25 September 2020 the Manager Market Announcements Office

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TPG Telecom Limited and Its Controlled Entities ABN 46 093 058 069

TPG Telecom Limited and its controlled entities ABN 46 093 058 069 Annual Report Year ended 31 July 2016 2 TPG Telecom Limited and its controlled entities Annual report For the year ended 31 July 2016 Contents Page Chairman’s letter 3 Directors’ report 5 Lead auditor’s independence declaration 34 Consolidated income statement 35 Consolidated statement of comprehensive income 36 Consolidated statement of financial position 37 Consolidated statement of changes in equity 38 Consolidated statement of cash flows 39 Notes to the consolidated financial statements 40 Directors’ declaration 91 Independent auditor’s report 92 ASX additional information 94 3 TPG Telecom Limited and its controlled entities Chairman’s letter For the year ended 31 July 2016 Dear Shareholders On behalf of the Board of Directors, I am pleased to present to you the TPG Telecom Limited Annual Report for the financial year ended 31 July 2016 (“FY16”). Financial Performance FY16 was another successful year for the Group. Continued organic growth and the integration of iiNet into the business have resulted in further increases in revenue, profits and dividends for shareholders. FY16 represents the eighth consecutive year that this has been the case. A detailed review of the Group’s operating and financial performance for the year is provided in the Operating and Financial Review section of the Directors’ Report starting on page 7 of this Annual Report, and set out below are some of the key financial highlights and earnings attributable to shareholders from the year. FY16 FY15 Movement Revenue ($m) 2,387.8 1,270.6 +88% EBITDA ($m) 849.4 484.5 +75% NPAT ($m) 379.6 224.1 +69% EPS (cents/share) 45.3 28.2 +61% Dividends (cents/share) 14.5 11.5 +26% iiNet Acquisition At the beginning of FY16 we completed the acquisition of iiNet and consequently there has been significant focus during the year on integrating the businesses to improve the efficiency of the combined organisation. -

2021 NBN Plan Awards Methodology Report

Mozo Experts Choice Awards NBN Plans 2021 This is the third year running that we’ve gathered together countless pieces of information and applied our methodology to find the leading NBN broadband plans in Australia. Product providers don’t pay to be in the running with our awards, and we don’t play favourites. Our judges base their decision on hard-nosed calculations of value to the consumer, using Mozo’s extensive product database and research capacity. We identify the most important features of each product, group each product into like-for-like comparisons, and then calculate which are better value than most or offer market-leading features. This report lists the winners and explains the judging methodology for our 2021 NBN awards. 1 NBN Plans - 2021 Winners Fast (NBN 100) This category assessed Premium plans offering the NBN’s top speeds and no data limits. Accord with Officeworks Super Fast Dodo nbn100 Exetel Premium nbn100 iPrimus Premium Kogan Gold Mate Soul Mates Spintel Premium 100 Tangerine Telecom XXL Speed Boost TPG NBN100 Unlimited Standard Plus (NBN 50) For this category, the judges looked at plans for the middle tier NBN speed, with no limit on data usage. Belong Standard Plus Exetel Standard Plus nbn50 iPrimus Standard Plus Kogan Silver Spintel Plus 50 Tangerine Telecom XL Speed Boost 2 Standard (NBN 25) People looking for a more entry level internet service may not need to high speeds of other tiers, and have lower data usage. In this category, plans with a data limit of at least 500GB could qualify, as long as there was a meaningful price benefit. -

Approved Securities List

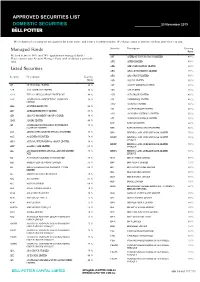

APPROVED SECURITIES LIST DOMESTIC SECURITIES 23 November 2019 The inclusion of a security on our approval list is not advice and is not a recommendation. We change ratios at any time without prior notice to you. Security Description Gearing Managed Funds Ratio We lend between 50% and 70% against most managed funds. APT AFTERPAY TOUCH GROUP LIMITED 40 % Please contact your Account Manager if you wish to discuss a particular fund. APX APPEN LIMITED 40 % Listed Securities ARB ARB CORPORATION LIMITED. 60 % ARG ARGO INVESTMENTS LIMITED 75 % Security Description Gearing ARQ ARQ GROUP LIMITED 50 % Ratio ASB AUSTAL LIMITED 50 % 3PL 3P LEARNING LIMITED.. 40 % AST AUSNET SERVICES LIMITED 65 % A2B A2B AUSTRALIA LIMITED 50 % ASX ASX LIMITED 70 % A2M THE A2 MILK COMPANY LIMITED NZ 40 % AUB AUB GROUP LIMITED 40 % AAC AUSTRALIAN AGRICULTURAL COMPANY 50 % AVJ AVJENNINGS LIMITED 40 % LIMITED. AWC ALUMINA LIMITED 70 % ABA AUSWIDE BANK LTD 40 % AX1 ACCENT GROUP LIMITED 50 % ABC ADELAIDE BRIGHTON LIMITED 65 % AYS AMAYSIM AUSTRALIA LIMITED 50 % ABP ABACUS PROPERTY GROUP STAPLED 50 % AZJ AURIZON HOLDINGS LIMITED 70 % ADH ADAIRS LIMITED 40 % BAP BAPCOR LIMITED 60 % AFI AUSTRALIAN FOUNDATION INVESTMENT 75 % COMPANY LIMITED BBN BABY BUNTING GROUP LIMITED 50 % AGI AINSWORTH GAME TECHNOLOGY LIMITED 55 % BEN BENDIGO AND ADELAIDE BANK LIMITED 70 % AGL AGL ENERGY LIMITED. 70 % BENPE BENDIGO AND ADELAIDE BANK LIMITED 70 % LPYR6UT AHG AUTOMOTIVE HOLDINGS GROUP LIMITED. 50 % BENPF BENDIGO AND ADELAIDE BANK LIMITED 70 % AHY ASALEO CARE LIMITED 65 % LPYR6UT AIA AUCKLAND INTERNATIONAL AIRPORT LIMITED 70 % BENPG BENDIGO AND ADELAIDE BANK LIMITED 70 % NZX LPYR3UT ALF AUSTRALIAN LEADERS FUND LIMITED 50 % BGA BEGA CHEESE LIMITED 60 % ALG ARDENT LEISURE GROUP LIMITED 55 % BHP BHP GROUP LIMITED 75 % ALI ARGO GLOBAL LISTED INFRASTRUCTURE 60 % BIN BINGO INDUSTRIES LIMITED 50 % LIMITED BKL BLACKMORES LIMITED 60 % ALL ARISTOCRAT LEISURE LIMITED 70 % BKW BRICKWORKS LIMITED 60 % ALQ ALS LIMITED 65 % BLD BORAL LIMITED. -

Quarterly Investment Update Antares High Growth Shares Fund – June 2021

Quarterly Investment Update Antares High Growth Shares Fund – June 2021 For adviser use only Highlights for the quarter Performance: The Fund returned 9.6% (net of fees) for the June quarter, outperforming its benchmark by 1.3%. Contributors to performance: Positive contributors – Aristocrat Leisure, Telix Pharmaceuticals, Megaport, Boral, Woodside (not owned); Negative contributors – Incitec Pivot, Qantas, ANZ, Resmed (not owned) and Altium (not owned). Stock activity: Buys/additions – Ansell, Downer and TPG Telecom ; Sells/reductions – BlueScope Steel, Boral, Endeavour Group and Worley Fund snapshot Inception date 7 December 1999 Benchmark S&P/ASX 200 Total Return Index To outperform the benchmark (after fees) over rolling Investment objective 5-year periods Investment returns as at 30 June 20211 Period 3 months 1 year 3 years pa 5 years pa 10 years pa Since inception pa Net return2 % 9.6 39.9 9.2 12.6 10.0 11.0 Gross return3 % 9.9 41.9 10.5 13.9 11.2 12.5 Benchmark return % 8.3 27.8 9.6 11.2 9.3 8.5 Net excess return % 1.3 12.1 -0.4 1.4 0.7 2.5 Gross excess return % 1.6 14.1 0.9 2.7 1.9 4.0 1 Past performance is not a reliable indicator of future performance. Returns are not guaranteed and actual returns may vary from any target returns described in this document. 2 Investment returns are based on exit prices, and are net of management fees and assume reinvestment of all distributions. Contributors to performance Pleasingly the Fund enjoyed another strong quarter, returning 9.6% (net of fees) vs the benchmark return of 8.3%. -

Bringing the Future Faster

6mm hinge Bringing the future faster. Annual Report 2019 WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Bringing the future faster Spark New Zealand Annual Report 2019 Bringing the future faster Contents Build customer intimacy We need to understand BRINGING THE FUTURE FASTER and anticipate the needs of New Zealanders, and Spark performance snapshot 4 technology enables us Chair and CEO review 6 to apply these insights Our purpose and strategy 10 to every interaction, Our performance 12 helping us serve our Our customers 14 customers better. Our products and technology 18 Read more pages 7 and 14. Our people 20 Our environmental impact 22 Our community involvement 24 Our Board 26 Our Leadership Squad 30 Our governance and risk management 32 Our suppliers 33 Leadership and Board remuneration 34 FINANCIAL STATEMENTS Financial statements 38 Notes to the financial statements 44 Independent auditor’s report 90 OTHER INFORMATION Corporate governance disclosures 95 Managing risk framework roles and 106 responsibilities Materiality assessment 107 Stakeholder engagement 108 Global Reporting Initiative (GRI) content 109 index Glossary 112 Contact details 113 This report is dated 21 August 2019 and is signed on behalf of the Board of Spark New Zealand Limited by Justine Smyth, Chair and Charles Sitch, Chair, Audit and Risk Management Committee. Justine Smyth Key Dates Annual Meeting 7 November 2019 Chair FY20 half-year results announcement 19 February 2020 FY20 year-end results announcement 26 August 2020 Charles Sitch Chair Audit and Risk Management Committee WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Create New Zealand’s premier sports streaming business Spark Sport is revolutionising how New Zealanders watch their favourite sports events. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ASX/Media Release

ASX/Media Release 29 March 2017 Sale of Investment in Macquarie Telecom Group Vocus Group Limited (ASX: VOC, ‘Vocus’) today announces that it has disposed of 3,358,511 shares representing ~16% relevant interest in the ordinary shares of Macquarie Telecom Group Limited (ASX: MAQ). The shares were held via a total return swap as described in the FY16 Vocus financial statements. Attached is the Form 605 Notice of ceasing to be a substantial holder. ENDS For further information please contact: Kelly Hibbins Investor Relations Debra Mansfield Corporate Communications P: +61 2 8316 9856 P: +61 3 9674 6569 M: +61 414 609 192 E: [email protected] E: [email protected] About Vocus: Vocus Group (ASX: VOC) is a vertically integrated telecommunications provider, operating in the Australian and New Zealand markets. The Company owns an extensive national infrastructure network of metro and back haul fibre connecting all capital cities and most regional centres across Australia and New Zealand. Vocus infrastructure now connects directly to more than 5,500 buildings. Vocus owns a portfolio of brands catering to corporate, small business, government and residential customers across Australia and New Zealand. Vocus also operates in the wholesale market providing high performance, high availability and highly scalable communications solutions which allow service providers to quickly and easily deploy new services for their own customer base. For more information please go to our website www.vocusgroup.com.au. VOCUSGROUP.COM.AU 605 page 1/2 15 July 2001 Form 605 Corporations Act 2001 Section 671B Notice of ceasing to be a substantial holder To Company Name/Scheme ACN/ARSN 1. -

TIO Quarter One 2020 Complaints Report.Pdf

Quarterly report Quarter 1 Financial year 2020 Complaints total complaints 32,801 referred to providers Internet services were the most Top 5 issues complained about service type No or delayed action by provider 11.5k Service and equipment fees 15,925 48.6% 10.5k fault and connection of total complaints complaints Delay establishing a service 4.6k Providers No phone or internet service 4.2k of providers had a complaint in Q1 13.6% Resolution agreed but not met 3.6k of total complaints came from the top 10 providers 92.9% 0 12k Enquiries Who complained residential 86% consumers 13,030 enquiries 14% small business consumers Dispute resolution Contacts complaints came back Online Calls 5,420 unresolved from providers unresolved complaints 47.9k 40k were escalated for 4,225 dispute resolution Contacts and complaints Contacts Q1 40,010 4 7,9 1 8 19-20 Q4 39,482 45,914 18-19 Q3 18-19 39,477 48,213 Q2 18-19 35,900 41,486 Q1 Calls 40,485 42,154 18-19 Online 0 20k 40k 60k 80k 100k Complaints Q1 32,801 19-20 Q4 33,894 18-19 Q3 37,599 18-19 Q2 18-19 30,035 Q1 30,859 18-19 0 5k 10k 15k 20k 25k 30k 35k 40k Enquiries Q1 13,030 19-20 Q4 11,989 18-19 Q3 18-19 12,984 Q2 18-19 11,843 Q1 12,538 18-19 0 3k 6k 9k 12k 15k Quarter 1 Report 2019-20 2. Complaints by service type Complaints by service type Q1 10,657 (33%) 4,398 (13%) 9,968 (30%) 7,395 (23%) 383 (1%) 19-20 Q4 18-19 11,575 (34%) 4,763 (14%) 9,533 (28%) 7, 62 1 (23%) 402 (1%) Q3 18-19 12,969 (35%) 4,812 (13%) 10,682 (28%) 8,841 (24%) 295 (1%) Q2 9,621 (32%) 3,862 (13%) 9,583 (32%) 6,734 (22%) 235 -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Australian Equity Microcap Insights

UBS Asset Management For professional / qualified / institutional investors only. May 2020 Australian Equity Microcap Insights Opportunities abound in Microcap space As the economy moves into the post COVID-19 recovery phase, UBS Microcap Fund Portfolio Manager Joel Fleming expects microcap companies to be an important contributor to the recovery, Joel Fleming with many smaller firms driving high levels Portfolio Manager Yarra Capital Management of growth as they take advantage of the lasting changes caused by the pandemic. There are a large number of common misconceptions Microcap recap about the contribution made by Australia’s smaller firms to Microcaps offer the largest investable universe by number the domestic economy. Some of Joels’s favourites include: on the ASX. With no ETF or passive products, a more constrained liquidity profile compared to large caps, and a • “Micro companies are largely in retail and service vast investable universe, Microcap investing is all about sectors and employ relatively few people in active management. comparison to larger firms” The index represents opportunity, with many examples of • “Micro and small companies tend to not be profitable. companies that have delivered on an idea and transitioned Profits in Australia are driven by large firms in the into the sphere of Australia’s Top 100 listed companies. mining, banks, supermarket and health care sectors” Think Afterpay, A2 Milk, Domino’s Pizza or TPG Telecom. • “Micro companies pay small dividends and have low While much of the universe will deliver poor returns, operating margins. Investing in the space is all about despite the hype and promise, the success stories can capital growth” deliver many multiples of an initial investment. -

Stoxx® Australia 150 Index

STOXX® AUSTRALIA 150 INDEX Components1 Company Supersector Country Weight (%) Commonwealth Bank of Australia Banks Australia 8.37 CSL Ltd. Health Care Australia 7.46 BHP GROUP LTD. Basic Resources Australia 7.23 National Australia Bank Ltd. Banks Australia 4.37 Westpac Banking Corp. Banks Australia 4.09 Australia & New Zealand Bankin Banks Australia 3.75 Wesfarmers Ltd. Retail Australia 3.30 WOOLWORTHS GROUP Personal Care, Drug & Grocery Australia 2.87 Macquarie Group Ltd. Financial Services Australia 2.84 Rio Tinto Ltd. Basic Resources Australia 2.48 Fortescue Metals Group Ltd. Basic Resources Australia 2.27 Transurban Group Industrial Goods & Services Australia 2.20 Telstra Corp. Ltd. Telecommunications Australia 2.05 Goodman Group Real Estate Australia 1.77 AFTERPAY Industrial Goods & Services Australia 1.54 Coles Group Personal Care, Drug & Grocery Australia 1.39 Woodside Petroleum Ltd. Energy Australia 1.28 Newcrest Mining Ltd. Basic Resources Australia 1.27 Aristocrat Leisure Ltd. Travel & Leisure Australia 1.11 XERO Technology Australia 1.00 SYDNEY AIRPORT Industrial Goods & Services Australia 0.93 Brambles Ltd. Industrial Goods & Services Australia 0.91 Sonic Healthcare Ltd. Health Care Australia 0.90 ASX Ltd. Financial Services Australia 0.82 SCENTRE GROUP Real Estate Australia 0.80 Cochlear Ltd. Health Care Australia 0.74 QBE Insurance Group Ltd. Insurance Australia 0.73 SUNCORP GROUP LTD. Insurance Australia 0.71 South32 Australia Basic Resources Australia 0.71 Santos Ltd. Energy Australia 0.68 Ramsay Health Care Ltd. Health Care Australia 0.66 Insurance Australia Group Ltd. Insurance Australia 0.65 Mirvac Group Real Estate Australia 0.60 DEXUS Real Estate Australia 0.59 SEEK Ltd. -

ICT Services Contractor Profiles: Category 3 1 February 2016 to 31 March 2021

Contract No: ICTS2015 Last Updated: 20 May 2020 Document number: 01791286 ICT Services Contractor Profiles: Category 3 1 February 2016 to 31 March 2021 CONTRACT MANAGER Email: [email protected] Tel: 08 6551 1375 Government Procurement Department of Finance Optima Centre 16 Parkland Road OSBORNE PARK WA 6017 Contents 4Logic ......................................................................................................................................................... 5 Agile Computing Pty Ltd ............................................................................................................................. 6 agility IT Consulting .................................................................................................................................... 7 Amristar Solutions ...................................................................................................................................... 8 ASG Group Limited .................................................................................................................................... 9 Asterisk Information Security .................................................................................................................... 10 Aurora Consulting Pty Ltd ......................................................................................................................... 11 Avantgarde Technologies ......................................................................................................................... 12