Debt, Deleveraging, and the Liquidity Trap: a Fisher‐Minsky‐Koo Approach

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Debt-Deflation Theory of Great Depressions by Irving Fisher

THE DEBT-DEFLATION THEORY OF GREAT DEPRESSIONS BY IRVING FISHER INTRODUCTORY IN Booms and Depressions, I have developed, theoretically and sta- tistically, what may be called a debt-deflation theory of great depres- sions. In the preface, I stated that the results "seem largely new," I spoke thus cautiously because of my unfamiliarity with the vast literature on the subject. Since the book was published its special con- clusions have been widely accepted and, so far as I know, no one has yet found them anticipated by previous writers, though several, in- cluding myself, have zealously sought to find such anticipations. Two of the best-read authorities in this field assure me that those conclu- sions are, in the words of one of them, "both new and important." Partly to specify what some of these special conclusions are which are believed to be new and partly to fit them into the conclusions of other students in this field, I am offering this paper as embodying, in brief, my present "creed" on the whole subject of so-called "cycle theory." My "creed" consists of 49 "articles" some of which are old and some new. I say "creed" because, for brevity, it is purposely ex- pressed dogmatically and without proof. But it is not a creed in the sense that my faith in it does not rest on evidence and that I am not ready to modify it on presentation of new evidence. On the contrary, it is quite tentative. It may serve as a challenge to others and as raw material to help them work out a better product. -

Inflation, Income Taxes, and the Rate of Interest: a Theoretical Analysis

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Inflation, Tax Rules, and Capital Formation Volume Author/Editor: Martin Feldstein Volume Publisher: University of Chicago Press Volume ISBN: 0-226-24085-1 Volume URL: http://www.nber.org/books/feld83-1 Publication Date: 1983 Chapter Title: Inflation, Income Taxes, and the Rate of Interest: A Theoretical Analysis Chapter Author: Martin Feldstein Chapter URL: http://www.nber.org/chapters/c11328 Chapter pages in book: (p. 28 - 43) Inflation, Income Taxes, and the Rate of Interest: A Theoretical Analysis Income taxes are a central feature of economic life but not of the growth models that we use to study the long-run effects of monetary and fiscal policies. The taxes in current monetary growth models are lump sum transfers that alter disposable income but do not directly affect factor rewards or the cost of capital. In contrast, the actual personal and corporate income taxes do influence the cost of capital to firms and the net rate of return to savers. The existence of such taxes also in general changes the effect of inflation on the rate of interest and on the process of capital accumulation.1 The current paper presents a neoclassical monetary growth model in which the influence of such taxes can be studied. The model is then used in sections 3.2 and 3.3 to study the effect of inflation on the capital intensity of the economy. James Tobin's (1955, 1965) early result that inflation increases capital intensity appears as a possible special case. -

Deleveraging and the Aftermath of Overexpansion

May 28th, 2009 Jeffrey Owen Herzog Deleveraging and the aftermath of overexpansion [email protected] O The deleveraging process for commercial banks is likely to last years and overshoot compared to fundamentals Banking System Asset and Leverage Growth O A strong procyclical correlation exists between asset growth and Nominal Values, 1934-2008 leverage growth over the past 75 years 25% O At the level of the firm, boom times generate decreasing 20% 1942 collateralization rates and increasing average loan sizes 15% O Given two-year loan losses of $1.1tr and leverage declines of -5% 10% 2008 to -7.5%, we expect deleveraging to curtail commercial bank 5% credit by $646bn and $687bn per year for 2009-2010 0% -5% Trends in deleveraging and commercial banking over time Leverage Growth -10% 2004 -15% 1946 Deleveraging is the process whereby commercial banks reduce their ratio of -20% assets to equity capital, thus bringing down their aggregate exposure to the 0% 5% -5% 10% 15% 20% 25% 30% economy. Many commentators point to this process as an eventual destination -10% Asset Growth for the US commercial banking system, but few have described where or how Source: FDIC we arrive at a more deleveraged commercial banking system. Commercial Bank Assets and Equity Adjusted for Inflation by CPI, $tr Over the past seventy years, the commercial banking sector’s aggregate 0.6 6 balance sheet has demonstrated a strong positive correlation between leverage and asset growth. For the banking industry, 2004 was an 0.5 5 S&L Crisis, 1989-1991 exceptionally unusual year, with equity increasing yoy by 22%. -

Welfare Economic Foundation of Hoarding Loss by Money Circulation Optimization

Munich Personal RePEc Archive Welfare economic foundation of hoarding loss by money circulation optimization Miura, Shinji Independent 13 August 2018 Online at https://mpra.ub.uni-muenchen.de/88443/ MPRA Paper No. 88443, posted 20 Aug 2018 10:07 UTC Welfare economic foundation of hoarding loss by money circulation optimization Shinji Miura (Independent. Gifu, Japan) Abstract Saving brings an economic loss. This is one of the basic propositions of the under-consumption theory. This paper aims to give a welfare economic foundation of this proposition through an optimization method considering money circulation in the case where a type of saving is limited to hoarding. If price is fixed, a non-hoarding state is a necessary condition for Pareto efficiency. However, individual agents who prefer future expenditure hoard money, thus individual rational behavior brings about a Pareto inefficient state. This irrationality of rationality occurs because of a qualitative difference of the budget constraint between the whole society and an individual agent. The former’s constraint incorporates a truth that hoarding decreases other’s revenue, whereas the latter’s does not. Selfish individual agents make a decision with an ignorance of this relational truth because their interest is limited to their private range. As a result, agents fall into an irrational situation despite their rational judgment. Keywords: Money Circulation, Welfare Economics, Under-Consumption, Paradox of Thrift, Intertemporal Choice. 1. Introduction Saving brings an economic loss even though it is often regarded as a virtue. This proposition, known as the paradox of thrift, is one of main elements of the under-consumption theory. -

What Have We Learned? Macroeconomic Policy After the Crisis

What Have We Learned? What Have We Learned? Macroeconomic Policy after the Crisis edited by George Akerlof, Olivier Blanchard, David Romer, and Joseph Stiglitz The MIT Press Cambridge, Massachusetts London, England © 2014 International Monetary Fund and Massachusetts Institute of Technology All rights reserved. No part of this book may be reproduced in any form by any elec- tronic or mechanical means (including photocopying, recording, or information storage and retrieval) without permission in writing from the publisher. Nothing contained in this book should be reported as representing the views of the IMF, its Executive Board, member governments, or any other entity mentioned herein. The views expressed in this book belong solely to the authors. MIT Press books may be purchased at special quantity discounts for business or sales promotional use. For information, please email [email protected]. This book was set in Sabon by Toppan Best-set Premedia Limited, Hong Kong. Printed and bound in the United States of America. Library of Congress Cataloging-in-Publication Data What have we learned ? : macroeconomic policy after the crisis / edited by George Akerlof, Olivier Blanchard, David Romer, and Joseph Stiglitz. pages cm Includes bibliographical references and index. ISBN 978-0-262-02734-2 (hardcover : alk. paper) 1. Monetary policy. 2. Fiscal policy. 3. Financial crises — Government policy. 4. Economic policy. 5. Macroeconomics. I. Akerlof, George A., 1940 – HG230.3.W49 2014 339.5 — dc23 2013037345 10 9 8 7 6 5 4 3 2 1 Contents Introduction: Rethinking Macro Policy II — Getting Granular 1 Olivier Blanchard, Giovanni Dell ’ Ariccia, and Paolo Mauro Part I: Monetary Policy 1 Many Targets, Many Instruments: Where Do We Stand? 31 Janet L. -

The Paradox of Thrift

ECONOMICS PAGE ONE NEWSLETTER the back story on front page economics May I 2012 Wait, Is Saving Good or Bad? The Paradox of Thrift E. Katarina Vermann, Research Associate “[Saving] is a paradox because in kindergarten we are all taught that thrift is always a good thing.”1 —Paul A. Samuelson, first American to win the Nobel Prize in Economics (1970) People save for various reasons. Some save with a specific purchase in mind, such as cos- metic surgery or a Porsche, while others save just to have more money. Economists say that individuals save to buy durable goods and/or accumulate wealth to maintain a certain lifestyle during retirement or in times of financial uncertainty. These reasons all confer benefits to a saver. In the near term, the saver can finally buy the latest and greatest gadget, and in the long term, the saver can be more financially secure during retirement or unplanned unemployment. Normally, personal saving declines during recessions because people want to maintain their existing level of consumption. During the Great Recession, though, saving increased. The chart shows the personal saving rate, the year-over-year growth rate of gross domestic prod- uct (GDP), and recession periods from 2000 to 2011. Before the Great Recession, the average saving rate for the typical American household was 2.9 percent. Since the recession started in 2007, the average saving rate has risen to 5.0 percent. This increase was largely driven by uncer- Source: Bureau of Economic Analysis, Naonal Bureau of Economic Research, and FRED. Recession Average Saving Rate GDP Growth Personal Saving Rate 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2011 -6 -4 -2 0 Percent 2 4 6 Great Recession 8 U.S. -

The New Paradox of Thrift: Financialisation, Retirement Protection, and Income Polarisation in Hong Kong

China Perspectives 2014/1 | 2014 Post-1997 Hong Kong The New Paradox of Thrift: Financialisation, retirement protection, and income polarisation in Hong Kong Kim Ming Lee, Benny Ho-pong To and Kar Ming Yu Electronic version URL: http://journals.openedition.org/chinaperspectives/6363 DOI: 10.4000/chinaperspectives.6363 ISSN: 1996-4617 Publisher Centre d'étude français sur la Chine contemporaine Printed version Date of publication: 1 March 2014 Number of pages: 5-14 ISSN: 2070-3449 Electronic reference Kim Ming Lee, Benny Ho-pong To and Kar Ming Yu, « The New Paradox of Thrift: », China Perspectives [Online], 2014/1 | 2014, Online since 01 January 2017, connection on 28 October 2019. URL : http:// journals.openedition.org/chinaperspectives/6363 ; DOI : 10.4000/chinaperspectives.6363 © All rights reserved Special feature China perspectives The New Paradox of Thrift Financialisation, retirement protection, and income polarisation in Hong Kong KIM MING LEE, BENNY HO-PONG TO, AND KAR MING YU ABSTRACT: The Hong Kong SAR government has always been proud of the fact that Hong Kong retains its top ranking in terms of “mar - ket freedom” according to most international rating agencies and think tanks. What the government has been much more reluctant to recognise is that, more than 15 years after the handover, Hong Kong now also tops other developed economies in terms of income ine - quality. The growing inequality is caused, among other things, by worsening poverty among the aged. This paper attempts to provide an updated analysis of income and wealth polarisation in Hong Kong, with a particular focus on the retirement protection policy and old-age poverty. -

Philip R Lane: Determinants of the Real Interest Rate

SPEECH Determinants of the real interest rate Remarks by Philip R. Lane, Member of the Executive Board of the ECB, at the National Treasury Management Agency Dublin, 28 November 2019 Introduction It is a pleasure to address the Annual Investee and Business Leaders’ Dinner organised by the National Treasury Management Agency (NTMA).[1] I plan today to explore some of the factors determining the evolution of the real (that is, inflation-adjusted) interest rate over time. This is obviously relevant to the NTMA in its role as manager of Ireland’s national debt and also to its other business areas (Ireland Strategic Investment Fund; State Claims Agency; NewEra; National Development Finance Agency) and related entities (National Asset Management Agency; Strategic Banking Corporation of Ireland; Home Building Finance Ireland). More generally, the real interest rate is at the core of many financial valuation models, while simultaneously acting as a fundamental macroeconomic adjustment mechanism by reconciling desired savings and desired investment patterns. My primary focus today is on the real interest rate on sovereign bonds, which in turn is the baseline for pricing riskier bonds and equities through the addition of various risk premia. The real return on government bonds in advanced economies has undergone pronounced shifts over time. Chart 1 shows that, since the 1980s, the real return on sovereign debt has registered a steady decline towards levels that are low from a historical perspective. Looking at the 1970s, ex-post calculations of the real interest rate were also low during this period, since inflation turned out to be unexpectedly high. -

The Deleveraging of U.S. Households: Credit Card Debt Over the Lifecycle

2016 n Number 11 ECONOMIC Synopses The Deleveraging of U.S. Households: Credit Card Debt over the Lifecycle Helu Jiang, Technical Research Associate Juan M. Sanchez, Research Officer and Economist ggertsson and Krugman (2012) contend that “if there Total Credit Card Debt is a single word that appears most frequently in dis - $ Billions cussions of the economic problems now afflicting E 900 both the United States and Europe, that word is surely 858 865 debt.” These authors and others offer theoretical models 850 that present the debt phenomenon as follows: The econo my 800 788 792 756 is populated by impatient and patient individuals. Impatient 744 751 750 individuals borrow as much as possible, up to a debt limit. 718 When the debt limit suddenly tightens, impatient individ - 700 683 665 656 648 uals must cut expenditures to pay their debt, depressing 650 aggregate demand and generating debt-driven slumps. Such 600 a reduction in debt is called deleveraging . 2004 2005 2006 2007 2008 2009 2010 20 11 2012 2013 2014 2015 SOURCE: Federal Reserve Bank of New York Consumer Credit Panel/Equifax. Individuals younger than 46 deleveraged the most after the Share of the Change in Total Credit Card Debt financial crisis of 2008. by Age Group Percent 25 21 20 The evolution of total credit card debt around the finan - 14 14 14 15 13 11 cial crisis of 2008 appears consistent with that sequence: 8 10 6 Credit card debt increased quickly before the financial cri sis 5 1 3 3 0 and then fell for six years after that episode. -

Macro-Economics of Balance-Sheet Problems and the Liquidity Trap

Contents Summary ........................................................................................................................................................................ 4 1 Introduction ..................................................................................................................................................... 7 2 The IS/MP–AD/AS model ........................................................................................................................ 9 2.1 The IS/MP model ............................................................................................................................................ 9 2.2 Aggregate demand: the AD-curve ........................................................................................................ 13 2.3 Aggregate supply: the AS-curve ............................................................................................................ 16 2.4 The AD/AS model ........................................................................................................................................ 17 3 Economic recovery after a demand shock with balance-sheet problems and at the zero lower bound .................................................................................................................................................. 18 3.1 A demand shock under normal conditions without balance-sheet problems ................... 18 3.2 A demand shock under normal conditions, with balance-sheet problems ......................... 19 3.3 -

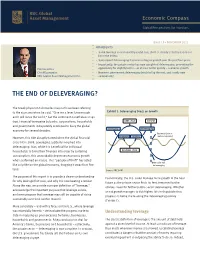

The End of Deleveraging?

Economic Compass Global Perspectives for Investors Issue 19 • NOVEMBER 2012 HIGHLIGHTS › Some leverage is economically useful, but, the U.S. clearly took this notion too far in the 2000s. › Subsequent deleveraging has been a drag on growth over the past four years. › Importantly, the private sector has now completed deleveraging, presenting the Eric Lascelles opportunity for slightly better – or at least better quality – economic growth. Chief Economist › However, government deleveraging tends to lag the rest, and is only now RBC Global Asset Management Inc. commencing. THE END OF DELEVERAGING? The Greek physicist Archimedes may not have been referring to the economy when he said, “Give me a lever long enough Exhibit 1: Deleveraging Drags on Growth and I will move the world,” but the sentiment nonetheless rings true. Financial leveraging by banks, corporations, households DEBT CYCLE PRESENT and governments indisputably combined to buoy the global Leveraging Deleveraging economy for several decades. Business Cycle in However, this tide abruptly turned when the global financial Downswing Upswing cautious upswing crisis hit in 2008. Leveraging suddenly morphed into deleveraging. Alas, while it is beneficial for individual households to bring their finances into order by curtailing BUSINESS CYCLE consumption, this unavoidably depresses economic growth when performed en masse. This “paradox of thrift” has acted Debt Cycle still like a riptide on the global economy, dragging it away from firm deleveraging land. Source: RBC GAM The purpose of this report is to provide a clearer understanding Economically, the U.S. could manage more growth in the near for why leverage first rose, and why it is now beating a retreat. -

Credit Reallocation, Deleveraging, and Financial Crises

Credit Reallocation, Deleveraging, and Financial Crises Junghwan Hyun Raoul Minetti∗ Hiroshima University Michigan State University Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the methodology proposed by Davis and Haltiwanger (1992) for measuring job reallocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit − boom preceding the 1997 crisis featured a slowdown of credit reallocation. Af- ter the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit realloca- tion. The findings suggest that the crisis and the associated reforms have triggered an efficiency-enhancing increase in the fluidity of the credit market. Keywords: Credit Reallocation, Credit Growth, Financial Crises. JEL Codes: E44 ∗Raoul Minetti: Department of Economics, 486 W. Circle Drive, 110 Marshall-Adams Hall, Michi- gan State University, East Lansing, MI 48824-1038. E-mail: [email protected] . Junghwan Hyun: gre- [email protected] . We wish to thank several seminar and conference participants for their comments and suggestions. All remaining errors are ours. 1 Credit Reallocation, Deleveraging, and Financial Crises Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the method- ology proposed by Davis and Haltiwanger (1992) for measuring job re- allocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit boom preceding − the 1997 crisis featured a slowdown of credit reallocation. After the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit reallocation.