DC G<!(\ZX?>CA v. APACHE NITROGEN PRODUCTS Appeal No. 94 0553-|fc and W.H. BURT EXPLOSIVES, Priority No. 15 Defendants and Appellees, |v. DOUGLAS BAILEY, Third Party Defendant. APPEAL FROM DIRECTED VERDICT ENTERED IN THE SEVENTH JUDICIAL DISTRICT COURT OF GRAND COUNTY The Honorable Lyle R. -

Case 4:20-Cv-00463-BGM Document 3-1 Filed 10/28/20 Page 1 of 63

Case 4:20-cv-00463-BGM Document 3-1 Filed 10/28/20 Page 1 of 63 1 Ellen M. Mahan 2 Deputy Section Chief Deborah A. Gitin 3 Senior Counsel 4 Environmental Enforcement Section Environment and Natural Resources Division 5 U.S. Department of Justice 6 450 Golden Gate Ave., Room 7-6714 San Francisco, California 94102 7 (CA Bar No. 284947) Telephone: (415) 744-6488 8 Facsimile: (415) 744-6476 9 Email: [email protected] 10 Attorneys for the United States of America 11 12 (names of additional counsel on following page) 13 IN THE UNITED STATES DISTRICT COURT 14 FOR THE DISTRICT OF ARIZONA 15 16 United States of America, Case No. CV-20-00463-TUC-BGM 17 18 Plaintiff, 19 CONSENT DECREE 20 v. 21 22 Apache Nitrogen Products, Inc., an Arizona corporation, 23 24 Defendant. 25 26 27 28 Case 4:20-cv-00463-BGM Document 3-1 Filed 10/28/20 Page 2 of 63 1 Chris S. Leason Gallagher & Kennedy, PA 2 2575 East Camelback Road 3 Suite 1100 Phoenix, AZ 85016 4 (AZ Bar No. 021887) 5 Telephone: (602) 530-8000 Facsimile: (602) 530-8500 6 Email: [email protected] 7 Attorney for Apache Nitrogen Products, Inc. 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 ii Case 4:20-cv-00463-BGM Document 3-1 Filed 10/28/20 Page 3 of 63 1 2 TABLE OF CONTENTS 3 4 I. BACKGROUND .................................................................................................1 5 II. JURISDICTION AND VENUE ..........................................................................3 6 III. -

Apache Powder Put the Boom in Arizona Mining

Apache Powder put the boom in Arizona mining • By William Ascarza For the Arizona Daily Star • Jun 12, 2016 One of the great technical breakthroughs in late 19th century mining occurred with the introduction of nitroglycerin, a colorless, earth-shattering liquid used initially in quarrying. Nitro, a high explosive five times as powerful as black powder, was known for its volatile characteristics. These were attributed to its speed of decomposition, making it less desirable and unsafe because of its ability to become unstable through the slightest jolt or friction. Swedish chemist Alfred Nobel tamed the instability of nitro by adding it to inert fillers — including sawdust — giving it the appearance of a fat paper candle he christened dynamite. A pinch of fulminate of mercury or another supersensitive explosive was added at the base to instigate the shock necessary for detonation. There was also the ability to alter the nitroglycerin percentage to compensate for the strength of the rock to be blasted. Ease of handling made dynamite the preferred choice among miners to move more rock with more precision and with less expense and time. The Apache Powder Co. was incorporated on June 11, 1920, by a conglomerate of mining companies in the Southwest as a means of decreasing the excessive market price of explosives. The company became the largest single plant for the manufacture of dynamite in the United States. Located near St. David, the company was heavily involved in supplying explosives to the mining industry. The extensive operation grew to 140 buildings on more than 700 acres, employing several hundred people and making it one of the largest employers in Southern Arizona. -

8 ELLEN M. MAHAN Deputy Section Chief Environmental Enforcement

Case 4:17-cv-00612-RCC Document 3 Filed 12/20/17 Page 1 of 62 1 ELLEN M. MAHAN 2 i Deputy Section Chief Environmental Enforcement Section 3 Environment and Natural Resources Division 4 U.S. Department of Justice AMES R. MacAYEAL (D.C. Bar # 474664) 5 J Senior Counsel 6 Environmental Enforcement Section United States Department of Justice, P.O. Box 7611 Washington, D.C. 20044-7611 a j amie.macayeal@usdoj. gov 9 ELIZABETH A. STRANGE io Acting United States Attorney ~~ JANET K. MARTIN(AZ BAR # 6014) is Civil Chief District Arizona 13 405 W. Congress Street, Suite 4800 14 Tucson, AZ 85701-5040 (520)620-7300 15 j [email protected] 16 ~~ Attorneys for Plaintiff United States of America is IN THE UNITED STATES DISTRICT COURT 19 FOR THE DISTRICT OF ARIZONA ao al UNITED STATES OF AMERICA, as Plaintiff, 23 Action No. 24 Civil 25 CONSENT DECREE (Proposed) 26 APACHE NITROGEN PRODUCTS, ; ~C.~ 27 ~8 Defendant. Case 4:17-cv-00612-RCC Document 3 Filed 12/20/17 Page 2 of 62 1 2 TABLE OF CONTENTS 3 I. JURISDICTION AND VENiJE .......................................................6 4 II. DEFINITIONS .................................................................................7 5 III. INJUNCTIVE RELIEF ..................................................................12 6 IV. CIVIL PENALTY ..........................................................................14 V. PERIODIC REPORTING ..............................................................15 s VI. REVIEW OF SUBMITTALS ........................................................16 9 VII. STIPULATED -

Federal Register/Vol. 82, No. 248/Thursday

61590 Federal Register / Vol. 82, No. 248 / Thursday, December 28, 2017 / Notices Liquid nitrated polyol and Potassium chlorate and lead sulfocyanate Water-bearing explosives having salts of trimethylolethane. explosive. oxidizing acids and nitrogen bases, sulfates, Liquid oxygen explosives. Potassium nitrate explosive mixtures. or sulfamates (cap sensitive). M Potassium nitroaminotetrazole. Water-in-oil emulsion explosive Magnesium ophorite explosives. Pyrotechnic compositions. compositions. Mannitol hexanitrate. Pyrotechnic fuses. X MDNP [methyl 4,4-dinitropentanoate]. PYX [2,6-bis(picrylamino)] 3,5- Xanthomonas hydrophilic colloid MEAN [monoethanolamine nitrate]. dinitropyridine. explosive mixture. Mercuric fulminate. R Mercury oxalate. RDX [cyclonite, hexogen, T4, cyclo-1,3,5,- Thomas E. Brandon, Mercury tartrate. trimethylene-2,4,6,-trinitramine; hexahydro- Deputy Director. Metriol trinitrate. 1,3,5-trinitro-S-triazine]. Minol-2 [40% TNT, 40% ammonium S [FR Doc. 2017–28010 Filed 12–27–17; 8:45 am] nitrate, 20% aluminum]. Safety fuse. BILLING CODE 4410–FY–P MMAN [monomethylamine nitrate]; Salts of organic amino sulfonic acid methylamine nitrate. explosive mixture. Mononitrotoluene-nitroglycerin mixture. Salutes (bulk). DEPARTMENT OF JUSTICE Monopropellants. Silver acetylide. N Silver azide. Notice of Lodging of Proposed NIBTN [nitroisobutametriol trinitrate]. Silver fulminate. Consent Decree Under the Clean Air Nitrate explosive mixtures. Silver oxalate explosive mixtures. Act Nitrate sensitized with gelled nitroparaffin. Silver styphnate. Nitrated carbohydrate explosive. Silver tartrate explosive mixtures. On December 20, 2017, the Nitrated glucoside explosive. Silver tetrazene. Department of Justice lodged a proposed Nitrated polyhydric alcohol explosives. Slurried explosive mixtures of water, consent decree with the United States Nitric acid and a nitro aromatic compound inorganic oxidizing salt, gelling agent, fuel, District Court for the District of Arizona explosive. -

EPA Review of Arizona's 2016 303(D)

Enclosure EPA Review of Arizona’s 2016 303(d) List Date of Receipt by the EPA: December 27, 2016 Date of Receipt by the EPA of Additional Information Requested: January 17, 2017; January 23, 2017; February 1, 2017; February 2, 2017; February 9, 2017; April 14, 2017; April 21, 2017; and May 23, 2017. Purpose The purpose of this document is to describe the rationale for the EPA's action on Arizona’s 2016 Clean Water Act (CWA) Section 303(d) list of water quality limited segments (WQLSs) requiring a Total Maximum Daily Load (TMDL) pursuant to 40 CFR 130.7(a) (2016 List). The EPA reviewed the State's submittal including the listing decisions, the assessment methodology used by the State in developing its 2016 List, and supporting data. The EPA's review of the 2016 List is based on the EPA's analysis of whether the State reasonably considered existing and readily available water quality-related data and information, and reasonably identified waters required to be listed. This review describes the basis for the EPA’s decision to approve the State’s 2016 List identified in Appendix C of Arizona’s submittal, to disapprove the omission of six WQLSs that meet listing criteria, and to propose adding these waters to the 2016 List. The EPA’s determinations are based on materials submitted by the State and the references cited at the end of this document. Statutory and Regulatory Background Identification of WQLSs for Inclusion in the List CWA Section 303(d)(1) directs each state to identify those waters within its boundaries for which effluent limitations required by Section 301(b)(1)(A) and (B) are not stringent enough to achieve any applicable water quality standard (WQS), and to establish a priority ranking for addressing such waters, taking into account the severity of the pollution and the uses to be made of such waters. -

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

Case 4:17-cv-00612-RCC Document 1 Filed 12/20/17 Page 1 of 16 1 ELLEN M. MAHAN 2 Deputy Section Chief Environmental Enforcement Section 3 Environment and Natural Resources Division 4 JAMES R. MacAYEAL (D.C. Bar # 474664) Senior Counsel 5 Environmental Enforcement Section 6 United States Department of Justice P.O. Box 7611, Washington, D.C. 20044-7611 7 Telephone: (202)616-8777 8 j amie.macayeal@usdoj. gov 9 ELIZABETH A. STRANGE 10 Acting United States Attorney JANET MARTIN(Az Bar # 6014) 11 Civil Chief 12 District of Arizona 405 W. Congress Street, Suite 4800 13 Tucson, AZ 85701-5040 14 Attorneys for Plaintiff United States 15 16 UNITED STATES DISTRICT COURT 17 FOR THE DISTRICT OF ARIZONA 18 UNITED STATES OF AMERICA, 19 Plaintiff, 20 CASE NO. 21 v. COMPLAINT 22 APACHE NITROGEN PRODUCTS, 23 INC., 24 Defendant. 25 The United States of America, by authority of the Attorney General of the 26 United States and through the undersigned attorneys, acting at the request of the 27 Administrator of the United States Environmental Protection Agency ("EPA"), alleges 28 as follows: Case 4:17-cv-00612-RCC Document 1 Filed 12/20/17 Page 2 of 16 1 NATURE OF ACTION 2 1. This is a civil action pursuant to Section 113(b) of the Clean Air Act 3 (the "Act"), 42 U.S.C. § 7413(b). 4 2. The United States seeks civil penalties and injunctive relief against 5 Defendant Apache Nitrogen Products, Inc.("Apache" or "ANPI")for violating the 6 Arizona State Implementation Plan (the "Arizona SIP"), including the requirements 7 for the Prevention of Significant Deterioration ("PSD"), as set forth in the Arizona 8 Administrative Code("AAC") and for violating, a federal standard of performance 9 for new sources, 40 C.F.R. -

National Register of Historic Places Continuation Sheet

NFS Form 10-900-a OMB Approval No. 1024-4018 (8-86) United States Department of the Interior National Park Service National Register of Historic Places Continuation Sheet Section number ___ Page ___ SUPPLEMENTARY LISTING RECORD NRIS Reference Number: 94000078 Date Listed: 3/11/94 Apache Powder Historic Residential District Cochise AZ Property Name County State Historic Architectural Properties in Benson, Arizona, MPS Multiple Name This property is listed in the National Register of Historic Places in accordance with the attached nomination documentation subject to the following exceptions, exclusions, or amendments, notwithstanding the National Park Service certification included in the nomination documentation. js^ +*^ x") » /* *c<*j5f ' ^ '"_____ jty^L______ ^, Signa'ture 9^ the^Keeper Da'te' o^ Action Amended Items in Nomination: Materials: Add Wall Materials; Stucco to note the dominant use of the material on the exterior of a majority of the properties. Significance: The Period of Significance is amended to reflect a starting date of 1925, corresponding to the Apache Powder Company's initial purchase of property and the commencement of construction. [The full period should read: 1925-1942]. This information was confirmed with Reba Grandrud of the AZ SHPO DISTRIBUTION: National Register property file Nominating Authority (without nomination attachment) £ OC^i% NPS Form 10-000 owe NO. 1024-oora (R«v. W«) RECEIVED United States Department of the Interior National Park Service National Register of Historic Places NATIONAL Registration Form REGISTER This form is for use in nominating or requesting determinations of eligibility for individual properties or districts. See instructions iri Guidelines for Completing National Register Forms (National Register Bulletin 16). -

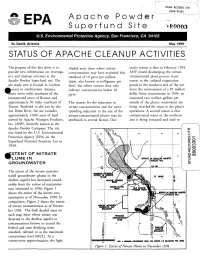

Status of Apache Cleanup Activities

SFUND RECORDS CTR 0048-91654 Apache Powder EPA Superfund Site R0003 U.S. Environmental Protection Agency, San Francisco, CA 94105 St. David, Arizona May 1999 STATUS OF APACHE CLEANUP ACTIVITIES The purpose of this fact sheet is to shaded areas show where nitrate major reason is that in February 1995, provide new information on investiga concentrations may have exceeded this ANP ceased discharging the nitrate- tive and cleanup activities at the standard of 10 parts pet million contaminated plant process waste Apache Powder Superfund site. The (ppm, also known as milligrams per waters to the unlined evaporation site study area is located in Cochise liter), but where current data only ponds in the southern area of the site. Sounty in southeastern Arizona, indicate concentrations below 10 Since the construction of a $5 million Ibout seven miles southeast of the ppm. dollar brine concentrator in 1994, an incorporated town of Benson and estimated two million gallons per approximately 50 miles southeast of The reasons for the reduction in month of the plant's wastewaters are Tucson. Bordered to the east by the nitrate concentrations and the corre being recycled for reuse in the plant's San Pedro River, the site includes sponding reduction in the size of the operations. A second reason is that approximately 1,000 acres of land nitrate-contaminated plume may be contaminated water in the northern owned by Apache Nitrogen Products, attributed to several factors. One area is being extracted and used to Inc. (ANP), formerly known as the Apache Powder Company. The site cm h- was listed by the U.S.