1St View 1 January 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Observed Hurricane Wind Speed Asymmetries and Relationships to Motion and Environmental Shear

1290 MONTHLY WEATHER REVIEW VOLUME 142 Observed Hurricane Wind Speed Asymmetries and Relationships to Motion and Environmental Shear ERIC W. UHLHORN NOAA/AOML/Hurricane Research Division, Miami, Florida BRADLEY W. KLOTZ Cooperative Institute for Marine and Atmospheric Studies, Rosenstiel School of Marine and Atmospheric Science, University of Miami, Miami, Florida TOMISLAVA VUKICEVIC,PAUL D. REASOR, AND ROBERT F. ROGERS NOAA/AOML/Hurricane Research Division, Miami, Florida (Manuscript received 6 June 2013, in final form 19 November 2013) ABSTRACT Wavenumber-1 wind speed asymmetries in 35 hurricanes are quantified in terms of their amplitude and phase, based on aircraft observations from 128 individual flights between 1998 and 2011. The impacts of motion and 850–200-mb environmental vertical shear are examined separately to estimate the resulting asymmetric structures at the sea surface and standard 700-mb reconnaissance flight level. The surface asymmetry amplitude is on average around 50% smaller than found at flight level, and while the asymmetry amplitude grows in proportion to storm translation speed at the flight level, no significant growth at the surface is observed, contrary to conventional assumption. However, a significant upwind storm-motion- relative phase rotation is found at the surface as translation speed increases, while the flight-level phase remains fairly constant. After removing the estimated impact of storm motion on the asymmetry, a significant residual shear direction-relative asymmetry is found, particularly at the surface, and, on average, is located downshear to the left of shear. Furthermore, the shear-relative phase has a significant downwind rotation as shear magnitude increases, such that the maximum rotates from the downshear to left-of-shear azimuthal location. -

Waste Management Strategy for the British Virgin Islands Ministry of Health & Social Development

FINAL REPORT ON WASTE MANAGEMENT WASTE CHARACTERISATION STRATEGY FOR THE BRITISH J U L Y 2 0 1 9 VIRGIN ISLANDS Ref. 32-BV-2018Waste Management Strategy for the British Virgin Islands Ministry of Health & Social Development TABLE OF CONTENTS LIST OF ACRONYMS..............................................................................2 1 INTRODUCTION.........................................................3 1.1 BACKGROUND OF THE STUDY..........................................................3 1.2 SUBJECT OF THE PRESENT REPORT..................................................3 1.3 OBJECTIVE OF THE WASTE CHARACTERISATION................................3 2 METHODOLOGY.........................................................4 2.1 ORGANISATION AND IMPLEMENTATION OF THE WASTE CHARACTERISATION....................................................................4 2.2 LIMITATIONS AND DIFFICULTIES......................................................6 3 RESULTS...................................................................7 3.1 GRANULOMETRY.............................................................................7 3.2 GRANULOMETRY.............................................................................8 3.2.1 Overall waste composition..................................................................8 3.2.2 Development of waste composition over the years..........................11 3.2.3 Waste composition per fraction........................................................12 3.3 STATISTICAL ANALYSIS.................................................................17 -

World Bank Document

The World Bank Costa Rica Catastrophe Deferred Drawdown Option (CAT DDO) (P111926) Document of The World Bank Public Disclosure Authorized Report No: ICR00004369 IMPLEMENTATION COMPLETION AND RESULTS REPORT (IBRD-75940) ON A LOAN Public Disclosure Authorized IN THE AMOUNT OF US$65 MILLION TO THE REPUBLIC OF COSTA RICA FOR A DEVELOPMENT POLICY LOAN WITH A CATASTROPHE DEFERRED DRAWDOWN OPTION (CAT DDO) Public Disclosure Authorized October 17, 2018 Public Disclosure Authorized Social, Urban, Rural and Resilience Global Practice Central America Country Management Unit Latin America and the Caribbean Region The World Bank Costa Rica Catastrophe Deferred Drawdown Option (CAT DDO) (P111926) CURRENCY EQUIVALENTS (Exchange Rate Effective October 31, 2017) Currency Unit = Costa Rican Colones (CRC) CRC 1 = US$ 0.0018 US$1 = CRC 569.75 FISCAL YEAR January 1–December 31 ABBREVIATIONS AND ACRONYMS AyA Costa Rican National Water and Sanitation Institution (Instituto Costarricense de Acueductos y Alcantarillados) Cat DDO Catastrophe Deferred Drawdown Option CCA Climate Change Adaptation CCRIF Caribbean Catastrophe Risk Insurance Facility CEPREDENAC Coordination Center for the Prevention of Disasters in Central America and the Dominican Republic (Centro de Coordinación para la Prevención de los Desastres en America Central y República Dominicana) CNE National Commission for Risk Prevention and Emergency Management (Comisión Nacional de Prevención de Riesgos y Atención de Emergencias) Before 1999: National Emergency Commission (Comisión Nacional de Emergencia) -

The Tropic Islesbreezes

Published by On Trac Publishing, P.O. Box 985, Bradenton, FL 34206 (941) 723-5003 Tropic Isles • 1503 28th Ave. West • Palmetto, Florida 34221 • (941) 721-8888 • Website: www.TropicIsles.net Home of the Month Meet Your New Neighbors By Cindy Shaw The Tropic Isles I’d like to introduce you to our new, part-time neighbors, PAUL September and MIRIAM GROSSI. They live in their new home at 128 Capri Dr. Paul is originally from New York City, NY, but both he and Miriam now reside part-time in Millersburg, Ohio. Paul is a retired hospital administrator in Ohio and Okla- homa where he worked for 35 years. Miriam is a retired RN of 17 years and has foster parented newborns for many years. Paul and Miriam also ran a B & B in Millersburg for 13 years. They have been coming down to this area for 14 years and have been vacationing on Anna Maria Island. While on vacation, they 2017 would often ride out to Emerson Point. They would also do an exchange system with their B & B allowing interested people to September’s “Home of the Month” belongs to Tommy and stay in their B & B in exchange for staying in other peoples’ homes. Charlene Barlow at 1312 29th Ave. W. Lots of work and loving When they became interested in putting down roots, they touches, both inside and out, went into the creation of this cute began looking at vacant lots in the area where they could build little “tropical cottage”. Congratulations! a house. They went to Jacobson Homes who sent them to Tropic Isles. -

Recent Advances in Research on Tropical Cyclogenesis

Available online at www.sciencedirect.com ScienceDirect Tropical Cyclone Research and Review 9 (2020) 87e105 www.keaipublishing.com/tcrr Recent advances in research on tropical cyclogenesis Brian H. Tang a,*, Juan Fang b, Alicia Bentley a,y, Gerard Kilroy c, Masuo Nakano d, Myung-Sook Park e, V.P.M. Rajasree f, Zhuo Wang g, Allison A. Wing h, Liguang Wu i a University at Albany, State University of New York, Albany, USA b Nanjing University, Nanjing, China c Ludwig-Maximilians University of Munich, Munich, Germany d Japan Agency for Marine-Earth Science and Technology, Yokohama, Japan e Korea Institute of Ocean Science and Technology, Busan, South Korea f Centre for Atmospheric and Climate Physics Research, University of Hertfordshire, Hatfield, UK g University of Illinois, Urbana, USA h Florida State University, Tallahassee, USA i Fudan University, Shanghai, China Available online 7 May 2020 Abstract This review article summarizes recent (2014e2019) advances in our understanding of tropical cyclogenesis, stemming from activities at the ninth International Workshop on Tropical Cyclones. Tropical cyclogenesis involves the interaction of dynamic and thermodynamic processes at multiple spatio-temporal scales. Studies have furthered our understanding of how tropical cyclogenesis may be affected by external processes, such as intraseasonal oscillations, monsoon circulations, the intertropical convergence zone, and midlatitude troughs and cutoff lows. Addi- tionally, studies have furthered our understanding of how tropical cyclogenesis may be affected by internal processes, such as the organization of deep convection; the evolution of the “pouch” structure; the role of friction; the development of the moist, warm core; the importance of surface fluxes; and the role of the mid-level vortex. -

State of the Climate in 2016

STATE OF THE CLIMATE IN 2016 Special Supplement to the Bullei of the Aerica Meteorological Society Vol. 98, No. 8, August 2017 STATE OF THE CLIMATE IN 2016 Editors Jessica Blunden Derek S. Arndt Chapter Editors Howard J. Diamond Jeremy T. Mathis Ahira Sánchez-Lugo Robert J. H. Dunn Ademe Mekonnen Ted A. Scambos Nadine Gobron James A. Renwick Carl J. Schreck III Dale F. Hurst Jacqueline A. Richter-Menge Sharon Stammerjohn Gregory C. Johnson Kate M. Willett Technical Editor Mara Sprain AMERICAN METEOROLOGICAL SOCIETY COVER CREDITS: FRONT/BACK: Courtesy of Reuters/Mike Hutchings Malawian subsistence farmer Rozaria Hamiton plants sweet potatoes near the capital Lilongwe, Malawi, 1 February 2016. Late rains in Malawi threaten the staple maize crop and have pushed prices to record highs. About 14 million people face hunger in Southern Africa because of a drought that has been exacerbated by an El Niño weather pattern, according to the United Nations World Food Programme. A supplement to this report is available online (10.1175/2017BAMSStateoftheClimate.2) How to cite this document: Citing the complete report: Blunden, J., and D. S. Arndt, Eds., 2017: State of the Climate in 2016. Bull. Amer. Meteor. Soc., 98 (8), Si–S277, doi:10.1175/2017BAMSStateoftheClimate.1. Citing a chapter (example): Diamond, H. J., and C. J. Schreck III, Eds., 2017: The Tropics [in “State of the Climate in 2016”]. Bull. Amer. Meteor. Soc., 98 (8), S93–S128, doi:10.1175/2017BAMSStateoftheClimate.1. Citing a section (example): Bell, G., M. L’Heureux, and M. S. Halpert, 2017: ENSO and the tropical Paciic [in “State of the Climate in 2016”]. -

Hurricane & Tropical Storm

5.8 HURRICANE & TROPICAL STORM SECTION 5.8 HURRICANE AND TROPICAL STORM 5.8.1 HAZARD DESCRIPTION A tropical cyclone is a rotating, organized system of clouds and thunderstorms that originates over tropical or sub-tropical waters and has a closed low-level circulation. Tropical depressions, tropical storms, and hurricanes are all considered tropical cyclones. These storms rotate counterclockwise in the northern hemisphere around the center and are accompanied by heavy rain and strong winds (NOAA, 2013). Almost all tropical storms and hurricanes in the Atlantic basin (which includes the Gulf of Mexico and Caribbean Sea) form between June 1 and November 30 (hurricane season). August and September are peak months for hurricane development. The average wind speeds for tropical storms and hurricanes are listed below: . A tropical depression has a maximum sustained wind speeds of 38 miles per hour (mph) or less . A tropical storm has maximum sustained wind speeds of 39 to 73 mph . A hurricane has maximum sustained wind speeds of 74 mph or higher. In the western North Pacific, hurricanes are called typhoons; similar storms in the Indian Ocean and South Pacific Ocean are called cyclones. A major hurricane has maximum sustained wind speeds of 111 mph or higher (NOAA, 2013). Over a two-year period, the United States coastline is struck by an average of three hurricanes, one of which is classified as a major hurricane. Hurricanes, tropical storms, and tropical depressions may pose a threat to life and property. These storms bring heavy rain, storm surge and flooding (NOAA, 2013). The cooler waters off the coast of New Jersey can serve to diminish the energy of storms that have traveled up the eastern seaboard. -

The Effects of Hurricane Otto on the Soil Ecosystems of Three Forest Types in the Northern

bioRxiv preprint doi: https://doi.org/10.1101/2020.03.19.998799; this version posted March 19, 2020. The copyright holder for this preprint (which was not certified by peer review) is the author/funder, who has granted bioRxiv a license to display the preprint in perpetuity. It is made available under aCC-BY 4.0 International license. The effects of Hurricane Otto on the soil ecosystems of three forest types in the Northern Zone of Costa Rica William D. Eaton1#, Katie M. McGee2, Kiley Alderfer1¶, Angie Ramirez Jimenez1¶, and Mehrdad Hajibabaei2 1 Pace University Biology Department, One Pace Plaza, New York, NY 10038 2Biodiversity Institute of Ontario, Department of Integrative Biology, University of Guelph, 50 Stone Road East, Guelph, ON, N1G 2W1, Canada. ¶These authors contributed equally to this work # Corresponding author E-mail: [email protected] William D. Eaton Roles: Conceptualization, Formal Analysis, Funding Acquisition, Investigation, Resources, Supervision, Writing-Original Draft Preparation, Writing-Review and Editing Katie M. McGee Roles: Investigation, Formal Analysis, Writing-Original Draft Preparation, Writing-Review and Editing Kiley Alderfer Contributed equally in this work with: Kiley Aldefer and Angie Ramirez Jimenez Roles: Investigation, Formal Analysis, Writing-Original Draft Preparation Angie Ramirez Jimenez Contributed equally in this work with: Kiley Aldefer and Angie Ramirez Jimenez Roles: Investigation, Formal Analysis, Writing-Original Draft Preparation Mehrdad Hajibabaei Roles: Data Curation, Resources bioRxiv preprint doi: https://doi.org/10.1101/2020.03.19.998799; this version posted March 19, 2020. The copyright holder for this preprint (which was not certified by peer review) is the author/funder, who has granted bioRxiv a license to display the preprint in perpetuity. -

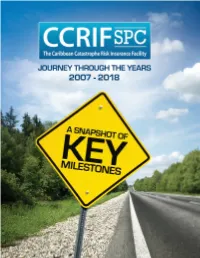

CCRIFSPC Journey Through T

CCRIF receives the ‘Reinsurance Initiative of the Year’ Award for the reinsurance initiative that generated the most promising CARICOM Heads of Government approach change to a signifi cant area of the World Bank for assistance to design business – the award was offered and implement a cost-effective risk transfer by The Review, the leading programme for member governments magazine of the international reinsurance industry Hurricane Ivan causes CCRIF makes payout to Turks and billions of dollars of losses Caicos Islands for Hurricane Ike across the Caribbean CCRIF makes the Real-Time Forecasting System (RTFS) available CCRIF is named to members for the fi rst ‘Transaction of time – each year it is the Year’ at the available to members Insurance Day at the beginning of London Market the Atlantic Hurricane Awards Season 2007 2004 2008 The Caribbean Catastrophe Risk Insurance Facility is formed as the fi rst multi-country, multi-peril pooled catastrophe risk insurance facility in the world A Multi-donor Trust Fund (MDTF) is established to support CCRIF’s initial operations CCRIF signs fi rst MOU with the Caribbean Institute CCRIF provides tropical cyclone (hurricane) and earthquake for Meteorology and Hydrology (CIMH) – over the coverage to 16 Caribbean member governments years, CCRIF has signed MOUs with the Caribbean Community Climate Change Centre (CCCCC), United Nations Economic Commission for Latin America and the Caribbean (ECLAC), Caribbean Disaster Emergency Management Agency (CDEMA), Inter- American Development Bank (IDB), University -

UNDP – Financing for Development Challenges in Caribbean SIDS

United Nations Development Programme FINANCING FOR DEVELOPMENT CHALLENGES IN CARIBBEAN SIDS A CASE FOR REVIEW OF ELIGIBILITY CRITERIA FOR ACCESS TO CONCESSIONAL FINANCING Report Prepared for the United Nations Development Programme by Professor Compton Bourne assisted by Megan Alexander, Daren Conrad and Julia Jhinkoo A Publication of the UNDP Trinidad & Tobago Country Office FINANCING FOR DEVELOPMENT CHALLENGES IN CARIBBEAN SIDS A CASE FOR REVIEW OF ELIGIBILITY CRITERIA FOR ACCESS TO CONCESSIONAL FINANCING Report Prepared for the United Nations Development Programme by Professor Compton Bourne assisted by Megan Alexander, Daren Conrad and Julia Jhinkoo June 2015 Financing for Development Challenges in Caribbean SIDS: A Case for Review of Eligibility Criteria for Access to Concessional Financing Copyright 2015 by the United Nations Development Programme UN House, 3A Chancery Lane, Port of Spain, Trinidad and Tobago All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior permission. Website: www.tt.undp.org Printed in Trinidad and Tobago by the Multi Media Production Centre, The University of the West Indies, St. Augustine Campus For a list of any errors or omissions found subsequent to printing please visit our website www.tt.undp.org Acknowledgements Financial support for this publication was provided by UNDP’s Regional Bureau for Latin America and the Caribbean. The paper benefited from guidance and comments provided by a number of people and the authors would like to thank them for their inputs. These people include: Alison Drayton, George Gray Molina, Craig Hawke, Gail Hurley, Stacy Richards-Kennedy and Kenroy Roach. -

1 a Hyperactive End to the Atlantic Hurricane Season: October–November 2020

1 A Hyperactive End to the Atlantic Hurricane Season: October–November 2020 2 3 Philip J. Klotzbach* 4 Department of Atmospheric Science 5 Colorado State University 6 Fort Collins CO 80523 7 8 Kimberly M. Wood# 9 Department of Geosciences 10 Mississippi State University 11 Mississippi State MS 39762 12 13 Michael M. Bell 14 Department of Atmospheric Science 15 Colorado State University 16 Fort Collins CO 80523 17 1 18 Eric S. Blake 19 National Hurricane Center 1 Early Online Release: This preliminary version has been accepted for publication in Bulletin of the American Meteorological Society, may be fully cited, and has been assigned DOI 10.1175/BAMS-D-20-0312.1. The final typeset copyedited article will replace the EOR at the above DOI when it is published. © 2021 American Meteorological Society Unauthenticated | Downloaded 09/26/21 05:03 AM UTC 20 National Oceanic and Atmospheric Administration 21 Miami FL 33165 22 23 Steven G. Bowen 24 Aon 25 Chicago IL 60601 26 27 Louis-Philippe Caron 28 Ouranos 29 Montreal Canada H3A 1B9 30 31 Barcelona Supercomputing Center 32 Barcelona Spain 08034 33 34 Jennifer M. Collins 35 School of Geosciences 36 University of South Florida 37 Tampa FL 33620 38 2 Unauthenticated | Downloaded 09/26/21 05:03 AM UTC Accepted for publication in Bulletin of the American Meteorological Society. DOI 10.1175/BAMS-D-20-0312.1. 39 Ethan J. Gibney 40 UCAR/Cooperative Programs for the Advancement of Earth System Science 41 San Diego, CA 92127 42 43 Carl J. Schreck III 44 North Carolina Institute for Climate Studies, Cooperative Institute for Satellite Earth System 45 Studies (CISESS) 46 North Carolina State University 47 Asheville NC 28801 48 49 Ryan E. -

Pdf | 211.33 Kb

REDLAC Weekly Note on Emergencies Latin America & the Caribbean This note is compiled for The Risk Emergency Disaster Working Group for Latin America and the Caribbean (REDLAC) by the OCHA Regional Office through disaster monitoring and input from our Regional Humanitarian partners. This note does not intend to be an analytical tool, but a summary paper of key facts and actions reported by the sources indicated. Activities carried out in affected countries are not limited to the ones reported here. Please check with sources for further information. For input, feedback and suggestions send us an email to [email protected] HIGHLIGHTS: HAITI: More than 3 thousand people affected by cholera, 250 dead. NICARAGUA: Increase in the cases of leptospirosis. 58 per cent are in León. BELIZE, HONDURAS and MEXICO: Hurricane Richard causes damages in Belize and Honduras and Mexico is on alert. PERU: Flooding in Cusco affects 120 families. Year 3 - Volume 180 25 October 2010 EPIDEMIC CHOLERA IN HAITI: Approximately 250 people have died and 3,100 are ill due to cholera. The most severe cases are in Saint-Marc, Grande-Saline, Mirebalais and Arcahaie. It is estimated that 150 thousand people live in the affected zones. The Government issued a state of sanitary emergency for the country. Authorities in the Dominican Republic installed health centres as sanitation filters to avoid the spreading of the disease and to maintain control of the sale of food in the border. The authorities, together with humanitarian workers, are working to keep the disease from spreading to refugee camps in the capital, where 1.5 million people have been living since the earthquake last January.