How Will the Royal Ahold Purchase of Pathmark Supermarkets Affect Prices?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Federal Retail Pharmacy Partnership Strategy for COVID-19 Vaccination for General Public Program Summary of Program for Jurisdictions

December 2, 2020 Federal Retail Pharmacy Partnership Strategy for COVID-19 Vaccination for General Public Program Summary of Program for Jurisdictions The U.S. Department of Health and Human Services and the Centers for Disease Control and Prevention are partnering with pharmacies to increase access to COVID-19 vaccine once one or more vaccines are authorized by the U.S. Food and Drug Administration for use in the United States. There are two federal pharmacy programs: The Pharmacy Partnership for Long-Term Care Program and the Federal Retail Pharmacy Partnership Strategy for COVID-19 Vaccination. Through the Federal Retail Pharmacy Partnership Strategy for COVID-19 Vaccination, retail pharmacy partners can help jurisdictions augment access to vaccine when supply increases and vaccine is recommended beyond the initial populations. With more than 90% of people in the United States living within five miles of a pharmacy, pharmacies have unique reach and ability to provide access to COVID-19 vaccine and support broad vaccination efforts. This program will provide critical vaccination services for the U.S. population, with vaccine administered at store locations at no cost to recipients. The program will be implemented in close coordination with jurisdictions to ensure optimal COVID-19 vaccination coverage and vaccine access nationwide. Program activation will be on a national scale, with select pharmacy partners receiving a direct allocation of COVID- 19 vaccine. Timing and scale of activation (how many partners, how many stores) will depend on various factors, including supply. The federal retail pharmacy program does not include every pharmacy in the United States. Pharmacies not included in the federal program will need to coordinate with their jurisdictions to become COVID- 19 vaccination providers. -

Stimulating Supermarket Development in Maryland

STIMULATING SUPERMARKET DEVELOPMENT IN MARYLAND A report of the Maryland Fresh Food Retail Task Force Task Force Baltimore Development Maryland Department of Maryland Family Network Safeway Inc. Members Corporation Agriculture Linda Ramsey, Deputy Director Greg Ten Eyck, Director of Public Will Beckford, Executive Director Joanna Kille, Director of of Family Support Affairs and Government Relations of Commercial Revitalization Government Relations Margaret Williams, Executive (Task force co-chair) Advocates for Children Kristen Mitchell, Senior Economic Mark Powell, Chief of Marketing Director and Youth Development Officer and Agribusiness Development Santoni’s Super Market Becky Wagner, Executive Director Leon Pinkett, Senior Economic Maryland Food Bank Rob Santoni, Owner (Task force co-chair and Development Officer Maryland Department of Deborah Flateman, CEO convening partner) Business and Economic Saubel’s Markets Bank of America Development Maryland Governor’s Office Greg Saubel, President Ahold USA Brooke Hodges, Senior Vice Victor Clark, Program Manager, for Children Tom Cormier, Director, President Office of Small Business Christina Drushel, Interagency Supervalu Government Affairs Dominick Murray, Deputy Prevention Specialist Tim Parks, Area Sales Director, B. Green Co. Secretary Eastern Region Angels Food Market Benjy Green, CEO Maryland Hunger Solutions Walt Clocker, Owner and Chairman Maryland Department of Cathy Demeroto, Director The Association of Baltimore of the Maryland Retailers CommonHealth ACTION Health and Mental -

Chapter 3: Socioeconomic Conditions

Chapter 3: Socioeconomic Conditions A. INTRODUCTION This chapter analyzes whether the proposed actions would result in changes in residential and economic activity that would constitute significant adverse socioeconomic impacts as defined by the City Environmental Quality Review (CEQR) Technical Manual.1 The proposed actions would result in the redevelopment of an underutilized site with an approximately 214,000- square-foot (sf), 60-foot-tall commercial building currently anticipated to be a BJ’s Wholesale Club along with up to three other retail stores on the second level, 690 parking spaces, and approximately 2.4 acres of publicly accessible waterfront open space. The Brooklyn Bay Center site (“project site”) is located at 1752 Shore Parkway between Shore Parkway South to the east, Gravesend Bay (Lower New York Bay) to the west, and between the prolongation of 24th Avenue to the north and the prolongation of Bay 37th Street to the south. The objective of the socioeconomic conditions analysis is to determine if the introduction of the retail uses planned under the proposed actions would directly or indirectly impact population, housing stock, or economic activities in the local study area or in the larger retail trade area. Pursuant to the CEQR Technical Manual, significant impacts could occur if an action meets one or more of the following tests: (1) if the action would lead to the direct displacement of residents such that the socioeconomic profile of the neighborhood would be substantially altered; (2) if the action would lead to the displacement of substantial numbers of businesses or employees, or would displace a business that plays a critical role in the community; (3) if the action would result in substantial new development that is markedly different from existing uses in a neighborhood; (4) if the action would affect real estate market conditions not only on the site anticipated to be developed, but in a larger study area; or (5) if the action would have a significant adverse effect on economic conditions in a specific industry. -

1 Venditore 1500 W Chestnut St Washington, Pa 15301 1022

1 VENDITORE 1022 MARSHALL ENTERPRISES 10TH STREET MARKET 1500 W CHESTNUT ST INC 802 N 10TH ST WASHINGTON, PA 15301 1022-24 N MARSHALL ST ALLENTOWN, PA 18102 PHILADELPHIA, PA 19123 12TH STREET CANTINA 15TH STREET A-PLUS INC 1655 SUNNY I INC 913 OLD YORK RD 1501 MAUCH CHUNK RD 1655 S CHADWICK ST JENKINTOWN, PA 19046 ALLENTOWN, PA 18102 PHILADELPHIA, PA 19145 16781N'S MARKET 16TH STREET VARIETY 17 SQUARE THIRD ST PO BOX 155 1542 TASKER ST 17 ON THE SQUARE NU MINE, PA 16244 PHILADELPHIA, PA 19146 GETTYSBURG, PA 17325 1946 WEST DIAMOND INC 1ST ORIENTAL SUPERMARKET 2 B'S COUNTRY STORE 1946 W DIAMOND ST 1111 S 6TH ST 2746 S DARIEN ST PHILADELPHIA, PA 19121 PHILADELPHIA, PA 19147 PHILADELPHIA, PA 19148 20674NINE FARMS COUNTRY 220 PIT STOP 22ND STREET BROTHER'S STORE 4997 US HIGHWAY 220 GROCERY 1428 SEVEN VALLEYS RD HUGHESVILLE, PA 17737 755 S 22ND ST YORK, PA 17404 PHILADELPHIA, PA 19146 2345 RIDGE INC 25TH STREET MARKET 26TH STREET GROCERY 2345 RIDGE AVE 2300 N 25TH ST 2533 N 26TH ST PHILADELPHIA, PA 19121 PHILADELPHIA, PA 19132 PHILADELPHIA, PA 19132 2900-06 ENTERPRISES INC 3 T'S 307 MINI MART 2900-06 RIDGE AVE 3162 W ALLEGHENY AVE RTE 307 & 380 PHILADELPHIA, PA 19121 PHILADELPHIA, PA 19132 MOSCOW, PA 18444 40 STOP MINI MARKET 40TH STREET MARKET 414 FIRST & LAST STOP 4001 MARKET ST 1013 N 40TH ST RT 414 PHILADELPHIA, PA 19104 PHILADELPHIA, PA 19104 JERSEY MILL, PA 17739 42 FARM MARKET 46 MINI MARKET 4900 DISCOUNT ROUTE 42 4600 WOODLAND AVE 4810 SPRUCE ST UNITYVILLE, PA 17774 PHILADELPHIA, PA 19143 PHILADELPHIA, PA 19143 5 TWELVE FOOD MART 52ND -

Loyalty Programs Krasdale Foods, Ken Krasne, CEO Phillip A

Communication Partners Worldwide, Inc. 12/9/17 Krasdale Foods: CTOWN Supermarkets Marketing & Loyalty Programs Krasdale Foods, Ken Krasne, CEO Phillip A. Schein, President CONFIDENTIAL 2005 Confidential Page 1 Communication Partners Worldwide, Inc. 12/9/17 Market Segment and Demographics: “Asians and Hispanics are wealthier than expected and underserved. Children also made the news – good and bad. The good news is their buying power is substantial and their influencing role as well. The bad news is they are obese…so selling to them more may not contribute to their longevity as customers”. [1] “Seniors and single-person households were also recognized as viable target groups because of their spending power, fueling interest among manufacturers for smaller sizes”. [1] Advertising to Growing Hispanic Market: “According to the 2000 Census Report, Hispanic Americans constitute a bigger, more dispersed, and more affluent market than previously predicted. The number of US Hispanics grew by 58% in the past decade to 35.3 million…buying power increased 118% to $452 billion (dramatically exceeding the the 68% growth in non- Hispanic buying power).” [1] Convenience and Price Critical: Brand loyalty varied significantly by category and their convenience and price drive store selections: • 37% - 24 hour operations a reason to shop a particular store • 21% - FSP • 52% - sale items and coupons “The challenges for retailers is to keep prices low while maintaining a high-value image and differentiating themselves from each other…and Wal-Mart.” [1] How Shoppers Really Feel About Advertising Inserts and Circulars: “According to Consumer Focus 2002…advertising inserts are effective marketing. Specifically 86% say trhey read inserts…” [1] 1. -

NGA Retailer Membership List October 2013

NGA Retailer Membership List October 2013 Company Name City State 159-MP Corp. dba Foodtown Brooklyn NY 2945 Meat & Produce, Inc. dba Foodtown Bronx NY 5th Street IGA Minden NE 8772 Meat Corporation dba Key Food #1160 Brooklyn NY A & R Supermarkets, Inc. dba Sav-Mor Calera AL A.J.C.Food Market Corp. dba Foodtown Bronx NY ADAMCO, Inc. Coeur D Alene ID Adams & Lindsey Lakeway IGA dba Lakeway IGA Paris TN Adrian's Market Inc. dba Adrian's Market Hopwood PA Akins Foods, Inc. Spokane Vly WA Akins Harvest Foods- Quincy Quincy WA Akins Harvest Foods-Bonners Ferry Bonner's Ferry ID Alaska Growth Business Corp. dba Howser's IGA Supermarket Haines AK Albert E. Lees, Inc. dba Lees Supermarket Westport Pt MA Alex Lee, Inc. dba Lowe's Food Stores Inc. Hickory NC Allegiance Retail Services, LLC Iselin NJ Alpena Supermarket, Inc. dba Neimans Family Market Alpena MI American Consumers, Inc. dba Shop-Rite Supermarkets Rossville GA Americana Grocery of MD Silver Spring MD Anderson's Market Glen Arbor MI Angeli Foods Company dba Angeli's Iron River MI Angelo & Joe Market Inc. Little Neck NY Antonico Food Corp. dba La Bella Marketplace Staten Island NY Asker's Thrift Inc., dba Asker's Harvest Foods Grangeville ID Autry Greer & Sons, Inc. Mobile AL B & K Enterprises Inc. dba Alexandria County Market Alexandria KY B & R Stores, Inc. dba Russ' Market; Super Saver, Best Apple Market Lincoln NE B & S Inc. - Windham IGA Willimantic CT B. Green & Company, Inc. Baltimore MD B.W. Bishop & Sons, Inc. dba Bishops Orchards Guilford CT Baesler's, Inc. -

Food & Beverage

Supply Chain Assets Asset Industry Clusters Legend Cold Storage Packaging Consulting/Services Transportation/ Warehouse/Trucking Food & Beverage Engineering New York Loves Food Industry connects the agribusiness industry to the academia, R&D, and food manufacturing resources needed Equipment Highway to be successful in the United States. Manufactured Ingredients Rail Labs POTSDAM CANADA NEW YORK LAKE ONTARIO TORONTO ROCHESTER NIAGARA FALLS SYRACUSE UTICA BATAVIA CANANDAIGUA ALBANY BUFFALO ITHACA ALFRED LAKE ERIE Drive Times Labs FISHKILL BUFFALO COMPANY CITY Toronto, ON, CA 2 Hours Acts Testing Labs, Inc./Bureau Veritas Buffalo New York, NY 6 Hours Ameritech Laboratories College Point Washington DC 7 Hours Bacti-Chem Labs of NY, Inc. Long Island NEW YORK CITY Chicago, IL 8.5 Hours Biotrax Testing Laboratory Cheektowaga SYRACUSE Certified Laboratories, Inc. Melville Montreal, QC, CA 4 Hours Chestnut Labs Ithaca New York, NY 4 Hours Cornell Nutrient Analysis Laboratory Ithaca Philadelphia, PA 4 Hours Dairy One Ithaca ATLANTIC OCEAN Washington DC 6 Hours EMSL Analytical, Inc. New York ALBANY FDA Northeast Regional/District Office Buffalo/Rochester/New York Boston, MA 2.5 Hours FDA Northeast Regional/District Office Syracuse/Binghampton/Albany/Jamaica New York, NY 2.5 Hours MICROBAC Cortland Montreal, QC, CA 3.5 Hours NYS Food Laboratory Albany Philadelphia, PA 4 Hours NYSAES- Food Research Lab Geneva harvestny.cce.cornell.edu Supply Chain Assets Food & Beverage Grocery Stores in New York HQ IN NEW YORK HQ OUTSIDE OF NEW YORK SUPERMARKET -

Lidl Expanding to New York with Best Market Purchase

INSIDE TAKING THIS ISSUE STOCK by Jeff Metzger At Capital Markets Day, Ahold Delhaize Reveals Post-Merger Growth Platform Krasdale Celebrates “The merger and integration of Ahold and Delhaize Group have created a 110th At NYC’s Museum strong and efficient platform for growth, while maintaining strong business per- Of Natural History formance and building a culture of success. In an industry that’s undergoing 12 rapid change, fueled by shifting customer behavior and preferences, we will focus on growth by investing in our stores, omnichannel offering and techno- logical capabilities which will enrich the customer experience and increase efficiencies. Ultimately, this will drive growth by making everyday shopping easier, fresher and healthier for our customers.” Those were the words of Ahold Delhaize president and CEO Frans Muller to the investment and business community delivered at the company’s “Leading Wawa’s Mike Sherlock WWW.BEST-MET.COM Together” themed Capital Markets Day held at the Citi Executive Conference Among Those Inducted 20 In SJU ‘Hall Of Honor’ Vol. 74 No. 11 BROKERS ISSUE November 2018 See TAKING STOCK on page 6 Discounter To Convert 27 Stores Next Year Lidl Expanding To New York With Best Market Purchase Lidl, which has struggled since anteed employment opportunities high quality and huge savings for it entered the U.S. 17 months ago, with Lidl following the transition. more shoppers.” is expanding its footprint after an- Team members will be welcomed Fieber, a 10-year Lidl veteran, nouncing it has signed an agree- into positions with Lidl that offer became U.S. CEO in May, replac- ment to acquire 27 Best Market wages and benefits that are equal ing Brendan Proctor who led the AHOLD DELHAIZE HELD ITS CAPITAL MARKETS DAY AT THE CITIBANK Con- stores in New York (26 stores – to or better than what they cur- company’s U.S. -

Economic News & Trends

ECONOMIC NEWS & TRENDS March 3, 2017 ECONOMIC NEWS & TRENDS This nonconfidential edition includes excerpts from articles, studies, and economic research. The content focuses on trends and news during the third and fourth quarters of 2016. This report may be forwarded to others in your agency, the local chamber, and in your community. CONTENTS FIGURES HIGHLIGHTS. PAGE 2 FIGURE 1. GDP CHANGES OVER QUARTERS (2013–2016), PAGE 3 Section 1. U.S. ECONOMY, PAGE 3 FIGURE 2. UNEMPLOYMENT FOR 4Q2016, PAGE 5 Section 2. U.S. AUTO REPORT, PAGE 7 TABLES Section 3. TEXAS ECONOMY, PAGE 7 TABLE 1. PERCENT CHANGES IN CPI FOR ALL URBAN CONSUMERS 2016, PAGE 4 Section 4. RETAIL AND E-COMMERCE SALES AND TRENDS, PAGE 9 TABLE 2. U.S. HOUSING MARKET INDICATORS FOR 4Q2016, PAGE 5 Section 5. RESTAURANT NEWS AND SUPERMARKET TRENDS, PAGE 10 TABLE 3. ESTIMATED QUARTERLY REVENUE FOR SELECTED SERVICES FOR EMPLOYER FIRMS, NOT SEASONALLY ADJUSTED FROM 3Q2016 TO Section 6. SELECTED REGIONAL REPORT, PAGE 12 4Q2016, PAGE 6 CLIENT TEAM, PAGE 12 TABLE 4. TEXAS HOUSING MARKET INDICATORS FOR 4Q2016, PAGE 8 TABLE 5. U.S RESTAURANT EXPANSION 2016, PAGE 11 For more information about MuniServices, visit: www.MuniServices.com or contact us at [email protected]. ECONOMIC NEWS & TRENDS March 3, 2017 HIGHLIGHTS U.S. GDP: Real gross domestic product (GDP) increased at U.S. median home sales price: In 4Q2016, the median asking an annual rate of 1.9 percent in 4Q2016, according to the sales price for vacant-for-sale units was $167,700. New “advance” estimate released by the Bureau of Economic vehicles: U.S. -

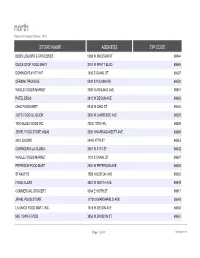

Store Name Address Zip Code

north Based on Grocery Stores - 2013 STORE NAME ADDRESS ZIP CODE BOB'S LIQUORS & GROCERIES 5069 W MADISON ST 60644 QUICK STOP FOOD MART 2751 W PRATT BLVD 60645 DOMINICK'S #147/1147 1340 S CANAL ST 60607 CERMAK PRODUCE 5220 S PULASKI RD 60632 WHOLE FOODS MARKET 3300 N ASHLAND AVE 60657 PATEL BROS 2610 W DEVON AVE 60659 OHIO FOOD MART 5345 W OHIO ST 60644 JOE'S FOOD & LIQUOR 3626 W LAWRENCE AVE 60625 TWO BLUE FOODS INC 702 E 100TH PL 60628 JEWEL FOOD STORE #3349 2520 N NARRAGANSETT AVE 60639 200 LIQUORS 204 E 47TH ST 60653 CARNICERIA LA GLORIA 2551 W 51ST ST 60632 WHOLE FOODS MARKET 1101 S CANAL ST 60607 PETERSON FOOD MART 2534 W PETERSON AVE 60659 STANLEY'S 1558 N ELSTON AVE 60622 FOOD 4 LESS 4821 W NORTH AVE 60639 COMMERCIAL GROCERY 3004 E 100TH ST 60617 JEWEL FOOD STORE 11730 S MARSHFIELD AVE 60643 LA UNICA FOOD MART, INC. 1515 W DEVON AVE 60660 MID TOWN FOODS 3855 W DIVISION ST 60651 Page 1 of 50 09/26/2021 north Based on Grocery Stores - 2013 WARD 28 50 2 23 44 50 37 39 8 36 3 14 2 50 32 37 10 34 40 27 Page 2 of 50 09/26/2021 north Based on Grocery Stores - 2013 7400 S HALSTED FOOD AND LIQUORS, INC. 7400 S HALSTED ST 60621 THREE BROTHER 900 N FRANCISCO AVE 60622 CUENCA'S BAKERY & GROCERIES 4229 W MONTROSE AVE 60641 JEWEL FOOD STORES #3262 4660 W IRVING PARK RD 60641 ROMAN BROS 1 INC 6978 N CLARK ST 60626 TAI NAM CORPORATION 4925 N BROADWAY 60640 LA JALISCIENCE 3239 W 26TH ST 60623 HOLLYWOOD TOWER MKT 5701 N SHERIDAN RD 60660 A & R FOOD MART 5952 W GRAND AVE 60639 S. -

1215 Lexington Ave Flyer.Indd

FOR SALE 1215 LEXINGTON AVE 1215 LEXINGTON AVE | NEW YORK, NY rd Streets nd & 83 Between 82 DAVID SINGER Sales Associate [email protected] (212) 257-5061 SPACE DETAILS East block between 82nd & 83rd Streets 475 sf ground fl oor 475 sf basement 15 ft frontage 10 ft ceilings Current Rent: Upon request Asking Key $: Upon request HIGHLIGHTS Great quick service restaurant opportunity located in one of Manhattans most affl uent residential neighborhoods with an average household income of $192K within a 1/4 mile Close proximity to Hunter College, Lenox Hill, New York-Presbyterian, Cornell Medical Center, Memorial Sloan Kettering Cancer Center and Hospitals Daytime population with 155,000 employees within a 1/2 mile Nearby Metro Stations New installation DEMOGRAPHICS .25 MILES .50 MILES .75 MILES Type 1 venting POPULATION 22,660 92,407 174,819 Currently operating as Portu Grill HOUSEHOLDS 12,201 53,191 100,613 Co-Tenants: Sugaring NC, Warby Parker,Sabas Pizza, Chaise Fitness, HL Purdy Inc. Opticians, Diva Nail Salon, DAYTIME EMPLOYEES 13,095 50,661 76,589 Joe & The Juice, Pressed Juicery, Starbucks, and Oren’s Daily AVERAGE HH INCOME $308,718 $247,233 $232,458 Roast 1215 LEXINGTON AVE HIGHLIGHTS | PROPERTY NEW YORK, NY katzassociates.com 2 AVAILABLE Unit: Square Footage Ground 475 Basement 475 1215 LEXINGTON AVE PLAN | SITE NEW YORK, NY katzassociates.com 3 Food Liberation alice + olivia Dalton School US Postal Service Morton Williams Gristedes Natalia Delizia 92 Zigzag Jewelry Supermarkets T-Mobile Kings Pharmacy Baskin-Robbins Reif’s Bar -

Incorporating Food Systems in Planning

Incorporating Food Systems into Planning Matthew Potteiger Landscape Architecture SUNY College of Environmental Science and Forestry Evan Weissman Public Health, Food Studies & Nutrition Syracuse University Scope: __ Purposes for food system planning __ Precedents and current practice __ FoodPlanCNY Project Overview __ Approaches to food system planning – assessment, engagement __ Challenges and Opportunities Increased public awareness around food and food issues The food system: A stranger to the planning field Kameshwari Pothukuchi; Jerome L Kaufman American Planning Association. Journal of the American Planning Association; Spring 2000; 66, 2; ABI/INFORM Global pg. 113 Why? Perception that there is not a problem markets full of produce “Food is Reproducedan agricultural with permission of the copyright issue owner. notFurther reproductionurban” prohibited without permission. “What can planners do? Who can we collaborate with?” “Where’s the funding?” Reproduced with permission of the copyright owner. Further reproduction prohibited without permission. Emerging Practice: Over the past decade, the food system has enjoyed increased attention from planners and policy makers. Scholars, activists, practitioners, planners, and policy makers engage in various efforts to assess the environmental, economic, and social (including public health) impacts of the food system and used planning to strengthen the food system (Clancy 2004; Jacobson 2008; Freedgood, et al 2011; Meter 2010, 2011; Pothukuchi & Kaufman 1999, 2007). Why do food system planning? The market alone is not working -- social, health and environmental externalities -- concentration and lack of transparency Planners have skills and stake in the food system -- land use, spatial, multi-sectoral/systems thinking Effective means of addressing economic, public health, and environmental imperatives Opportunities to have positive local impacts in relation to globalized system Recognition of opportunities .