Network Neutrality Adobe Acrobat PDF File 482 KB This

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FY21 Results Overview

Annual Report 2021 01 Chorus Board and management overview 14 Management commentary 24 Financial statements 60 Governance and disclosures 92 Glossary FY21 results overview Fixed line connections1 Broadband connections1 FY21 FY20 FY21 FY20 1,340,000 1,415,000 1,180,000 1,206,000 Fibre connections1 Net profit after tax FY21 FY20 FY21 FY20 871,000 751,000 $47m $52m EBITDA2 Customer satisfaction Installation Intact FY21 FY20 FY21 FY21 $649m $648m 8.2 out of 10 7.5 out of 10 (target 8.0) (target 7.5) Dividend Employee engagement score3 FY21 FY20 FY21 FY20 25cps 24cps 8.5 out of 103 8.5 This report is dated 23 August 2021 and is signed on behalf of the Board of Chorus Limited. Patrick Strange Mark Cross Chair Chair Audit & Risk Management Committee 1 Excludes partly subsidised education connections provided as part of Chorus’ COVID-19 response. 2 Earnings before interest, income tax, depreciation and amortisation (EBITDA) is a non-GAAP profit measure. We monitor this as a key performance indicator and we believe it assists investors in assessing the performance of the core operations of our business. 3 Based on the average response to four key engagement questions. Dear investors Our focus in FY21 was to help consumers especially important because fixed wireless services don’t capitalise on the gigabit head start our fibre provide the same level of service as fibre - or even VDSL in network has given New Zealand. We knocked most cases – and these service limitations often aren’t made clear to the customer. on about a quarter of a million doors and supported our 100 or so retailers to connect As expected, other fibre companies continued to win copper customers in those areas where they have overbuilt our another 120,000 consumers to fibre. -

2013 Annual Telecommunications Monitoring Report

ISSN 1179-724X Project no. 13.3/10147 Public Annual Telecommunications Monitoring Report 2013 Telecommunications monitoring report Date: May 2014 2 CONTENTS Executive Summary 3 Introduction 5 Purpose of this report 5 Data sources 5 Market overview 6 TelstraClear disappears 6 UFB drives up telecommunications investment 6 Broadband connections continue to grow 8 Calling volumes converging 10 Total revenue rise not sustained 11 Fixed-line and mobile markets show similar levels of concentration 12 Retail fixed-line market 14 Market overview 14 Fall in local calling accelerates 15 Most fixed-line revenues continue to fall 17 Telecom’s retail voice share continues to slip, including wholesale 18 Consolidation in broadband market 19 Lift in average broadband speed 21 Retail mobile market 23 Market overview 23 Rising data revenues underpin modest growth 24 Mobile voice minutes resume upward trend 25 Off-net calling becomes more popular 26 Texting appears to have peaked 28 Competition progressing in prepay but not much in business 30 The telecommunications consumer – from smartphone to smart living 33 How much appetite do users have for data and speed? 34 What drives consumption? 38 What is the impact on citizens’ welfare and New Zealand’s economic growth? 44 Challenges of digital life 50 The 2013 year in review 52 List of defined terms and abbreviations 57 3 Executive Summary This is the Commerce Commission’s seventh annual telecommunications market monitoring report. It is produced as part of the Commission’s on-going monitoring of the evolution of competition in the telecommunications sector in New Zealand. We have included two infographics showing how the telecommunications market is delivering more to consumers and helping to drive the economy. -

Bringing the Future Faster

6mm hinge Bringing the future faster. Annual Report 2019 WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Bringing the future faster Spark New Zealand Annual Report 2019 Bringing the future faster Contents Build customer intimacy We need to understand BRINGING THE FUTURE FASTER and anticipate the needs of New Zealanders, and Spark performance snapshot 4 technology enables us Chair and CEO review 6 to apply these insights Our purpose and strategy 10 to every interaction, Our performance 12 helping us serve our Our customers 14 customers better. Our products and technology 18 Read more pages 7 and 14. Our people 20 Our environmental impact 22 Our community involvement 24 Our Board 26 Our Leadership Squad 30 Our governance and risk management 32 Our suppliers 33 Leadership and Board remuneration 34 FINANCIAL STATEMENTS Financial statements 38 Notes to the financial statements 44 Independent auditor’s report 90 OTHER INFORMATION Corporate governance disclosures 95 Managing risk framework roles and 106 responsibilities Materiality assessment 107 Stakeholder engagement 108 Global Reporting Initiative (GRI) content 109 index Glossary 112 Contact details 113 This report is dated 21 August 2019 and is signed on behalf of the Board of Spark New Zealand Limited by Justine Smyth, Chair and Charles Sitch, Chair, Audit and Risk Management Committee. Justine Smyth Key Dates Annual Meeting 7 November 2019 Chair FY20 half-year results announcement 19 February 2020 FY20 year-end results announcement 26 August 2020 Charles Sitch Chair Audit and Risk Management Committee WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Create New Zealand’s premier sports streaming business Spark Sport is revolutionising how New Zealanders watch their favourite sports events. -

The World Internet Project International Report 6Th Edition

The World Internet Project International Report 6th Edition THE WORLD INTERNET PROJECT International Report ̶ Sixth Edition Jeffrey I. Cole, Ph.D. Director, USC Annenberg School Center for the Digital Future Founder and Organizer, World Internet Project Michael Suman, Ph.D., Research Director Phoebe Schramm, Associate Director Liuning Zhou, Ph.D., Research Associate Interns: Negin Aminian, Hany Chang, Zoe Covello, Ryan Eason, Grace Marie Laffoon‐Alejanre, Eunice Lee, Zejun Li, Cheechee Lin, Guadalupe Madrigal, Mariam Manukyan, Lauren Uba, Tingxue Yu Written by Monica Dunahee and Harlan Lebo World Internet Project International Report ̶ Sixth Edition | i WORLD INTERNET PROJECT – International Report Sixth Edition Copyright © 2016 University of Southern California COPIES You are welcome to download additional copies of The World Internet Project International Report for research or individual use. However, this report is protected by copyright and intellectual property laws, and cannot be distributed in any way. By acquiring this publication you agree to the following terms: this copy of the sixth edition of the World Internet Project International Report is for your exclusive use. Any abuse of this agreement or any distribution will result in liability for its illegal use. To download the full text and graphs in this report, go to www.digitalcenter.org. ATTRIBUTION Excerpted material from this report can be cited in media coverage and institutional publications. Text excerpts should be attributed to The World Internet Project. Graphs should be attributed in a source line to: The World Internet Project International Report (sixth edition) USC Annenberg School Center for the Digital Future REPRINTING Reprinting this report in any form other than brief excerpts requires permission from the USC Annenberg School Center for the Digital Future at the address below. -

Cross-Media News Repertories in New Zealand

. Volume 14, Issue 2 November 2017 Shopping in a narrow field: Cross-media news repertories in New Zealand Craig Hight, University of Newcastle, Australia Arezou Zalipour, University of Waikato, New Zealand Abstract: This article reports on the New Zealand case study within a larger project investigating cross-media news repertoires within (and across) national audiences. Six key news media repertoires emerged in this case study; heavy news consumers; hybrid browsers; digital browsers; ambivalent networkers; mainstream multiplatformers; and casual and connected). Despite a range of news media outlets available within New Zealand, particularly across digital platforms, participants consistently noted a relatively narrow social, cultural and political discursive field for news content in the country. Within this context, the news repertoires identified within this case study highlighted the high value placed by news consumers on national daily newspapers (print and online), and the continued salience of television and radio news broadcasting for some audience segments. But findings also offered a snapshot of the ways these are being supplemented or replaced, for some audience segments, by digital news outlets (even as these also generated dissatisfaction from many participants). Keywords: news repertoires, New Zealand, Q-methodology, news consumption, cross- cultural Introduction This article reports on the New Zealand case study within a larger project investigating patterns of news repertoires (Schrøder 2015) within (and across) national audiences, at a time of broadening forms of distribution of news content across a variety of media Page 416 Volume 14, Issue 2 November 2017 platforms. The overall project involved 12 countries and used a Q-sort methodology (Kobbernagel & Schrøder, 2016) to analyze and examine cross-media news consumption among audiences. -

2021–24 Media Rights Sales

Media rights sales: 2021-24 UEFA Europa League™/ UEFA Europa Conference League™ Last Update: 24 August 2021 The media content rights sales process for the UEFA Europa League and the UEFA Europa Conference League (seasons 2021/22, 2022/23 and 2023/24) will be conducted on a market-by-market basis with such media rights being offered on a platform neutral basis and in accordance with the principles established by the European Commission. The sales process will usually be effected initially by means of an ‘Invitation to Submit Offer’ (ISO) process under which qualified media content distributors will be invited to submit offers before the submission deadline (as indicated in the Schedule A below) for the media rights in their respective territories. Schedule B lists the relevant territories for which media rights agreements have been signed (including details of the respective partners). The sales process will be administered on behalf of UEFA by TEAM Marketing, UEFA’s exclusive marketing agency for the exploitation of certain media and commercial rights relating to its club competitions. All enquiries in respect of the acquisition of such rights should therefore be directed to TEAM Marketing at the following e-mail address: [email protected]. Further communications and updates shall be provided as and when UEFA commences the media content rights sales process in respect of any other territories. Schedule A: ISO list The list of dates (subject to changes at UEFA’s discretion) on which an ISO has been or will be issued is, by territory, as follows: -

New Zealand Guide

WridgWays Global Guide to Living in New Zealand Image source: Photo by Laura Smetsers on Unsplash Disclaimer: Though WridgWays strives to maintain the materials in this document, keeping them as accurate and current as possible, the information is collected for reference purpose. WridgWays assumes no liability for any inaccurate or incomplete information, nor for any actions taken in reliance thereon. Table of Contents 1. General Information 2 2. Culture, Lifestyle and Language 4 3. Visa and Migration 7 4. Housing 8 5. Banking Services 11 6. Medical Services 12 7. Schooling 16 8. Utilities 18 9. Telecommunications 19 10. Public Transport 20 11. Driving 23 12. Moving your Pet 27 13. Household Goods Shipment and Customs Information 28 14. Shopping 29 1 1. General Information Geographic Location Main Locations New Zealand or Aotearoa, the Māori name, is an island country in Almost three-quarters of the population live on the North Island of the southwestern Pacific Ocean, with a total land area spanning New Zealand. Of this, one-third of the population live in the largest city, 268,021 km2. It consists of two main landmasses, the North Island Auckland. (Te Ika-a-Mui) and the South Island (Te Waipounamu), and Auckland is the commercial heart and international hub of New approximately 600 smaller islands. Aotearoa’s literal translation Zealand. It is considered one of the world's most liveable cities, and is “land of the long white cloud.” The country is long and narrow, offers a culturally diverse and cosmopolitan lifestyle. 1,600 kilometres north to south, and 400 kilometres at its widest point. -

Annual Telecommunications Monitoring Report

ANNUAL TELECOMMUNICATIONS MONITORING REPORT 2014 CONTENTS EXECUTIVE SUMMARY 3 INTRODUCTION 5 Purpose of this report 6 Data sources 6 MARKET OVERVIEW 7 700MHz spectrum auction completed 7 Orcon sold again 7 Telecom becomes Spark 7 Wholesale copper pricing reduced but not finalised 8 Fibre becoming more common 8 New online streaming services keep arriving 8 2degrees buys Snap 8 UFB continues to underpin high level of telecommunications investment 9 Broadband connections of all types continue to grow 10 Calling volumes continue opposing trends 11 Total revenue declines again 12 RETAIL FIXED-LINE MARKET 13 Market overview 13 Fall in calling largely continues 15 All but broadband revenues continue to fall 16 Spark’s retail and wholesale voice share continues to decline 17 Further consolidation in broadband market 18 Broadband subscribers using more data 19 Mixed results in broadband price benchmarking 21 Broadband prices continued to trend down in 2014 23 Significant rise in average broadband speed 24 RETAIL MOBILE MARKET 25 Market overview 25 Spark claws back market share while 2degrees marks time 26 Mobile voice minutes per connection continue to climb 28 Off-net calling shows strongest growth 29 Texting continues to slide from peak 29 Mobile data consumption nearly doubles again 30 New Zealand below average price for all levels of mobile phone usage 30 Mobile prices have fallen dramatically in recent years 31 Mobile broadband still expensive 32 THE TELECOMMUNICATIONS CONSUMER 34 THE 2014 YEAR IN REVIEW 47 LIST OF DEFINED TERMS AND ABBREVIATIONS 54 2 Commerce Commission Annual Telecommunications Monitoring Report 2014 Executive Summary This is the Commerce Commission’s eighth annual telecommunications market monitoring report. -

ANNUAL TELECOMMUNICATIONS MONITORING REPORT 2010 April 2011

ANNUAL TELECOMMUNICATIONS MONITORING REPORT 2010 April 2011 TABLE OF CONTENTS INTRODUCTION ........................................................................................... 4 KEY MARKET TRENDS AND OBSERVATIONS FOR 2010 ................. 5 MARKET OVERVIEW ................................................................................. 8 Investment in Telecommunications Markets ............................................ 8 Investment Initiatives .................................................................................. 9 Fixed Line and Mobile Comparisons ....................................................... 11 Call Volumes ............................................................................................... 12 Revenue from Telecommunications Services .......................................... 14 THE FIXED LINE MARKET ..................................................................... 18 Market Overview ....................................................................................... 18 Fixed Line Voice ......................................................................................... 19 Fixed Line Data .......................................................................................... 25 Development of Unbundling ..................................................................... 28 Broadband Quality .................................................................................... 31 MOBILE MARKET ..................................................................................... -

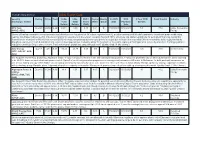

Utility Report Card Security Rating Price Yield 12-Mo

Conrad’s Utility Investor Utility Report Card Security Rating Price Yield 12-Mo. 3-Mo. DVD / Payout Quality Ex-DVD DVD 3-Year DVD Debt/ Capital Industry (Exchange: Ticker) Total Total Share Ratio Grade Date Payment Growth Return Return (CAD) Date AES Corp Buy<28 24.64 2.44 43.81 -0.66 0.15 39.1 B 7/30/2021 8/16/2021 5.3 77.2 Utility, Renewable (NYSE: AES) Energy Shares of leading renewable energy generator and developer are low priced at 14.3 times expected next 12 months earnings with Moody's upgrade to investment grade credit rating nearing. Alto Maipo hydro project in Chile is on track for full operations in December, company has built 100% of tunnels and starts negotiations for permanent financing, remaining financial share of project is $46 mil, has invested $972 mil. Asset encumbered by lower spot prices for output due to faster than expected Chilean renewables build, output limited by drought in country near term but financial risk to parent now appears low. Company plans 72 megawatt of new solar capacity in Michigan for in service by mid-2022. Earnings guidance mid-point remains $1.54 per share in 2021, 7-9% annual profit growth rate target through 2025. Quality Grade B (No Change). AGL Energy Buy<7 4.9 6.33 -50.46 -23.89 0.25 100 C 8/24/2021 10/6/2021 -6.6 36.6 Int'l Electricity (OTC: AGLXY, ASX: AGL) See August 13 Alert "AGL Bottoming, Algonquin a Buy." FY2021 (end June 30) are in line with management guidance, FY2022 net profit after tax on which dividends are set is expected to be 25-30% lower on weak wholesale power market. -

SPARK NEW ZEALAND Spark Increases Speed to Market and Reduces Costs with CSG

CUSTOMER SUCCESS STORY SPARK NEW ZEALAND Spark increases speed to market and reduces costs with CSG CLIENT OVERVIEW A HISTORY OF INNOVATION Spark is New Zealand’s largest telecommunications Before deploying CSG Singleview, Spark had to and digital services company. Spark provides rearchitect its billing function whenever it wanted to mobile, broadband and digital services to millions offer a new product. Turning to CSG for a convergent of New Zealanders and thousands of New Zealand charging and billing system, Singleview allowed Spark businesses. Spark’s end-to-end digital services to quickly offer new products, configuring offers without offerings include cloud transformation, managed needing new code. services, security, data, automation, analytics, IoT Spark uses Singleview to manage different products, and much more. such as supporting prepaid and postpaid plans from EXECUTIVE SUMMARY one solution. This convergent solution allowed Spark to respond to the demands of the fast-maturing New In the last several years, Spark has undergone Zealand mobile market. With Singleview, complex intense transformation. The company rebranded and scenarios are simplified, like sharing data across changed its name, reengineered its internal IT mobile devices in an account or free calling circles for systems, restructured into an Agile organization, otherwise unrelated customers. This allows Spark to tap and reinforced its commitment to lead with into lucrative market segments. wireless services. “Whether you use prepaid or postpaid plans is just a 2013 saw Spark embark on a three-year journey payment choice,” says Paul Adamson, Domain Chapter to rebuild its internal IT systems, with the goals of Lead for Billing. “You should be able to get the same improving time to market and reducing opex. -

The Internet, the Law, and Privacy in New Zealand: Dignity with Liberty?

International Journal of Communication 6 (2012), 127–143 1932–8036/20120127 The Internet, the Law, and Privacy in New Zealand: Dignity with Liberty? JONATHAN BARRETT LUKE STRONGMAN Open Polytechnic of New Zealand Early participants in the Internet experienced very little legal or social pressure with respect to either data privacy or regulation. However, the innovations of Web 2.0 are symptomatic of a re-creation of cyberspace from an original “free for all,” in which websites had no normative constraints, toward a significant shift to website management that addresses privacy concerns. If the laws of the non-virtual world are difficult to apply to the online world, must the non-virtual world create new laws to control the online world? Should a balance be made between laws of the non-virtual and virtual worlds, or should a new set of laws be created specifically to govern the Internet? Concordant with this dilemma is the issue that although precedent may create new laws, when the law changes with the possibilities for uses and abuses of new online technologies, to what extent can it be said to either perpetuate or create to any internally consistent system? Introduction For many of its early participants, the Internet presented the opportunity for a benignly anarchic and anomic space for freedom of expression that, in principle and practice, should be liberated from established legal traditions and social pressures. Its debt to the military notwithstanding (see Morozov, 2011b), Web 1.0 was typically conceived as a virtual realm that could be created, grown, and governed— or non-governed—by its participants.