History of Retailing in North America

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

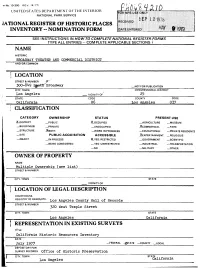

Jational Register of Historic Places Inventory -- Nomination Form

•m No. 10-300 REV. (9/77) UNITED STATES DEPARTMENT OF THE INTERIOR NATIONAL PARK SERVICE JATIONAL REGISTER OF HISTORIC PLACES INVENTORY -- NOMINATION FORM SEE INSTRUCTIONS IN HOW TO COMPLETE NATIONAL REGISTER FORMS ____________TYPE ALL ENTRIES -- COMPLETE APPLICABLE SECTIONS >_____ NAME HISTORIC BROADWAY THEATER AND COMMERCIAL DISTRICT________________________ AND/OR COMMON LOCATION STREET & NUMBER <f' 300-8^9 ^tttff Broadway —NOT FOR PUBLICATION CITY. TOWN CONGRESSIONAL DISTRICT Los Angeles VICINITY OF 25 STATE CODE COUNTY CODE California 06 Los Angeles 037 | CLASSIFICATION CATEGORY OWNERSHIP STATUS PRESENT USE X.DISTRICT —PUBLIC ^.OCCUPIED _ AGRICULTURE —MUSEUM _BUILDING(S) —PRIVATE —UNOCCUPIED .^COMMERCIAL —PARK —STRUCTURE .XBOTH —WORK IN PROGRESS —EDUCATIONAL —PRIVATE RESIDENCE —SITE PUBLIC ACQUISITION ACCESSIBLE ^ENTERTAINMENT _ REUGIOUS —OBJECT _IN PROCESS 2L.YES: RESTRICTED —GOVERNMENT —SCIENTIFIC —BEING CONSIDERED — YES: UNRESTRICTED —INDUSTRIAL —TRANSPORTATION —NO —MILITARY —OTHER: NAME Multiple Ownership (see list) STREET & NUMBER CITY. TOWN STATE VICINITY OF | LOCATION OF LEGAL DESCRIPTION COURTHOUSE. REGISTRY OF DEEDSETC. Los Angeie s County Hall of Records STREET & NUMBER 320 West Temple Street CITY. TOWN STATE Los Angeles California ! REPRESENTATION IN EXISTING SURVEYS TiTLE California Historic Resources Inventory DATE July 1977 —FEDERAL ^JSTATE —COUNTY —LOCAL DEPOSITORY FOR SURVEY RECORDS office of Historic Preservation CITY, TOWN STATE . ,. Los Angeles California DESCRIPTION CONDITION CHECK ONE CHECK ONE —EXCELLENT —DETERIORATED —UNALTERED ^ORIGINAL SITE X.GOOD 0 —RUINS X_ALTERED _MOVED DATE- —FAIR _UNEXPOSED DESCRIBE THE PRESENT AND ORIGINAL (IF KNOWN) PHYSICAL APPEARANCE The Broadway Theater and Commercial District is a six-block complex of predominately commercial and entertainment structures done in a variety of architectural styles. The district extends along both sides of Broadway from Third to Ninth Streets and exhibits a number of structures in varying condition and degree of alteration. -

Target Corporation

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Honors Theses, University of Nebraska-Lincoln Honors Program Spring 4-7-2019 Strategic Audit: Target Corporation Andee Capell University of Nebraska - Lincoln Follow this and additional works at: https://digitalcommons.unl.edu/honorstheses Part of the Accounting Commons, and the Strategic Management Policy Commons Capell, Andee, "Strategic Audit: Target Corporation" (2019). Honors Theses, University of Nebraska- Lincoln. 192. https://digitalcommons.unl.edu/honorstheses/192 This Thesis is brought to you for free and open access by the Honors Program at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Honors Theses, University of Nebraska-Lincoln by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. Strategic Audit: Target Corporation An Undergraduate Honors Thesis Submitted in Partial fulfillment of University Honors Program Requirements University of Nebraska-Lincoln by Andee Capell, BS Accounting College of Business April 7th, 2019 Faculty Mentor: Samuel Nelson, PhD, Management Abstract Target Corporation is a notable publicly traded discount retailer in the United States. In recent years they have gone through significant changes including a new CEO Brian Cornell and the closing of their Canadian stores. With change comes a new strategy, which includes growing stores in the United States. In order to be able to continue to grow Target should consider multiple strategic options. Using internal and external analysis, while examining Target’s profitability ratios recommendations were made to proceed with their growth both in profit and capacity. After recommendations are made implementation and contingency plans can be made. Key words: Strategy, Target, Ratio(s), Plan 1 Table of Contents Section Page(s) Background information …………………..…………………………………………….…..…...3 External Analysis ………………..……………………………………………………..............3-5 a. -

What Is a Warehouse Club?

What is a Warehouse Club? The principle operators in the warehouse club industry are BJ’s Wholesale, Cost-U-Less, Costco Wholesale, PriceSmart and Sam’s Club. These five companies follow the basic warehouse club principles developed by Sol and Robert Price, who founded the warehouse club industry when they opened the first Price Club in San Diego, California in 1976. However, the five warehouse club operators have adapted those basic concepts to today’s retail environment. This chapter provides an explanation of the key characteristics of a warehouse club in 2010. Overall Description A warehouse club offers its paid members low prices on a limited selection of nationally branded and private label merchandise within a wide range of product categories (see picture on the right of Mott’s sliced apples at BJ’s). Rapid inventory turnover, high sales volume and reduced operating costs enable warehouse clubs to operate at lower gross margins (8% to 14%) than discount chains, supermarkets and supercenters, which operate on gross margins of 20% to 40%. BJ’s – Mott’s Sliced Apples Overall Operating Philosophy When it comes to buying and merchandising, the warehouse clubs follow the same simple and straightforward six-point philosophy that was originated by Sol Price: 1. Purchase quality merchandise. 2. Purchase the right merchandise at the right time. 3. Sell products at the lowest possible retail price. 4. Merchandise items in a clean, undamaged condition. 5. Merchandise products in the right location. 6. Stock items with the correct amount of inventory, making sure that supply is not excessive. In 1983, Joseph Ellis, an analyst at Goldman Sachs, summarized the warehouse club operating philosophy in a meaningful and relevant way. -

St John's University Undergraduate Student Managed Investment Fund Presents: Target Corporation Stock Analysis November 11, 20

St John’s University Undergraduate Student Managed Investment Fund Presents: Target Corporation Stock Analysis November 11, 2003 Recommendation: Purchase 300 shares of Target stock at market value Industry: Retail Analysts: Jennifer Tang – [email protected] Michael Vida – [email protected] Share Data: Fundamentals: Price - $39.15 P/E (2/03) – 21.63 Date – November 6, 2003 P/E (2/04E) – 21.96 Target Price – $44.58 P/E (2/05E) – 22.95 52 Week Price Range – $25.60 - $41.80 Book Value/Share – $11.03 Market Capitalization – $35.40 billion Price/Book Value – $3.60 Revenue 2002 – $43.917 billion Dividend Yield – 0.72% Projected EPS Growth – 15% Shares Outstanding – 910.9 million ROE 2002 – 17.51% Stock Chart: Executive Summary After analyzing Target Corp’s financials, industry and future outlook, we recommend the purchase of 300 shares of the company’s stock at market order. As a leading discount retailer, only behind Walmart, Target has made considerable growth in the industry over the past few years. Target offers an array of merchandise from women’s apparel, household products, toys and even food. One of the strengths of Target lies in its development of private brands, which helps create a strong image of the store in the customers’ minds. The company is able to further lower its costs through direct sourcing, buying merchandise at lower prices and strengthening its bargaining position with suppliers. While Target Corp hasn’t seen as much success with its other operations of Marshall Fields and Mervyn’s as it has with its namesake store, the company plans to invest resources into these two areas to turn around results. -

1 Draft Paper Elisabete Mendes Silva Polytechnic Institute of Bragança

Draft paper Elisabete Mendes Silva Polytechnic Institute of Bragança-Portugal University of Lisbon Centre for English Studies, Faculty of Arts and Humanities, Portugal [email protected] Power, cosmopolitanism and socio-spatial division in the commercial arena in Victorian and Edwardian London The developments of the English Revolution and of the British Empire expedited commerce and transformed the social and cultural status quo of Britain and the world. More specifically in London, the metropolis of the country, in the eighteenth century, there was already a sheer number of retail shops that would set forth an urban world of commerce and consumerism. Magnificent and wide-ranging shops served householders with commodities that mesmerized consumers, giving way to new traditions within the commercial and social fabric of London. Therefore, going shopping during the Victorian Age became mandatory in the middle and upper classes‟ social agendas. Harrods Department store opens in 1864, adding new elements to retailing by providing a sole space with a myriad of different commodities. In 1909, Gordon Selfridge opens Selfridges, transforming the concept of urban commerce by imposing a more cosmopolitan outlook in the commercial arena. Within this context, I intend to focus primarily on two of the largest department stores, Harrods and Selfridges, drawing attention to the way these two spaces were perceived when they first opened to the public and the effect they had in the city of London and in its people. I shall discuss how these department stores rendered space for social inclusion and exclusion, gender and race under the spell of the Victorian ethos, national conservatism and imperialism. -

2017 Warehouse Club Industry Guide

2017 Warehouse Club Industry Guide BJs.com Costco.com 7 1 0 2 , 2 2 SamsClub.com y a M — te a D CostULess.come PriceSmart.com s a le e R HHC Publishing, Inc.— Providing Club Industry Data, Information and Analysis since 1997 Online access and/or book delivery for the 2017 Warehouse Club Industry Guide Order Form will occur by May 22, 2017. These PRE PUBLICATION discounts expire May 15, 2017. ONE Version Option TWO Version Option Save Purchase either Save Purchase both Save up $200 the print or $300 the print and online version online versions to $300 and pay $599, a $200 and pay $699, a $300 discount off the everyday discount off the everyday price of $799. price of $999. ORDER ONE Version Order—Check One TWO Version Order—Check Box $599 Book Online $699 Book and Online DELIVERY AND PAYMENT Name To get your 2017 Warehouse Club Industry Guide, simply Title/Position complete this form and return it to: HHC Publishing, Inc. Company PO Box 9138 Foxboro, MA 02035-9138 Address 617-770-0102 City, State, Zip You can also fax the completed form to: Telephone, Email 617-479-4961 Invoice Me Check Enclosed UNCONDITIONAL MONEY BACK GUARANTEE American Express MasterCard Visa If you are not completely Credit Card Number satisfied with the 2017 Warehouse Club Industry Expiration Date & Guide, you are entitled to a full Signature refund. March 17, 2017 Volume 21, Issue 473 WAREHOUSE CLUB FOCUS Costco February Sales—5. Costco MVM Program—7. 1 For 21 years, your best source for information about the clubs. -

Building Blocks

The Essential Resource for Today’s Busy Insolvency Professional Building Blocks BY LISA LAUKITIS AND EDWARD P. MAHANEY-WALTER1 Precedent in Bankruptcy Cases lthough all lawyers use precedent, few have are precedential: “parts ... that focus on the legal considered its nature and effect closely. To questions actually presented ... and decided ... the Ahelp, in 2016, Bryan Garner, editor-in-chief ‘court’s determination of a matter of law pivotal to of Black’s Law Dictionary, published, for a general- its decision.’” Everything else is “dicta” and not ist legal audience, The Law of Judicial Precedent. binding law. With limited exceptions, precedent is He had 12 appellate judges as co-authors, includ- either strictly binding — obliging judges to follow ing now-Supreme Court Justices Neil Gorsuch and it even when they disagree — or not binding, but Brett Kavanaugh.2 It is the first hornbook on prece- instead persuasive.6 dent since 1912.3 According to Garner, “This tricky If a logical predicate of a holding is not explicit Lisa Laukitis subject is dealt with to a degree, but not thoroughly, but was clearly briefed, it can be an “implicit hold- Skadden, Arps, Slate, Meagher & Flom LLP in legal-methods courses, and then it’s discussed ing” that has precedential force, but generally a New York occasionally throughout law school. But it’s such court’s assumptions — accurate or not — are not an important subject that it needs a full, system- precedent: “[P]recedent is limited to the points of atic treatment. That was the inspiration — because law raised by the record, considered by the court, writings about it are often exceedingly narrow, and and determined by the outcome.” Issues not consid- they’re scattered among the law reviews.”4 ered by the court do not create precedent. -

Case No. DSP-15020-01 Capital Plaza Walmart Applicant

Case No. DSP-15020-01 Capital Plaza Walmart Applicant: Walmart Real Estate Business Trust FINAL DECISION ― DISAPPROVAL OF DETAILED SITE PLAN Detailed Site Plan 15020-01 (“DSP”), to construct a 35,287 square foot expansion to combine certain uses in the C-S-C Zone, is DISAPPOVED.1 FINDINGS OF FACT AND CONCLUSIONS OF LAW I. Procedural and Factual Background2 In September 2014, Walmart filed an application for a DSP with the Planning Department to expand its existing 144,227 square foot department store/retail “use”3 by 35,287 square 1 See the Land Use Article Section 25-210 (“LU”), Md. Ann. Code (2012 Ed. & Supp. 2015), the Prince George’s County Code, Subtitle 27, Section 27-290 (“PGCC”) (2015), and Cnty. Council of Prince George’s Cnty. v. Zimmer Dev. Co., 444 Md. 490; 120 A.3d 677 (2015) (The District Council is expressly authorized to review a final decision of the county planning board to approve or disapprove a detailed site plan and the District Council’s review results in a final decision). 2 The District Council may take judicial notice of any evidence contained in the record of any earlier phase of the approval process relating to all or a portion of the same property, including the approval of a preliminary plat of subdivision. See PGCC § 27-141. The District Council may also take administrative notice of facts of general knowledge, technical or scientific facts, laws, ordinances and regulations. It shall give effect to the rules of privileges recognized by law. The District Council may exclude incompetent, irrelevant, immaterial or unduly repetitious evidence. -

Membership Wholesale Clubs: a Low-Price Alternative

The Food Industry: Changing With the Times Membership Wholesale Clubs: A Low-Price Alternative Walter Epps and Judy Putnam (202) 786-1866 ffered the choice of paying $3.29 or posted wholesale prices, about 5 percent in O $2.79 for a 12-pack case of 12-ounce 1985. Pepsi's, obviously most buyers would Most wholesale clubs stock 4,000 to choose the lower price. This price appeal 6,000 items. This compares with up to goes a long way toward explaining the 25,000 items offered by conventional super meteoric ·rise of wholesale clubs-fully com markets and 30,000 to 50,000 items stocked puterized "no-frills" operations offering a by traditional discount stores. However, a limited selection of first quality, name-brand club's range of items is broad-from micro merchandise to smalJ businesses and select wave ovens to plastic trash bags. Within ed groups of consumers. any product category, clubs stock only a Today's clubs trace their lineage to the couple of fast-moving, welJ-known brands. cash-and-carry operations started more than Grocery items account for 40 to 60 percent 50 years ago by wholesale food distributors of clubs' sales, with general merchandise to serve their smalJ business customers who making up the remainder. couldn't buy in large quantities. As the Included in their food lines are canned name implies, customers pay cash at these peas, trout fillets, and frozen french fries. outlets and assume responsibility for receipt In short, there is the range of products, and delivery of their order, thus avoiding though not the variety of brands and sizes distributor service charges. -

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

PIPELINE FOODS, LLC, Et Al.,1 Debtors

Case 21-11002-KBO Doc 289 Filed 08/13/21 Page 1 of 9 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ) In re: ) Chapter 11 ) PIPELINE FOODS, LLC, et al.,1 ) Case No. 21-11002 (KBO) ) Debtors. ) Jointly Administered ) ) Hearing Date: August 20, 2021 at 12:00 p.m. (ET) (Requested) ) Objection Deadline: August 19, 2021 at 12:00 p.m. ) (ET) (Requested) MOTION OF THE DEBTORS FOR ENTRY OF AN ORDER AUTHORIZING THE REJECTION OF CONTRACT WITH CERES CONSULTING LLC Pipeline Foods, LLC (“Pipeline Foods”) and its affiliated debtors and debtors in possession (collectively, the “Debtors”) in the above-captioned chapter 11 cases (the “Chapter 11 Cases”), by and through their undersigned counsel, file this motion (the “Motion”) for entry of an order, substantially in the form attached hereto as Exhibit A (the “Proposed Order”), pursuant to section 365(a) of title 11 of the United States Code (the “Bankruptcy Code”), authorizing the Debtors to reject that certain shipping contract between the Debtors and Ceres Consulting L.L.C. (“Ceres”) dated May 21, 2021, a copy of which is attached hereto as Exhibit B (the “Rejected Shipping Contract”), effective as of the date of this Motion (the “Rejection Effective Date”). In support of this Motion, the Debtors respectfully state as follows: 1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification number, are: Pipeline Foods, LLC (5070); Pipeline Holdings, LLC (5754); Pipeline Foods Real Estate Holding Company, LLC (7057); Pipeline Foods, ULC (3762); Pipeline Foods Southern Cone S.R.L. -

Deloitte Studie

Global Powers of Retailing 2018 Transformative change, reinvigorated commerce Contents Top 250 quick statistics 4 Retail trends: Transformative change, reinvigorated commerce 5 Retailing through the lens of young consumers 8 A retrospective: Then and now 10 Global economic outlook 12 Top 10 highlights 16 Global Powers of Retailing Top 250 18 Geographic analysis 26 Product sector analysis 30 New entrants 33 Fastest 50 34 Study methodology and data sources 39 Endnotes 43 Contacts 47 Global Powers of Retailing identifies the 250 largest retailers around the world based on publicly available data for FY2016 (fiscal years ended through June 2017), and analyzes their performance across geographies and product sectors. It also provides a global economic outlook and looks at the 50 fastest-growing retailers and new entrants to the Top 250. This year’s report will focus on the theme of “Transformative change, reinvigorated commerce”, which looks at the latest retail trends and the future of retailing through the lens of young consumers. To mark this 21st edition, there will be a retrospective which looks at how the Top 250 has changed over the last 15 years. 3 Top 250 quick statistics, FY2016 5 year retail Composite revenue growth US$4.4 net profit margin (Compound annual growth rate CAGR trillion 3.2% from FY2011-2016) Aggregate retail revenue 4.8% of Top 250 Minimum retail Top 250 US$17.6 revenue required to be retailers with foreign billion among Top 250 operations Average size US$3.6 66.8% of Top 250 (retail revenue) billion Composite year-over-year retail 3.3% 22.5% 10 revenue growth Composite Share of Top 250 Average number return on assets aggregate retail revenue of countries with 4.1% from foreign retail operations operations per company Source: Deloitte Touche Tohmatsu Limited.