Annual Telecommunications Monitoring Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FY21 Results Overview

Annual Report 2021 01 Chorus Board and management overview 14 Management commentary 24 Financial statements 60 Governance and disclosures 92 Glossary FY21 results overview Fixed line connections1 Broadband connections1 FY21 FY20 FY21 FY20 1,340,000 1,415,000 1,180,000 1,206,000 Fibre connections1 Net profit after tax FY21 FY20 FY21 FY20 871,000 751,000 $47m $52m EBITDA2 Customer satisfaction Installation Intact FY21 FY20 FY21 FY21 $649m $648m 8.2 out of 10 7.5 out of 10 (target 8.0) (target 7.5) Dividend Employee engagement score3 FY21 FY20 FY21 FY20 25cps 24cps 8.5 out of 103 8.5 This report is dated 23 August 2021 and is signed on behalf of the Board of Chorus Limited. Patrick Strange Mark Cross Chair Chair Audit & Risk Management Committee 1 Excludes partly subsidised education connections provided as part of Chorus’ COVID-19 response. 2 Earnings before interest, income tax, depreciation and amortisation (EBITDA) is a non-GAAP profit measure. We monitor this as a key performance indicator and we believe it assists investors in assessing the performance of the core operations of our business. 3 Based on the average response to four key engagement questions. Dear investors Our focus in FY21 was to help consumers especially important because fixed wireless services don’t capitalise on the gigabit head start our fibre provide the same level of service as fibre - or even VDSL in network has given New Zealand. We knocked most cases – and these service limitations often aren’t made clear to the customer. on about a quarter of a million doors and supported our 100 or so retailers to connect As expected, other fibre companies continued to win copper customers in those areas where they have overbuilt our another 120,000 consumers to fibre. -

Bringing the Future Faster

6mm hinge Bringing the future faster. Annual Report 2019 WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Bringing the future faster Spark New Zealand Annual Report 2019 Bringing the future faster Contents Build customer intimacy We need to understand BRINGING THE FUTURE FASTER and anticipate the needs of New Zealanders, and Spark performance snapshot 4 technology enables us Chair and CEO review 6 to apply these insights Our purpose and strategy 10 to every interaction, Our performance 12 helping us serve our Our customers 14 customers better. Our products and technology 18 Read more pages 7 and 14. Our people 20 Our environmental impact 22 Our community involvement 24 Our Board 26 Our Leadership Squad 30 Our governance and risk management 32 Our suppliers 33 Leadership and Board remuneration 34 FINANCIAL STATEMENTS Financial statements 38 Notes to the financial statements 44 Independent auditor’s report 90 OTHER INFORMATION Corporate governance disclosures 95 Managing risk framework roles and 106 responsibilities Materiality assessment 107 Stakeholder engagement 108 Global Reporting Initiative (GRI) content 109 index Glossary 112 Contact details 113 This report is dated 21 August 2019 and is signed on behalf of the Board of Spark New Zealand Limited by Justine Smyth, Chair and Charles Sitch, Chair, Audit and Risk Management Committee. Justine Smyth Key Dates Annual Meeting 7 November 2019 Chair FY20 half-year results announcement 19 February 2020 FY20 year-end results announcement 26 August 2020 Charles Sitch Chair Audit and Risk Management Committee WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Create New Zealand’s premier sports streaming business Spark Sport is revolutionising how New Zealanders watch their favourite sports events. -

2021–24 Media Rights Sales

Media rights sales: 2021-24 UEFA Europa League™/ UEFA Europa Conference League™ Last Update: 24 August 2021 The media content rights sales process for the UEFA Europa League and the UEFA Europa Conference League (seasons 2021/22, 2022/23 and 2023/24) will be conducted on a market-by-market basis with such media rights being offered on a platform neutral basis and in accordance with the principles established by the European Commission. The sales process will usually be effected initially by means of an ‘Invitation to Submit Offer’ (ISO) process under which qualified media content distributors will be invited to submit offers before the submission deadline (as indicated in the Schedule A below) for the media rights in their respective territories. Schedule B lists the relevant territories for which media rights agreements have been signed (including details of the respective partners). The sales process will be administered on behalf of UEFA by TEAM Marketing, UEFA’s exclusive marketing agency for the exploitation of certain media and commercial rights relating to its club competitions. All enquiries in respect of the acquisition of such rights should therefore be directed to TEAM Marketing at the following e-mail address: [email protected]. Further communications and updates shall be provided as and when UEFA commences the media content rights sales process in respect of any other territories. Schedule A: ISO list The list of dates (subject to changes at UEFA’s discretion) on which an ISO has been or will be issued is, by territory, as follows: -

New Zealand Guide

WridgWays Global Guide to Living in New Zealand Image source: Photo by Laura Smetsers on Unsplash Disclaimer: Though WridgWays strives to maintain the materials in this document, keeping them as accurate and current as possible, the information is collected for reference purpose. WridgWays assumes no liability for any inaccurate or incomplete information, nor for any actions taken in reliance thereon. Table of Contents 1. General Information 2 2. Culture, Lifestyle and Language 4 3. Visa and Migration 7 4. Housing 8 5. Banking Services 11 6. Medical Services 12 7. Schooling 16 8. Utilities 18 9. Telecommunications 19 10. Public Transport 20 11. Driving 23 12. Moving your Pet 27 13. Household Goods Shipment and Customs Information 28 14. Shopping 29 1 1. General Information Geographic Location Main Locations New Zealand or Aotearoa, the Māori name, is an island country in Almost three-quarters of the population live on the North Island of the southwestern Pacific Ocean, with a total land area spanning New Zealand. Of this, one-third of the population live in the largest city, 268,021 km2. It consists of two main landmasses, the North Island Auckland. (Te Ika-a-Mui) and the South Island (Te Waipounamu), and Auckland is the commercial heart and international hub of New approximately 600 smaller islands. Aotearoa’s literal translation Zealand. It is considered one of the world's most liveable cities, and is “land of the long white cloud.” The country is long and narrow, offers a culturally diverse and cosmopolitan lifestyle. 1,600 kilometres north to south, and 400 kilometres at its widest point. -

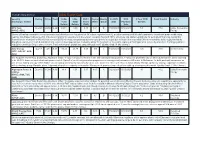

Utility Report Card Security Rating Price Yield 12-Mo

Conrad’s Utility Investor Utility Report Card Security Rating Price Yield 12-Mo. 3-Mo. DVD / Payout Quality Ex-DVD DVD 3-Year DVD Debt/ Capital Industry (Exchange: Ticker) Total Total Share Ratio Grade Date Payment Growth Return Return (CAD) Date AES Corp Buy<28 24.64 2.44 43.81 -0.66 0.15 39.1 B 7/30/2021 8/16/2021 5.3 77.2 Utility, Renewable (NYSE: AES) Energy Shares of leading renewable energy generator and developer are low priced at 14.3 times expected next 12 months earnings with Moody's upgrade to investment grade credit rating nearing. Alto Maipo hydro project in Chile is on track for full operations in December, company has built 100% of tunnels and starts negotiations for permanent financing, remaining financial share of project is $46 mil, has invested $972 mil. Asset encumbered by lower spot prices for output due to faster than expected Chilean renewables build, output limited by drought in country near term but financial risk to parent now appears low. Company plans 72 megawatt of new solar capacity in Michigan for in service by mid-2022. Earnings guidance mid-point remains $1.54 per share in 2021, 7-9% annual profit growth rate target through 2025. Quality Grade B (No Change). AGL Energy Buy<7 4.9 6.33 -50.46 -23.89 0.25 100 C 8/24/2021 10/6/2021 -6.6 36.6 Int'l Electricity (OTC: AGLXY, ASX: AGL) See August 13 Alert "AGL Bottoming, Algonquin a Buy." FY2021 (end June 30) are in line with management guidance, FY2022 net profit after tax on which dividends are set is expected to be 25-30% lower on weak wholesale power market. -

SPARK NEW ZEALAND Spark Increases Speed to Market and Reduces Costs with CSG

CUSTOMER SUCCESS STORY SPARK NEW ZEALAND Spark increases speed to market and reduces costs with CSG CLIENT OVERVIEW A HISTORY OF INNOVATION Spark is New Zealand’s largest telecommunications Before deploying CSG Singleview, Spark had to and digital services company. Spark provides rearchitect its billing function whenever it wanted to mobile, broadband and digital services to millions offer a new product. Turning to CSG for a convergent of New Zealanders and thousands of New Zealand charging and billing system, Singleview allowed Spark businesses. Spark’s end-to-end digital services to quickly offer new products, configuring offers without offerings include cloud transformation, managed needing new code. services, security, data, automation, analytics, IoT Spark uses Singleview to manage different products, and much more. such as supporting prepaid and postpaid plans from EXECUTIVE SUMMARY one solution. This convergent solution allowed Spark to respond to the demands of the fast-maturing New In the last several years, Spark has undergone Zealand mobile market. With Singleview, complex intense transformation. The company rebranded and scenarios are simplified, like sharing data across changed its name, reengineered its internal IT mobile devices in an account or free calling circles for systems, restructured into an Agile organization, otherwise unrelated customers. This allows Spark to tap and reinforced its commitment to lead with into lucrative market segments. wireless services. “Whether you use prepaid or postpaid plans is just a 2013 saw Spark embark on a three-year journey payment choice,” says Paul Adamson, Domain Chapter to rebuild its internal IT systems, with the goals of Lead for Billing. “You should be able to get the same improving time to market and reducing opex. -

Market and Economic Review

Milford KiwiSaver Plan Monthly Review December 2019 Market and Economic Review November saw investors embrace optimism for the first time this year as we inch closer to a trade deal and evidence builds of an emerging global growth rebound. Fund returns were strong this month, reflecting sharply higher share markets both locally and overseas. For most of the year, investors have been concerned about the deteriorating global economic outlook, driven by the impact of the US-China trade war on global trade and the business sector. Recently there has been a pause in the escalation of tariffs and there is hope that a trade deal will be signed before Christmas, paving the way for improvements in business sentiment. This development has enticed investors off the sidelines and money has been put to work in shares across the globe, boosting prices. When markets experience inflows it tends to be the larger stocks that benefit, and this was true in Australia and NZ this month with large cap stocks outperforming in both regions. However, November also saw plenty of opportunity for stock selection. In NZ, positive trading updates from the likes of a2 Milk and Fisher and Paykel Healthcare saw these stocks up 19.4% and 15.7% respectively in the month. Elsewhere, a long-term shareholder in EBOS Group decided to sell a large stake at a discount offering investors a rare chance to buy the shares in good volume. In Australia, the banks continue to strengthen their balance sheets and this time it was Westpac’s turn to ask investors for A$2bn of more capital. -

New Zealand Consumer Interest Growing for 5G Mobile

Journal of Telecommunications and the Digital Economy New Zealand Consumer Interest Growing for 5G Mobile Nigel Pugh Managing Director, Venture Insights Abstract: This paper summarizes results from a survey of the New Zealand mobile market by Venture Insights in October 2018. The survey had over 1,000 respondents, all of whom were responsible for making their mobile purchasing decisions, with a representative spread across New Zealand, all adult age groups, and customers from the three major mobile service providers. The survey identified a strong consumer interest in and awareness of 5G, with 31% of respondents willing to consider a move to 5G within two years of launch. Mobile video will be a strong driver, with 69% of respondents having viewed video on their mobile and, again, a willingness to move to 5G within two years. Fixed wireless broadband service was also strongly supported, with 18% of those with a household fixed broadband service indicating a possible transition within two years to a 5G fixed wireless service. However, the Ultra-Fast Broadband fixed service is likely to be a strong competitor to fixed wireless broadband. Keywords: 5G, Fixed wireless, Wireless broadband, New Zealand market Introduction In October 2018, Venture Insights conducted a market survey in order to better understand consumer interest in the evolving New Zealand mobile market and the early adoption of 5G services and platforms. This paper, after some background on the respondents, focusses on four key aspects of the survey: • Consumer 5G awareness and competition for the early adopter market; • Consumer usage of mobile video and streaming services; • 5G use case for mobile and telco media bundling; • 5G use case for fixed wireless broadband. -

Success Story - Smart Agriculture

Success Story - Smart agriculture - PLAINVUE FARM KEY FIGURES 93 hectares 280 cows 109 K SPARK & Located in South Dairy farm solid milk production SENSYS Auckland NZ July 2017, New Zealand control systems with intelligence for Regulation & resources management dairy, horticulture, safety and security, Water is scarce and storage is limited, Spark and SenSys and tracking. It is New Zealand’s leading so farmers must know how much or supported by Actility company in developing long-range, how little water to use to avoid runoff. wide-area network (LoRaWAN) sensors. This requires constant monitoring of soil enable smart agriculture moisture, air temperature, etc. In addi- in New Zealand I’m not a computer whiz, tion, farmers must avoid overusing ferti- Armed With New LoRaWAN but technology helps. lizers and nutrients and prevent storage leakage. There are also high health stan- Sensors, NZ Dairy Farmer Doesn’t Tony Walters, Dairy farmer and co-owner of Plainvue Farms dards, such as strict temperature control Look Back of milk throughout the supply chain. Maximize profit through sustainable The primary objective of Plainvue Farms For all the above, farmers are expected to provide clear documented proof of pasture-based dairy farming is to maximize profit through sustai- nable pasture-based dairy farming. compliance and failure to do so can Dairy farmers in remote areas of New Early adopters of technology on their result in tough penalties. Zealand face a variety of environmental farm, the Walters seek to trial and constraints and regulations. In response, Functionality showcase new solutions that meet the Tony and Marlene Walters, owners following challenges: Gathering data is extremely useful, of South Auckland’s Plainvue Farms, but it is impractical for farmers to take have trialed new low-power, wide area Connectivity measurements each evening and enter (LPWA) technology, supported by Many farms in New Zealand are remote, information into a database manually. -

Subscription Video on Demand: Viewing Preferences Among New Zealand Audiences

Subscription Video on Demand: Viewing preferences among New Zealand audiences Rachel Hayley Daniels A thesis submitted to Auckland University of Technology in partial fulfilment of the requirements for the degree of Master of Communication Studies (MCS) 2017 School of Communication Studies Abstract With the development of digital television platforms in New Zealand and the launch of Subscription Video on Demand (SVOD) services such as Netflix NZ, Lightbox, Quickflix and Neon, a more discerning television audience is emerging. SVOD services are influencing a change within the television broadcasting landscape in New Zealand, fragmenting audiences away from traditional linear television, appealing to viewers in new and innovative ways and changing viewing behaviour. This thesis provides qualitative and quantitative analysis of SVOD viewers’ experiences, expectations, and behaviours with respect to viewing content on the digital platforms and services available to New Zealand subscribers. Quantitative data was collected from an online survey; participants were drawn from readers of the New Zealand Herald online. The quantitative data was collected in order to help position and supplement the qualitative data, which was obtained through focus group interviews. A thematic analysis was used to identify key themes and draw insight from the data sets. The thesis identifies that viewers place a high degree of preference and value on the freedom and opportunities that SVOD provides in personalizing their own viewing practices. Key preferences among these was the ability to control content selection and engage in the practice of anytime viewing, i.e. to choose from an increasingly broad selection of content wherever they are, whenever they like and on whatever device they prefer to view it on. -

Ief-I Q3 2020

Units Cost Market Value INTERNATIONAL EQUITY FUND-I International Equities 96.98% International Common Stocks AUSTRALIA ABACUS PROPERTY GROUP 1,012 2,330 2,115 ACCENT GROUP LTD 3,078 2,769 3,636 ADBRI LTD 222,373 489,412 455,535 AFTERPAY LTD 18,738 959,482 1,095,892 AGL ENERGY LTD 3,706 49,589 36,243 ALTIUM LTD 8,294 143,981 216,118 ALUMINA LTD 4,292 6,887 4,283 AMP LTD 15,427 26,616 14,529 ANSELL LTD 484 8,876 12,950 APA GROUP 14,634 114,162 108,585 APPEN LTD 11,282 194,407 276,316 AUB GROUP LTD 224 2,028 2,677 AUSNET SERVICES 9,482 10,386 12,844 AUSTRALIA & NEW ZEALAND BANKIN 19,794 340,672 245,226 AUSTRALIAN PHARMACEUTICAL INDU 4,466 3,770 3,377 BANK OF QUEENSLAND LTD 1,943 13,268 8,008 BEACH ENERGY LTD 3,992 4,280 3,824 BEGA CHEESE LTD 740 2,588 2,684 BENDIGO & ADELAIDE BANK LTD 2,573 19,560 11,180 BHP GROUP LTD 16,897 429,820 435,111 BHP GROUP PLC 83,670 1,755,966 1,787,133 BLUESCOPE STEEL LTD 9,170 73,684 83,770 BORAL LTD 6,095 21,195 19,989 BRAMBLES LTD 135,706 987,557 1,022,317 BRICKWORKS LTD 256 2,997 3,571 BWP TRUST 2,510 6,241 7,282 CENTURIA INDUSTRIAL REIT 1,754 3,538 3,919 CENTURIA OFFICE REIT 154,762 199,550 226,593 CHALLENGER LTD 2,442 13,473 6,728 CHAMPION IRON LTD 1,118 2,075 2,350 CHARTER HALL LONG WALE REIT 2,392 8,444 8,621 CHARTER HALL RETAIL REIT 174,503 464,770 421,358 CHARTER HALL SOCIAL INFRASTRUC 1,209 2,007 2,458 CIMIC GROUP LTD 4,894 73,980 65,249 COCA-COLA AMATIL LTD 2,108 12,258 14,383 COCHLEAR LTD 1,177 155,370 167,412 COMMONWEALTH BANK OF AUSTRALIA 12,637 659,871 577,971 CORONADO GLOBAL RESOURCES INC 1,327 -

M Funds Quarterly Holdings 3.31.2020*

M International Equity Fund 31-Mar-20 CUSIP SECURITY NAME SHARES MARKET VALUE % OF TOTAL ASSETS 233203421 DFA Emerging Markets Core Equity P 2,263,150 35,237,238.84 24.59% 712387901 Nestle SA, Registered 22,264 2,294,710.93 1.60% 711038901 Roche Holding AG 4,932 1,603,462.36 1.12% 690064001 Toyota Motor Corp. 22,300 1,342,499.45 0.94% 710306903 Novartis AG, Registered 13,215 1,092,154.20 0.76% 079805909 BP Plc 202,870 863,043.67 0.60% 780087953 Royal Bank of Canada 12,100 749,489.80 0.52% ACI07GG13 Novo Nordisk A/S, Class B 12,082 728,803.67 0.51% B15C55900 Total SA 18,666 723,857.50 0.51% 098952906 AstraZeneca Plc 7,627 681,305.26 0.48% 406141903 LVMH Moet Hennessy Louis Vuitton S 1,684 625,092.87 0.44% 682150008 Sony Corp. 10,500 624,153.63 0.44% B03MLX903 Royal Dutch Shell Plc, Class A 35,072 613,753.12 0.43% 618549901 CSL, Ltd. 3,152 571,782.15 0.40% ACI02GTQ9 ASML Holding NV 2,066 549,061.02 0.38% B4TX8S909 AIA Group, Ltd. 60,200 541,577.35 0.38% 677062903 SoftBank Group Corp. 15,400 539,261.93 0.38% 621503002 Commonwealth Bank of Australia 13,861 523,563.51 0.37% 092528900 GlaxoSmithKline Plc 26,092 489,416.83 0.34% 891160954 Toronto-Dominion Bank (The) 11,126 473,011.14 0.33% B1527V903 Unilever NV 9,584 472,203.46 0.33% 624899902 KDDI Corp.